Chapter 10 LIABILITIES The Nature of Liabilities Defined

Chapter 10 LIABILITIES

The Nature of Liabilities Defined as debts or obligations arising from past transactions or events. Maturity = 1 year or less Maturity > 1 year Current Liabilities Noncurrent Liabilities I. O. U.

TYPES OF CURRENT LIABILITIES Key features of a current liability: It is expected to be paid from existing current assets or through the creation of other current liabilities It will be paid within one year or the operating cycle, whichever is longer. Notes Payable Accounts Payable Unearned Revenues Accrued Liabilities

Current Liabilities Notes Payable When a company borrows money, a note payable is created. Current Portion of Notes Payable The portion of a note payable that is due within one year, or one operating cycle, whichever is longer. Current Notes Payable Total Notes Payable Noncurrent Notes Payable

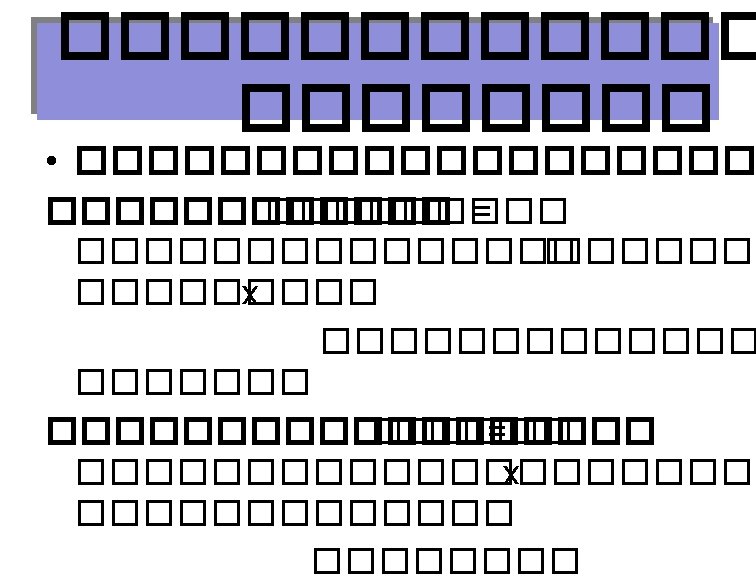

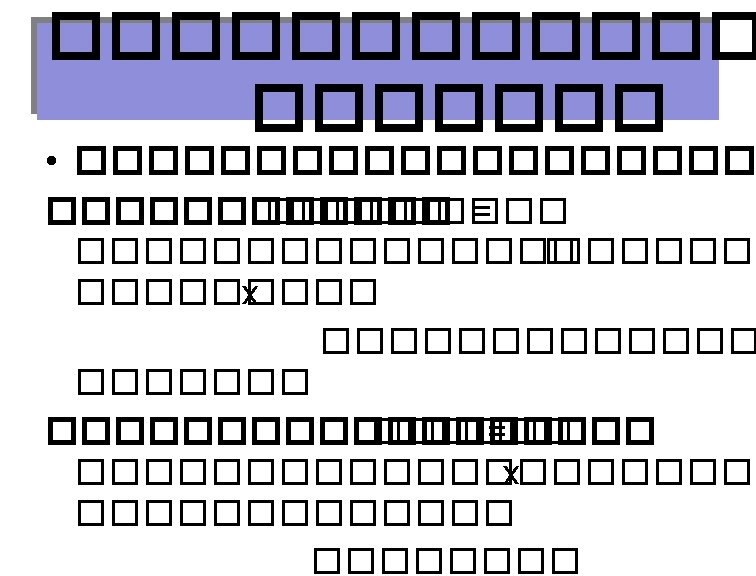

NOTES PAYABLE-����� ISSUANCE DATE General Journal Date Account Titles March 1 Cash Notes Payable Debit Credit 100, 000 Assume First National Bank agrees to lend $100, 000 on March 1, 20 X 1, if Cole Williams Co. 12%, 4 -month note. Assets received = face value of note

INTEREST FORMULA If the loan term is expressed in days, use the number of days divided by 365. If loan term is expressed in months, use the number of months divided by 12. Using the Cole Williams Co. data: Face Value of Note $100, 000 x Annual Interest Rate 12% Time in Terms of One Year x 4/12 = Interest $4, 000

NOTES PAYABLE- ����� INTEREST ACCRUAL General Journal Date Account Titles June 30 Interest Expense Interest Payable Debit Credit 4, 000 If Cole Williams Co. prepares financial statements semiannually, an adjusting entry is required to recognize interest expense and interest payable of $4, 000 at June 30.

