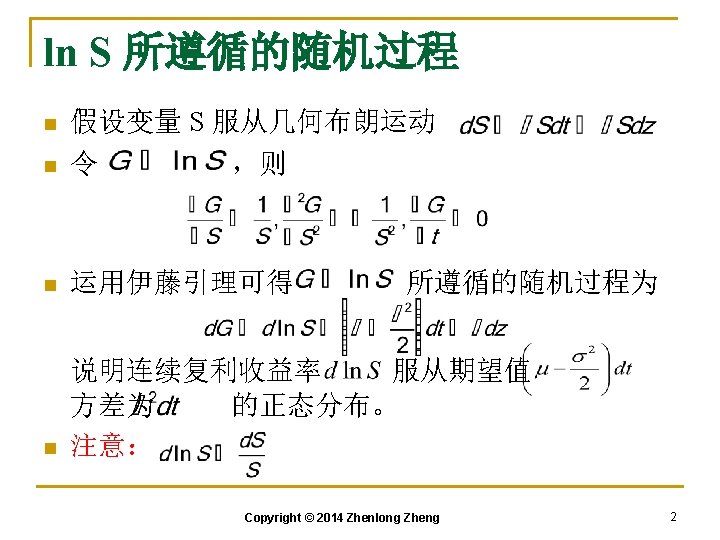

Chapter 15 The BlackScholesMerton Model http efinance org

Chapter 15 The Black-Scholes-Merton Model 郑振龙 厦门大学金融系 课程网站:http: //efinance. org. cn Email: zlzheng@xmu. edu. cn

沪深 300: 20020107-20150525 g n nlo e h Z g © t h ig n e Zh r y p o C 厦门大学 郑振龙 2015 5

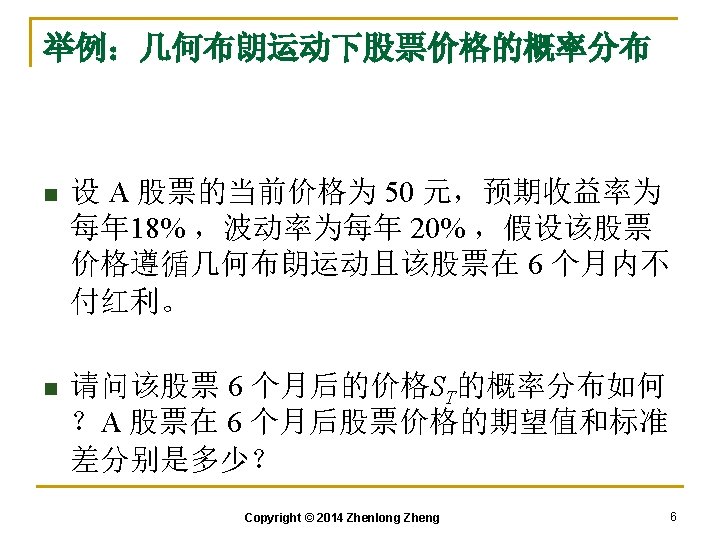

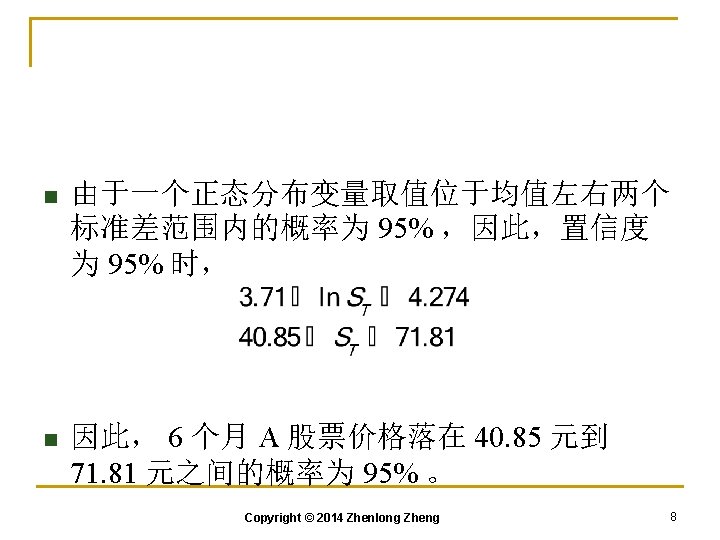

n S = 50, µ = 0. 18, σ = 0. 2, T − t = 0. 5 年 因此 6 个月后ST的概率分布为 n 即 n Copyright © 2014 Zhenlong Zheng 7

