Chapter 3 A Prod Activities Deduct Corporate AMT

![Students should: 1. Understand the basics of the Production Activities Deduction. [Page 1] 2.](https://slidetodoc.com/presentation_image_h2/9d8a298400e8162b4de5dc6e2f1b0b60/image-2.jpg "Students should: 1. Understand the basics of the Production Activities Deduction. [Page 1] 2.")

Allowance of Deduction. (1) In")

Qualified Production Activities Income For purposes of this section (1) In general. The")

Domestic production gross receipts. (A) In general. The term \"domestic production gross receipts\"")

equals the entire AMT amount paid.")

with unused minimum tax")

Local has regular taxable income of $100, 000. Tax")

• Dad started a")

• C Corp. will owe AMT (ACE")

is to show our earlier")

- Slides: 78

Chapter 3 A. Prod. Activities Deduct. Corporate AMT Howard Godfrey, Ph. D. , CPA Professor of Accounting Copyright © Howard Godfrey, 2014 Edited January 10, 2014 C 13 -Chp-03 -1 A-AMT-2014

Students should: 1. Understand the basics of the Production Activities Deduction. [Page 1] 2. Understand the purpose of the AMT and its focus on timing of benefits. [Page 16] 3. Understand the AMT formula. [Page 17] 4. Understand the exemption from AMT for small corporations. [Page 17] 5. Understand nature of AMT adjustments & why they may be positive or negative. [Page 18] 6. Understand how different AMT depreciation methods cause different asset basis amounts, and multiple amounts of gain on sale of assets. [Page 19]

Students should be: 7. Understand how to make appropriate adjustments where taxpayer uses the completed contract method for long-term construction contracts. [Page 19] 8. Understand how to report preferences. [Page 20] 9. Be able to properly report the ACE adjustment. [Page 21] 10. Compute the AMT exemption [Page 24] 11. Understand the AMT Credit [Page 25] 12. Complete the process by computing the amount of AMT and the AMT credit.

