Chapter 2 Random variables 2 1 Random variables

Chapter 2 Random variables

2. 1 Random variables Definition. Suppose that S={e} is the sampling space of random trial, if X is a real-valued function with domain S, i. e. for each e S, there exists an unique X=X(e), then it is called that X a Random vector. Usually , we denote random variable by notation X, Y, Z or , , etc. . For notation convenience, From now on, we denote random variable by r. v.

2. 2 Discrete random variables Definition Suppose that r. v. X assume value x 1, x 2, …, xn, … with probability p 1, p 2, …, pn, …respectively, then it is said that r. v. X is a discrete r. v. and name P{X=xk}=pk, (k=1, 2, … ) the distribution law of X. The distirbution law of X can be represented by X~ P{X=xk}=pk, (k=1, 2, … ), or X x 1 x 2 … x. K … Pk p 1 p 2 … pk …

pk 0, k= 1, 2, … ; (2)")

2. Characteristics of distribution law (1) pk 0, k= 1, 2, … ; (2) Example 1 Suppose that there are 5 balls in a bag, 2 of them are white and the others are black, now pick 3 ball from the bag without putting back, try to determine the distribution law of r. v. X, where X is the number of whithe ball among the 3 picked ball. In fact, X assumes value 0,1,2 and

distribution let X denote the number that")

Several Important Discrete R. V. (0 -1) distribution let X denote the number that event A appeared in a trail, then X has the following distribution law X~P{X=k}=pk(1-p)1-k, (0<p<1) k= 0,1 or and X is said to follow a (0 -1) distribution

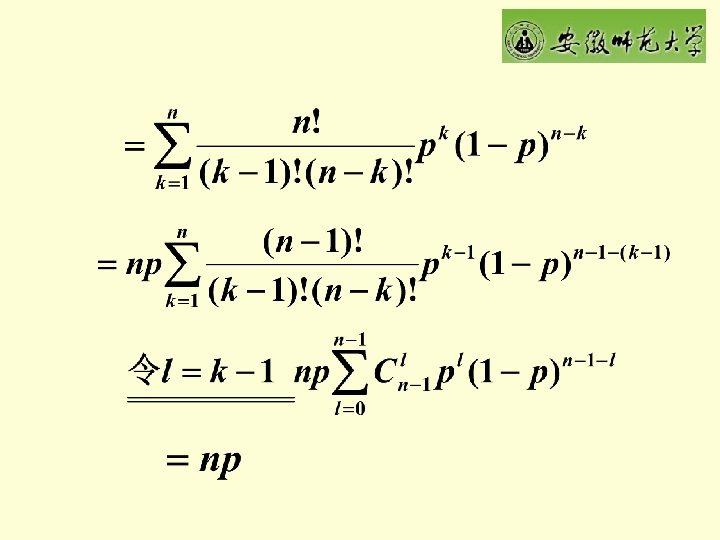

Let X denote the numbers that event A appeared in a n-repeated Bernoulli experiment, then X is said to follow a binomial distribution with parameters n, p and represent it by X B(n, p). The distribution law of X is given as :

Example A soldier try to shot a bomber with probability 0. 02 that he can hit the target, suppose the he independently give the target 400 shots, try to determine the probability that he hit the target at least for twice. Answer Let X represent the number that hit the target in 400 shots Then X~B(400, 0. 02), thus P{X 2}= 1- P{X= 0}-P {X= 1}= 1-0. 98400 -400)(0. 02)(0. 98399)=… Poisson theorem If Xn~B(n, p), (n= 0, 1, 2, …) and n is large enough, p is very small, denote =np,then

(0. 02)= 8, then")

Now, lets try to solve the aforementioned problem by putting =np=(400)(0. 02)= 8, then approximately we have P{X 2}= 1- P{X= 0}-P {X= 1} = 1-(1+8)e-8= 0. 996981. Poisson distribution X~P{X=k}= , k= 0, 1, 2, … ( 0)

Poisson theorem indicates that Poisson distribution is the limit distribution of binomial distribution, when n is large enough and p is very small, then we can approximate binomial distribution by putting =np.

Random variable Several important r. v. s Discrete r. v. Distribution law 0 -1 distribution Poisson distribution Bionomial distribution

2. 3 Distribution function of r. v. Definition Suppose that X is a r. v. , for any real number x,Define the probability of event {X x}, i. e. P {X x} the distribution function of r. v. X, denote it by F(x), i. e. F(x)=P {X x}.

