Chapter 4 Completing the Accounting Cycle Objectives 1

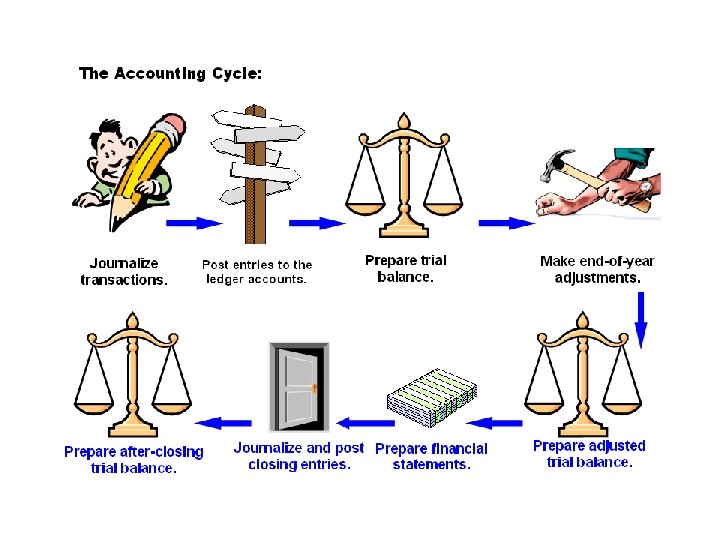

Chapter 4: Completing the Accounting Cycle Objectives 1: Prepare an accounting work sheet. The Accounting Cycle Process by which accountants prepare financial statements for an entity for a specific period of time.

• Objective 2: The Work Sheet: • The Accounting Work Sheet • Used to help move data from the trial balance to the financial statements. • An internal document – not financial statement.

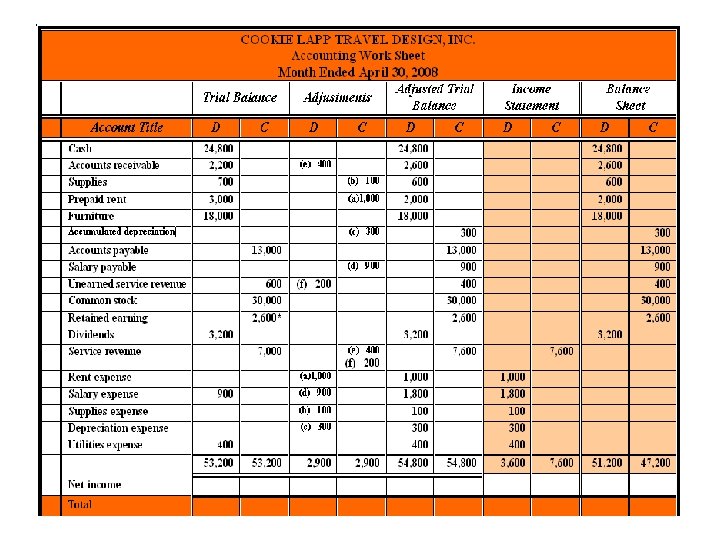

Step 1: Prepare Unadjusted Trial Balance

Step 2: Plan Adjustments (Enter the adjusting entries in the Adjustments columns. Total the accounts).

Step 3: Adjusted Trial Balance (Combine the trial balance and adjustment amounts. Enter the amounts in the Adjusted Trial Balance columns):

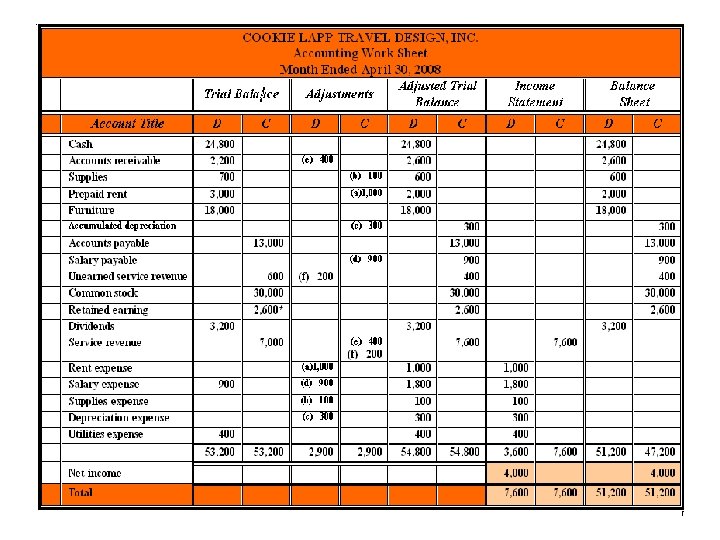

• Step 4: Sort Adjusted Amounts to Statement Columns: • A: Extend asset, liability, and stockholders’ equity amounts to the Balance Sheet columns. Extend the revenue and expense amounts to the Income Statement columns. Total the statement colums.