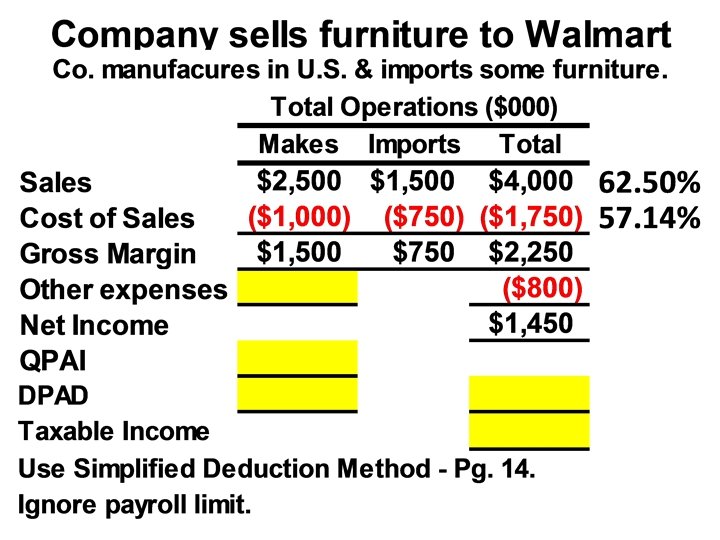

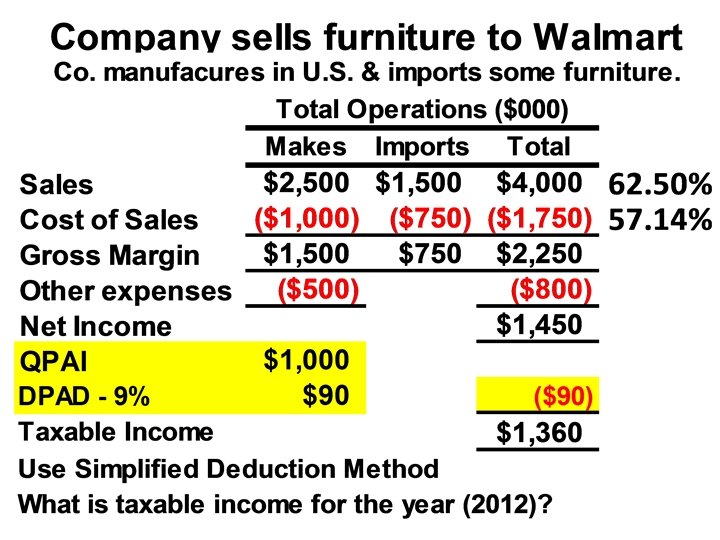

U. S. Production Activities Deduction. Corporations are allowed a U. S. production activities deduction equal to a percentage times the lesser of: (1) qualified production activities income or (2) taxable income before the U. S. production activities deduction. For 2005 -2006 the percentage was 3%; 20072009 it is 6%; and, 2010 and thereafter it is 9%. The deduction cannot exceed 50% of the W-2 wages for the year. The effect - lowering marginal tax bracket about 3%.

Qualified production activities income includes gross receipts from domestic production reduced by cost of goods sold, directly allocable expenses and a ratable portion of other deductions not directly allocable. Domestic production gross receipts include receipts from the lease, rental, license, sale, exchange, or other disposition of qualified production property manufactured, produced, grown, or extracted in whole or significant part within the United States, qualified film production, or electricity, natural gas, or potable water produced within the United States. 5

It also includes construction performed in the U. S. & engineering or architectural services performed in the United States for construction of projects in the United States. Domestic production gross receipts do not include receipts from the sale of food & beverages the taxpayer prepares at a retail establishment and do not apply to the transmission of electricity, natural gas, or potable water. 6

Please study the shaded areas of section 199 in the file for the section that is posted on the website. C 14 -Chp-03 -3 -Section-199 -Prod -Activities-Ded Part of that material is also included in following slides. 7

Sec. 199. INCOME ATTRIBUTABLE TO DOMESTIC PRODUCTION ACTIVITIES (a) Allowance of Deduction. (1) In general. There shall be allowed as a deduction an amount equal to 9 percent of the lesser of (A) the qualified production activities income of the taxpayer for the taxable year, or (B) taxable income (determined without regard to this section) for the taxable year. 8

(c) Qualified Production Activities Income For purposes of this section (1) In general. The term "qualified production activities income" for any taxable year means an amount equal to the excess (if any) of(A) the taxpayer's domestic production gross receipts for such taxable year, over (B) the sum of(i) the cost of goods sold that are allocable to such receipts, and (ii) other expenses, losses, or deductions (other than the deduction allowed under this section), which are properly allocable to such receipts. 9

(4) Domestic production gross receipts. (A) In general. The term "domestic production gross receipts" means the gross receipts of the taxpayer which are derived from (i) any lease, rental, license, sale, exchange, or other disposition of(I) qualifying production property which was manufactured, produced, grown, or extracted by the taxpayer in whole or in significant part within the United States, … 10

Campbell Corporation's taxable income for 2013 before the domestic production activities deduction was $25, 000. Its taxable income from qualified production activities in 2013 was $10, 000. Campbell Corporation's W-2 wages allocable to qualified production activities for 2013 were $8, 000. What is Campbell Corporation's taxable income for 2013? a. $21, 000 b. $24, 100, 000 c. $23, 500, 000 d. $24, 250, 000 13

Answer. b. Campbell Corporation's domestic production activities deduction is $900, 000 (9% × lesser of): (1) $25, 000 or (2) $10, 000. Deduction cannot exceed 50% × W-2 wages for qualified production activities: (50% × $8, 000 = $4, 000). Thus, its taxable income is $24, 100, 000 ($25, 000 - $900, 000). 14

AMT Students should have a copy of AMT-Code-Outline. xls Which is included in the lecture handout materials 15

16

17

Background on AMT Congress was concerned that corporations were not paying enough income tax because of 1. Having income that is tax-free 2. Deferring income to a later period 3. Taking large deductions currently that could be deferred 4. Etc.

