Chapter 08 Current Liabilities Participation Questions Chapter 8

Chapter 08 Current Liabilities

Participation Questions – Chapter 8 ¡ ¡ ¡ Which publicly traded company was showing a negative working capital in their 2012 financial results? l Walmart; Eastman Kodak; Apple Computers; or Ford Motors Current liabilities are usually due in more than one year. l True or False What account is “air traffic liability” shown on Southwest Airlines balance sheet similar to? l Sales tax payable; Deferred taxes; Unearned revenue; or Accounts Payable Which public company did we review the contingent liabilities notes for in class? l Southwest Airlines; Target; Apple Computers; or Eastman Kodak Which publicly traded company was included as an example for their warranty payable estimate? l Southwest Airlines; Eastman Kodak; Apple Computers; or Ford Motors

Announcements ¡ Exam Results l Average l Exam reviews – Webcourses, Calendar, Scheduler ¡ Excel Grade Calculator – Exam 2 Wrap-up Module at the start of Block 3 modules ¡ Assignments – Due 11/13/16 l Chapter 8 Homework (Connect) – unlimited attempts l Participation questions for Chapter 8 (Webcourses) – 1 attempt ¡ Syllabus Quiz #2 - Due 11/20/16 (opens 11/6/16)

Questions to be Answered Chapter 8 – How do we account transactions that impact known and unknown (estimate) current liabilities? How do these transactions impact the income statement and balance sheet?

Chart of Accounts

Current Liabilities Part A Current Liabilities are used to fund current assets in support of the operating cycle. 8 -6

Current Liabilities Liability - A present responsibility to sacrifice assets in the future due to a transaction or other event that happened in the past. o Current liabilities are usually, but not always, due within one year. o Note: If a company has an operating cycle longer than one year, its current liabilities are defined by the operating cycle rather than by the length of a year. 8 -7

Why are Current Liabilities Important? Working Capital – Informational purposes only – not on exam Definition - A measure of both a company's efficiency and its short-term financial health. The working capital ratio formula: Working Capital Ratio = Current Assets / Current Liabilities This ratio indicates whether a company has enough short term assets to cover its short term debt. Anything below 1 indicates negative W/C (working capital). While anything over 2 means that the company is not investing excess assets. Most believe that a ratio between 1. 2 and 2. 0 is sufficient.

Brunswick – Boats & Engines

Brunswick – Boats & Engines

Eastman Kodak

Eastman Kodak

Current vs. Long-Term Liabilities LIABILITIES CURRENT Payable within one year LONG-TERM With more in the than Payable company one year 8 -13

Current Liabilities – Two Types Known Amounts • Accounts Payable • Notes Payable • Unearned Revenue • Sale Tax Payable • Current Portion Long-term Debt • Deferred Taxes Estimated Amounts • Contingencies • Losses http: //blog. caranddriver. com/toyota • Warranty Payable recalling-844000 -u-s-cars-for-shrapnel • Gains shooting-airbags/ 14

Current Liabilities: Known Amount ¡ Accounts payable l ¡ Short-term notes payable l l l 15 Amounts owed for products or services purchased on account Due within one year Used to borrow cash or purchase asset Accrue interest at the end of each period

Accounts Payable 1/1/15 - Bought inventory on Account for $15, 000 2/15/15 – paid for inventory JOURNAL Date Accounts and explanation 1/1/15 Inventory Debit Credit 15, 000 Accounts Payable 15, 000 Purchase of Inventory on account 2/15/15 Accounts Payable 15, 000 Cash 15, 000 Payment of Accounts Payable 16

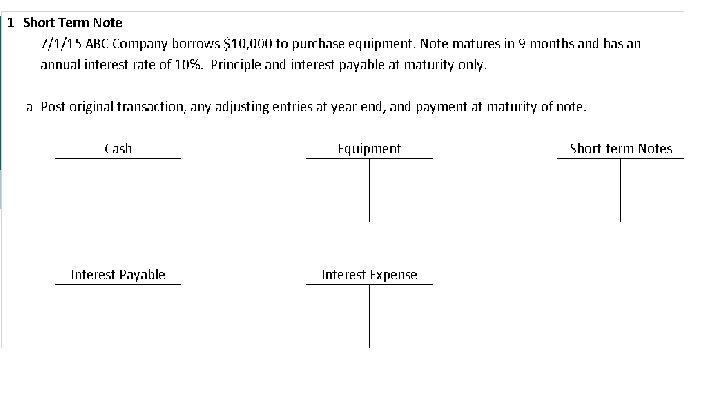

Short-term Notes Payable – 12/1/15 - ABC Company borrows $30, 000 to purchase equipment. Note due 3/1/16, annual interest rate = 9%. Interest and principal paid at maturity. Journal Entry initial transaction, year-end adjusting entry, & maturity Formula to calculate Interest Expense Interest = Face value x Annual interest rate x Fraction of the Yea r

