Chapter 1 What Is Economics Chapter 1 What

- Slides: 104

Chapter 1 What Is Economics?

Chapter 1: What is Economics? Lesson 1: Scarcity and the Science of Economics Students will know: ● Societies do not have enough productive resources to satisfy everyone’s wants and needs, so they must make choices about what, how, and for whom to produce. ● The value of a good or service depends on its scarcity and utility Students will be able to: ● Explain why all societies face the problem of scarcity. ● Categorize the various types of goods and services. ● Identify three basic choices that are faced by all societies. ● Summarize the four reasons people study economics.

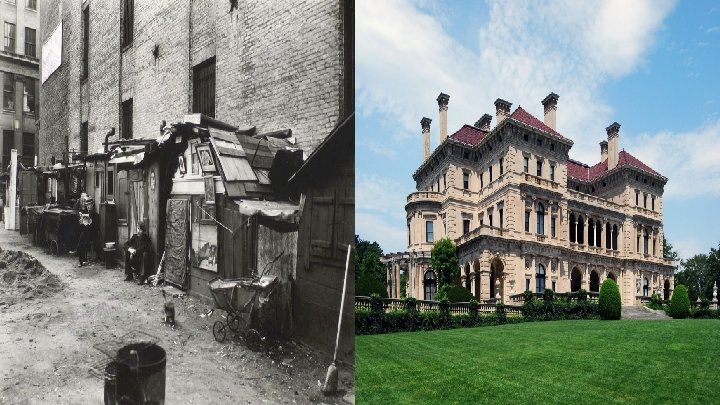

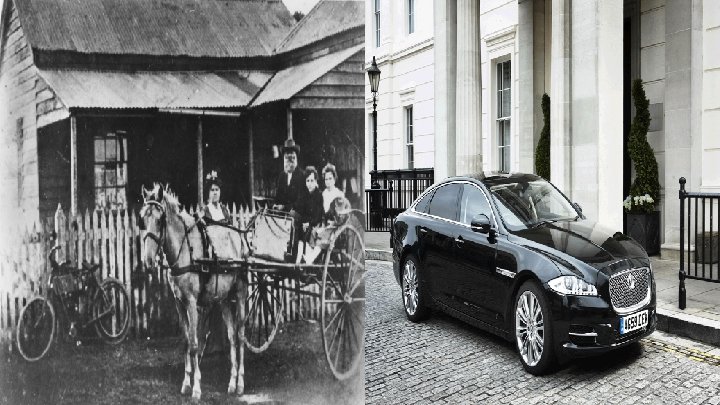

Lesson 1: Scarcity and the Science of Economics ● Economics is the social science dealing with how people satisfy seemingly unlimited and competing wants and needs with the careful use of limited resources. ● Scarcity is the fundamental problem of meeting people’s virtually unlimited needs and wants with limited resources. Not enough resources available on this earth to meet all the wants we have. ● What effect do limited resources and unlimited wants have on the economy? ○ They create scarcity. ● Get with a partner and look at figure 1. 1 on page 7 of your textbook. Answer the question under Critical Thinking: How does this picture illustrate scarcity?

Lesson 1: Scarcity and the Science of Economics ● Needs vs. Wants ○ A need is a basic requirement for survival, such as food, water, clothing, and shelter. ○ A want is something we would like to have, but is not necessary for survival.

Lesson 1: Scarcity and the Science of Economics ● Goods vs. Services ○ A good is a useful, tangible item that can be used to satisfy a need or want. (ex: books, cars, MP 3 player, Iphone) ○ A service is work performed for someone to satisfy a need or want. (ex: haircuts, home repairs, car repairs, doctors, lawyers, and teachers) ○ The difference between a good and a service is that a good is tangible and a service is not.

Lesson 1: Scarcity and the Science of Economics ● Types of Goods ○ ○ Durable goods are tangible items that are designed to last three years or more when used on a regular basis. (ex: tools, tractors, cars, washing machines, clothes dryer, refrigerator) Nondurable goods are tangible items that last for fewer than three years when used on a regular basis. (ex: food, writing paper, clothes) Consumer goods are tangible items intended for final use by individuals. (ex: clothes, shoes, food, car) Capital goods are tangible items intended for final use by businesses. (ex: machinery, equipment that is used by businesses to produce other products or services) ● Most goods and services have value, a term that refers to a worth that can be expressed in dollars and cents.

