Chapter 12 Work Sheet and Adjusting Entries Chapter

New Adjustments: 1. Adjustment for Supplies 2. Adjustment")

1100 2110 4110")

• Single step")

• Cost of all the goods sold during the")

• Written promises to pay the seller/lender the amount due in")

– Get cash soon •")

accounts with a credit")

- Slides: 79

Chapter 12 Work Sheet and Adjusting Entries

Chapter 12 • Performance Objectives: 1) New Adjustments: 1. Adjustment for Supplies 2. Adjustment for merchandise inventory under the periodic inventory system 3. Adjustment of unearned revenue 2) Complete the work sheet with the new adjustments 3) Journalize the adjusting entries for a merchandising business under the periodic inventory system

Adjustments • Bring the books “up to date” • Adjustments are made every time the financial statements are produced • Each adjustment will affect: • At least one income statement account – Adjusting entries update the I/S accounts so we get a more accurate net income number • At least one balance sheet account – Adjusting entries update the B/S accounts so we get a more accurate A = L + OE

Adjustments: • First – Record adjustments in the worksheet • Be sure to label each adjustment entry into the worksheet with a letter reference: a), b), c)… both sides of the entry! • Second – Record the adjusting journal entries in the general journal

Data for Adjusting Supplies • Debit Supplies when supplies are purchased throughout the period • Take inventory to determine the amount of supplies left at the end of the period • New Adjustment: – Make an adjusting entry for the amount used (total minus amount left) • Debit Supplies Expense • Credit Supplies

New Adjustments: Merchandise Inventory • What is merchandise inventory? • Goods bought with the intention of reselling for a profit • Office supplies are not merchandise inventory Examples: Shoe store? Shoes Kite store? Kites & boomerangs Hardware store? Hammers, lumber, etc.

Periodic Inventory System • The system under which the buying of merchandise during the year is recorded as: – Debit to purchases – Credit to accounts payable or cash • At the end of the period, a physical count of the stock of goods is taken – Adjusting entries are made to record the amount of the physical count

Prepare An Adjustment For Merchandise Inventory Under The Periodic Inventory System • Inventory account sits on books, untouched • Buy inventory during period and record it in “purchases” • At the end of the period, you perform a physical count • Income summary is used during adjustment process – “Put” beginning inventory into income summary (debit) – “Put” physical count number into income summary (credit) – Both numbers show up on face of income statement as part of COGS calculation • Difference shows up as: – “Cost of goods sold” (I/S) – Merchandise inventory (B/S)

New Adjustments: Merchandise Inventory • Step One: • Empty out inventory account – Credit • “Put” it into income summary – Debit • Step Two: • Record the physical count number in inventory account – Debit • “Put” it into income summary – Credit Brings Inventory Balance to Counted Total!

After Recording Adjustment In The Work Sheet, Inventory Adjusting Journal Entry:

Demonstration Problem We will complete a work sheet and make the adjusting journal entries

Empty Inventory Account

Place Counted Inventory Into Merch. Inv. Account

New Adjustments: Unearned Revenue “See both sides of the coin!” One person’s expense is another person’s revenue! • When we buy a one year insurance policy, we record: “prepaid insurance” • When the insurance company receives our check, they record: “unearned insurance revenue” – Each month, we incur 1/12 of it as insurance expense! – Each month, they earn 1/12 of it as insurance – This “updates our accounts” & makes our financial statements more accurate – This “updates their accounts” & makes their financial statements more accurate revenue

Unearned Revenue • If Time Magazine receives subscription revenue for the whole year, can they record it all as revenue in the first month? • No • They must record unearned subscription revenue, and then make adjustments each month • Other examples: – Sports teams receive ticket sales in advance – Health club advance payments

Asset, Liability Or Owner’s Equity? • Unearned revenue? • Time Magazine “owes” the customer the magazines, right? • The insurance company “owes” the customer the insurance coverage, right? • Unearned revenue is a liability! – The customer has a claim against the company for the goods or services until the goods are delivered or the services are rendered

Unearned Revenue • Revenue received in advance for goods or services to be delivered later • Considered to be a liability until the revenue is earned

