Chapter 13 Accounting Test Review Test is Friday

Study Guide Due By")

: ◦ Paid")

: ◦ Recorded employer")

- Slides: 29

Chapter 13 Accounting Test Review Test is Friday (53 Points) Study Guide Due By Thursday Challenge Problem (Extra Credit) Available Practice Test is Available Talk to Ames for reposts

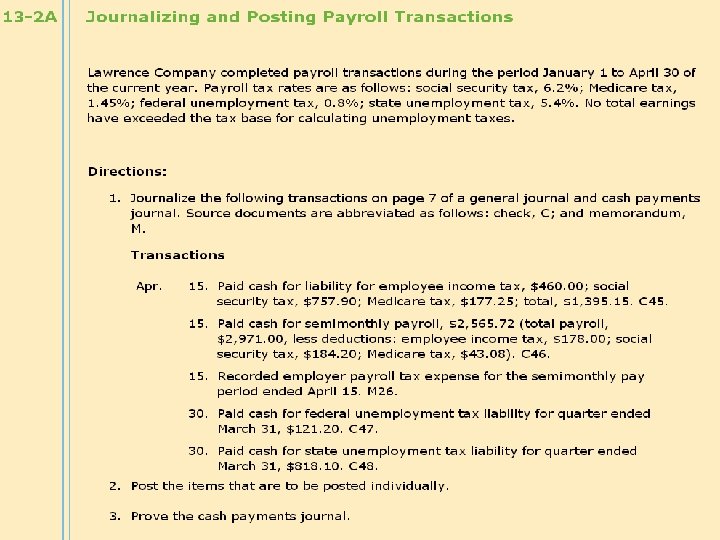

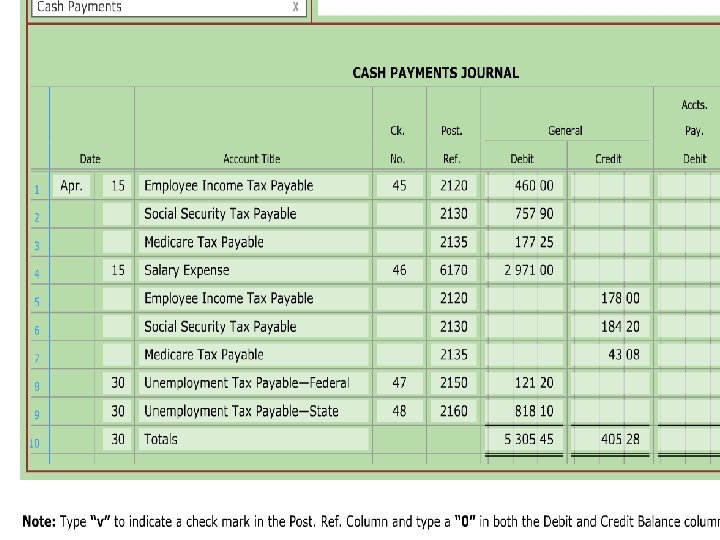

Transaction 1– Paying the Tax Liability � Paid cash for liability for employee income tax, $460. 00; social security tax, $757. 90; Medicare tax, $177. 25; total, $1, 395. 15. C 45. ◦ ◦ ◦ Goes in cash payments journal Debit Employee income tax payable $460 Debit Social security tax payable $757. 90 Debit Medicare tax payable $177. 25 Credit Cash $1395. 15

Transaction 2 – Recording the employees’ semimonthly payroll � Paid cash for semimonthly payroll, $2, 565. 72 (total payroll, $2, 971. 00, less deductions: employee income tax, $178. 00; social security tax, $184. 20; Medicare tax, $43. 08). C 46. ◦ ◦ ◦ Goes in the cash payments journal Debit Salary expense $2971. 00 Credit Employee income tax payable $178. 00 Credit Social security tax payable $184. 20 Credit Medicare tax payable $43. 08 Credit Cash $2565. 72

