Chapter 1 Participation Questions Wait for class to

Measuring - Account balances are changed by each")

Users of Accounting Information The two primary users of accounting information for decision-making:")

are Measured through the Accounting Equation Assets = Liabilities")

Revenues Minus Expenses Net Income If expenses exceed")

Examples 2011 2010 Revenues 1, 000, 000 Expenses 850,")

Income Statement 2. )")

at ONE point in time. ◦")

Two Components of Retained Earnings: 1. Net Income (Net Loss) -")

Revenue")

Income Statement 2. )")

Establishes the rules for recording transactions and preparing")

Corporations")

Expanding roles: Financial planners Info. tech. developers Financial analysts")

clinics throughout the Northeast. At the end")

, Buffalo Drilling has $9, 400 of")

, Buffalo Drilling has $9, 400 of")

- Slides: 74

Chapter 1 - Participation Questions – Wait for class to be 100% complete before answering 1. 2. 3. 4. 5. What is the only way to access the Connect Website for the first time? When an investor provides money ($) to a corporation for ownership, what does the corporation issue to the investor/owner in return? A ‘Payable’ is always a liability. T/F Which financial statement is always completed first? Which financial statement is more like a movie over a period of time versus a camera picture? 1

� � � Announcements Connect Enrollment Date closes on 1/24/16 – USE KNIGHTS E-MAIL ADDRESS ONLY Free access includes e-book through first assignment only due on 1/24 ◦ “Connect” - $85. 00 includes no e-book – purchase through Connect Website ◦ “Connect Plus” - $125. 00 includes e-book – purchase through Connect Website Assignments ◦ January 19 th (Complete this week by Friday at 5: 00 PM if receiving federal student aid) � Syllabus Quiz #1 – used for attendance for Federal Student Aid (Webcourses) – 2 attempts ◦ January 24 th � Participation Questions for Chapter #1 questions (Webcourses) – 1 attempt � Connect Homework Assignment #1 (Connect) – unlimited attempts � Materia Homework Assignment #1 (Webcourses) – unlimited attempts ◦ The Accounting Game: Basic Accounting Fresh from the Lemonade Stand. Darrell Mullis & Judith Orloff, ISBN 978 -1 -4022 -1186 -7 3

Overall Question to be answered this semester: How has society shaped today’s financial reporting? 4

Block 1 Chapter 1: Overview of Accounting and Financial Reporting Measure Aggregate Communicate Chapter 2 – 3: Accounting Cycle – Measure/analyze business transactions to aggregate data and construct financial statements for communication with decision makers 5

as e M ure Aggregate 1+1+1+1=4 Com mun icat e 6

Aggregating data to communicate to decision-makers l G a n i F “A” – e d ra Passing Yards: 10, . 5, 15, … Total for game = 150 Final Score – Yankees 10 vs. Buccaneers 18 Final Grades, final scores, passing yards function in a manner similar to the ACCOUNTS used to help measure business transactions. They collect and aggregate data. 7

Accounting in a Nutshell… 1. ) Measuring - Account balances are changed by each transaction: • Revenue Account Increase • Inventory Account Decreases 2. ) Aggregate 3. ) Communicate 8

Is Accounting Relevant? ? ? � Loan from Bank United � Customer Website - Edgar Securities and Exchange � https: //www. sec. gov/cgi-bin/viewer? action=view&cik=1166126&accession_number=0001166126 -14 -000017&xbrl_type=v# � https: //www. sec. gov/cgi-bin/viewer? action=view&cik=1378950&accession_number=0001193125 -14 -094601&xbrl_type=v# � Budgets - Sales Manager – EBITDA ◦ Sales; Travel & Expense; Marketing Budgets ◦ http: //www 2. massgeneral. org/facultydevelopment/cfd/pdf/20111006 Budgeting. Basics. pdf 9

Legal Forms of Business Organization � � � Sole Proprietorship ◦ Owned by a single person Partnership ◦ Owned by more than one person Corporation ◦ Owned by multiple shareholders through shares of “Stock” ◦ Pros – limited liability: stockholders are not personally responsible for financial obligations of corporation. ◦ Cons – �Double taxation �Corporate income is taxed �Shareholders taxed on distributions of earnings (dividends) 10

Stock Ownership A type of security that signifies ownership in a corporation and represents a claim on part of the corporation's assets and earnings. A holder of stock (a shareholder) has a claim to a part of the corporation's assets and earnings. In other words, a shareholder is an owner of a company. Ownership is determined by the number of shares a person owns relative to the number of outstanding shares. For example, if a company has 1, 000 shares of stock outstanding and one person owns 100 shares, that person would own and have claim to 10% of the company's assets. 11