After Recording Adjustment In The Work Sheet, Unearned Revenue Adjusting Entry: • (Recorded earlier in the year) insurance company receives cash for a one year insurance policy: • Time passes & insurance company earns one months revenue:

Journal Entries & Posting (T-Accounts Demo) 1100 2110 4110

Worksheet • Tool used by accountants to help prepare the financial statements • Chapter 12: – Adjusted trial balance is gone • Why? • Because we can carry the updated account numbers straight to either the: – Income statement column – Balance sheet column

Demonstration Problem We will complete a work sheet and make the adjusting journal entries

Work Sheet

Empty Inventory Account

Place Counted Inventory Into Merch. Inv. Account

Record All Adjustments

Carry Over To I/S Column

Carry Over To B/S Column

Work Sheet

Journal Entries Before Posting

Steps For Completing The Work Sheet 1. Place account totals in trial balance column – Total and rule (DR = CR) 2. Record adjustments in work sheet – Letter references: a), b)… – Total and rule (DR = CR) 3. Place I/S & B/S amounts into I/S and B/S columns, total at bottom (DR ≠ CR)

Steps For Completing The Work Sheet 4. In the income statement column, calculate net income/loss – Subtract the smaller side from the larger side – “Plug” this number to get DR = CR – If there is net income, the credit side of the columns will be larger and you will place net income on the debit side – If there is net loss, the debit side of the columns will be larger and you will place net loss on the credit side

Steps For Completing The Work Sheet 5. In the balance sheet column, calculate net income/loss – Subtracting the smaller side from the larger side – “Plug” this number to get DR = CR

Chapter 13 Financial Statements, Closing Entries, And Reversing Entries

Chapter 13 • Performance objectives: 1. Prepare a classified income statement for a merchandising firm – Net sales – Cost of goods sold – Gross profit – Income from operations 2. Prepare a classified balance sheet for any type of business – Current assets – Plant & equipment – Current liabilities – Long-term liabilities

Chapter 13 • Performance objectives: 3. Compute working capital and current ratio 4. Journalize the closing entries for a merchandising firm 5. Determine which adjusting entries can be reversed, and journalize the reversing entries

