Chapter 12 Share Capital Distributable Profits and Reduction

Chapter 12 Share Capital, Distributable Profits and Reduction of Capital

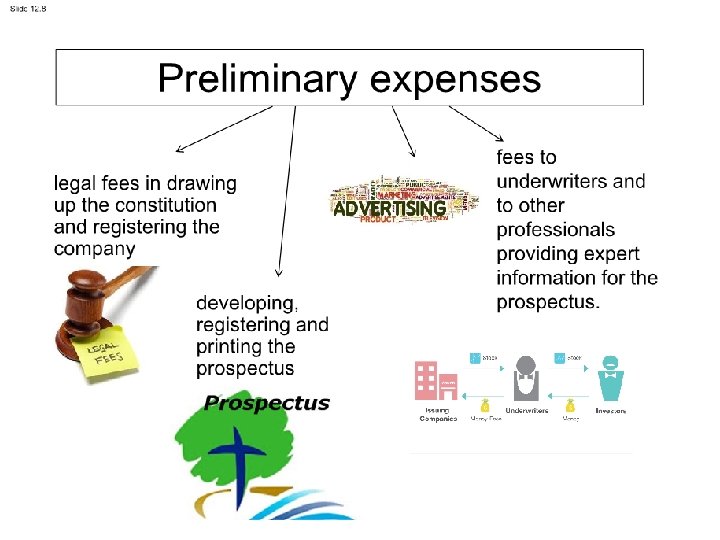

Preliminary expenses • Preliminary expenses should be written off in the Income Statement in the year in which they are incurred. • The journal entries would be: • Preliminary expenses $XXX • Accounts payable $XXX • Being artwork for prospectus • Accounts payable • Bank • Being payment of creditors $XXX

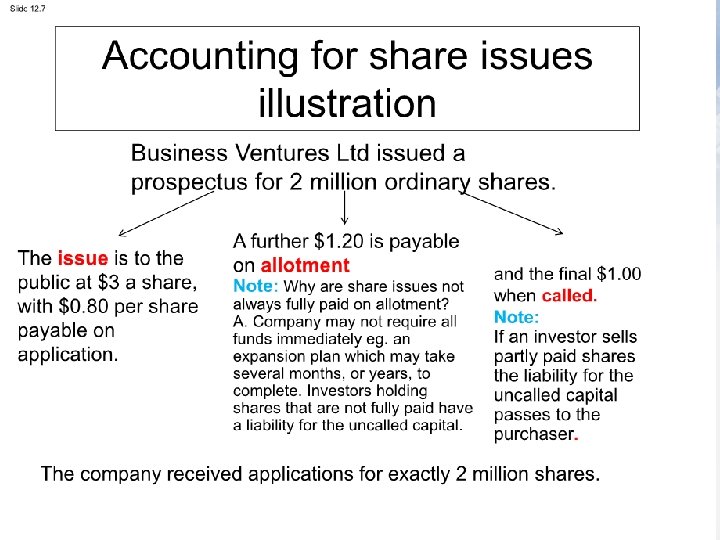

Accounting for share issues • Initial application • investors are not entitled to any shares until the directors make a formal allotment • all share application monies must be held in a trust account • the journal entry is:

• The directors approve and authorise")

Accounting for share issues • Allotment (or issue) • The directors approve and authorise the issue of shares • trust account funds transferred to the company’s general funds.

Accounting for share issues • trust bank account can now be closed • Pay preliminary expenses from net revenue earned on the application monies • Shareholders are liable to pay the second instalment of $1. 20 per share. • The allotment account entry anticipates receipt of this instalment.

When the moniesare received, the entry is:

Accounting for share issues • Why are share issues not always fully paid on allotment? • Company may not require all funds immediately eg. an expansion plan which may take several months, or years, to complete • Investors holding shares that are not fully paid have a liability for the uncalled capital • Calls • If an investor sells partly paid shares the liability for the uncalled capital passes to the purchaser • Instalments after allotment are termed calls

- Slides: 17