• B: On the Income Statement, compute net income as total revenues minus total expenses. Enter net income as a balancing amount on the income statement and on the balance sheet. Compute the adjusted column totals.

Recording Adjusting Entries: Work sheet helps identify accounts that need adjustments Actual adjustment of accounts requires journalizing and posting entries • Objective 3: Close the revenue, expense, and withdrawal accounts • • • Closing the Accounts: Prepares accounts for recording transactions during next period Updates retained earnings account Permanent Accounts Temporary Accounts Four Closing Entries: Close all income statement accounts to Income Summary (Notice: Only income statement accounts are closed to income summary). Entry 1: Close revenue accounts to Income Summary Entry 2: Close expense accounts to Income Summary Entry 3: Close Income Summary to Retained Earnings Entry 4: Close Dividends to Retained Earnings

• • • Income Summary Account: Debit balance = Net Loss Credit balance = Net Income Post-Closing Trial Balance: List of permanent accounts and their balances after posting closing entries • Total debits and credits must be equal • Only Balance Sheet accounts remain on the Post-Closing Trial Balance. All other accounts have a -$0 - balance.

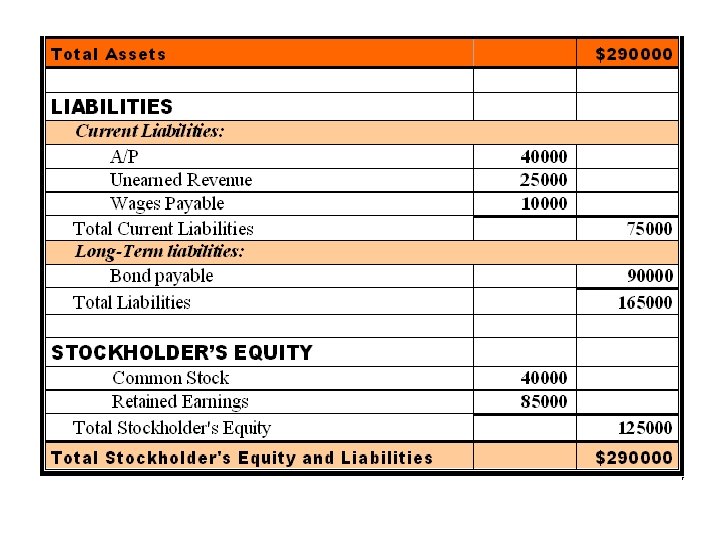

Objective 4: Classify assets and liabilities as current or long-term: • • • Assets and liabilities are classified as either current or long-term to show their relative liquidity. In classified statements, similar items are grouped together to produce subtotals which may assist users in their analysis. Liquidity: Measure of how quickly an item can be converted into cash. On the balance sheet, assets and liabilities are classified as either current or long-term to indicate their relative liquidity. Current Assets: Cash or assets that will be converted to cash or used up, in one year or within normal business operating cycle. Examples: – Short-term receivables. – Inventory. – Prepaid expenses. Current Liabilities: Debts or obligations due within one year or within operating cycle. Examples: – Accounts and salary payables. – Short-term notes payable. – Unearned revenue.

• Long-term Assets and Liabilities: • Long-term assets - all other assets: – Property, equipment. – Intangibles. • Long-term liabilities - all other debts due in longer than one year or entity’s operating cycle. • Different Formats of the Balance Sheet: • Account Format. • Report Format.

Sample Balance sheet to illustrate the classified balance sheet format, and some typical accounts:

Objective 5: Use the current ratio and the debt ratio to evaluate a company • Comparative Financial Statements • Enhance user’s ability to analyze company’s past performance. • Two common ratios used to measure liquidity: • Current ratio. • Debt ratio. • Current Ratio: • Measures ability of a business to pay its current liabilities with its current assets. The current ratio is computed by dividing total current assets by total current liabilities. It is considered a measure of the short-term debt-paying ability. • Current Ratio = Current assets ÷ Current liabilities.

• Debt Ratio: • Indicates the proportion of a business’s assets that are financed with debt. • The debt ratio is computed by dividing total liabilities by total assets. It is considered a measure of the long-term safety of creditors’ claims, rather than a measure of short -term liquidity. • Measures business’s ability to pay both current and longterm debt. • Debt Ratio = Total liabilities ÷ Total assets.

• • • Requirement: Compute the current ratio. The answer: The current ratio = Current Assets ÷ Current Liabilities The current ratio = 12, 000 ÷ 6, 000 = 2 times. A current ratio of 2 means that the company’s current assets are 2 times as large as its current liabilities. It has 2 dollars of current assets for each dollar of current liabilities.

• • Requirement: Compute the debit ratio. The answer: The debt ratio = Total Liabilities ÷ Total Assets The debt ratio = 15, 000 ÷ 24, 000 = 0. 625.

- Slides: 20