CHAPTER 1 INTRODUCTION TO COST ACCOUNTING BASIC COST

CHAPTER 1 : INTRODUCTION TO COST ACCOUNTING BASIC COST ACCOUNTING ZAINATULIZA ZAINAL ABIDIN

WHY? Business grew in size & importance Market became more sophisticated Legislations regulating business grew

COST TERMINOLOGY Ø COST: Cost means the amount of expenditure incurred on a particular thing. Ø COSTING: Costing means the process of ascertainment of costs. Ø COST ACCOUNTING: The application of cost control methods and the ascertainment of the profitability of activities carried out or planned”. Ø COST CONTROL: Cost control means the control of costs by management. Following are the aspects or stages of cost control. Ø JOB COSTING: It helps in finding out the cost of production of every order and thus helps in ascertaining profit or loss made out on its execution. The management can judge the profitability of each job and decide its future courses of action. Ø BATCH COSTING: Batch costing production is done in batches and each batch consists of a number of units, the determination of optimum quantity to constitute an economical batch is all the more important.

COSTING Ascertainment of cost by applying accounting and costing principles, methods and techniques. Cost may be ascertained after they are incurred or before they are incurred (estimates). Costing provides management with cost information for purposes planning and controlling. Costing applied to all kind of businesses.

COSTING SYSTEM To provide COST INFORMATION Information speedily and accurately An efficient system will: � Reveal unprofitable/ profitable activities � Cost comparison � Facilitate planning and controlling � Identify weaknesses/ inefficiency � Provide basis for pricing

has")

COST ACCOUNTING COST ACCOUNTING: The Institute of Cost and Management Accountant, England (ICMA) has defined Cost Accounting as – “the process of accounting for the costs from the point at which expenditure incurred, to the establishment of its ultimate relationship with cost centers and cost units. In its widest sense, it embraces the preparation of statistical data, the application of cost control methods and the ascertainment of the profitability of activities carried out or planned”. Cost Accounting = Costing + Cost Reporting + Cost Control.

COST ACCOUNTING Cost accounting is concerned with recording, classifying and summarizing costs for determination of costs of products or services, planning, controlling and reducing such costs and furnishing of information to management for decision making Cost accounting performs the costing function Cost accounting performs the planning and control function

The importance of cost accounting to the management: To determine product cost The cost of the product is of prime importance in cost accounting. The total product cost and cost per unit of product are important in making stock valuation, deciding price of the product and managerial decision making. To facilitate planning and control of regular business activities The cost formulation in cost accounting system is oriented to help in planning, control and decision making. The accumulation, classification and analysis of cost is done in such a way as to help management decision regarding business activities.

FINANCIAL ACCOUNTING VS COST ACCOUNTING Accounting is the process of identification, measurement, and communication of financial information about economic entities to interested parties. Two types: � � Financial accounting focuses on measuring the results of an organization’s operations for a period of time, reflected in the financial statements. Analysis, classification and historical recording transactions, ascertain profit and loss and the position of assets and liabilities. The F/Statement prepared for external users. Cost (or management) accounting focuses on cost allocation to a product, service, or contract; management uses the information to plan, evaluate, and control within its organization and to assure appropriate use of, and accountability for, its resources. The information is useful for internal users.

FINANCIAL ACCOUNTING VS COST ACCOUNTING 1. Nature Cost Accounting Classifies, records, present and interprets in a significant manner the material, labour, overhead costs involved in manufacturing and selling each product, job and service. Financial Accounting Classifies, records, presents and interprets in terms of financial character and provides the figures for the preparation of the financial statements. 2. Primary users of information The users are internal users. They The users of Financial are members of the management. Accounting statements are mainly external to the business enterprise. External users include shareholder, creditors, financial analyst and government authorities 3. Accounting method Does not based on the double Follows entry system. 4. Accounting Principle Does not bound to use the ‘generally accepted accounting principles’. It can use any accounting technique that generates useful information. the double entry The ‘generally accepted accounting principles’ are important and are used extensively.

FINANCIAL ACCOUNTING VS COST ACCOUNTING cont’d Cost Accounting 5. Unit measurement 6. Report frequency 7. Time dimension Financial Accounting of Applies any measurement All information is in term unit that is useful in a of money. particular situation; such as labour hours, and machine hours. Data and statements are prepared whenever needed. Reports may be prepared on a monthly, weekly or even daily basis. Concerned with future information as well as past information Data and statement are developed for a definite period, usually a year. Reports what has happened in the past in an organisation.