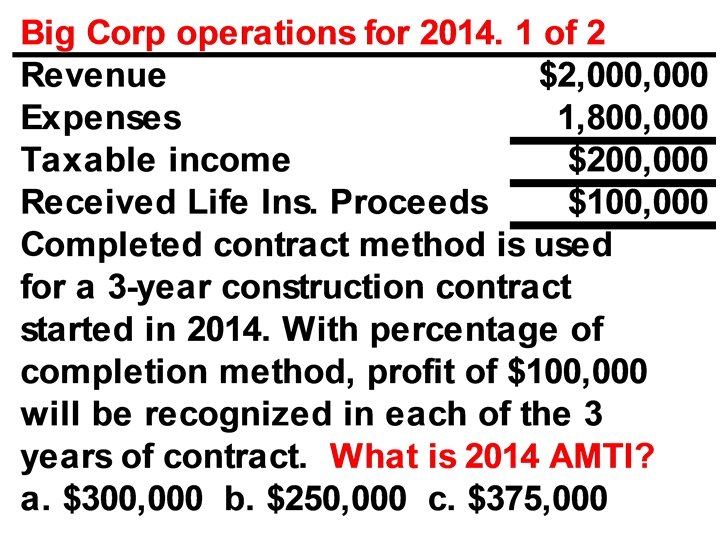

Background on AMT Some solutions in the AMT, which is a separate tax (an additional income tax). 1. Compute AMT by including some income (that is tax-exempt --not included in regular tax computations). 2. Compute AMT by including some income in AMT tax base this period (that is otherwise deferred to a future period in regular tax computations [long-term contracts]). 3. Compute AMT by deferring recognition of expenses to future periods (that are deducted currently in regular tax computations. [depreciation]).

