CHAPTER 3 MONEYTIME RELATIONSHIPS AND EQUIVALENCE It is

Where it occurs 2)")

Construct a cash flow diagram for the following cash flows: $25, 000")

Mulia Financing lent an engineering company RM 100, 000 to retrofit an")

- Slides: 30

CHAPTER 3 MONEY-TIME RELATIONSHIPS AND EQUIVALENCE

• It is well known fact that money makes money. • The time value of money explains the change in the amount of money over time for fund that are owned (invested) or owed (borrowed). • This is the most important concept in engineering economy.

WHAT YOU WILL LEARN? • Cash Flow – details – Interest - simple interest, compound interest • Economic equivalence • Money-time relation – Present value (P), Future value (F), Uniform series (Annuity, A)

Cash flow • Define Cash Flow • Discuss General Workflow • Work an Example

Cash flow Cash Flow – A series of expenses and credits that run over the lifetime of a project – transactions Transactions can take place at any point during a project It can be Costs (Expenses, Disbursements, Payments) Receipts (Credits, Revenue)

The cash flow diagram is a very important tool in an economic analysis, especially when the cash flow series is complex. It is graphical representation of cash flows drawn on the y axis with a time scale on the x axis. A vertical arrow pointing up indicates a positive cash flow. Conversely, a down-pointing arrow indicates a negative cash flow. We will use a bold, colored arrow to indicate what is unknown and to be determined.

The purpose to build cash flow diagram… ü To provide information about the cash inflows and outflows of an entity during a period. ü To summarize the operating, investing, and financing activities of the business.

Cash Flow Diagrams What a typical cash flow diagram might look like Draw a time line Always assume end-of-period cash flows 0 n-1 1 One n time Time 2 period Show the cash flows (to scale) … … … F= approximate$100 0 1 2 … … … n-1 Cash flows n are shown as directed arrows: + (up) for P = $80 inflow 1 -8 (down) for outflow - © 2012 by Mc. Graw-Hill, New York, N. Y All Rights Reserved

Cash Flow Diagram

Cash Flow Diagram

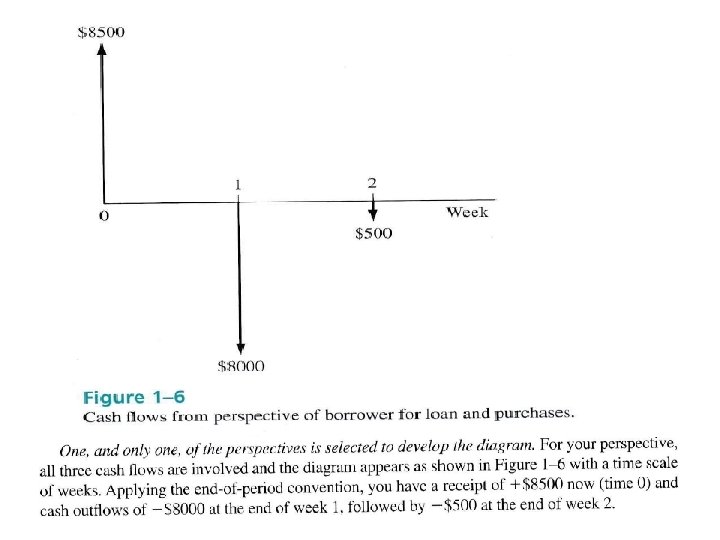

Assume you borrow $8500 from a bank today to purchase an $8000 used car for cash next week, and you plan to spend the remaining $500 on a new paint job for the car two weeks from now. There are several perspectives possible when developing the cash flow diagram – those of the borrower (that’s you), the banker, the car dealer, or the paint shop owner. The cash flow signs and amounts for these perspectives are as follows:

Cash flow- General Workflow • 1 st Step: Identify 1) Where it occurs 2) Expense or credit 3) Magnitude

INTEREST The fee that a borrower pays to a lender for the use of his or her money. INTEREST RATE The percentage of money being borrowed that is paid to the lender on some time basis.