Short-Term Notes Payable JOURNAL Date Accounts and explanation Dec 1 Equipment Debit Credit 30, 000 Note payable, short-term 30, 000 Purchase of Equip. using a 3 -month note payable @ 9% Dec 31 Interest expense 225 Interest payable 225 Accrued interest on note payable (30, 000 x 9% x 1/12) 18

Accounting for Short-Term Notes Payable JOURNAL Date Accounts and explanation Debit Mar 1 Interest expense (30, 000 x 9% x 2/12) 450 Interest payable 225 Credit 30, 000 Note payable, short-term Cash 30, 675 19

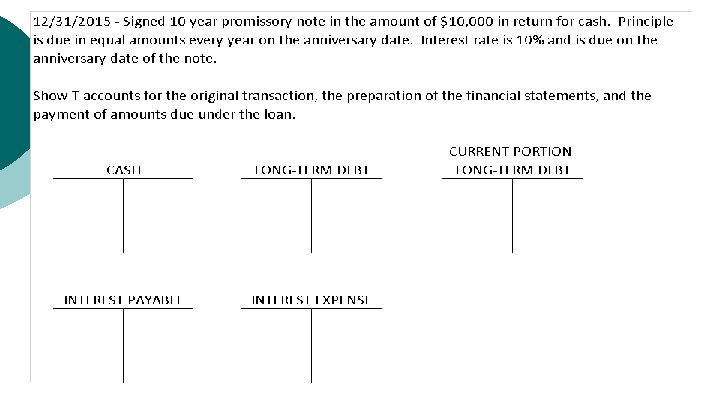

In-Class Exercise 4/1/15 $100, 000 Land Purchase 20% cash payment and 80% promissory note due in 10 months with 12% annual interest Prepare journal entries for initial transaction, financial statements at 12/31/15, and at maturity.

Deferred Revenues Definition - Business receives cash before services or products are provided to customers. Therefore, company cannot recognize any revenue when cash is received. Results in a liability (repay if don’t deliver) Steps: 1. Record cash receipt and set up deferred revenue account (liability) 2. As services or products are provided and revenue is earned, an adjusting journal entry is completed to recognize revenue earned. 1. Debit deferred revenue and credit revenue account. Complete Journal Entries: 2/1 – “I am the Best DJ, Inc. ” receives $300 deposit in advance for DJ for a Fraternity Party. 2/28 – Performs the best DJ services 21

Unearned Revenues ¡ Journal Entry for DJ Example JOURNAL Date Accounts and explanation 2/1 Cash Debit Credit 300 Unearned revenue 300 Received advance payment from customer 2/28 Deferred revenue Revenue To record earned portion of unearned revenue 22 300

Southwest Airlines As described in Note 1 to the Consolidated Financial Statements, tickets sold for passenger air travel are initially deferred as “Air traffic liability. ” Passenger revenue is recognized and air traffic liability is reduced when the service is provided (i. e. , when the flight takes place). “Air traffic liability” represents tickets sold for future travel dates and estimated future refunds and exchanges of tickets sold for past travel dates. 23

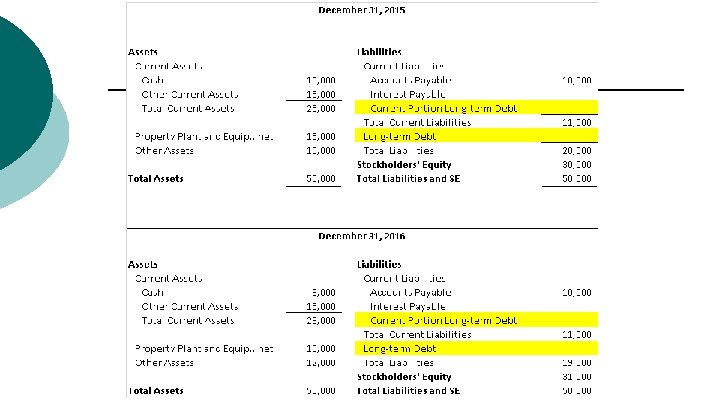

Example below – $10, 000 auto loan payable")

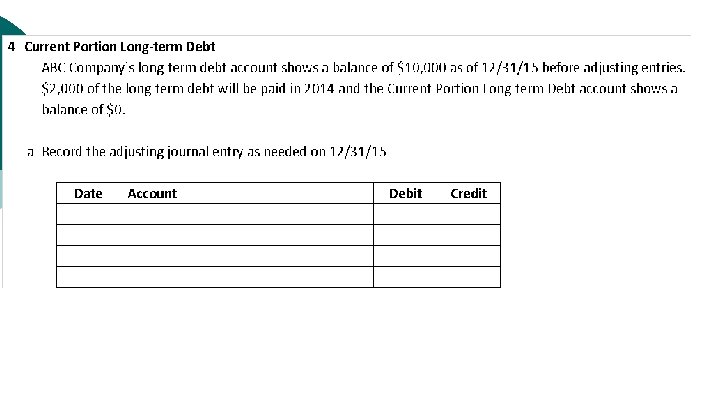

Current Portion of Long-Term Debt (CPLTD) Example below – $10, 000 auto loan payable over 5 years principal due in equal installments each year CPLTD Definition - Amount of principal (out of total long-term debt) payable within one year (12 months) What are we doing… Recognize the portion of long-term debt that will be repaid over the next 12 months and classify it as “Current Portion LTD” to show decision-makers what is due in the coming year. ¡ Steps for recognizing CPLTD: l Initial Transaction ¡ ¡ ¡ 24 Record (debit) for what is received in the long-term loan – i. e. cash, equipment, auto Amount of principal due in the next 12 months is recorded into the CPLTD account (Credit). Amount of principal due after the next 12 months is recorded into the LTD account (Credit).