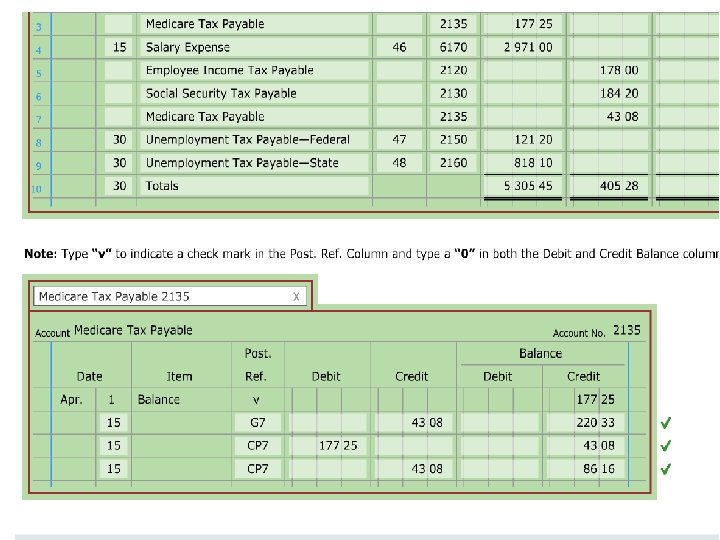

Transaction 3 – Recording the employer’s payroll tax expense � Recorded employer payroll tax expense for the semimonthly pay period ended April 15. M 26. ◦ Goes in the general journal ◦ Debit Payroll tax expense $411. 48 �Total of all the taxes below ◦ Credit Social security tax payable $184. 20 �Total earnings/payroll $2971 x. 062 ◦ Credit Medicare tax payable $43. 08 �Total earnings/payroll $2971 x. 0145 ◦ Credit Unemployment tax payable-Federal $23. 77 �Total earnings/payroll $2971 x. 008 ◦ Credit Unemployment tax payable-State $160. 43 �Total earnings/payroll $2971 x. 054

Transaction 4 – Recording the employer’s payroll tax expense ◦ Goes in the general journal ◦ Debit Payroll tax expense $411. 48 �Total of all the taxes below ◦ Credit Social security tax payable $184. 20 �Total earnings/payroll $2971 x. 062 ◦ Credit Medicare tax payable $43. 08 �Total earnings/payroll $2971 x. 0145 ◦ Credit Unemployment tax payable-Federal $23. 77 �Total earnings/payroll $2971 x. 008 ◦ Credit Unemployment tax payable-State $160. 43 �Total earnings/payroll $2971 x. 054

Transaction 5– Paying the Unemployment Tax Liability � Paid cash for federal unemployment tax liability for quarter ended March 31, $121. 20. C 47. ◦ Goes in cash payments journal ◦ Debit Unemployment tax payable-Federal $121. 60 ◦ Credit Cash $121. 60

Transaction 6– Paying the Unemployment Tax Liability � Paid cash for state unemployment tax liability for quarter ended March 31, $818. 10. C 48. ◦ Goes in cash payments journal ◦ Debit Unemployment tax payable-State $818. 10 ◦ Credit Cash $818. 10

Tax Employee Income Tax Social Security X X X Medicare X X Unemployment. Federal Unemployment. State Employer X X

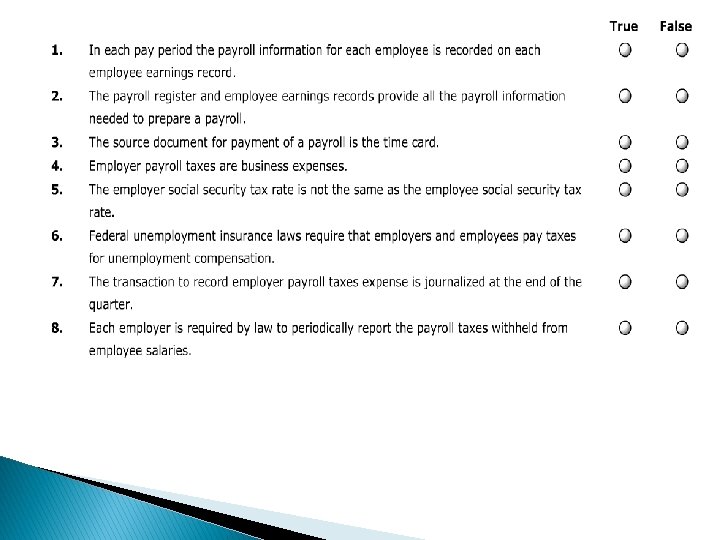

Employee Taxes � Employees have Federal Income, Social Security, and Medicare taxes removed from their checks � Tax amounts are based on a percentage of gross pay � Payroll register and employee earnings records provide the information needed

Employer Payroll Taxes � Business expenses for the company � Employers must pay Social Security, Medicare and Federal and State Unemployment taxes � Based on a percentage of employee earnings ◦ Employers pay the same percentage of Social Security and Medicare as employees ◦ Employers are not required to pay unemployment taxes after the first $7, 000 earned �If an employee’s accumulated earnings are $6, 500, the employer is only subject to the next $500 of employee earnings.