n Copyright © 2014 Zhenlong Zheng 9

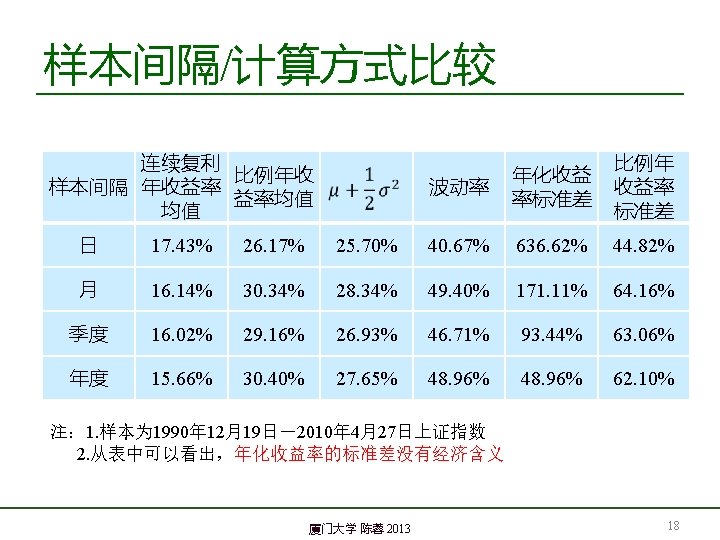

课后阅读:连续复利 n Copyright © 2014 Zhenlong Zheng 10

n n n")

Mutual Fund Returns (See Business Snapshot 13. 1 on page 281) n n n Suppose that returns in successive years are 15%, 20%, 30%, -20% and 25% The arithmetic mean of the returns is 14% The returned that would actually be earned over the five years (the geometric mean) is 12. 4% Copyright © 2014 Zhenlong Zheng 13

1900-2000主要国家股指实际收益率 Copyright © 2014 Zhenlong Zheng 14

预期收益率 µ n Copyright © 2014 Zhenlong Zheng 15

Estimating Volatility from Historical Data 1. Take observations S 0, S 1, . . . , Sn at intervals of t years 2. Define: 3. Calculate the standard deviation, s , of the ui ´s 4. The historical volatility estimate is: Copyright © 2014 Zhenlong Zheng 17

The Concepts Underlying Black. Scholes n n The option price & the stock price depend on the same underlying source of uncertainty We can form a portfolio consisting of the stock and the option which eliminates this source of uncertainty The portfolio is instantaneously riskless and must instantaneously earn the risk-free rate This leads to the Black-Scholes differential equation Copyright © 2014 Zhenlong Zheng 19

Assumptions of BS Formula n n n n The short-term interest rate is known and is constant through time. The stock price follows a random walk in continuous time with a variance rate proportional to the square of the stock price. Thus the distribution of stock prices is lognormal. The variance rate of the return on the stock is constant. The sock pays no dividends. The option is “European”. There are no transaction costs. It’s possible to borrow money to buy stocks. There are no penalties to short selling. Copyright © 2014 Zhenlong Zheng 20

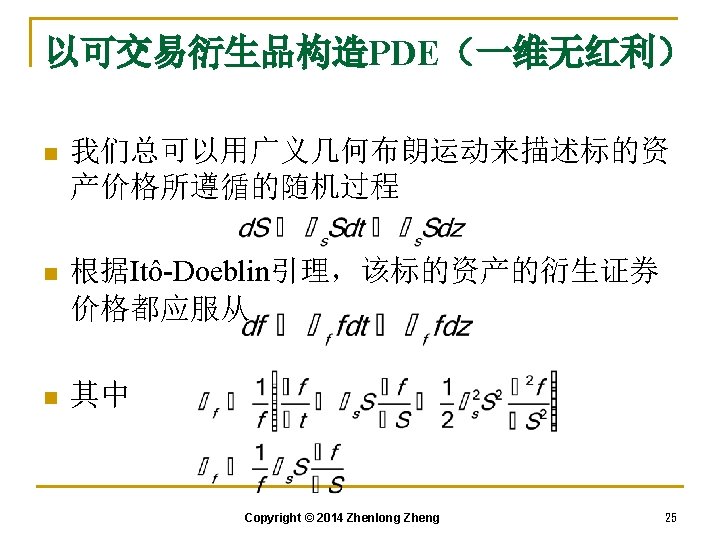

The Derivation of the Black-Scholes Differential Equation 1 of 3: Copyright © 2014 Zhenlong Zheng 21