NOTES PAYABLE- ����� MATURITY DATE General Journal Date Account Titles July 1 Notes Payable Interest Payable Cash Debit Credit 100, 000 4, 000 104, 000 When the loan is paid, the FACE VALUE is debited, any interest accrued is removed, and cash is decreased by this combined amount.

NOTES PAYABLE-����� ISSUANCE DATE General Journal Date Account Titles March 1 Cash Debit Credit 96, 000 Notes Payable Discount 4, 000 (���������� ( Notes Payable Assume First National Bank agrees to lend $100, 000 on March 1, 20 X 1, 4 -month note. 100, 000

NOTES PAYABLE-����� MATURITY DATE General Journal Date Account Titles July 1 Notes Payable Cash Interest Expense Notes Payable Discount Debit Credit 100, 000 4, 000 When the loan is paid, the FACE VALUE is debited,

Current Liabilities Accounts Payable Short-term obligations to suppliers for purchases of merchandise and to others for goods and services. Office supplies invoices Merchandise inventory invoices Shipping charges Utility and phone bills

OTHER CURRENT LIABILITIES SALES TAXES PAYABLE • Sales tax is expressed as a stated percentage of the sales price on goods sold to customers by a retailer. • The retailer collects the tax from the customer when the sale occurs. Retailer periodically remits the collections to the state’s department of revenue. Retailer is a collection agent for the tax authority.

SALES TAXES PAYABLE SALE DATE General Journal Date Mar. 25 Account Titles Cash Sales Tax Payable Debit Credit 10, 600 10, 000 600 On March 25 th cash register readings for Cooley Grocery show sales of $10, 000 and sales taxes of $600. Sales tax rate = 6%

SALES TAXES PAYABLE SALE DATE PAY TAXES DATE Dr Sales Tax Payable 600 Cr Cash 600 ������

PAYROLL AND PAYROLL TAXES PAYABLE Liabilities relating to employee wages and salaries include: Wages and salaries payable Withholding taxes Date March 7 Account Salaries & Wages Expense Debit Credit 100, 000 Income Taxes Payable 10, 000 Salaries & Wages Payable 90, 000 (record payroll & w/h taxes for week of March 7) March 11 Salaries & Wages Payable Cash (to record payment of March 7 payroll) 90, 000

SALES TAXES PAYABLE PAYROLL AND SALE DATE PAYROLL TAXES PAYABLE Dr Income Taxes Payable 10, 000 Cr Cash 10, 000 ����������

UNEARNED REVENUES Unearned Revenues occur when a company receives cash before a service is rendered. Examples: Airline sells a ticket for future flights Attorney receives legal fees before work is done.

UNEARNED REVENUES CASH RECEIPT General Journal Date Account Titles Aug. 6 Cash Unearned Football Ticket Revenue Debit Credit 500, 000 Superior University sells 10, 000 season football tickets at $50 each for its five-game home schedule.

UNEARNED REVENUES EARNINGS DATE General Journal Date Sept. 7 Account Titles Unearned Football Ticket Revenue Debit Credit 100, 000 As each game is completed, Unearned Football Ticket Revenue is debited for 1/5 of the unearned revenue. The earned revenue, Football Ticket Revenue, is credited.

CURRENT MATURITIES OF LONG-TERM DEBT That portion of long-term debt due within 1 year. Classified as a current liability on the balance sheet

FINANCIAL STATEMENT PRESENTATION

BONDS PAYABLE A form of interest-bearing notes payable issued by corporations, universities, & governmental agencies. Can be sold in small denominations to attract many investors. Sold to obtain long term capital. An alternative to issuing stock.