Lesson 1: Scarcity and the Science of Economics ● Paradox of Value is an apparent contradiction between the necessity of an item and its value. ○ ○ Necessities such as water and air have very low monetary value Non Necessities such as diamonds have a very high monetary value ● Utility is the capacity a good or service has to be useful and provide satisfaction. ● Discuss with a partner: Why do you think some goods and services are more valuable than others? ○ To have monetary value, a good must be scarce and have utility for the person purchasing it. Some goods that have utility are more scarce than others, which makes them more valuable (more expensive).

Lesson 1: Scarcity and the Science of Economics ● Wealth is the accumulation of items that are tangible, are scarce, have utility, and are transferable from one person to another. ○ ○ A nation’s wealth comprises all tangible items--including natural resources, factories, stores, houses, motels, theaters, furniture, clothing, books, highways video games, and even basketballs--that can be exchanged. Wealth excludes services because they are not tangible. ● TINSTAAFL--There is no such thing as a free lunch! ○ ○ ○ Because resources are limited, everything we do has a cost--even when it seems as if we are getting something “for free. ” Discuss with a partner: Do you really get a free meal when you use a “buy one get one free” coupon? The business that gives it away still has to pay for the resources that went into the meal, so it usually tries to recover these costs by charging more for its other products.

Lesson 1: Scarcity and the Science of Economics ● The Three Basic Economic Questions ○ ○ ○ What to Produce ■ Should a society direct its resources to make capital goods or consumer goods? ■ A society cannot produce everything its people want. ■ In some countries this decision is made by the government. ■ In other countries, spending decisions made by consumers largely determine where resources are directed. How to Produce ■ Should a factory owner use automated production methods that require more machines and fewer workers, or should they use fewer machines and more workers? ■ Automation can lower production costs making the price of goods less ■ If unemployment is too high there is no one who can afford the cheaper goods For Whom to Produce ■ Does a society produce items for the wealthy, the middle class, or the poor? ■ If the supply of an item is too low, who will receive the existing supply?

Lesson 1: Scarcity and the Science of Economics ● The Scope of Economics ○ ○ ○ Economics is the study of human efforts to satisfy seemingly unlimited and competing wants through the careful use of relatively scarce resources. Economics is a social science because it deals with the behavior of people as they deal with this basic issue. The four key elements of this study are description, analysis, explanation, and prediction.

Lesson 1: Scarcity and the Science of Economics ● The Scope of Economics ○ The four key elements of this study are description, analysis, explanation, and prediction. ■ Description: ● One part of economics describes economic activity ○ Gross Domestic Product is the monetary value of all final goods, services, and structures produced within a nation’s borders in a 12 month period. ● Economics also describes jobs, prices, trade, taxes, and government spending ■ Analysis: ● Economics analyzes the economic activity that it describes. ○ Why are prices for some items higher than others? Why do some people earn higher incomes than others? ■ Explanation: ● After economists analyze a problem and understand why and how things work, they need to communicate this knowledge to others. ■ Prediction: ● Economics studies both what is happening now and what might happen in the future.

Lesson 1: Scarcity and the Science of Economics ● With a partner read and discuss the cartoon on page 12. Explain how this man’s lunch may not have been truly “free, ” even if he didn’t have to hand over any money today.

Lesson 1: Scarcity and the Science of Economics ● Lesson 1 Review: ○ What effect do limited resources and unlimited wants have on the economy?

Lesson 1: Scarcity and the Science of Economics ● Lesson 1 Review: ○ What effect do limited resources and unlimited wants have on the economy? ■ They create scarcity

Lesson 1: Scarcity and the Science of Economics ● Lesson 1 Review: ○ Why do all societies face the problem of scarcity?

Lesson 1: Scarcity and the Science of Economics ● Lesson 1 Review: ○ Why do all societies face the problem of scarcity? ■ All people want more than they have

Lesson 1: Scarcity and the Science of Economics ● Lesson 1 Review: ○ What is the difference between a need and a want?