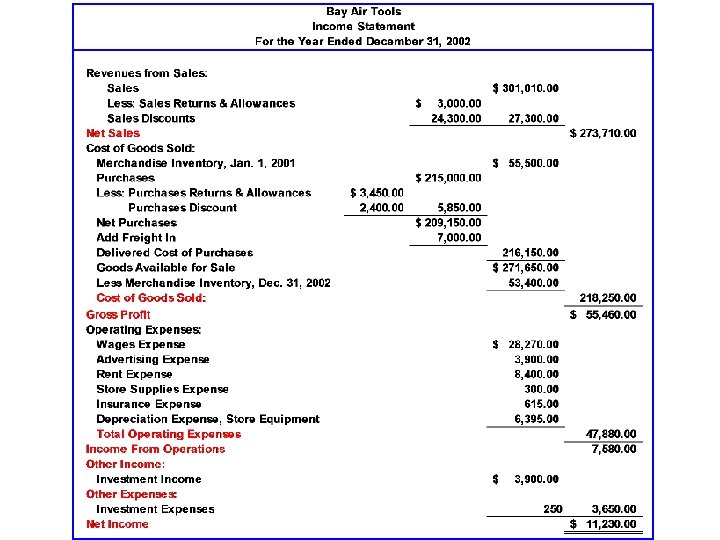

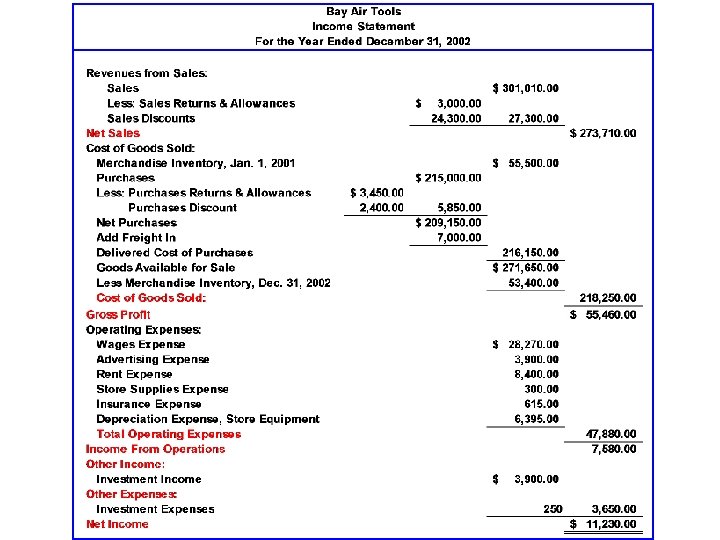

Prepare A Classified Income Statement For Merchandising Co. (“Multi-Step Income Statement”) • Single step income statement • Multi-step income statement

Performance Measures • Different measure on the classified income statement tell us different things: – Gross profit: • How profitable the company is after only subtracting COGS • Common measure used to compare companies (GP%) – Operating income: • How profitable the company is from its ordinary operations, before any “other revenue/expenses” • Common measure used in estimating future profitability – Net income: • The bottom line • Profit for the period

Other Income, Or Expenses • Not related to ordinary operations – Examples: • • Interest revenue Rent Revenue Interest expense Cash Sort & Over – (If Firm decides to classify it as such) – Spa Magic classifies it as such

Template for Classified Income Statement

Calculate Net Sales

Cost Of Goods Sold (COGS) • Cost of all the goods sold during the period • Example: – Shoe store sells shoes and accessories – At the end of the period, the accountants must determine the cost of all the shoes sold during the period in order to match it with the shoe sales revenue

Cost of Goods Sold • Good Diagram on page 457

Calculate COGS

Calculate Gross Profit

Calculate Income From Operations

Calculate Other Income & Expenses

Calculate Net Income

Statement Of Owner’s Equity • After we complete the income statement, we are ready to make the statement of owner’s equity • Preparation is the same as earlier chapters • Look on page 460

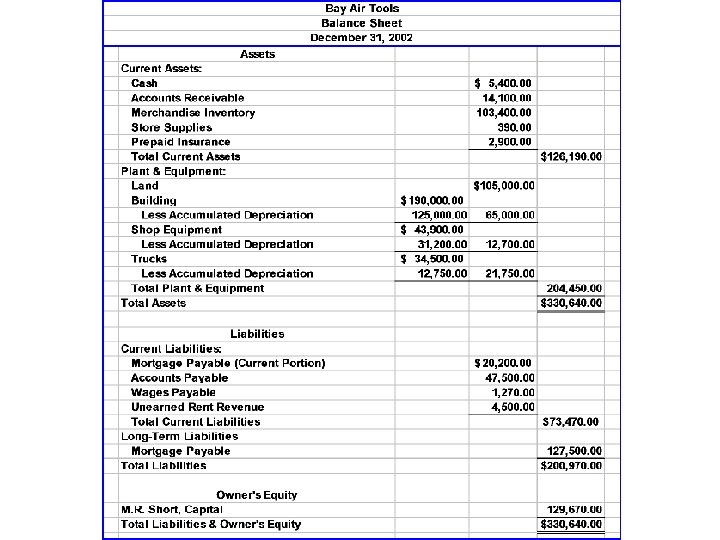

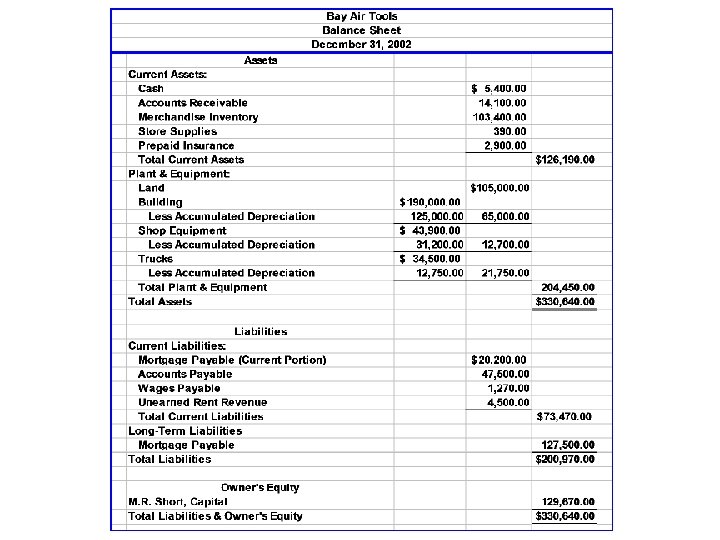

Balance Sheet Classifications • • Current Assets Plant and Equipment Current Liabilities Long-Term Liabilities