How a corporation begins… 12

Overview of Chapter 1 1. Accounting as a Measurement/Communication Process 2. Communicating through the Financial Statements. 3. Generally Accepted Accounting Principles 13

Two Functions of Financial Accounting To measure business activities of a company and to communicate those measurements to external parties for decision-making purposes. Walmart Company Statistics Website: http: //www. statisticbrain. com/wal-mart-company-statistics/ 14

Accounting Information - The Language of Business Make Decisions About People – ‘Who’ Companies – ‘What’ Communicate information to: Accountants – ‘How’ Activities Measured by: 1

(WHO) Users of Accounting Information The two primary users of accounting information for decision-making: � Investors - for present & potential capital providers � Creditors - Bonds and Banks for Investment & lending decisions Other users include: � Customers � Suppliers � Managers � Employees � Competitors � Regulators � Tax authorities Copyright © 2010 Pearson Education Inc. Publishing as Prentice Hall. 16 16

WHAT is Measured? BUSINESS ACTIVITIES These transaction are from the COMPANY PERSPECTIVE � � � Operating Activities ◦ Involves transactions in primary operations of business � Purchase inventory (lemonade) to sell $1, 000 � Selling Lemonade to 1, 000 customers for $2. 00 per cup. Financing Activities ◦ Involves funding from external sources � Individual invests $1, 000 in a business in return for company stock. � Bank loan of $1, 000. Investing Activities ◦ Involves purchase and sale of long-term resources � Purchased lemonade stand to operate business - $100 17 17

HOW - Business Activities (Transactions) are Measured through the Accounting Equation Assets = Liabilities Company’s resources + Stockholders’ Equity Claims to those resources 18

Accounting Equation Elements Assets Liabilities Stockholders’ Equity • Resources owned by company • Amounts owed to creditors • Owners claim to resources (stockholders of the corporations) 19

Claims on Assets ASSETS • Cash • Inventory • Equipment • Building AMOUNTS OWED – LIABILITIES • Bank • Supplier • Government • Employees OWNER’S CLAIMS – OWNER’S (STOCKHOLDER) EQUITY • Stockholders – common and preferred 20

Company Profits – Operating Cycle (How are well are we doing what we do? ) Revenue • Amounts earned from selling products and services to customers Expenses • Cost of providing products and services Net Profit • Difference between revenue and expense 21

Net Income (aka “the bottom line) Revenues Minus Expenses Net Income If expenses exceed revenues A net loss results 22

Net Income and (Net Loss) Examples 2011 2010 Revenues 1, 000, 000 Expenses 850, 000 1, 075, 000 Net Income/(Net Loss) 150, 000 (75, 000) 2

Misconceptions about Accounting � It is not an exact science – differing treatments can yield differing results. ◦ Receivables Allowances ◦ Inventory valuation ◦ Depreciation methods Revenue Cost of goods sold Gross Profit Less: Expenses LIFO 100, 000 33, 000 67, 000 60, 000 Operating Income 7, 000 FIFO 100, 000 30, 000 70, 000 60, 000 7. 0% 10, 000 10. 0% 1 -24

Reality Check… ____ Assets ____ Liabilities A. Costs of selling products and services B. Amounts received from sales of products or services ____ Owner’s Equity C. Amounts owed to creditors ____ Revenues D. Owner’s claims to company resources ____ Expenses E. Resources owned 25 25

Learning Objective #2 Communicating through the Basic Financial Statements 2

The Basic Financial Statements Fiscal or Calendar Year 1. ) Income Statement 2. ) Statement of Stockholder’s Equity 3. ) Balance Sheet 4. ) Cash Flow Statement Data flows from one financial statement to the other based on the order above.

Income Statement Format for Income Statement: 1. Start with all Revenue Accounts 2. Subtract all Expense Accounts 3. The Result is the Net Income (not an account, but a calculation) Income statement reports how the company performed operationally based on the company’s account balances for revenues and expenses over a period of time. �Similar to a Movie – Captures data over time (accounting period)

In-class Quiz – No Points Use the account balances below to create an Income Statement showing a net profit or loss – remember to only include operating cycle items and not assets. Payroll Expense Revenue New truck purchase Rent expense $10, 000 $30, 000 $25, 000 $5, 000 Answer: a) $30, 000; b) $15, 000; c) (-$10, 000); or d) $5, 000 29

Balance Sheet Shows resources and obligations (account balances) at ONE point in time. ◦ “SNAPSHOT” Format is based on the basic ACCOUNTING EQUATION ◦ Assets = Liabilities + Stockholders’ Equity

ASSETS – Sample of Accounts � Cash – liquid assets � Accounts Receivable – amounts the company expects to collect from customers. � Inventory – items for sale by company � Property, plant, and equipment – land, buildings, computers, store fixtures, manufacturing equipment.