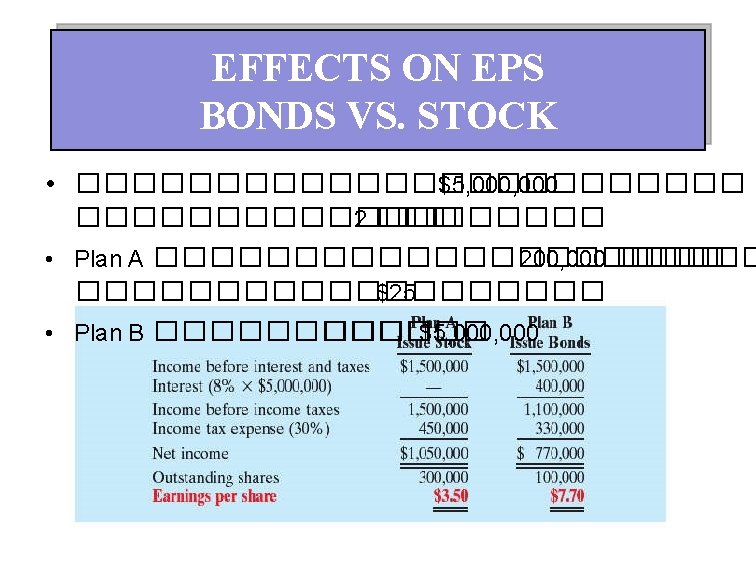

ADVANTAGES OF BOND FINANCING OVER STOCK

BOND ISSUANCE PROCEDURES • Corporate bonds are traded on securities exchanges. • Bond prices are quoted as a percentage of the face value of the bond (usually $1, 000). • Transactions between a bondholder and other investors are not journalized by the issuing corporation. • A corporation records entries when it issues/buys back bonds, and when bondholders convert bonds into stock.

INTEREST RATES AND BOND PRICES Issued when: BOND CONTRACTUAL INTEREST RATE 10% Market Rates Bonds Sell at: 8% Premium 10% Face Value 12% Discount ����������������

