Chapter 2 COMPONENTS OF FINANCIAL MARKET SYSTEM Financial

New York Stock Exchange, (NYSE) (2) American")

• • Membership seat: 1366 seats since 1953. Seat")

(2) (3) (4) profitability size market value public ownership.")

underwriting, • (2) distributing, • (3) advising.")

rail-road issues, (2) public utility")

current stockholders, • (2) employees, or • (3) customers.")

life insurance companies, • (2) state and local retirement funds,")

(BILLION OF DOLLARS")

(2) the underwriters spread issuing costs. (a) printing and")

Securities Acts Amendments of")

")

the unbiased expectations theory, • (2) the liquidity")

underwriting, (2) distributing, and (3) advising. • the")

life insurance firms, (2) state and local retirement funds, and")

- Slides: 47

Chapter 2 COMPONENTS OF FINANCIAL MARKET SYSTEM

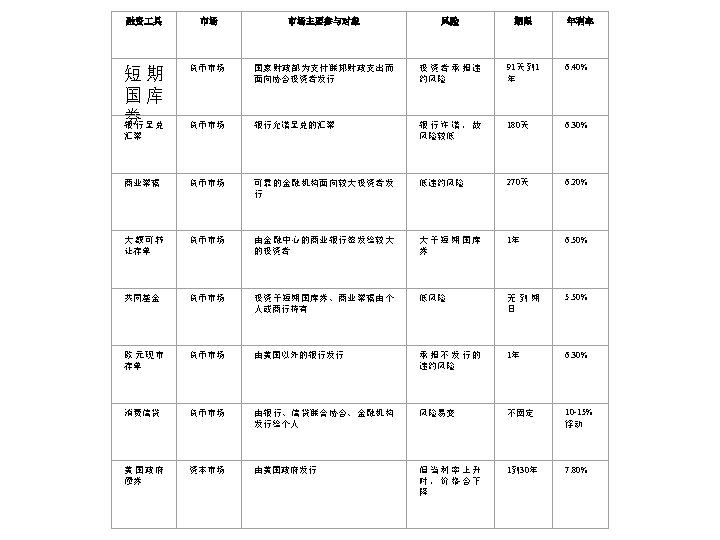

Financial Markets • • • Primary Market Second Market Money Market Capital Market Organized Securities Exchanges Over-the-Counter Markets • Public Offerings and Private Placement

Organized Securities Exchanges • • • (1) New York Stock Exchange, (NYSE) (2) American Stock Exchange, (AMEX) (3) Mid-west Stock Exchange, (4) Pacific Stock Exchange, (5) Philadelphia Stock Exchange, (6) Boston Stock Exchange, and

New York Stock Exchange (NYSE) • • Membership seat: 1366 seats since 1953. Seat fee: $760, 000 to a high of $830, 000. ' 1995 auction : “make a market” matching pricing (asked and offered) Price Quotes 82%

Function of the NYSE • 1 Providing a continuous market. • 2. Establishing and publicizing fair security prices. • 3. Helping business raise new capital.

Listing Requirements • • (1) (2) (3) (4) profitability size market value public ownership.

• Profitability • EBT: at 1 east $2. 5 million. • For the two years preceding EBT: at least $2. 0 million. • Size • Net tangible assets: at least $18. 0 million.

• • Market Value The market value: at least $18. 0 million. Public Ownership common shares : 1. 1 million publicly held holders of 100 shares : at least 2, 000.

THE INVESTMENT BANKER • a financial specialist involved as an intermediary in the merchandising of securities. • Banking Act of 1933(also known as the Glass-Steagall Act of 1933).

Functions of Institutes • (1) underwriting, • (2) distributing, • (3) advising.

Distribution Methods • • Most competitive bid purchases (1) rail-road issues, (2) public utility issues, (3) state and municipal bond issues. (4) Commission or Lest-Efforts Basis (5) Privileged Subscription (6) Direct Sale

• (1) current stockholders, • (2) employees, or • (3) customers.

PRIVATE PLACEMENTS • (1) life insurance companies, • (2) state and local retirement funds, • (3) private pension funds.

Advantages of private placement • 1. • 2. • 3. Speed. Reduced flotation costs. Financing flexibility.

disadvantages • 1. • 2. • 3. Interest costs. Restrictive covenants. The possibility of future SEC registration.

Leading U. S. Investment Bankers, 1995 (Domestic debt and Equity issue) (BILLION OF DOLLARS FIRM UNDERWRITING VOLUME $ 122. 3 Percent 1 Merrill Lynch 2 Lehman Brothers 70. 3 9. 9 3 Golden Sachs 68. 5 9. 7 3 Morgan Stanley 68. 5 9. 7 5 Salomon Brother 68. 1 9. 6 6 CS First Boston 64. 6 9. 1 7 J. R. Morgan 40. 2 5. 7 8 Bear, Sterns 25. 4 3. 6 9 Donaldson Lufkin & Jenrette 10 Smith Barney 20. 7 17. 9% 22. 2 3. 1 2. 9

Table 2 -6 Public and Privately Placed Corporate Debt Placed Domestically (Gross proceeds of All New U. S. Corporate Debt Issue) Total Volume Year (S Millions) Percent Publicly Placed (%) Percent Privately Placed (%) 1994 $441287 82.8 17.2 1993 361860 79.3 20.7 1992 443911 85.2 14.8 1991 603119 80.7 19.3 1990 276259 68.5 31.5 1989 298813 60.7 39.3 1988 329919 61.3 38.7 1987 301447 69.5 30.5 1986 313502 74.2 25.8

FLOTATION COSTS • • (1) (2) the underwriters spread issuing costs. (a) printing and engraving, (b) legal fees, (3) accounting fees, (4) trustee fees, several other miscellaneous components.