Lesson 1: Scarcity and the Science of Economics ● Lesson 1 Review: ○ What is the difference between a need and a want? ■ A need is a basic requirement for survival. A want is something we would like to have, but it is not necessary for survival.

Lesson 1: Scarcity and the Science of Economics ● Lesson 1 Review: ○ Who is credited with being the “Father of Economics”?

Lesson 1: Scarcity and the Science of Economics ● Lesson 1 Review: ○ Who is credited with being the “Father of Economics”? ■ Adam Smith, who wrote The Wealth of Nations in 1776. He believed that an economy would function optimally if the government did not control the economy and individuals were allowed to act in his or her own “rational self-interest”, which would act as an invisible hand in shaping the market.

Lesson 1: Scarcity and the Science of Economics ● Lesson 1 Review: ○ What effect do limited resources and unlimited wants have on the economy?

Lesson 1: Scarcity and the Science of Economics ● Lesson 1 Review: ○ What effect do limited resources and unlimited wants have on the economy? ■ They create scarcity and force societies to make choices

Lesson 1: Scarcity and the Science of Economics ● Lesson 1 Review: ○ Why are societies faced with the three basic questions of WHAT, HOW, and FOR WHOM?

Lesson 1: Scarcity and the Science of Economics ● Lesson 1 Review: ○ Why are societies faced with the three basic questions of WHAT, HOW, and FOR WHOM? ■ We live in a world or relatively scarce resources and we have to make choices regarding how to use those resources

Lesson 1: Scarcity and the Science of Economics ● Lesson 1 Review: ○ Why is economics considered to be a social science?

Lesson 1: Scarcity and the Science of Economics ● Lesson 1 Review: ○ Why is economics considered to be a social science? ■ Economics deals with the behavior of people as they deal with the basic issue of scarcity

Chapter 1: What is Economics? Lesson 2: Our Economic Choices Students will know: ● ● ● Land, labor, capital, and entrepreneurship are the four factors necessary to produce goods and services. Entrepreneurs take the risk to combine productive resources (land, labor, capital, entrepreneurship) to produce goods and services. How a production possibilities curve can be used to determine the most efficient allocation of resources. Students will be able to: ● ● ● Explain the four basic factors of production. Identify production alternatives using a production possibilities curve. Explain the concept of opportunity cost, including the opportunity cost of idle resources. Evaluate trade-offs and opportunity costs to choose wisely or make the best decision. List the rights and responsibilities of consumers.

Lesson 2: Our Economic Choices ● The economy is made up of two broad groups: ○ ○ ● The Factors of Production (CELL) - Often referred to as resources ○ ○ ● Producers - those who use the factors of production to produce goods and services Consumers - those who buy goods and services for final use Capital - sometimes called capital goods: tools, machinery, equipment, and factories used in the production of goods and services Entrepreneurs - risk-takers in search of profits who do something new with existing resources ■ Often thought of as being the driving force in an economy because they are the ones who start new businesses, or bring new products to market Land - “gifts of nature”, or natural resources not created by people ■ Soil, sand, plants, trees, mineral deposits, livestock, sunshine, air, climate Labor - People with all their efforts, abilities, and skills What would happen if one of the factors of production were missing?

Lesson 2: Our Economic Choices ● Production Possibilities ○ Since all resources are limited, choices have to be made as to how an economy will utilize their resources. ● Production Possibilities Curve ○ Also called the frontier, is a diagram that represents possible combinations of goods and services an economy can produce when all its resources are in use (full employment does not actually mean all resources, more on this later)

Lesson 2: Our Economic Choices ● Production Possibilities ○ Since all resources are limited, choices have to be made as to how an economy will utilize their resources. ● Production Possibilities Curve ○ Also called the frontier, is a diagram that represents possible combinations of goods and services an economy can produce when all its resources are in use (full employment does not actually mean all resources, more on this later) Capital Goods Consumer Goods

Lesson 2: Our Economic Choices ● Production Possibilities ○ Since all resources are limited, choices have to be made as to how an economy will utilize their resources. ● Production Possibilities Curve ○ Also called the frontier, is a diagram that represents possible combinations of goods and services an economy can produce when all its resources are in use (full employment does not actually mean all resources, more on this later) Capital Goods Any point inside the frontier represents an economy that is inefficient, not utilizing its resources to their fullest extent A inefficient Consumer Goods