, P {a<X b}=P{X b}-P{X")

It is easy to find that for a, b (a<b), P {a<X b}=P{X b}-P{X a}= F(b)-F(a). For notation convenience, we usually denote distribution fucntion by d. f.

F(x 2);")

Characteristics of d. f. 1. If x 1<x 2, then F(x 1) F(x 2); 2. for all x,0 F(x) 1,and 3. right continuous:for any x, Conversely, any function satisfying the above three characteristics must be a d. f. of a r. v.

Example 1 Suppose that X has distribution law given by the table Try to determine the d. f. of X X P 0 1 2 0. 1 0. 6 0. 3

For discrete distributed r. v. , X~P{X= xk}=pk, k= 1, 2, … the distribution function of X is given by

Suppose that the d. f. of r. v. X is specified as follows, Try to determine a, b and

Is there a more intuitive way to express the distribution Law of a r. v. ? Try to observe the following graph a b

is the")

2. 4 Continuous r. v. Probability density function Definition Suppose that F(x) is the distribution function of r. v. X,if there exists a nonnegative function f(x),(- <x<+ ), such that for any x,we have then it is said that X a continuous r. v. and f(x) the density function of X , i. e. X~ f(x) , (- <x<+ )

The geometric interpretation of density function

0,(- <x< ); (2) (1) and (2)")

2. Characteristics of density function (1 f(x) 0,(- <x< ); (2) (1) and (2) are the sufficient and necessary properties of a density function Suppose the density function of r. v. X is Try to determine the value of a.

If x is the continuous points of f(x), then Suppose that the d.")

(3) If x is the continuous points of f(x), then Suppose that the d. f. of r. v. X is specified as follows, try to determine the density function f(x)

For any b,if X~ f(x), (- <x< ),then P{X=b}= 0。 And")

(4) For any b,if X~ f(x), (- <x< ),then P{X=b}= 0。 And

Example 1. Suppose that the density function of X is specified by Try to determine 1)the d. f. F(x), 2)P{X (0. 5, 1. 5)}

…f(x) P{a<X<b} Density function")

Distribution function Monotonicity Right continuous Standardized Nonnegative F(x)…f(x) P{a<X<b} Density function

")

Suppose that the distribution function of X is specified by Try to determine (1) P{X<2}, P{0<X<3}, P{2<X<e-0. 1}. (2)Density function f(x)

= It is said that")

Several Important continuous r. v. 1. Uniformly distribution if X~f(x)= It is said that X are uniformly distributed in interval (a, b) and denote it by X~U(a, b) For any c, d (a<c<d<b),we have

2. Exponential distribution If X~ It is said that X follows an exponential distribution with parameter >0, the d. f. of exponential distribution is

, which follows an")

Example Suppose the age of a electronic instrument is X (year), which follows an exponential distribution with parameter 0. 5, try to determine (1)The probability that the age of the instrument is more than 2 years. (2)If the instrument has already been used for 1 year and a half, then try to determine the probability that it can be use 2 more years.

3. Normal distribution The normal distribution are one the most important distribution in probability theory, which is widely applied In management, statistics, finance and some other ereas. B A Suppose that the distance between A,B is , the observed value of X is X, then what is the density function of X ?

Suppose that the density fucntion of X is specified by where is a constant and >0 ,then, X is said to follows a normal distribution with parameters and 2 and represent it by X~N( , 2).

symmetry the curve of density function is")

Two important characteristics of Normal distribution (1) symmetry the curve of density function is symmetry with respect to x= and f( )=maxf(x)= .

influences the distribution ,the curve tends to be flat, ,the curve tends to")

(2) influences the distribution ,the curve tends to be flat, ,the curve tends to be sharp,

4. Standard normal distribution A normal distribution with parameters = 0 and 2= 1 is said to follow standard normal distribution and represented by X~N(0, 1)。

the density function of normal distribution is and the d. f. is given by

usually is not so easy to compute directly, so how")

The value of (x) usually is not so easy to compute directly, so how to use the normal distribution table is important. The following two rules are essential for attaining this purpose. Z~N(0,1), (0. 5)=0. 6915, P{1. 32<Z<2. 43}= (2. 43)- (1. 32)=0. 9925 -0. 9066 注:(1) (x)= 1- (-x); (2) 若X~N( , 2),则