LIABILITIES – Sample of Accounts � Accounts Payable – amounts owed to vendors for the purchase of materials or services. � Notes payable – amounts due to another party for loaning money to the company

Receivable versus Payable � Receivable – the firm will receive dollars, so it is a resource to the firm that can be utilized in the future. ALWAYS AN ASSET � Payable – the firm owes money to creditors, such as suppliers or the bank. ALWAYS AN LIABILITY

STOCKHOLDERS’ EQUITY – Two Primary Accounts � Paid-in-Capital ◦ Common Stock – external source �Amount shareholders have invested in the business � Retained Earnings – internal source ◦ Cumulative amount of net income (revenue less expenses) earned and kept in business less dividends paid out.

How to build the Balance Sheet 1. List all of the asset accounts with their balances and sum all of them. 2. List all liability accounts with their balances and sum all of them. 3. List all Stockholders’ Equity accounts with their balances and sum all of them.

In-class Quiz – No Points Use the account balances below to create a Balance Sheet Cash Accounts receivable Inventory Accounts payable Common stock Retained earnings $1, 000 $10, 000 $15, 000 $20, 000 $5, 000 $1, 000 What are the total assets? a) $36, 000; b) $72, 000; c) $20, 000; or d) $6, 000 36

37

38

Accounts for Apple Computers What is an Account – a place to record and aggregate similar transactions (Chart of Accounts) What Constitutes a Revenue Account? • List one or two accounts What constitutes an Expense Account? • List one or two accounts What constitutes a Balance Sheet Account? • List one or two accounts 39

Revenues and Expenses of Apple What Constitutes Revenue? • Products sales • Repairs • Itunes • Iphone contracts • Iwatch? ? ? What constitutes Expenses? • Rent • Employee wages • Insurance • Furniture and fixtures • Utilities • Supplies • Marketing Balance Sheet • Inventory • Equipment • Furnishings 40

Statement of Stockholders’ Equity Summarizes the changes to Stockholders’ Equity Accounts over an interval of time. ◦ Statement Includes the following main two (2) accounts: �Common Stock Account �Retained Earnings Account The format of this statement shows the user how the balances in these two accounts have changed from their beginning of period balance through their end of period balance.

Common Stock Format for Statement of Stockholders’ Equity Steps: 1. Start with the beginning account balance of Common Stock 2. Add any new issuance of Common Stock 3. Ending Account Balance of Common Stock = Beginning account balance + New Issuance $ Beginning Balance of Common Stock Plus Issuance of Stock ($ received) Equals Ending Balance of Common Stock 4

Retained Earnings (RE) Two Components of Retained Earnings: 1. Net Income (Net Loss) - Inflows (outflows) to retained earnings based on the profits retained by the company. 2. Dividends - Outflow of cash from retained earnings. Formula used calculate the Ending Retained Earnings Account Balance for the Accounting Period: Beginning Retained Earnings + Net Income – Dividends = Ending Retained Earnings 44

Net Loss decrease Net Income Increase Dividends decrease Retained earnings Copyright © 2010 Pearson Education Inc. Publishing as Prentice Hall.

Components of Retained Earnings 1. 2. 3. 4. Steps: Start with the beginning Retained Earnings account balance. Add any Net Income OR subtract Net Loss (Revenue accounts minus expense accounts) Subtract the balance in the Dividend Account. Ending Retained Earnings account balance = Beginning account balance + Net Income (or - net loss) – Dividends Beginning Balance of RE Plus or Minus Net Income (or Net Loss) for the Period Minus Dividends for the Period Equals Ending Balance of RE 4

Components of Retained Earnings Example #2 Net Loss Example #1 Net Income 100, 000 Beginning of Period RE 100, 000 Net Income 150, 000 Plus or Minus Net Loss (250, 000) Dividends 50, 000 Minus Dividends 0 200, 000 End of Period RE (150, 000) 4

In-class Quiz – No Points Use the account balances to calculate the ending balance in the retained earnings account: Beginning retained earnings account balance Total Revenue accounts Total Expense accounts Dividend account Ending retained earnings account balance � $10, 000 $100, 000 $80, 000 $10, 000 ? Answer? a) $200, 000; b) $40, 000; c) $30, 000; or d) $20, 000 48

Expanded Accounting Equation Assets = Liabilities + Stockholders’ Equity Paid in Capital (Stock) Revenue Retained Earnings Expenses Dividends

The Statement of Cash Flows Measures actual cash inflows and outflows over the accounting period. Does Net Income equal Cash Flow? � Categorizes ◦ Operating into three types of activities: �Cash receipts and payments from selling goods and services ◦ Investing �Purchasing & selling long-term assets ◦ Financing �Issuing stock and borrowing

The Basic Financial Statements Fiscal or Calendar Year 1. ) Income Statement 2. ) Statement of Stockholder’s Equity 3. ) Balance Sheet 4. ) Cash Flow Statement Data flows from one financial statement to the other based on the order above. Copyright © 2010 Pearson Education Inc. Publishing as Prentice Hall.