Lesson 2: Our Economic Choices ● Production Possibilities ○ Since all resources are limited, choices have to be made as to how an economy will utilize their resources. ● Production Possibilities Curve ○ Also called the frontier, is a diagram that represents possible combinations of goods and services an economy can produce when all its resources are in use (full employment does not actually mean all resources, more on this later) Capital Goods A B Any point on the frontier represents an economy at “full employment” of its resources (approximately 5% unemployment of labor and 20% unemployment of other resources Efficient Inefficient Consumer Goods

Lesson 2: Our Economic Choices ● Production Possibilities ○ Since all resources are limited, choices have to be made as to how an economy will utilize their resources. ● Production Possibilities Curve ○ Also called the frontier, is a diagram that represents possible combinations of goods and services an economy can produce when all its resources are in use (full employment does not actually mean all resources, more on this later) Capital Goods A B C Overextended Any point just outside the frontier represents an economy that is overextended. An economy can produce outside the frontier for a short period of time, but puts undue pressure on its resources and can cause damage to itself. Efficient Inefficient Consumer Goods

Lesson 2: Our Economic Choices ● Production Possibilities ○ Since all resources are limited, choices have to be made as to how an economy will utilize their resources. ● Production Possibilities Curve ○ Also called the frontier, is a diagram that represents possible combinations of goods and services an economy can produce when all its resources are in use (full employment does not actually mean all resources, more on this later) Capital Goods A C B Overextended Efficient Inefficient D Unattainable for now Consumer Goods A point at which all of an economy’s resources are employed is as far as an economy can theoretically produce. Any point beyond that is called unattainable for now. Once new resources are discovered, new technology is introduced, or new efficiencies are discovered and implemented, the frontier shifts to the right and a new frontier is established.

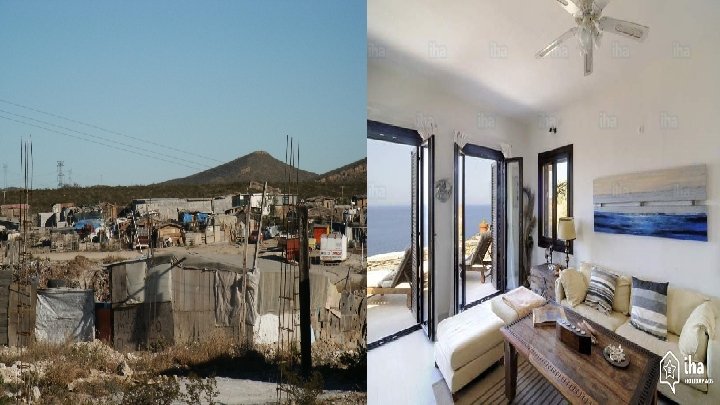

Lesson 2: Our Economic Choices ● Opportunity Cost ○ ○ ○ The value of the next best alternative given up Opportunity cost applies to all activities and is not always measured in dollars and cents For example, you need to balance the amount of time you spend doing homework and the time you spend with your friends. If you decide to spend an extra hour on your homework, the opportunity cost will be the time you could have spent with your friends If you have a number of “trade-offs” available whenever you make a decision, the opportunity cost is always the value of the next best alternative that you give up Get with a partner and look at figure 1. 3 on page 16. Discuss the answer to the Critical Thinking question. A production possibilities frontier indicates the maximum combinations of goods and services that can be produced. However, a firm will eventually have to choose a combination of two points. Choosing only two points on or inside the frontier must be decided because a firm’s resources are limited.

Lesson 2: Our Economic Choices ● Opportunity Cost ○ ○ ○ The value of the next best alternative given up Opportunity cost applies to all activities and is not always measured in dollars and cents For example, you need to balance the amount of time you spend doing homework and the time you spend with your friends. If you decide to spend an extra hour on your homework, the opportunity cost will be the time you could have spent with your friends If you have a number of “trade-offs” available whenever you make a decision, the opportunity cost is always the value of the next best alternative that you give up Get with a partner and look at figure 1. 4 on page 17. Discuss the answer to the Critical Thinking question.