, P{-2. 45<X<2. 45}=? 2. X N( , 2), P{ -3 <X<")

1 X~N(-1, 22), P{-2. 45<X<2. 45}=? 2. X N( , 2), P{ -3 <X< +3 }? EX 2 tells us the important 3 rules, which are widely applied in real world. Sometimes we take P{|X- |≤ 3 } ≈1 and ignore the probability of {|X- |>3 }

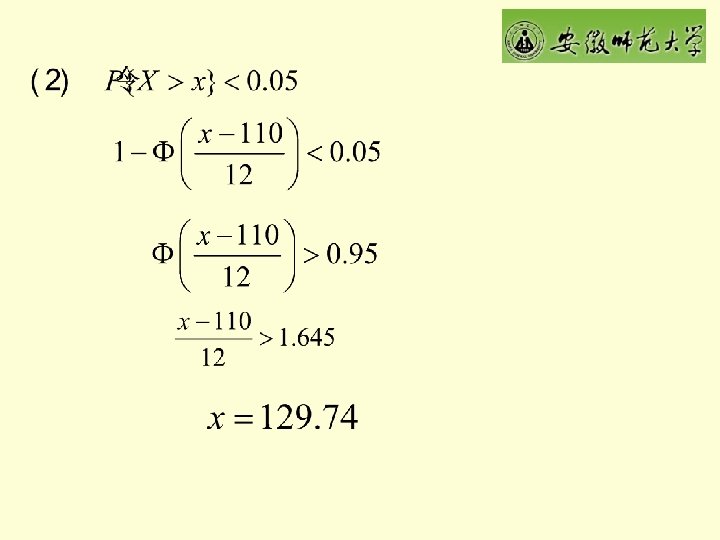

Example The blood pressure of women at age 18 are normally distributed with N(110, 122). Now, choose a women from the population, then try to determine (1) P{X<105}, P{100<X<120}; (2)find the minimal x such that P{X>x}<0. 05

Distribution of the function of r. v. s Distribution law of the function of discrete r. v. s Suppose that X~P{X=xk}=pk, k= 1, 2, … and y=g(x) is a real valued function, then Y=g(X) is also a r. v. , try to determine the law of Y. . Example X Pk Determine the law of Y=X 2 -1 0 1 Y Pk 1 0

or … Y=g(X)~P{Y=g(xk)}=pk , k= 1, 2,")

Generally X Pk Y=g(X) or … Y=g(X)~P{Y=g(xk)}=pk , k= 1, 2,

, -")

Density function of the function of continuous r. v. 1. If X f(x), - < x< + , Y=g(X) , then one can try to determine the density function, one can determine the d. f. of Y firstly FY (y) =P{Y y}=P {g(X) y}= and differentiate w. r. t. y yields the density funciton

, tyr to determine the d. f. and density function")

Example Let X U(-1, 1), tyr to determine the d. f. and density function of Y=X 2 If y<0 If 0≤y<1 If y≥ 1

Mathematical expectation Definition 1. If X~P{X=xk}=pk, k=1, 2, …n, define the mathematical expectation of r. v. X or mean of X.

Definition 2. If X~P{X=xk}=pk, k=1, 2, …, and define the mathematical expectation of r. v. X

Example 2 Toss an urn and denote the points by X, try to determine the mathematical expectation of X. Definition 3 Suppose that X~f(x), - <x< , and then define the mathematical expectation of r. v. X

Example 3. Suppose that r. v. X follows Laplace distribution with density function Try to determine E(X).

Mathematical expectation of several important r. v. s 1. 0 -1 distribution EX=p 2. Binomial distribution B(n, p)

")

3. Poisson distribution 4. Uniform distribution U(a, b)

5. Exponential distribution

")

6. Normal distribution N( , 2)

Mathematical expectation of the functions of r. v. s EX 1 Suppose that the distribution law of X X Pk -1 0 1 Try to determine the mathematical expectation of Y=X 2 Y Pk 1 0

is")

Theorem 1 let X~P{X=xk}=pk, k=1, 2, …, then the mathematical expectation of Y=g(X) is given by the following equation and denoted by E(g(X))

EX 2:Suppose that r. v. X follows standardized distribution Try to determine the mathematical expectation of Y=a. X+b Answer Y=ax is strictly monotonic with respect to x with inverse function Thus the density function of Y is given by

