Chapter 4 Types of ProductCosting Systems Process Costing

- Slides: 26

Chapter 4

Types of Product-Costing Systems Process Costing Job-Order Costing • Company produces many units of a single product for a long time • Mass-produced, automated continuous production process. • Costs cannot be directly traced to each unit of product. Process costing allocates costs to products by averaging costs over large numbers of nearly identical products

Types of Product-Costing Systems Process Costing Job-Order Costing Typical process cost applications: v Petrochemical refinery v Paint manufacturer v Paper mill

Types of Product-Costing Systems Process Costing Job-Order Costing F Job-shop operations v Products manufactured in very low volumes or one at a time. F Batch-production operations v Multiple products in batches of relatively small quantity.

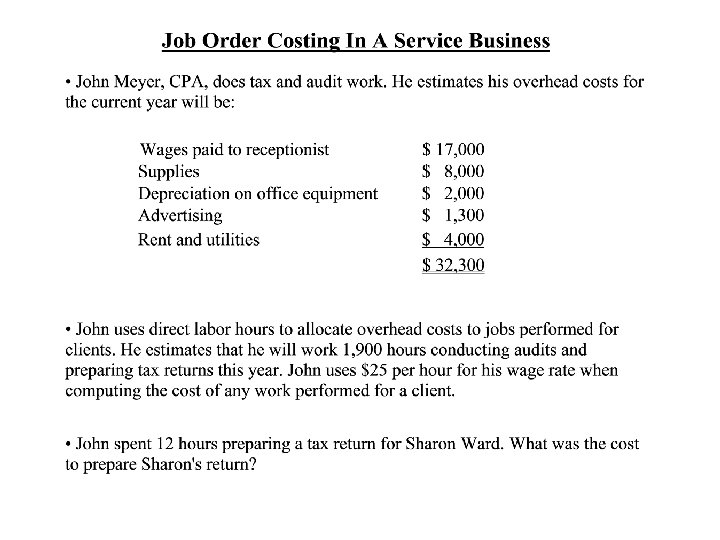

Types of Product-Costing Systems Process Costing Job-Order Costing F Typical job-order cost applications: v Special-order printing v Building construction F Also used in service industry v Hospitals v Law firms