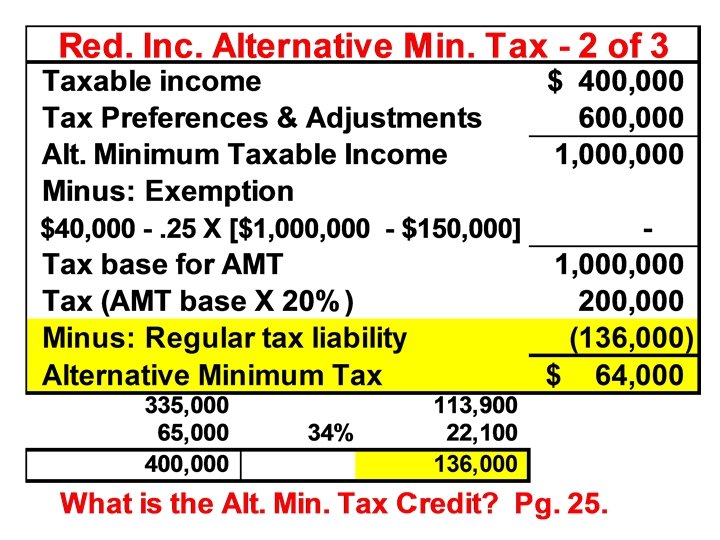

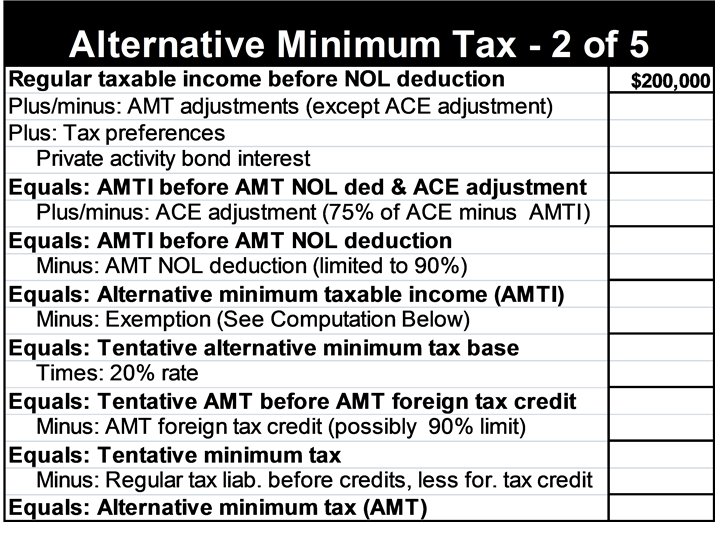

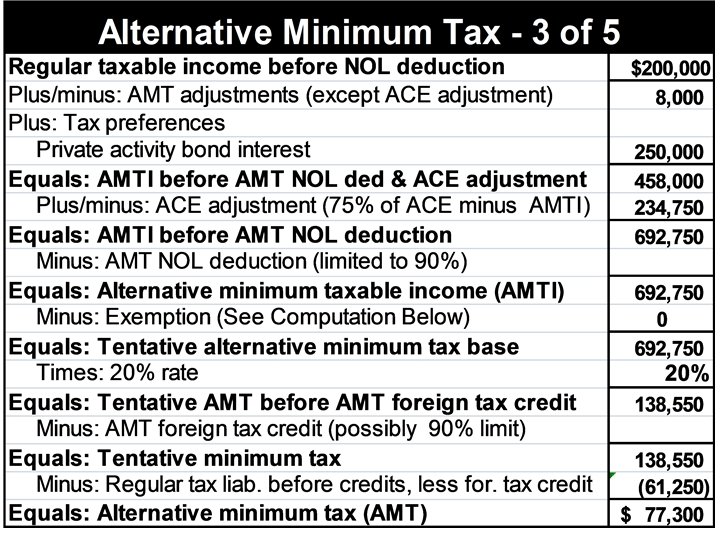

AMT Formula - 1 If a corporation's tentative minimum tax exceeds the regular tax, the excess amount is a. Subtracted from the regular tax. b. Payable in addition to the regular tax. c. Carried back to the third preceding taxable year. d. Carried back to the first preceding taxable year. (CPA-May-1990) 20

AMT Formula - 2 If a corporation's tentative minimum tax exceeds the regular tax, the excess amount is b. Payable in addition to the regular tax. See Sec. 55(a) C 12 -Chp-03 -3 -AMT-Code-Outline. xls 21