, - <x< , the mathematical expectation of Y=g(X) is specified")

Theorem 2 If X~f(x), - <x< , the mathematical expectation of Y=g(X) is specified as

distribution, try to determine E(X 2), E(X 3) and")

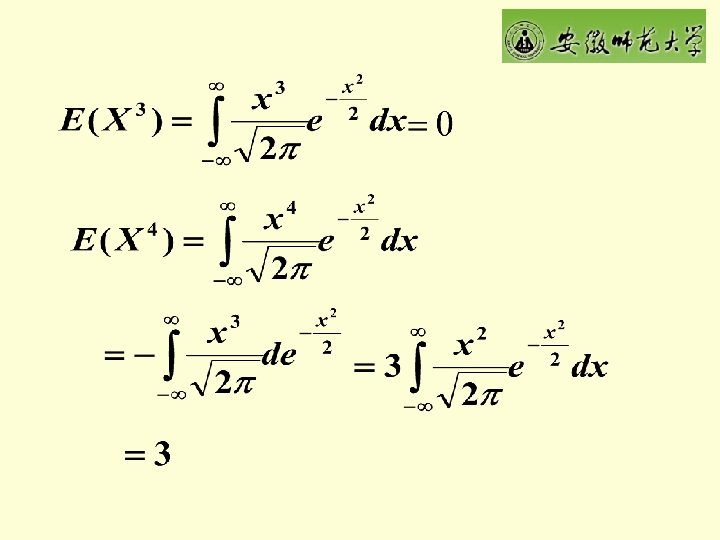

Suppose that X follows N(0,1) distribution, try to determine E(X 2), E(X 3) and E(X 4)

=c, where c is a constant; 2。E(c. X)=c. E(X),")

Properties of mathematical expectation 1. E(c)=c, where c is a constant; 2。E(c. X)=c. E(X), c is a constant. Proof. Let X~f(x), then

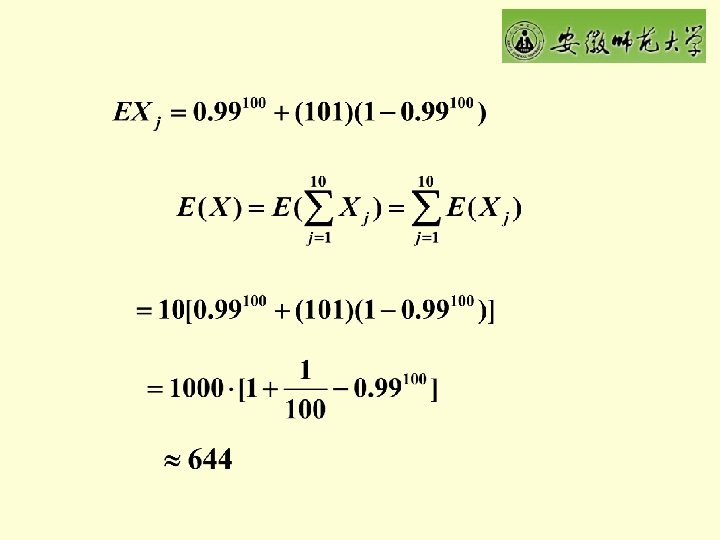

Example 2. Some disease will occur with probability 1%, investigate 1000 people now, it is necessary to check the blood. The method is clarified these people into ten group with each group 100 and check the mixed blood sample. If the result is negative, it is not need to do any test any more, if it is positive, then , it is necessary to test each blood sample respectively, try to determine the average times needed for the test. Let Xj is the number to be taken of jth group, and X the number to be taken in 1000 people, then Xj Pj 1 101

Variance Definition 1 Suppose that X is a r. v. with EX 2<∞, define E (X-EX)2 the variance of r. v. X and denote it by DX E (X-EX)2= E [X 2 -2 EXEX +E 2 X ]=EX 2 - E 2 X

distribution with P(X=0)=p, then")

The variance of several important r. v. s (0 -1) distribution with P(X=0)=p, then DX=pq Binomial distribution B(n, p), then DX=npq Poisson distribution with parameter then, DX=EX=

The variance of several important r. v. s Uniform distribution: Suppose that r. v. X is uniformly distributed on interval [a, b], then Normal distribution: then Exponential distribution: then

Definition of mathematical expectation Properties of mathematical expectation Mathematical expectation of the functions of r. v. Several important expectation

- Slides: 65