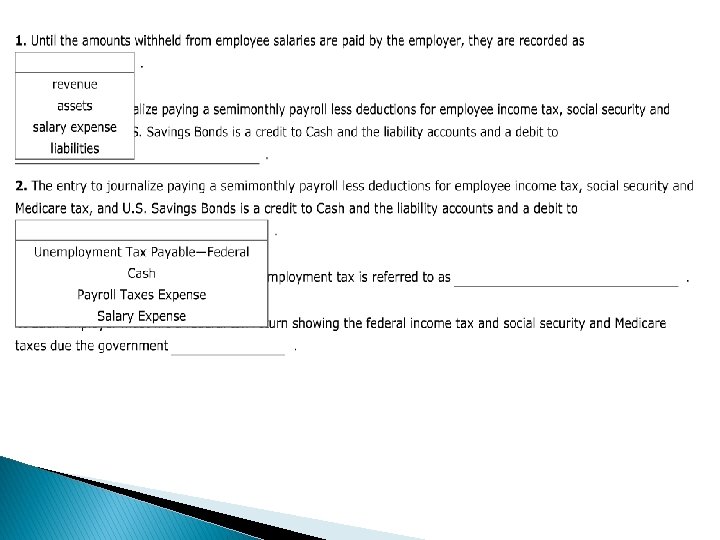

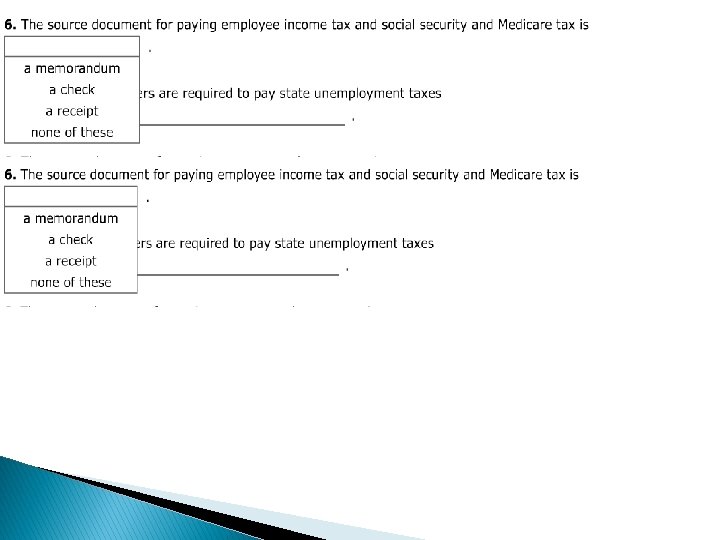

Journalizing Employee Taxes � To journalize the employee taxes (cash payments journal): ◦ Paid cash for semimonthly payroll, $2, 565. 72 (total payroll, $2, 971. 00, less deductions: employee income tax, $178. 00; social security tax, $184. 20; Medicare tax, $43. 08). �Debit to Salary Expense (using the total of the gross pay column of the payroll register) �Salary Expense $2, 971. 00 �Credit to employee income tax payable, social security tax payable, medicare tax payable and cash (total net pay) �Employee Income Tax Payable $178. 00 �Social Security Tax Payable $184. 20 �Medicare Tax Payable $43. 08 �Cash $2, 565. 72 ◦ The source document for payment of payroll is a check

Journalizing Employer Taxes � To journalize the employer taxes (general journal): ◦ Recorded employer payroll tax expense for the semimonthly pay period ended April 15. M 26. � Paid cash for semimonthly payroll, $2, 565. 72 (total payroll, $2, 971. 00, less deductions: employee income tax, $178. 00; social security tax, $184. 20; Medicare tax, $43. 08). � Total earning $2, 971. 00 ◦ The Employer payroll tax expense is journalized on the same date as the employee salary expenses � Credit to social security tax payable, medicare tax payable and federal and state unemployment payable � Social security Tax Payable $184. 20 � Medicare Tax Payable $43. 08 � Unemployment Tax Payable-Federal $23. 77 � Unemployment Tax Payable-State $160. 43 � All of the tax payables are liabilities � Debit to Payroll Tax Expense (total of all of the credits) � Payroll Tax Expense $411. 48 ◦ The source document for journalizing employer payroll taxes is a memo