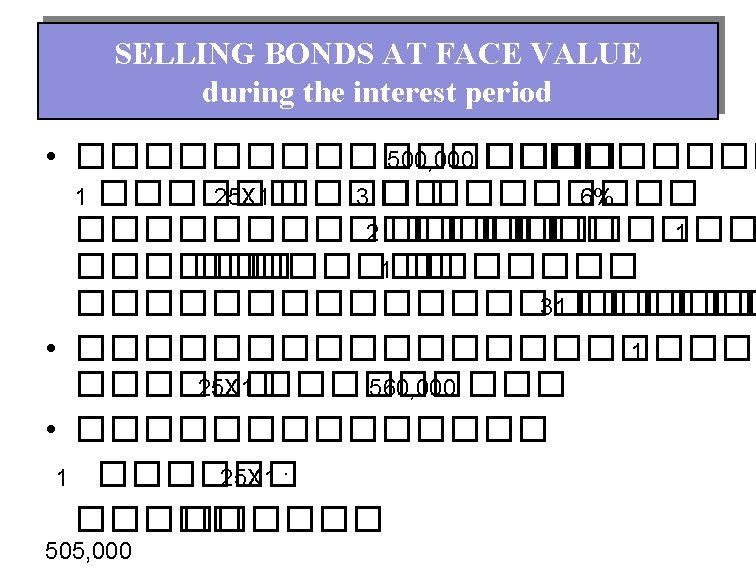

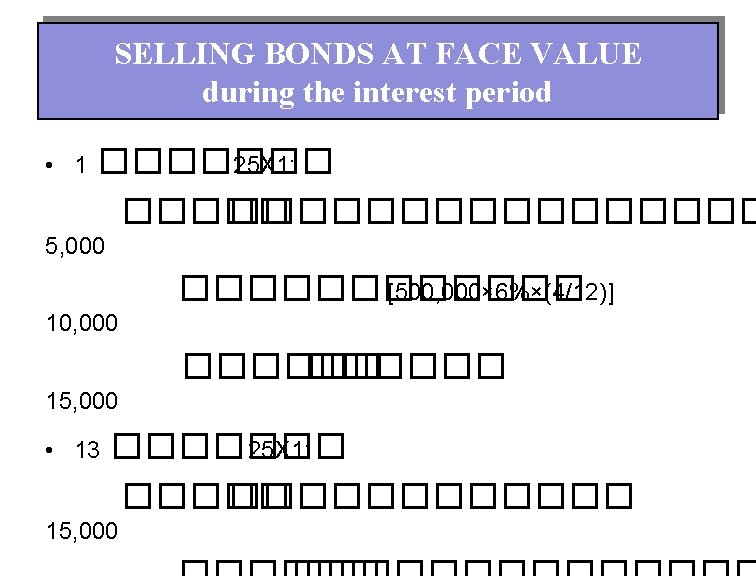

ISSUING BONDS AT FACE VALUE Assume that Devor Corporation issues 1000 10 -year, 9% $1, 000 bonds dated January 1, 20 x 1, at 100 (100% of face value). The entry to record the sale is: Date Jan 1 Account Cash Debit Credit 1, 000 Bonds payable (record sale of bonds at face value) 1000 bonds x $1000 = $1, 000, 000

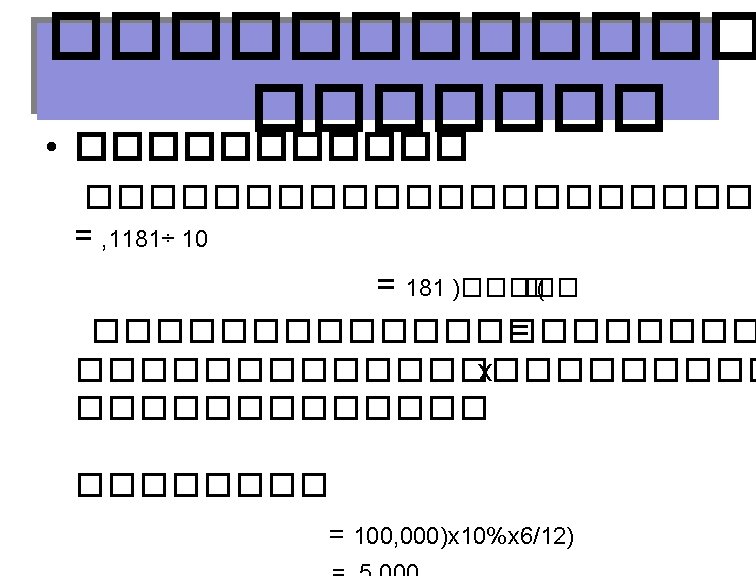

BOND INTEREST PAYMENT Assume that interest is payable semi-annually on January 1 and July 1. Next payment Is due July 1, 20 x 1. The entry is: Date July 1 Account Bond Interest Expense Debit Credit 45, 000 Cash (record semi-annual bond interest payment) $1, 000 x 9% x 6/12 = $45, 000

BOND INTEREST ACCRUAL Assume that interest is payable semi-annually on January 1 and July 1. Next payment Is due Jan 1, 20 x 2. At December 31, 20 x 1 the entry to accrue interest is: Date Dec 31 Account Bond Interest Expense Debit Credit 45, 000 Bond Interest Payable (record sale of bonds at face value) $1, 000 x 9% x 6/12 = $45, 000