Lesson 2: Our Economic Choices Get with a partner and look at figure 1. 4 on page 17. Discuss the answer to the Critical Thinking question. When the production of one item increases, the production of another must decrease. At point c, production is all clothing and no cars, thus the opportunity cost is what was given up in order to produce the additional units of clothing. For example, if the initial point was point a, and clothing production moved to point c, the opportunity cost of clothing at point c is 70 units of cars

Lesson 2: Our Economic Choices Guns 0 2 4 6 8 10 12 Bombs 6 5 4 3 2 1 0 The economy represented in this Production Possibilities Schedule produces only guns and bombs. Draw a Production Possibilities Curve using the data in this table

Lesson 2: Our Economic Choices Guns 12 10 0 2 4 6 8 10 12 Bombs 6 5 4 3 2 1 0 If this economy is currently producing 12 guns and 0 bombs: a. The opportunity cost of increasing production of bombs from 0 to one bomb is the loss of ____ guns. 8 6 4 2 0 Guns 1 2 3 4 5 6 Bombs

Lesson 2: Our Economic Choices Guns 12 10 0 2 4 6 8 10 12 Bombs 6 5 4 3 2 1 0 If this economy is currently producing 12 guns and 0 bombs: a. The opportunity cost of increasing production of bombs from 0 to one bomb is the loss of ___2_____ guns. 8 6 4 2 0 Guns 1 2 3 4 5 6 Bombs

Lesson 2: Our Economic Choices Guns 12 10 0 2 4 6 8 10 12 Bombs 6 5 4 3 2 1 0 If this economy is currently producing 12 guns and 0 bombs: a. The opportunity cost of increasing production of bombs from 0 to one bomb is the loss of ___2_____ guns. b. The opportunity cost of increasing production of bombs from 1 to 2 bombs is the loss of ____ guns. 8 6 4 2 0 Guns 1 2 3 4 5 6 Bombs

Lesson 2: Our Economic Choices Guns 12 10 0 2 4 6 8 10 12 Bombs 6 5 4 3 2 1 0 If this economy is currently producing 12 guns and 0 bombs: a. The opportunity cost of increasing production of bombs from 0 to one bomb is the loss of ___2_____ guns. b. The opportunity cost of increasing production of bombs from 1 to 2 bombs is the loss of ___2_____ guns. 8 6 4 2 0 Guns 1 2 3 4 5 6 Bombs

Lesson 2: Our Economic Choices Guns 12 10 0 2 4 6 8 10 12 Bombs 6 5 4 3 2 1 0 If this economy is currently producing 12 guns and 0 bombs: a. The opportunity cost of increasing production of bombs from 0 to one bomb is the loss of ___2_____ guns. b. The opportunity cost of increasing production of bombs from 1 to 2 bombs is the loss of ___2_____ guns. c. The opportunity cost of increasing production of bombs from 2 to 3 bombs is the loss of ____ guns. 8 6 4 2 0 Guns 1 2 3 4 5 6 Bombs

Lesson 2: Our Economic Choices Guns 12 10 0 2 4 6 8 10 12 Bombs 6 5 4 3 2 1 0 If this economy is currently producing 12 guns and 0 bombs: a. The opportunity cost of increasing production of bombs from 0 to one bomb is the loss of ___2_____ guns. b. The opportunity cost of increasing production of bombs from 1 to 2 bombs is the loss of ___2_____ guns. c. The opportunity cost of increasing production of bombs from 2 to 3 bombs is the loss of ___2_____ guns. 8 6 4 2 0 Guns 1 2 3 4 5 6 Bombs

Lesson 2: Our Economic Choices Guns 12 10 0 2 4 6 8 10 12 Bombs 6 5 4 3 2 1 0 If this economy is currently producing 12 guns and 0 bombs: a. The opportunity cost of increasing production of bombs from 0 to one bomb is the loss of ___2_____ guns. b. The opportunity cost of increasing production of bombs from 1 to 2 bombs is the loss of ___2_____ guns. c. The opportunity cost of increasing production of bombs from 2 to 3 bombs is the loss of ___2_____ guns. d. The opportunity cost of increasing production of guns from 6 to 8 guns is the loss of _____ bombs. 8 6 4 2 0 Guns 1 2 3 4 5 6 Bombs