• Full public disclosure • Firm file a registration statement with the SEC • a minimum 20 -day waiting period, • registration process a preliminary prospectus (the red herring)

25 investors not be registered • 1. less than $1. 5 billion of new securities per year. • 2. Issues that are sold entirely intrastate. • 3. short-term instruments: maturity periods of 270 days or less. • 4. Issues that are already regulated or controlled by some other federal agency

• Mr. Ivan F. Boesky, a loophole in the 1940 Ponzis Scheme • Enron and World. Com

REGULATION • • 1929 --1932, State statutes (blue sky laws) Securities Acts Amendments of 1975 Primary Market Regulations Securities Act of 1933.

Primary market regulation • Full public disclosure • Firm file a registration statement with the SEC • a minimum 20 -day waiting period, • registration process a preliminary prospectus (the red herring非招募章程)

Secondary Market Regulations Shelf Registration • 1. Major security exchanges must register with the SEC. • 2. Insider trading is regulated. • 3. Manipulative trading • 4. The SEC is given control over proxy procedures. • 5. The Board of Governors of the Federal Reserve System

Figure 2 -4 Average Annual Returns and Standard Deviations of Returns, 1926 -1995

Figure 2 -5 Rates of Return and Standard Deviations, 1926 -1995

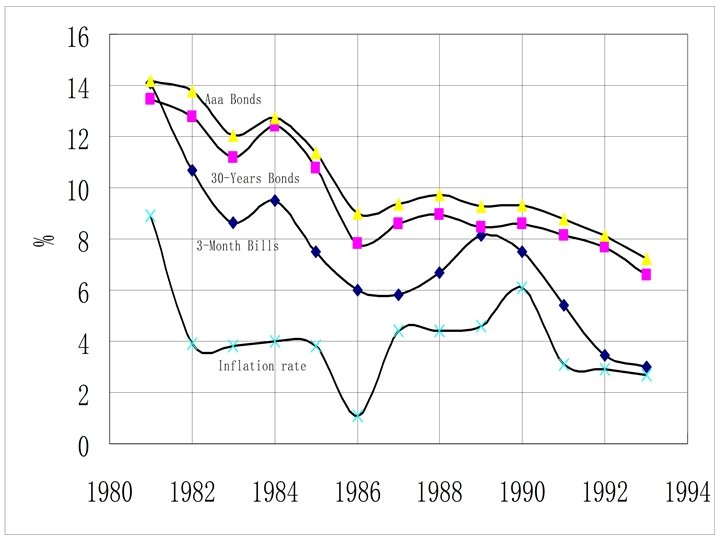

Table 2 -7 Interest Rate Level and Inflation Rates 1981 -1995 3 -Month Treasury Bills 30 -Year AAA Rated Treasury Bonds Corporate Bonds Inflation rate 1981 14. 08 13. 44 14. 17 8. 9 1982 10. 69 12. 76 13. 79 3. 9 1983 8. 63 11. 18 12. 04 3. 8 1984 9. 52 12. 39 12. 71 4. 0 1985 7. 49 10. 79 11. 37 3. 8 1986 5. 98 7. 80 9. 02 1. 1 1987 5. 82 8. 58 9. 38 4. 4 1988 6. 68 8. 96 9. 71 4. 4 1989 8. 12 8. 45 9. 26 4. 6 1990 7. 51 8. 61 9. 32 6. 1 1991 5. 42 8. 14 8. 77 3. 1 1992 3. 45 7. 67 8. 14 2. 9 1993 3. 02 6. 59 7. 22 2. 7

INTEREST RATE and DETERMINANTS • k = k* + IRP + DRP + MP + LP • • • k = the nominal or observed rate k* = the real risk--free rate of interest, IRP = inflation-risk premium. DRP = default-risk premium MP = maturity LP = liquidity premium

Krf = k* + IRP (2 -2)

The Effects of Inflation on Rates of Return and the Fisher Effect • Krf =k *+ IRP + (k*. IRP) • 0. 113 = k* +. 05 + '05 k* – K* =. 06 = 6%

MEAN NOMINAL YIELD SECURITY % Treasury bills 7. 08 MEAN INFLATION RATE % INFERRED REAL RATE % 3. 93 3. 15 Treasury bonds 9. 31 3. 93 5. 38 Corporate bonds 10. 03 3. 93 6. 10

THE TERM STRUCTURE OF INTEREST RATES

Historical Interest Rates 13 Int er est rat e 9 Oct 31, 19 79 Mar 31, 19 90 Nov 13, 19 91 1 2 10 Years to maturity 30

Explaining Term Structure • • (1) the unbiased expectations theory, • (2) the liquidity preference theory, • (3) the market segmentation theory.

SUMMARY • • market environment structure of financial markets the institution of investment banking various methods for distributing securities role of interest rates

Components of financial market • • public offerings private placements:institutional investors. financial instruments The secondary market money and capital markets primary and secondary organized security exchanges over-the-counter market

Investment banker • functions of (l) underwriting, (2) distributing, and (3) advising. • the negotiated purchase, (2) the competitive bid purchase, (3) the commission or bestefforts basis, (4) privileged subscriptions, and (5) direct sales.

Private placements • (l) life insurance firms, (2) state and local retirement funds, and (3) private pension funds. • advantages and disadvantages

• Flotation costs • securities Act Of l 933. • Rates of return