Materials Requisition Form

Employee Time Ticket

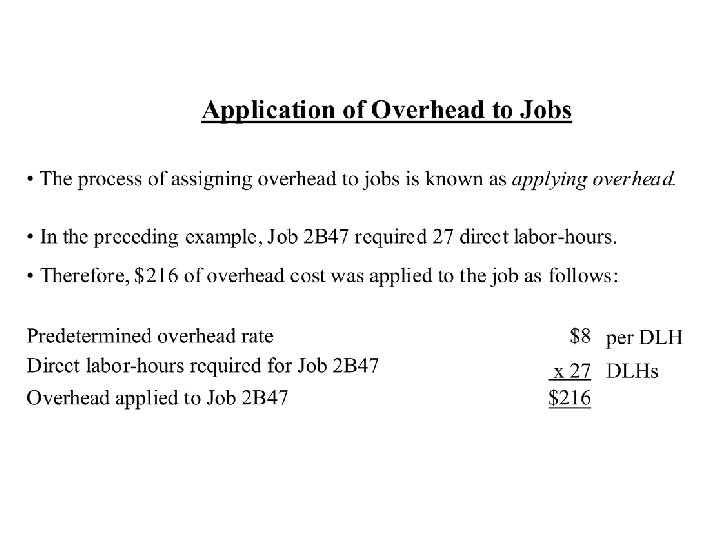

Job Cost Sheet

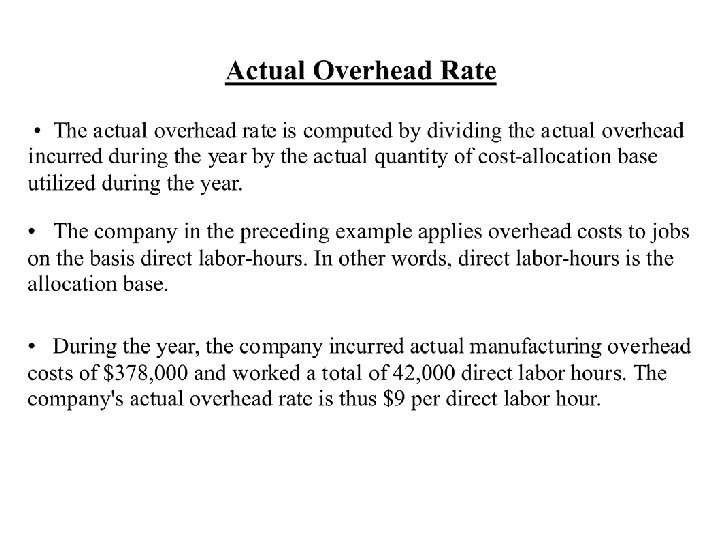

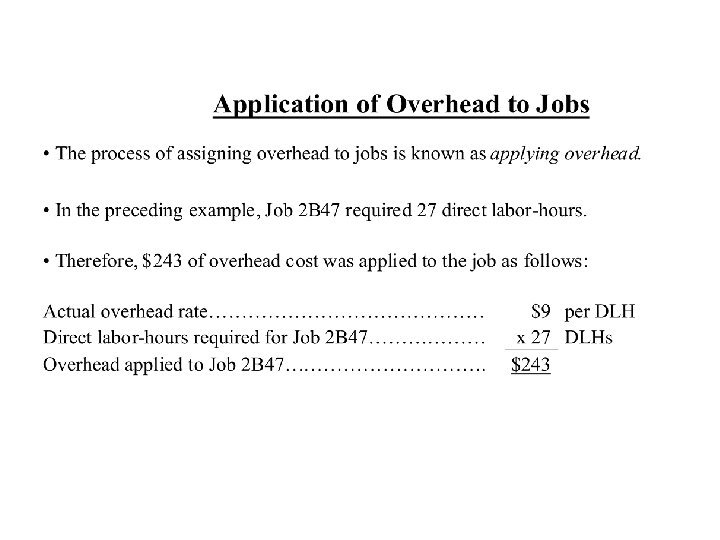

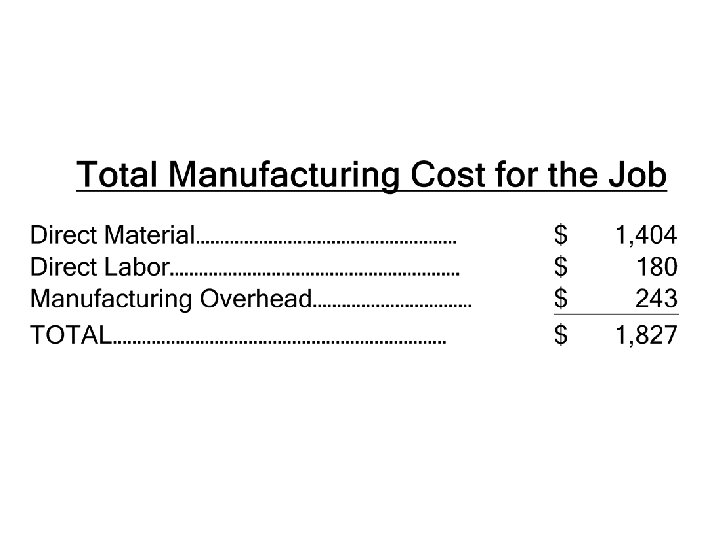

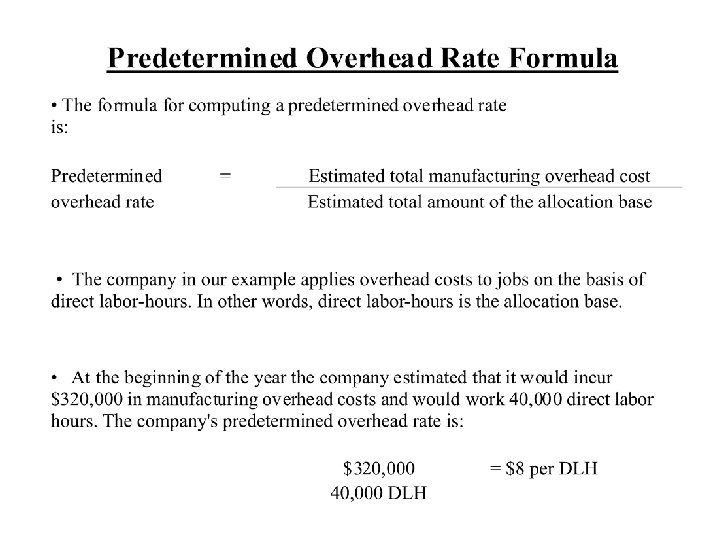

Practice with Overhead Actual manufacturing overhead Budgeted machine hours Budgeted direct labor rate Budgeted manufacturing oh Actual machine hours Actual direct labor rate POHR - Machine hours POHR - direct labor dollars $340, 000 10, 000 20, 000 $14 $364, 000 11, 000 18, 000 $15