Lesson 2: Our Economic Choices Guns 12 10 0 2 4 6 8 10 12 Bombs 6 5 4 3 2 1 0 If this economy is currently producing 12 guns and 0 bombs: a. The opportunity cost of increasing production of bombs from 0 to one bomb is the loss of ___2_____ guns. b. The opportunity cost of increasing production of bombs from 1 to 2 bombs is the loss of ___2_____ guns. c. The opportunity cost of increasing production of bombs from 2 to 3 bombs is the loss of ___2_____ guns. d. The opportunity cost of increasing production of guns from 6 to 8 guns is the loss of ____1_____ bombs. 8 6 4 2 0 Guns 1 2 3 4 5 6 Bombs

Lesson 2: Our Economic Choices ● Trade-offs - alternative choices that are given up in favor of the choice we select ● Producers are not the only ones that face opportunity costs ● Decision Making Grid - a good way to analyze an economic problem because it forces you to consider a number of alternatives and the criteria you will use to evaluate the alternatives. ○ It forces you to evaluate each alternative on the basis of the criteria you select ● Consumers deal with the scarcity of items frequently, especially when a new electronics gadget first comes on the market. Long lines at electronic stores occur and people even camp out overnight in front of the stores to make sure that when the stores open with the new gadget for sale, they will get one of those gadgets.

Lesson 2: Our Economic Choices Decision Making Grid Criteria/ Alternative Buy used motorcycle Go to prom in spring Take a trip during spring break Buy a new computer Will not require further expenditures Will probably last a long time Will impress friends Does not require parental approval Can be used multiple times

Lesson 2: Our Economic Choices Decision Making Grid Criteria/ Alternative Will not require further expenditures Will probably last a long time Will impress friends Buy used motorcycle X X Go to prom in spring X X Take a trip during spring break Buy a new computer X X Does not require parental approval Can be used multiple times X X X

Lesson 2: Our Economic Choices ● Consumer Rights ○ ○ Consumers as a whole help decide WHAT producers should make, and therefore where a nation will be on it production possibilities curve In 1962, consumers were given some protection against manufacturers and other consumer rights have been added since ■ The right to safety ■ The right to be informed ■ The right to choose ■ The right to be heard ■ The right to redress

Lesson 2: Our Economic Choices ● Consumer Responsibilities ○ ○ ○ Include important details and copies of receipts, guarantees, and contracts to support case Report the problem immediately. Do not try to fix a product yourself because doing so may cancel the warranty If you need to contact the manufacturer in writing, type your letter or sent an email directly and keep a copy Keep cool. The person who will help you solve you problem is probably not responsible for causing the problem Keep an accurate record of your efforts to get the problem solved. Include the names of people you have spoken to or written to and the dates on which you communicated

Lesson 2: Our Economic Choices ● Lesson 2 Review: ○ What would happen if one of the factors of production were missing?

Lesson 2: Our Economic Choices ● Lesson 2 Review: ○ What would happen if one of the factors of production were missing? ■ There would be an increased scarcity of products

Lesson 2: Our Economic Choices ● Lesson 2 Review: ○ If you wanted to play in the marching band play on the football team and you chose to play in the marching band, what would be your opportunity cost?

Lesson 2: Our Economic Choices ● Lesson 2 Review: ○ If you wanted to play in the marching band play on the football team and you chose to play in the marching band, what would be your opportunity cost? ■ Playing on the football team

Lesson 2: Our Economic Choices ● Lesson 2 Review: ○ If you wanted to play in the marching band, play on the football team, and get a job, in that order, and you chose to get a job, what would be your opportunity cost?

Lesson 2: Our Economic Choices ● Lesson 2 Review: ○ If you wanted to play in the marching band, play on the football team, and get a job, in that order, and you chose to get a job, what would be your opportunity cost? ■ Playing in the marching band

Lesson 2: Our Economic Choices ● Lesson 2 Review: ○ How can the production possibilities frontier be used to illustrate economic growth?