INTEREST “Hurt no one so that no one may hurt you. Remember that you will indeed meet your LORD, and that HE will indeed reckon your deeds. ALLAH has forbidden you to take usury (interest), therefore all interest obligation shall henceforth be waived”. “Janganlah kamu sakiti sesiapapun agar orang lain tidak menyakiti kamu pula. Ingatlah bahawa sesungguhnya kamu akan menemui Tuhan kamu dan Dia pasti akan membuat perhitungan atas segala amalan kamu. Allah telah mengharamkan riba', oleh itu segala urusan yang melibatkan riba' hendaklah dibatalkan mulai sekarang” Muhammad (pbuh), The Farewell Sermon, Mount Arafat (0632)

SIMPLE INTEREST • The total interest earned or charged is linearly proportional to the initial amount of the loan (principal), the interest rate and the number of interest periods for which the principal is committed. • When applied, total interest “I” may be found by I = ( P ) ( N ) ( i ), where – P = principal amount lent or borrowed – N = number of interest periods ( e. g. , years ) – i = interest rate per interest period

INTEREST • You are starting your own small business in Kangar. You borrow $10, 000 from the bank at a 9% rate for 5 years. Find the interest you will pay on this loan. I=Px. Nxi =10, 000 x 5 x 0. 09 = $ 4500

Simple and Compound Interest q Simple Interest is calculated using principal only Interest = (principal)(number of periods)(interest rate) I = Pni Example: $100, 000 lent for 3 years at simple i = 10% per year. What is repayment after 3 years? Interest = 100, 000(3)(0. 10) = $30, 000 © 2012 by Mc. Graw-Hill, New York, N. Y All Rights 1 -20 + 30, 000 Total due = 100, 000 = $130, 000 Reserved

Simple and Compound Interest q Compound Interest is based on principal plus all accrued interest That is, interest compounds over time Interest = (principal + all accrued interest) (interest rate) Interest for time period t is 1 -21 © 2012 by Mc. Graw-Hill, New York, N. Y All Rights Reserved

Simple Interest vs Compound Interest SIMPLE INTEREST The total amount repaid at the end of N interest periods is P + I. Thus, if $1000 were loaned for three years at a simple interest rate of 10% per year, the interest earned would be: I = $1000 x 3 x 0. 10 = $300 The total amount owed at the end of three years would be $1, 000 + $300 = $1, 300. Notice that the cumulative amount of interest owed is a linear function of time until the principal (and interest) is repaid (usually not until the end of period N).

COMPOUND INTEREST • Whenever the interest charge for any interest period is based on the remaining principal amount plus any accumulated interest charges up to the beginning of that period. Period Amount owed Interest at beginning of amount of the period (@10%) Amount owed at the end of the period 1 1, 000 1, 100 2 1, 100 110 1, 210 3 1, 210 121 1, 331

As you can see, a total of $1, 331 would be due for repayment at the end of the third period. If the length of a period is one year, the $1, 331 at the end of three periods (years) can be compared with the $1, 300 given earlier for the same problem with simple interest. A graphical comparison of simple interest and compound interest is given in Figure 4 -1.

The difference is due to the effect of compounding, which is essentially the calculation of interest on previously earned interest. This difference would be much greater for: ü larger amounts of money ü Higher interest rates ü Greater number of interest periods.

• Compound interest is much more common in practice than simple interest

QUIZ 1) Construct a cash flow diagram for the following cash flows: $25, 000 outflow at time 0, $9000 per year inflow in years 1 through 5 at an interest rate of 10% per year, and an unknown future amount in year 5.

QUIZ 2) Mulia Financing lent an engineering company RM 100, 000 to retrofit an environmentally unfriendly building. The loan is for 3 years at 10% per year simple interest. How much money will the firm repay at the end of 3 years?

1: Solution:

2: Solution The interest for each of the 3 years is: Interest per year = RM 100, 000 (0. 10) = RM 10, 000 Total interest for 3 years is: Total interest = RM 100, 000 (3) (0. 10) = RM 30, 000 The amount due after 3 years is: Total due = RM 100, 000 + RM 30, 000 = RM 130, 000