The Derivation of the Black-Scholes Differential Equation 2 of 3: Copyright © 2014 Zhenlong Zheng 22

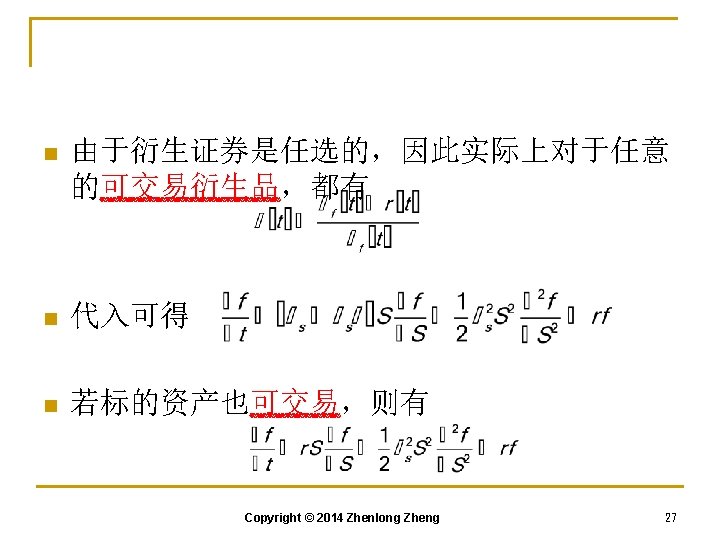

The Derivation of the Black-Scholes Differential Equation 3 of 3: n The return on the portfolio must be the risk-free rate. Hence n We substitute for and differential equation: in these equations to get the Black-Scholes Copyright © 2014 Zhenlong Zheng 23

n Copyright © 2014 Zhenlong Zheng 26

标的资产的市场风险的价格 n Copyright © 2014 Zhenlong Zheng 28

Discounted Feynman-Kac Theorem n Copyright © 2014 Zhenlong Zheng 30

n Discounted Feynman-Kac theorem的本质建立了 PDE跟SDE的对应关系,最后将偏微分方程的 解表达成了某一扩散扩散过程的期望值。 Copyright © 2014 Zhenlong Zheng 31

Valuing a Forward Contract with Risk -Neutral Valuation n Payoff is ST – K Expected payoff in a risk-neutral world is S 0 er. T – K Present value of expected payoff is e-r. T[S 0 er. T – K]=S 0 – Ke-r. T Copyright © 2014 Zhenlong Zheng 39

Perpetual Derivative n For a perpetual derivative there is no dependence on time and the differential equation becomes A derivative that pays off Q when S = H is worth QS/H when S<H and when S>H. (These values satisfy the differential equation and the boundary conditions) Copyright © 2014 Zhenlong Zheng 40

The Black-Scholes Formulas Copyright © 2014 Zhenlong Zheng 41

Function n N(x) is the probability that a normally distributed variable with")

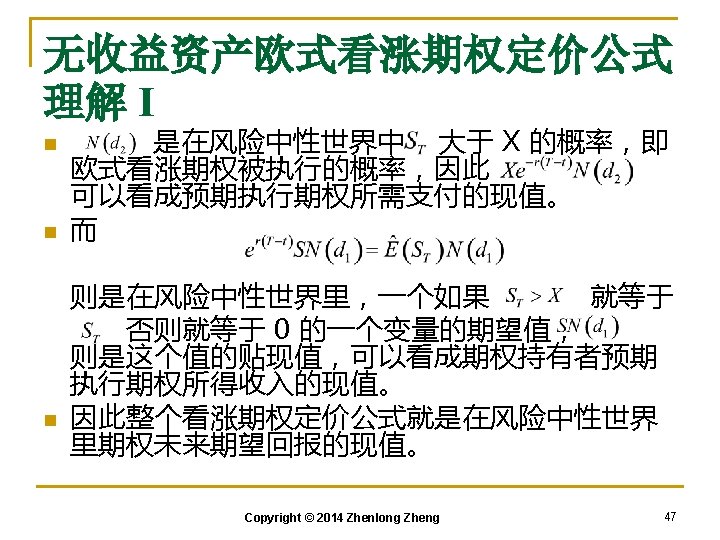

The N(x) Function n N(x) is the probability that a normally distributed variable with a mean of zero and a standard deviation of 1 is less than x n See tables at the end of the book Copyright © 2014 Zhenlong Zheng 42