Relationships between Financial Statements

Relationships between Financial Statements

Balance Sheet December 31, 2010 Assets $$$, $$$ Liabilities $$$, $$$ Stockholders’ equity: Common stock $$$, $$$ Retained earnings $$$, $$$ Total liabilities and equity $$$, $$$ Statement of Cash Flows For the year ended December 31, 2010 Cash flows from operating activities $$$, $$$ Cash flows from investing activities $$, $$$ Cash flows from financing activities $$, $$$ Net cash flows $$, $$$ Cash balance, December 31, 2009 $$, $$$ Cash balance, December 31, 2010 $$, $$$ Copyright © 2010 Pearson Education Inc. Publishing as Prentice Hall. Cash from the Asset section of the Balance Sheet equals ending Cash on the Statement of Cash Flows

APPLE COMPUTERS 55

Objective #3 Generally Accepted Accounting Principles The Organizations That Govern Accounting 1. Securities and Exchange Commission (SEC) 1. 2. 3. 2. Securities Act of 1934 Oversees the US financial markets Responsible for GAAP, but delegates authority to FASB Financial Accounting Standards Board (FASB) 1. 2. Privately funded Creates the rules and standards that govern financial accounting, known as Generally Accepted Accounting Principles (GAAP). 57

Generally Accepted Accounting Principles (Cont. ) Establishes the rules for recording transactions and preparing financial statements. Requires that information be useful. � Relevant = The info allows users to make a decision. � Faithfully Representative = The info is complete, neutral, and free from material error. 1 -58

Role of Auditors are trained individuals hired by a company as an independent party to express a professional opinion of the accuracy of that company’s financial statements. Role of auditors Help ensure that management has in fact appropriately applied GAAP in preparing the company’s financial statements Help investors and creditors in their decisions by adding credibility to the financial statements. 59

Auditor Designations Certified Public Accountants – CPA’s are licensed professional accountants that serve the general public. Certified Management Accountants – CMA’s are certified professionals who specialize in accounting and financial management, usually for private industry. 60

Flow of Accounting Income Statement of Retained Earnings Balance Sheet Statement of Cash Flows Accounting Equation: Assets = Liabilities + Owners Equity GAAP (Rules) formulated by FASB 6 61

Careers in Accounting � http: //fortune. com/2014/08/06/15 -most- profitable-business-sectors/ � Kramer at work � http: //www. youtube. com/watch? v=b. U 6 m 5 Uq Lx 9 M&list=RDXEL 65 gyww. HQ&index=2 62

Careers in Accounting Clients: Traditional roles: Public Accounting (Big 4 and Non-Big 4) Corporations Governments Nonprofit organizations Individuals Auditors Tax preparers/planners Business consultants Private Accounting Your employer Financial accountants Managerial accountants Budget analysts Internal auditors Tax preparers Payroll managers 63 1 -63

Careers in Accounting (cont. ) Expanding roles: Financial planners Info. tech. developers Financial analysts Forensic accountants Information risk managers Investment bankers Environmental accountants Financial advisors Tax lawyers Information managers Management advisors Tax planners Acquisition specialists FBI agents Sports agents Other career options : Governmental accounting, sole proprietorship, and education. 64 1 -64

Chapter 1 Practice Set from Connect Descriptions Account Classifications Amounts earned from sale of products or services Owners’ claims to resources Distributions to shareholders Amounts owed to creditors Costs of selling products or services Resources owned 1. 2. 3. 4. 5. 6. Assets Revenues Dividends Liabilities Expenses Stockholders’ Equity 65

Financial Statements Descriptions Financial Statements Change to Owners’ claim to resources Profitability of the company Change in cash as a result of operating, investing, and financing activities Resources equal creditors’ and owners’ claims to the resources 1. 2. 3. 4. Balance Sheet Statement of Cash Flows Income Statement of Stockholders’ Equity 66