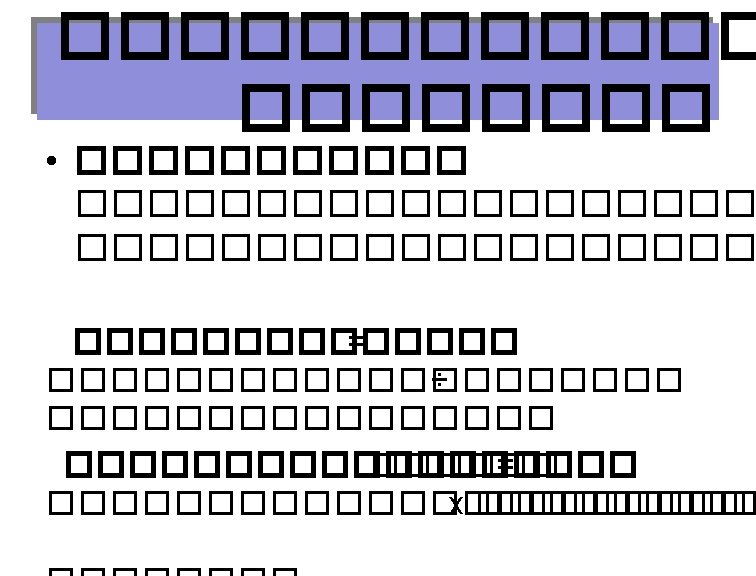

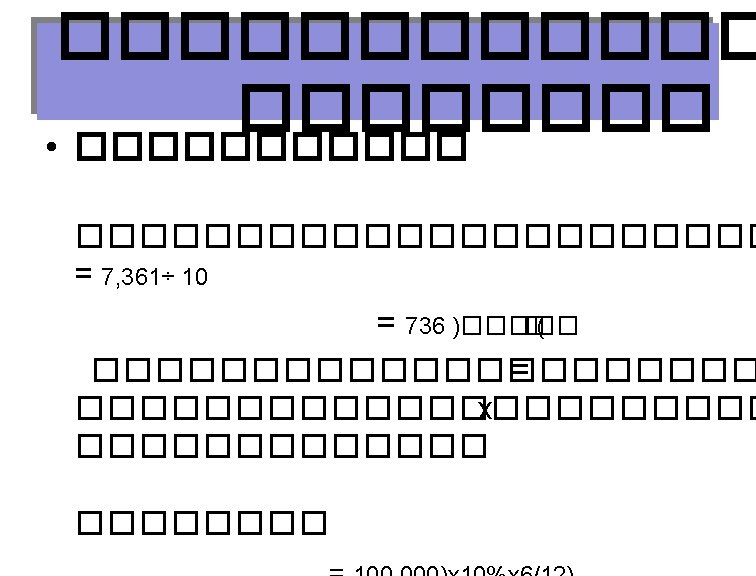

ISSUING BONDS AT A DISCOUNT On January 1, 20 x 1, Candlestick, Inc. sells $100, 000, 5 -year, 10% bonds for $92, 639 with interest payable on July 1 & January 1. The entry to record the issuance is: Date Jan 1 Account Cash Discount on Bonds Debit Credit 92, 639 7, 361 Payable ( Bonds)���������� Payable 100, 000 (record issuance of bonds at a discount) Market value of bonds = $92, 639

FINANCIAL STATEMENT PRESENTATION--DISCOUNT Discount on Bonds Payable is a contra account, which is deducted from bonds payable on the balance sheet: CANDLESTICK, INC. Balance Sheet (partial) Long-term liabilities Bonds payable $100, 000 Less: Discount on Bond Payable $7, 361 $92, 639 Carrying value of bonds = $92, 639 ��������������������������

TOTAL COST OF BORROWING BONDS ISSUED AT A DISCOUNT • The the discount is an additional cost of borrowing that is recorded as bond interest expense over the life of the bonds. • The total cost of borrowing for Candlestick, Inc. , is computed as follows: Bonds Issued at a Discount Semiannual Interest Payments Add: Bond Discount Total Cost of Borrowing xxx 10)%����� ÷(2 xxx 2)%����� ÷(2 xxx 12)%����� ÷(2

ISSUING BONDS AT A PREMIUM On January 1, 20 x 1, Candlestick, Inc. sells $100, 000, 5 -year, 10% bonds for $108, 111 with interest payable on July 1 & January 1. The entry to record the issuance is: Date Jan 1 Account Cash Debit Credit 108, 111 Premium on Bonds 8, 111 Payable ( Bonds)���������� Payable 100, 000 (record issuance of bonds at a premium) Market value of bonds = $108, 111

FINANCIAL STATEMENT PRESENTATION—PREMIUM Premium on Bonds Payable is added to bonds payable on the balance sheet: CANDLESTICK, INC. Balance Sheet (partial) Long-term liabilities Bonds payable $100, 000 Add: Premium on Bonds Payable $8, 111 $108, 111 Carrying value of bonds = $108, 111 �������������������������������

TOTAL COST OF BORROWING BONDS ISSUED AT A PREMIUM The premium is considered to be a reduction in the cost of borrowing that should be credited to Bond Interest Expense over the life of the bonds. Bonds Issued at a Premium Semiannual Interest Payments 10)%����� ÷ (2 Less: Bond Premium 2)%����� ÷(2 Total Cost of Borrowing 8)%����� ÷(2 xx xx xx