22

23

24

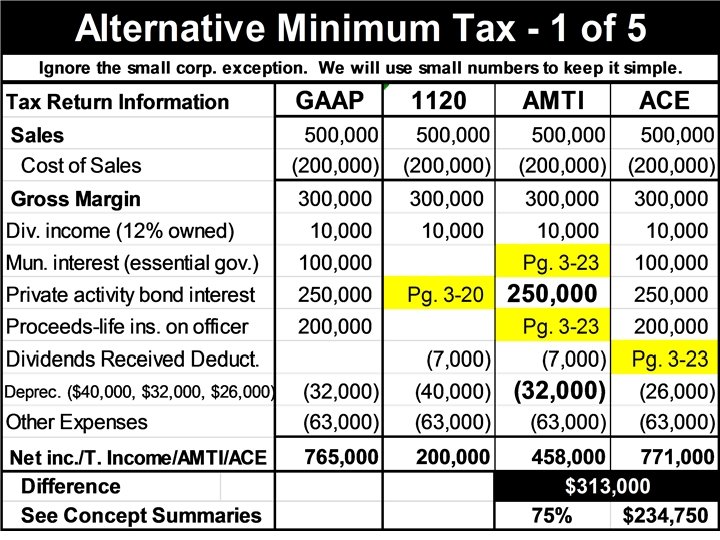

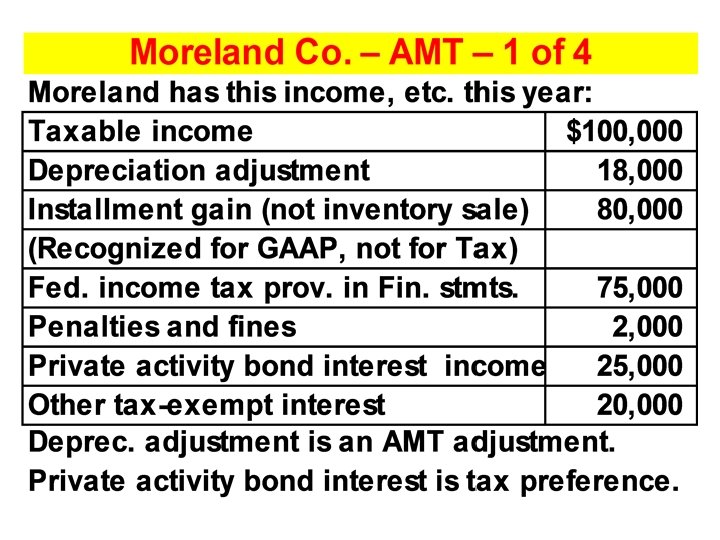

Corporate Alternative Minimum Tax Adjustments -Pg. 18. Recomputation of certain income, gain, deduction, and loss items. May either increase or decrease taxable income. Tax preference items - Pg. 20. Tax preferences will always increase taxable income. Interest on Private activity bond issued in 2009 -2010 was not a preference. Investors had stopped buying them.

Adjusted Current Earnings– ACE- Pg 21 A corp. makes a positive adjustment equal to 75% of the excess of its adjusted current earnings (ACE) over pre-adjustment AMTI. ACE is a concept based on the earnings and profits definition found in Sec. 312. A negative ACE adjustment also can be made when pre-adjustment AMTI exceeds ACE. The negative adjustment is 75% of the excess of pre-adjustment AMTI over ACE, but not in excess of the corporation's prior net positive ACE adjustments. 28

ACE adjustment = 75% of difference between AMTI and ACE –Can be positive or negative –Negative adjustment is limited to aggregate positive adjustments Starting point for determining ACE is AMTI –AMTI is defined as regular taxable income after AMT adjustments and tax preferences (other than the NOL and ACE adjustments) 29

33

34

36

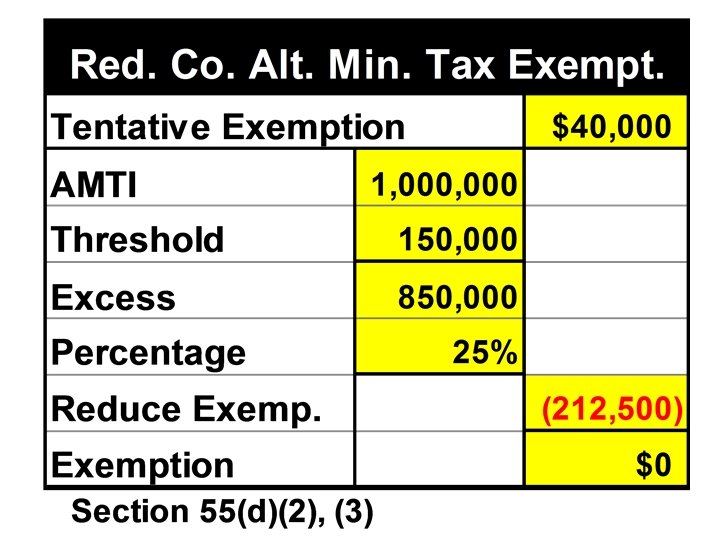

Corporate AMT Exemption The exemption amount for corporations is $40, 000. Exemption is reduced by 25% of excess of AMTI over $150, 000. Phased-out when AMTI reaches $310, 000. Sec. 55(d)(2) and (3) AMT-Code-Outline. xls 37

Rona Corporation – 1 of 3 Rona Corp. 's 2014 alternative minimum taxable income was $200, 000. Rona's 2014 alternative minimum exemption is a. $0 b. $12, 500 c. $27, 500 d. $52, 500 CPA - May, 1991 38

39

40

Minimum Tax Credit. AMT is an acceleration of the payment of a corporation's income taxes. When a corp. pays the AMT, it is allowed a credit that can be carried over and used to offset its regular (income) tax liabilities in subsequent years. 41

Minimum Tax Credit. The corporate AMT credit (MTC) equals the entire AMT amount paid. The MTC that can be used in a tax year equals the total of the net minimum taxes paid since 1986, minus the amount claimed as MTC in those years. Use of available MTCs in the current year is limited to the excess of (1) regular tax liability (minus all credits other than refundable credits) over (2) its tentative minimum tax. Indefinite carryover period.