Accounts Balances Cowboy Law Firm Cash Salaries expense Accounts payable Retained earnings Utilities expense Supplies Service revenue Common stock $4, 370 1, 590 2, 390 3, 610 Service Revenue 970 12, 250 Expenses: 8, 560 4, 620 Income Statement Total expense Net income (loss) 67

Accounts Balances Cowboy Law Firm Cash Salaries expense Accounts payable Retained earnings Utilities expense Supplies Service revenue Common stock $4, 370 1, 590 2, 390 3, 610 970 12, 250 8, 560 4, 620 Income Statement Service Revenue $8, 560 Expenses: Salaries expense $1, 590 Utilities expense 970 Total expense 2, 560 Net income (loss) $6, 000 68

Eagle Corp. operates Magnetic Resonance Imaging (MRI) clinics throughout the Northeast. At the end of the current period, the company reports the following amounts: Assets = $41, 900 Liabilities = $21, 100 Dividends = $2, 100 Revenues = $11, 100 Expenses = $8, 200. Net Income = ? 69

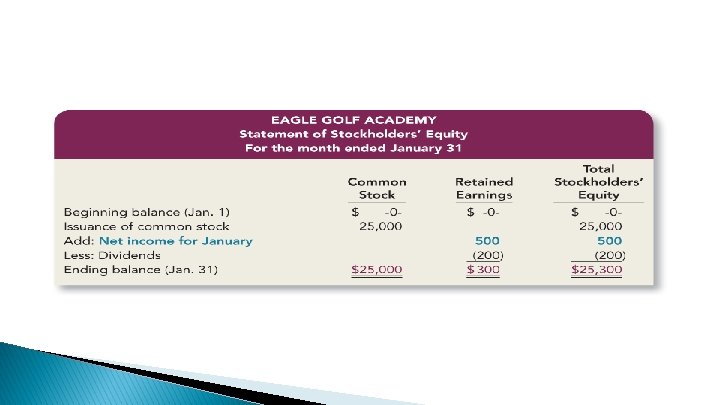

At the beginning of the year (January 1), Buffalo Drilling has $9, 400 of common stock outstanding and retained earnings of $7, 100. During the year, Buffalo reports net income of $7, 400 and pays dividends of $2, 340. In addition, Buffalo issues additional common stock for $6, 800. Buffalo Drilling Statement of Stockholders’ Equity Common Stock Retained Earnings Total Stockholders’ Equity Beginning Balance Issuance of Common Stock Add: Net Income Less: Dividends Ending Balance 70

At the beginning of the year (January 1), Buffalo Drilling has $9, 400 of common stock outstanding and retained earnings of $7, 100. During the year, Buffalo reports net income of $7, 400 and pays dividends of $2, 340. In addition, Buffalo issues additional common stock for $6, 800. Buffalo Drilling Statement of Stockholders’ Equity Beginning Balance Issuance of Common Stock $9, 400 Retained Total Stockholders’ Earnings Equity $7, 100 $16, 500 6, 800 Add: Net Income 7, 400 Less: Dividends (2, 340) Ending Balance $16, 200 $12, 160 $28, 360 71

Accounts and Balances at Year End Equipment $21, 300 Service revenue Accounts payable (A/P) 2, 060 Cash Salaries expense 26, 300 Retained earnings Common stock 16, 200 Land 14, 150 Notes payable (N/P) 15, 950 30, 800 10, 920 ? Buffalo Drilling Balance Sheet Assets Liabilities Total Liabilities Total Stockholders’ Equity Total Assets Stockholders’ Equity Total Liabilities and Stockholders’ Equity 72

Accounts and Balances at Year End Equipment $21, 300 Service revenue Accounts payable (A/P) 2, 060 Cash Salaries expense 26, 300 Retained earnings Common stock 16, 200 Land 14, 150 Notes payable (N/P) 15, 950 30, 800 10, 920 ? Wolfpack Construction Balance Sheet Assets Cash Liabilities $10, 920 Accounts Payable $2, 060 Land 14, 150 Notes Payable 15, 950 Equipment 21, 300 Total Liabilities 18, 010 Common Stock Retained Earnings 12, 160 Total Stockholders’ Equity 28, 360 Total Assets Stockholders’ Equity $46, 370 Total Liabilities and Stockholders’ Equity 16, 200 $46, 370 73

During its first five years of operations, Red Raider Consulting reports net income and pays dividends as follows. Calculate the balance of retained earnings at the end of each year of Red Raider Consulting. Note that retained earnings will always equal $0 at the beginning of year 1. Year Net Income Dividends 1 2 3 4 5 $1, 100 1, 900 2, 150 3, 450 4, 150 $500 400 1, 050 1, 100 850 Retained Earnings 74