Lesson 2: Our Economic Choices ● Lesson 2 Review: ○ How can the production possibilities frontier be used to illustrate economic growth? ■ The production possibilities frontier represents various combinations of goods and services an economy can produce when all its resources are in use. An economy’s growth is illustrated by moving the frontier outward.

Lesson 2: Our Economic Choices ● Lesson 2 Review: ○ How do you think our society would be different if citizens did not study economics?

Lesson 2: Our Economic Choices ● Lesson 2 Review: ○ How do you think our society would be different if citizens did not study economics? ■ Consumers would probably make many bad economic decisions and producers would not produce goods and services that consumers wanted

Chapter 1: What is Economics? Lesson 3: Using Economic Models Students will know: ● ● Productivity is the most important factor to economic growth. The economic activity in markets connects individuals and businesses. Effective decision making requires comparing the additional costs of alternatives with the additional benefits. Simple economic models can be used to understand complex economic systems. Students will be able to: ● ● ● Describe the importance of economic growth and the factors that make economic growth possible. Compare the factor market and the labor market and their roles in the circular flow of economic activity. Discuss the use of economic models to explain economic activity. Analyze the benefits of an action or plan using a cost-benefit analysis. Explain how the study of economics can help people make better economic choices.

Lesson 3: Using Economic Models Economic Growth occurs when a nation’s total output of goods and services increases over time Economic growth is important for two main reasons ● Scarcity - everybody currently wants more goods and services than they can have now ● Population growth - there will be more people wanting goods and services to satisfy their wants in the future Economic Growth

Lesson 3: Using Economic Models Six characteristics that affect economic growth Economic Growth

Lesson 3: Using Economic Models Six characteristics that affect economic growth Risk and Sacrifice Economic Growth

Lesson 3: Using Economic Models Six characteristics that affect economic growth Risk and Sacrifice Economic Growth Economic growth requires investments today that may or may not pay off in the future. Sacrifice requires not consuming today in order to have the ability to consume tomorrow.

Lesson 3: Using Economic Models Six characteristics that affect economic growth Risk and Sacrifice Productivity Economic Growth

Lesson 3: Using Economic Models Six characteristics that affect economic growth Risk and Sacrifice Productivity Economic Growth A measure of the amount of goods and services produced with a given amount of resources in a specific period of time

Lesson 3: Using Economic Models Six characteristics that affect economic growth Risk and Sacrifice Productivity Economic Growth Human capital

Lesson 3: Using Economic Models Six characteristics that affect economic growth Risk and Sacrifice Productivity Economic Growth The sum of people’s skills, abilities, health, knowledge, and motivation. Human capital

Lesson 3: Using Economic Models Six characteristics that affect economic growth Risk and Sacrifice Productivity Economic Growth Human capital Division of labor

Lesson 3: Using Economic Models Six characteristics that affect economic growth Risk and Sacrifice Productivity Economic Growth Human capital Division of labor Organizing work so that each worker or work group completes a separate part of the overall task.

Lesson 3: Using Economic Models Six characteristics that affect economic growth Risk and Sacrifice Productivity Economic Growth Human capital Specialization Division of labor

Lesson 3: Using Economic Models Six characteristics that affect economic growth Risk and Sacrifice Productivity Economic Growth Human capital Specialization Factors of production perform only tasks they can do better or more efficiently than others. Division of labor

Lesson 3: Using Economic Models Six characteristics that affect economic growth Risk and Sacrifice Economic interdependence Productivity Economic Growth Human capital Specialization Division of labor

Lesson 3: Using Economic Models Six characteristics that affect economic growth Risk and Sacrifice We rely on others, and others rely on us, to provide most of the goods and services we all consume Economic interdependence Productivity Economic Growth Human capital Specialization Division of labor

Lesson 3: Using Economic Models Circular Flow of Economic Activity ● Market - a location or other mechanism that allows buyers and sellers to exchange a specific product ● Factor (resource) Market - where all the factors of production are bought and sold ● Product Market - where producers sell their goods and service