COSTING PRINCIPLES COST UNIT : Quantitative unit of product/ services relation to costs can be ascertained. E. g jobs, contracts, kg of material, kilowatt hrs, passenger miles etc. COST CENTRE: CIMA defined a location, person or item of equipment in respect of which costs may be ascertained and related to cost units. E. g, a salesman with the salesman commission (location,

Opportunity Costs The potential benefit that is given up when one alternative is selected over another. Example: If you were not attending this program, you could save RM 10, 000 per year. Your opportunity cost? 13/82

Sunk Costs 14/82 Sunk costs have already been incurred and cannot be changed now or in the future. They should be ignored when making decisions. Example: You bought an automobile that cost RM 10, 000 two years ago. The RM 10, 000 cost is sunk because whether you drive it, park it, trade it, or sell it, you cannot change the RM 10, 000 cost.

COSTS “the arrangement of items in logical groups having regards to their nature of purpose. The first part of this definition relates to the nature of expenditure e. g expenditure on raw materials and the latter part indicates where the expenditure is to be charged. ”

THE ELEMENTS OF COST AND ITS CLASSIFICATION In carrying out its activities, a company will incur many different types of costs. It has to pay for the raw materials, labour, rental, electricity, royalty, advertising, interest on bank loan, and many other cost items. For ease of use and analysis, these costs are generally classified according to their function: Production costs, Administration costs; Marketing and Distribution costs, Financing costs and Research and Development costs.

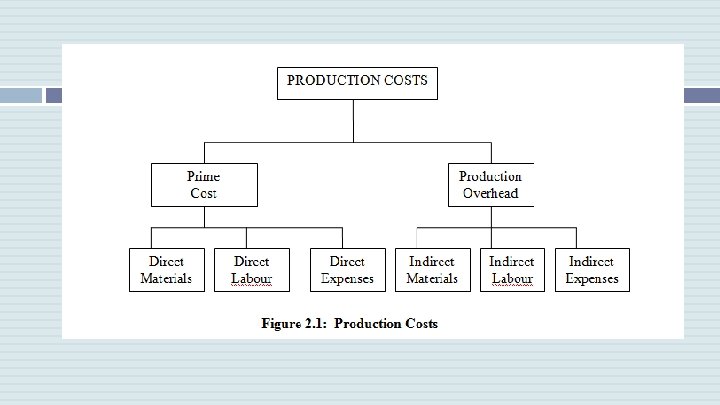

THE ELEMENTS OF COST AND ITS CLASSIFICATION The elements of cost consist of: Direct materials Direct wages Direct expenses Overhead � � � Production Administration Selling and distribution

Direct Material All materials that become a part of the product, of which the costs are directly charged as part of the prime cost is referred to as direct material. In other words, direct material is the material that can be measured and charged directly to the cost of the product. Some examples of direct materials are: raw cotton in textile, rubber to make tyre and crude oil to make diesel fuel. Other material such as nail, glue and varnish are classified as indirect materials.

Direct Wages Direct wages are incurred in altering the construction, composition, conformation or condition of the product. The wages paid to skilled and unskilled workers for this purpose can be allocated specifically to the particular accounts concerned. For example, carpenters and machine operators are treated as direct labour because these are people who work directly on the materials and actually make the product. Whereas, foremen, supervisors, electricians are treated as indirect labour because they are not involved in the actual manufacturing of the product.

Direct Expenses Direct expenses include any expenditure other than direct material or direct labour that are directly incurred on a specific cost unit. Such special necessary expense is charged directly to the particular account concerned, as part of the prime cost. Examples of direct expenses are as follows: The hiring of special – or single-purpose tools or equipment for a particular production order or product. Cost of special layout, designs or drawings. Maintenance costs of such equipment.

The three elements of cost which are mentioned above constitute prime cost, and all expense over and above prime cost is overhead.

Overhead “Overhead” may be defined as the cost of indirect material, indirect labour and such other expenses, including services, which cannot conveniently be charged direct to specific cost units. Alternatively, overheads are all expenses other than direct expenses. The main groups of overhead are as follows: Production overhead, including services. Administration overhead Selling and Distribution overhead

Behaviour Of Costs Variable Costs These are costs that change in direct proportion with production activity. For example, when we produce more furniture, we make use of more timber, more carpenters and more royalty are paid. When we produce less furniture, we incurred less of these costs. Let us assumed that the changes in these costs are in direct p proportion with the production activity (volume of production).

Behaviour Of Costs Fixed Costs These are costs that remain unchanged when production activity changes over a certain relevant range. For example, rental cost will remain constant, and not be affected by production. Examples of fixed costs include rent, insurance, depreciation, salaries of Production staff, wages of supervisors, etc.

Behaviour Of Costs Semi variable and fixed costs Are made up of fixed and variable elements. It is a combination of semi variable and semi-fixed costs. The former, semi-variable costs fluctuate with volume due to the effects of the variable components and do not change in direct proportion to output because of the fixed components. The later, semi-fixed costs remained constant up to a certain level of output after which they become variable

The Statement Of Cost

Thank You. .

- Slides: 28