Current Assets • Cash and any other assets or resources that are expected to be realized in cash or to be sold or consumed during the normal operating cycle* of the business * One year, if the normal operating cycle is less than twelve months • Listed on balance sheet in the order of liquidity (how quickly can it be converted to cash): – Cash – N/R (current) – A/R – Inventory – Prepaid items (supplies, prepaid insurance)

Notes Receivable (Current) • Written promises to pay the seller/lender the amount due in a period of less than one year

Calculate Current Assets

Plant And Equipment • Long-lived assets that are held for use in the production or sale of other assets or services – Also called fixed assets • Order on Balance Sheet: – Rank according to length of life • Longest life first

Calculate Plant & Equipment & Total Assets

Current Liabilities • Debts that will become due within the normal operating cycle of a business – Usually within one year • Normally paid from current assets • Listed on balance sheet in the order they will be paid off: – Mortgage payable (current portion) – A/P – N/P – Wages payable – Unearned revenue

Calculate Current Liabilities

Long-Term Liabilities • Debts payable over a comparatively long period – Usually more than one year • For sole-proprietorship only LTL: – Mortgage payable (LT portion)

Calculate Total Liabilities & Owner’s Equity

Liquidity • “How quickly an asset can be converted to cash” • The ability of an asset to be quickly turned into cash, either by selling it or by putting it up as security for a loan – Banks want to know if the firm can make its interest payments – Managers want to know if they have enough money to pay the bills and buy assets – Cash is queen! (Cash is king)

Current Assets & Current Liabilities • Current assets (CA) – Get cash soon • Current liabilities (CL) – Pay cash soon • Short term cash management measures (liquidity measures): 1. Working capital 2. Current ratio

Total CA & Total CL

Liquidity Measures: • Current Ratio – A firm’s current assets divided by its current liabilities • Because of the division, the number can be used to compare with other companies – Portrays a firm’s short-term debt-paying ability • Ability to pay current liabilities with current assets • CA/CL = Current Ratio

CA/CL

Liquidity Measures: • Working Capital – A firm’s current assets less its current liabilities – The amount of capital a firm has available to use or to work with during a normal operating cycle • CA – CL = Working Capital

Working Capital

Closing Entries For Merchandising Co. 1. Close all temporary (nominal) accounts with a credit balance (except income summary line) – Debit nominal accounts • – Revenues & contra expenses like purchase discounts Credit income summary 2. Close all temporary (nominal) accounts with a debit balance (except income summary line) – Credit nominal accounts • – Expenses & contra revenues like sales discounts Debit income summary 3. Close income summary to capital 4. Close drawings to capital

Step 1

Step 2

Steps 3 and 4

Reversing Entries • The reverse of certain adjusting entries, recorded as of the first day of the following fiscal period • Make it easier for the accountant next period – Next period the accountant does not need to worry about compound entries for payables and receivables where the cash is paid or is received • The use of reversing entries is optional

Determine Which Adjusting Entries Can Be Reversed 1. Must be first day of the period after you made adjusting entries 2. Look at all adjusting entries and find entries that meet all three qualifications: 1. An asset or liability was increased 2. The asset or liability did not have a previous balance 3. Entry does not involve merchandise inventory or contra accounts 3. Reverse it by making a new journal entry with the reverse debits and credits – • When you post, don’t forget to write “reversing” in item column in the ledger accounts Example

Adjusting Entries

Journalize the Reversing Entries

Posting Reversing Entries to Wages Payable Account

Posting Reversing Entries to Wages Expense Account Notice that posting of $2, 000 wages expense results in an $800 balance.