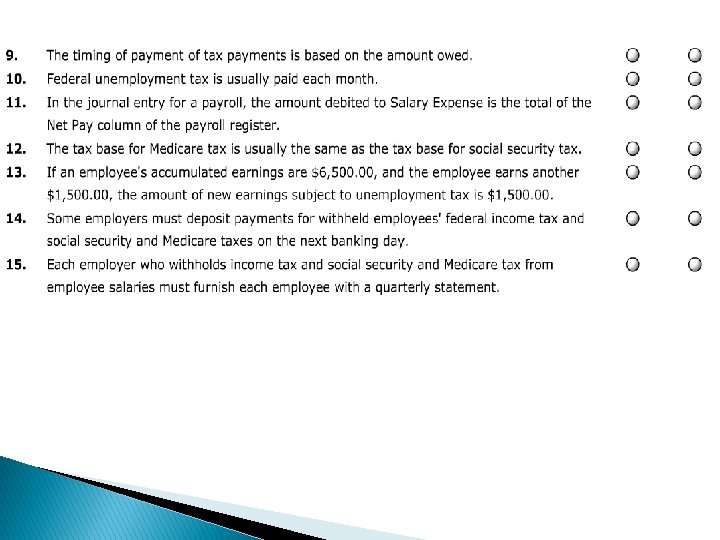

Payment of Taxes � Employee Income, Social Security and Medicare taxes are paid periodically to the federal government in a combined payment ◦ Some employers must pay on the next banking day, others end of the month or semiweekly ◦ Some use the Electronic Federal Tax Payment System (EFTPS)…. not required ◦ Paid cash for liability for employee income tax, $460. 00; social security tax, $757. 90; Medicare tax, $177. 25; total, $1, 395. 15. C 45. �Debit Tax Payables � Employee Income Tax Payable $460. 00 � Social Security Tax Payable $757. 90 � Medicare Tax Payable $177. 25 �Credit Cash � Cash $1, 395. 15

Payment of Unemployment Tax � Unemployment tax payment ◦ Paid quarterly ◦ Paid cash for federal unemployment tax liability for quarter ended March 31, $121. 20. C 47. �Debit to state or federal unemployment tax payable �Unemployment Tax Payable-Federal $121. 20 �Credit to cash �Cash $121. 20 ◦ Source document for paying state/federal unemployment tax is a check

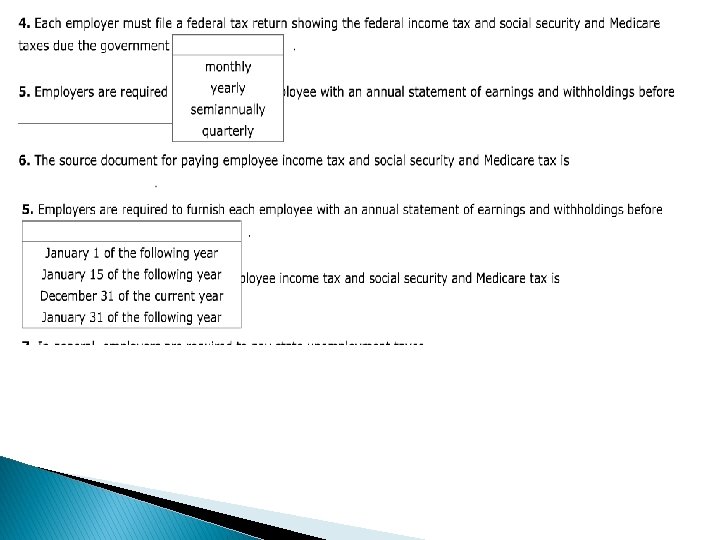

Other Concepts � Each employer is required by law to periodically report the payroll taxes withheld from employee salaries ◦ Each employer who withholds income tax and social security and Medicare tax from employee salaries must furnish each employee with an annual statement �The annual statement of earnings and withholdings must be provided to the employee by January 31 of the following year � The federal tax used for state and federal administrative expenses of the unemployment program is federal income tax