Lesson 3: Using Economic Models Circular Flow of Economic Activity

Lesson 3: Using Economic Models Circular Flow of Economic Activity The circular flow model is unique in that it has no starting point or ending point. The important thing to remember is that individuals and businesses are connected by markets Businesses purchase resources from households in the factor market Households purchase goods and services from businesses in the product market

Lesson 3: Using Economic Models - simplified equation, graph, or figure showing how the economy works ● Transferring statistical information to a written or visual form as needed for clarity, making simple models that reduce complex situations to their most basic elements ● The Production Possibilities Curve and the Circular Flow Diagram are examples of how complex economic activity can be explained in a simple model ● Economic models are often revised to make them better ○ ○ If an economist discovers that a model helped make a prediction that turns out to be right, the model can used again If an economist discovers that a model helped make a prediction that turns out to be wrong, the model might need changing to make predictions more reliable in the future

Lesson 3: Using Economic Models Cost-Benefit Analysis - a way of comparing the benefits of an action to the expected costs ● If the benefits exceed the costs, the action is carried out ● If the costs exceed the benefits, another action is considered Regardless of the model used, it often helps to take small, incremental steps toward the final goal. This is especially valuable when we are unsure of the exact cost involved If the cost turns out to be larger than we anticipated, then the resulting decision can be reversed without too much being lost

Lesson 3: Using Economic Models Free Enterprise Economy - an economy in which consumers and privately owned businesses, rather than the government, make the majority of the WHAT, HOW, FOR WHOM decisions The study of economics will provide you with a working knowledge of the economic incentives, laws of supply and demand, price systems, economic institutions, and property rights that make the US economy function. Standard of Living - the quality of life based on the ownership of the necessities and luxuries that make life easier

Lesson 3: Using Economic Models Free Enterprise Economy - an economy in which consumers and privately owned businesses, rather than the government, make the majority of the WHAT, HOW, FOR WHOM decisions The study of economics will provide you with a working knowledge of the economic incentives, laws of supply and demand, price systems, economic institutions, and property rights that make the US economy function. Standard of Living - the quality of life based on the ownership of the necessities and luxuries that make life easier Get with a partner and read “The Global Economy and You” on page 28 and answer the question under Critical Thinking.

Lesson 3: Using Economic Models Lesson 3 Review: ● Why is economic growth important?

Lesson 3: Using Economic Models Lesson 3 Review: ● Why is economic growth important? ○ Everybody wants more than they already have and the population is growing, so the economy must grow to satisfy the wants and needs of this growing population.

Lesson 3: Using Economic Models Lesson 3 Review: ● What role does specialization play in the productivity of an economy?

Lesson 3: Using Economic Models Lesson 3 Review: ● What role does specialization play in the productivity of an economy? ○ Specialization can improve productivity by assigning factors of production tasks in which they are most efficient.

Lesson 3: Using Economic Models Lesson 3 Review: ● How do businesses and individuals participate in both the product market and the factor market in an economy?

Lesson 3: Using Economic Models Lesson 3 Review: ● How do businesses and individuals participate in both the product market and the factor market in an economy? ○ Businesses purchase resources from individuals in the factor market and individuals purchase goods and services from businesses in the product market.

Lesson 3: Using Economic Models Lesson 3 Review: ● What roles do factor markets and product markets play in an economy?

Lesson 3: Using Economic Models Lesson 3 Review: ● What roles do factor markets and product markets play in an economy? ○ The wages and salaries that people receive from businesses in the resource markets in exchange for resources return to businesses in the product markets in exchange for goods and services.

Lesson 3: Using Economic Models Lesson 3 Review: ● How does cost-benefit analysis help make economic decisions?

Lesson 3: Using Economic Models Lesson 3 Review: ● How does cost-benefit analysis help make economic decisions? ○ It is a way of comparing the benefits of an action to the expected costs. If the benefits are greater than the costs, then the action is done. If the costs are greater than the benefits, then another action will be considered.

Lesson 3: Using Economic Models Lesson 3 Review: ● How does the study of economics help you make better choices?

Lesson 3: Using Economic Models Lesson 3 Review: ● How does the study of economics help you make better choices? ○ The study of economics provides understanding of how things are made and sold, how incomes are earned and spent, how jobs are created, and how the economy works on a daily basis. This understanding helps people make the best choices on economic issues.