������ • ��������������������� � Account ������� Date Debit Credit July 1 Interest Expense Discount on Bonds Payable Cash 5, 736 5, 000

������ • ��������������������� � ����� Date Account Debit Credit Dec 1 Interest Expense Discount on Bonds Payable Interest Payable 5, 736 5, 000

%÷ 2( )Face value ����� �� �������")

������ Date �������� ������ �� ����� ������� 12)%÷ 2( )Face value ����� �� ������� - Discount( �� ������ 01)%÷ 2( ������� �� 7, 361 5, 558. 34 6, 802. 66 92, 639)X 6%( - 5, 558. 34) - 7, 361) (5, 000 (558. 34 92, 639 July 1, 20 x 1 5, 000 93, 197. 34 Dec 31, 20 x 1 5, 000 5, 591. 84 6, 210. 82 93, 789. 18 July 1, 20 x 2 5, 000 5, 627. 35 5, 583. 47 94, 416. 53 Dec 31, 20 x 2 5, 000 5, 664. 99 4, 918. 48 95, 081. 52

������ • ��������������������� � Account ������� Date Debit Credit July 1 Interest Expense Discount on Bonds Payable Cash 5, 558. 34 5, 000

������� • ��������������� � �������� Date Account Debit Credit July 1 Interest Expense Premium on Bonds Payable Cash 4, 189 811 5, 000

)Face value ������������� 01)%÷")

������ � Date ��������� ������ �� ����� ������ (8%÷ 2) )Face value ������������� 01)%÷ 2( ����� ���+ Premium( ���� 8, 111 108, 111 July 1, 20 x 1 5, 000 4, 324. 44 108, 111 X 4%) ( 675. 56 , 000 -5) 4, 324. 44( 7, 435. 44 (8, 111 - 675. 56) 107, 435. 44 Dec 31, 20 x 1 5, 000 4, 297. 42 702. 58 6, 732. 86 106, 732. 86 July 1, 20 x 2 5, 000 4, 269. 31 730. 69 6, 002. 17 106, 002. 17 Dec 31, 20 x 2 5, 000 4, 240. 09 759. 91 5, 242. 26 105, 242. 26

������� • ��������������������� � �������� Date Account Debit Credit July 1 Interest Expense Premium on Bonds Payable Cash 4, 324. 44 675. 56 5, 000

REDEEMING BONDS AT MATURITY Book value of the bonds at maturity will equal their face value. The entry to record the redemption of the Candlestick bonds at maturity is: Date Account Maturity date Bonds Payable Debit Credit 100, 000 Cash (record payment of bonds at maturity) This assumes all interest has been paid to maturity. The entry will be the same regardless of whether The bonds were issued at face value, discount, or premium 100, 000

LONG-TERM NOTES PAYABLE • • Terms exceed one year. May be secured by a specific assets (mortgage). Mortgage N/P are recorded initially at face value. Subsequent entries required for installment payments. Porter Technology Inc. issues a $500, 000, 12%, 20 -year mortgage note on December 31, 20 x 1, to build a research lab. The terms provide for semiannual installment payment of $33, 231. The installment payment schedule for the first year is shown below: Semiannual Interest Period (A) Cash Payment (B) Interest Expense (D) x 6% Issue date (C) Reduction Of Principal (A) – (B) (D) Principal Balance (D) –(C) $500, 000 1 33, 231 $30, 000 $3, 231 496, 769 2 $33, 231 29, 806 3, 425 493, 344

LONG-TERM NOTES PAYABLE JOURNAL ENTRIES The entries to record the issuance and first interest payment are: Date Dec 31 Account Cash Debit Credit 500, 000 Mortgage Notes Payable 500, 000 (record mortgage loan) June 30 Interest Expense Mortgage Notes Payable Cash (record first installment payment) 30, 000 3, 231 33, 231

PRESENTATION & ANALYSIS The long-term liabilities for LAX Corporation are shown below: LAX Corporation Balance Sheet (partial) Long-term liabilities $1, 000 Bonds payable 10% due in 2012 80, 000 $920, 000 Less: Discount on bonds payable Mortgage notes payable, 11%, due in 2018 500, 000 and secured by plant assets 540, 000 Lease liability $1, 960, 000 Total long-term liabilities

End of Chapter 10

- Slides: 62