Properties of Black-Scholes Formula n As S 0 becomes very large c tends to S 0 – Ke-r. T and p tends to zero • As S 0 becomes very small c tends to zero and p tends to Ke-r. T – S 0 Copyright © 2014 Zhenlong Zheng 43

Copyright © 2014 Zhenlong Zheng 44")

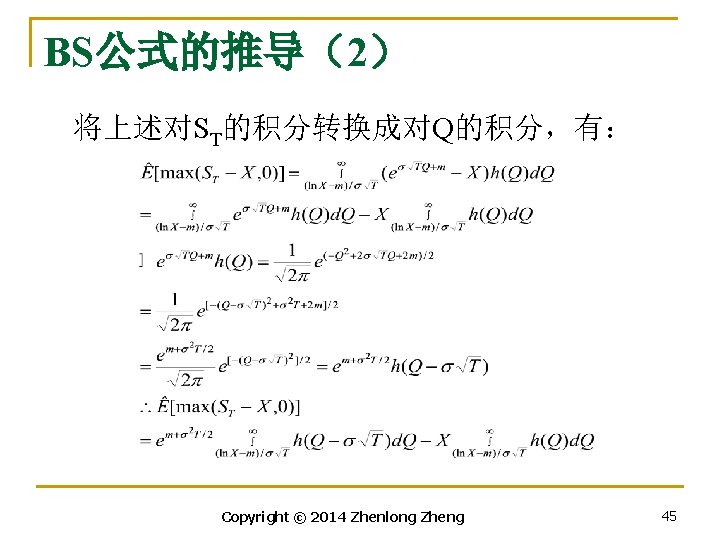

BS公式的推导(1) Copyright © 2014 Zhenlong Zheng 44

Copyright © 2014 Zhenlong Zheng 46")

BS公式的推导(3) Copyright © 2014 Zhenlong Zheng 46

Implied Volatility n n n The implied volatility of an option is the volatility for which the Black-Scholes price equals the market price The is a one-to-one correspondence between prices and implied volatilities Traders and brokers often quote implied volatilities rather than dollar prices Copyright © 2014 Zhenlong Zheng 50

Causes of Volatility n n Volatility is usually much greater when the market is open (i. e. the asset is trading) than when it is closed For this reason time is usually measured in “trading days” not calendar days when options are valued Copyright © 2014 Zhenlong Zheng 51

VXO与VIX对比 Copyright © 2014 Zhenlong Zheng 52

平价期权的经验法则 n Copyright © 2014 Zhenlong Zheng 54

平价期权 c/S与波动率与期限的关系 Copyright © 2014 Zhenlong Zheng 55

拓展 2:无收益资产欧式看跌期权 n Copyright © 2014 Zhenlong Zheng 56

n Copyright © 2014 Zhenlong Zheng 59

Warrant Valuation n The analysis of warrants is much more complicated than that of options, because: Ø Ø The Exercise price of the warrant is usually not adjusted at all for dividends. The exercise price of a warrant sometimes changes on specified dates. If the company is involved in a merger, the adjustment that is made in the terms of the warrant may change its value. The exercise of a large number of warrants may sometimes result in a significant increase in the number of common shares outstanding. Copyright © 2014 Zhenlong Zheng 64

Warrants & Dilution n n When a regular call option is exercised the stock that is delivered must be purchased in the open market When a warrant is exercised new stock is issued by the company the stock price will reduce at the time the issue of is announced. There is no further dilution (See Business Snapshot 15. 3. ) 因此权证的定价公式与期权一样。 Copyright © 2014 Zhenlong Zheng 65

Any Questions? Copyright © 2014 Zhenlong Zheng 66

Copyright © 2014 Zhenlong Zheng 67

- Slides: 67