Tax Credits and the AMT. A corporation is allowed to reduce its regular tax liability by any available credit. For most corporations, the general business credit can be claimed only to the extent that the corporation's regular tax liability exceeds its tentative minimum tax amount. 43

Minimum Tax Credit Small corporations (no longer subject to AMT) with unused minimum tax credits after 1997 may use them against regular tax liability Limit = regular tax - [25% X (regular tax - $25, 000)] 44

Tax Planning Considerations AMT Elections. Two elections permit taxpayers to defer the claiming of certain deductions for income tax purposes. An extended write-off period applies to certain expenditures (e. g. , research and experimental expenditures) that would otherwise be tax preference items or adjustments. If this extended write-off period is elected, the expenditures will not be a tax preference item. A second election permits a taxpayer to elect to use the depreciation method generally required for AMT purposes--the 150% declining balance method over the property's class life for personalty--in computing its regular tax liability. 45

Eliminating the ACE Adjustment. C corporations are required to increase their AMTI by the amount of the ACE adjustment. If the C corporation is closely-held, it can elect to be taxed under the S corporation rules and this adjustment can be avoided. 46

48

49

50

51

Continue the Eastern Corporation case above. Actually it is repeated on next slide. Assume there are no additional adjustments. What is the AMT Exemption? What is the regular tax? What is the AMT? 52

54

55

56

57

Local Corporation (1 of 5) Local has regular taxable income of $100, 000. Tax preference items and positive adjustments total $170, 000. Local has no credits. AMT is a. $26, 000. b. $29, 500. c. $22, 500. d. $10, 000. e. $0. 58

59

60

61

62

Small Corporation Exemption - 1 For tax years beginning after 1997, small corporations are not subject to AMT –A small corporation has average annual gross receipts of $5 million or less for the preceding three-year period –Small corporation continues to qualify as long as average gross receipts for the preceding three-year period do not exceed $7. 5 million –Sec. 55(e) 63

Small Corporation Exemption -2 A corporation can maintain its exemption from the AMT if? a. it reports average gross receipts of less than $1, 000 per year b. it reports average gross receipts of less than $7, 500, 000 per year c. it reports average gross receipts of less than $5, 000 per year 64

Small Corporation Exemption -3 A corporation can maintain its exemption from the AMT if? b. it reports average gross receipts of less than $7, 500, 000 per year 65

67

68

69

70

71

C Corporation Case – Old Law (Pg. 1 of 2) • Dad started a C Corporation -- usually breaks even. Has little or no E & P. • Owned by Dad & two adult children. • Dad has terminal illness – will die soon. Corp. will collect life ins. of $10, 000. • Corporation does not need the money, and will distribute the money to Widow and Children. Do you see any Tax Problems? 72

C Corporation Case (Pg. 2 of 2) • C Corp. will owe AMT (ACE adj. ) • 20% (of 75%) gives AMT of $1, 500, 000 • That leaves $8, 500, 000 for distribution • Tax-free income increases E & P • Stockholders will pay about 40%, or another $3, 200, 000. (Old tax law) • This is a total of $4, 800, 000 in tax. • Stockholders keep (after tax) $5, 200, 000. • Would a temporary S election help? 73

Note: The purpose of the table (next two slides) is to show our earlier study of earnings and profits set the stage for understanding the concept of adjusted current earnings. 74

75

76

Compliance and Procedural Considerations The corporate AMT liability is reported on Form 4626 (Alternative Minimum Tax -- Corporations). 77

The End 78