Job-Order System Cost Flows Word Documents Fisher Company Journal Entries T-Accounts Over/Under-applied Overhead Cost of Goods Manufactured Cost of Goods Sold Income Statement

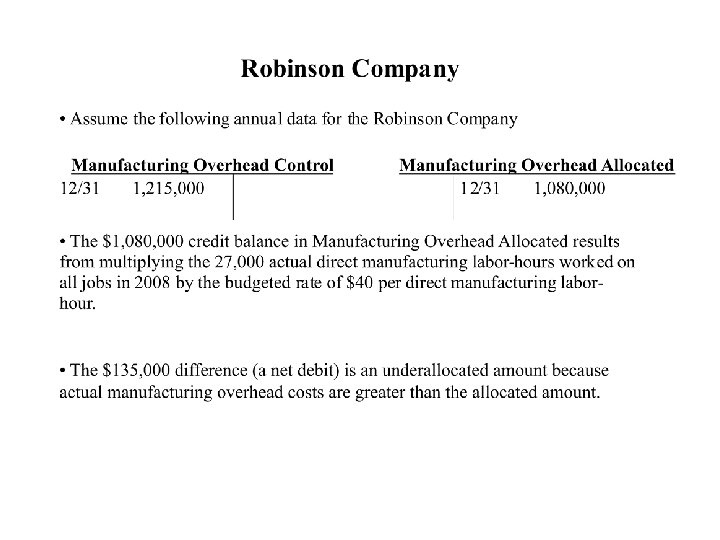

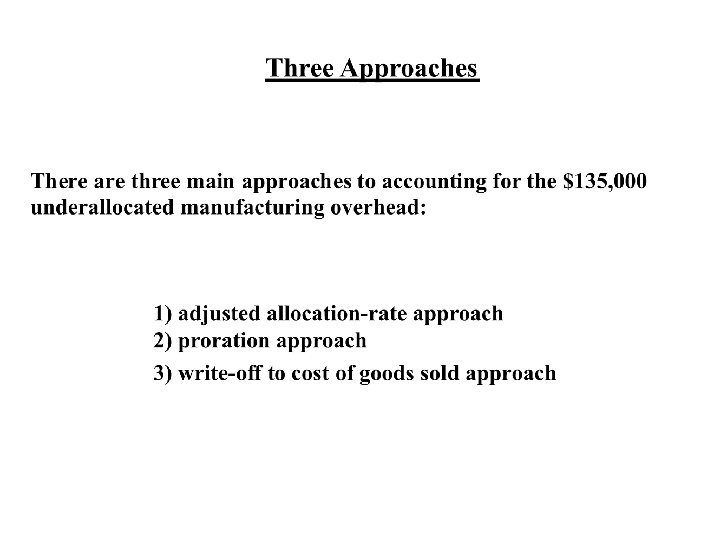

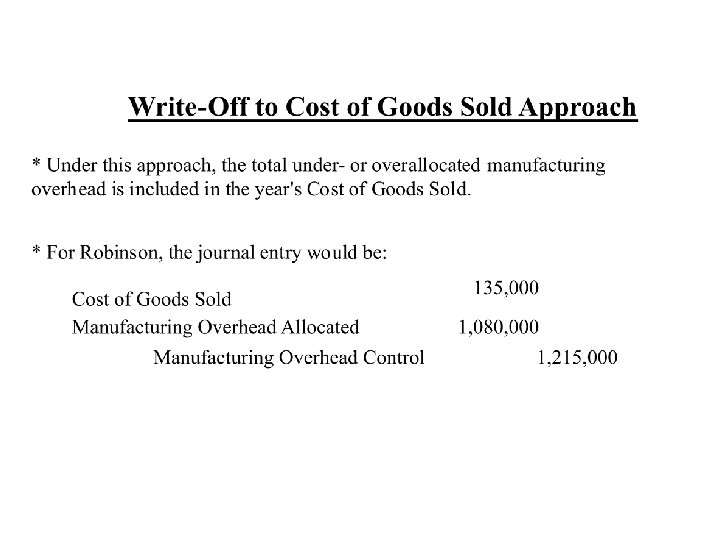

Overapplied and Underapplied Manufacturing Overhead - Summary

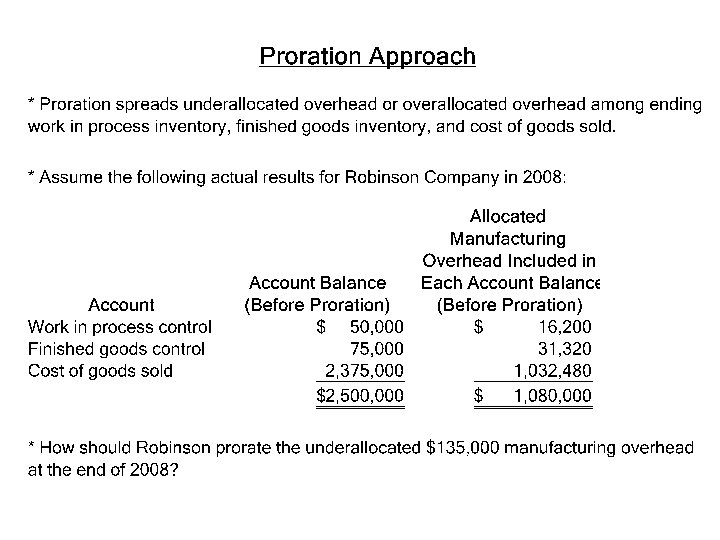

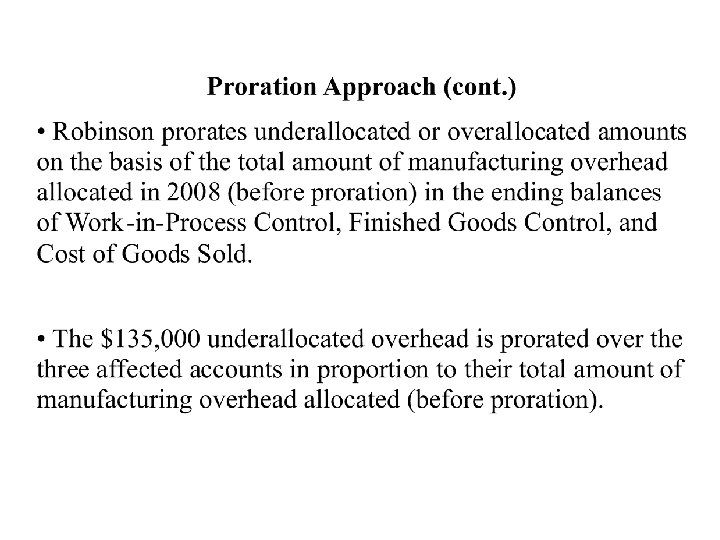

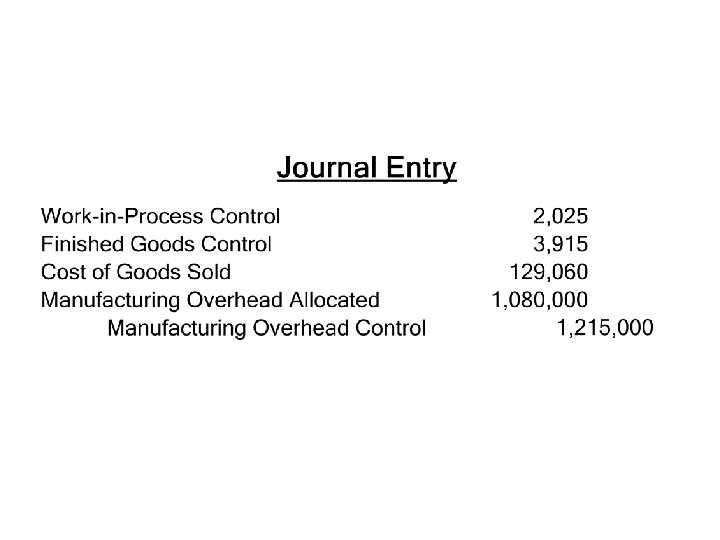

Allocation Account Work in Process control Finished goods control Cost of goods sold Total Account Balance (Before Proration) $ 50, 000 Allocated Manufacturing Overhead Allocated Included in Each Manufacturing Account Balance Overhead Included in Proration of $135, 000 of Underallocated (Before Each Account Balance Proration) as a Percent of Total Manufacturing Overhead 16, 200 1. 50% 0. 015 x $135, 000= 75, 000 31, 320 2. 90% 0. 029 x $135, 000= 3, 915 78, 915 2, 375, 000 1, 032, 480 95. 60% 0. 956 x $135, 000= 129, 060 2, 504, 060 1, 080, 000 100. 00% $135, 000 $2, 635, 000 $2, 500, 000 $ $ $ 2, 025 Account Balance (After Proration) $ 52, 025