Example below – $10, 000 auto loan payable")

Current Portion of Long-Term Debt (CPLTD) Example below – $10, 000 auto loan payable over 5 years principal due in equal installments each year Steps for recognizing CPLTD: ¡ l Second Year and later: ¡ l Step 2 – reset balance in CPLTD account. ¡ ¡ 25 Step 1: l When the principal balance is paid over the next 12 months, the CPLTD account is decreased (debited) and cash is credited. Credit amount of principal due in the next 12 months Debit LTD to reduce balance in this account.

Southwest Airlines 26 http: //www. sec. gov/Archives/edgar/data/92380/000119312513041608/d 480533 d 10 k. htm

Current Portion of Long-Term Debt – ¡ Southwest Airlines Example if they just took out 3. 154 million of LTD JOURNAL Date Accounts and explanation Debit 12/31 Cash 3, 154 Mil. Long-Term Debt Current Portion Long-Term Debt 27 Credit 2, 883 Mil. 271 Mil.

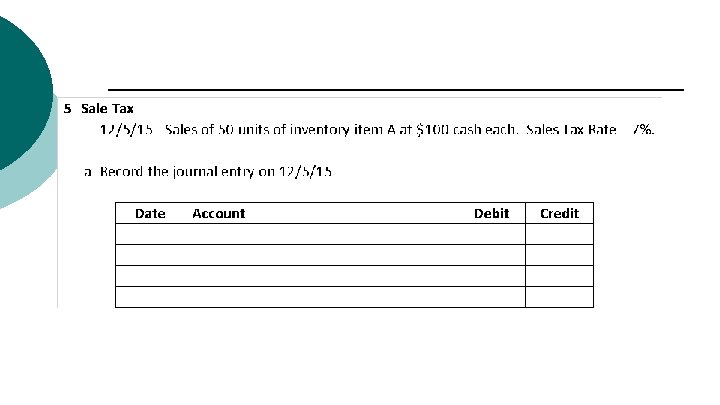

Sales Taxes Payable o Company selling products subject to sales taxes is responsible for collecting the sales tax directly from customers and periodically sending the sales taxes collected to the state and local governments. o Sales tax collection DO NOT increase revenue recognized. o Steps for when a sale is made and sales tax is collected: o Record cash receipt or accounts receivable from sale (debit). o Record revenue earned (credit) o Record sales tax collected into the ‘Sales Tax Payable Account’ (credit). o When sales tax payment is made to the to state, county, etc. : o Debit sales tax payable and credit cash. 8 -28

Sales Taxes Payable Suppose you buy lunch in the airport for $15 plus 9% sales tax. The airport restaurant records the transaction this way: Florida Sales Tax Form DR-15 8 -29

Deferred Tax Results from differences between GAAP net income and IRS taxable Income based on different accounting rules. Definition – Recording GAAP net income now, but deferring payment of some of its income tax expense to future years. o For example – different depreciation methods can be used for GAAP and IRS o Straight Line for financial statements o Double Declining Balance for tax return Steps: Calculate both amounts of taxes due based on GAAP and IRS. One of the following two situations will apply: 1. If GAAP tax amount is greater than IRS amount, a deferred tax liability is created for the difference. 1. 2. 3. Debit - Income Tax Expense for full amount of GAAP income tax Credit - Income Tax Payable for the amount due the IRS Credit – Deferred tax liability for the difference (amount due at a future date) 8 -30

Steps: Calculate both amounts of taxes due based on GAAP")

Deferred Tax (Cont. ) Steps: Calculate both amounts of taxes due based on GAAP and IRS. 2. ) If GAAP tax amount is less than IRS amount, a deferred tax asset is created for the difference. 1. 2. 3. Debit - Income Tax Expense for full amount of GAAP income tax Debit – Deferred tax asset for the difference Credit - Income Tax Payable for the amount due the IRS 8 -31

¡ Informational purposes only – Target - Deferred tax assets and liabilities are recognized for the future tax consequences attributable to temporary differences between financial statement carrying amounts of existing assets and liabilities and their respective tax bases. Deferred tax assets and liabilities are measured using enacted income tax rates in effect for the year the temporary differences are expected to be recovered or settled. Tax rate changes affecting deferred tax assets and liabilities are recognized in income at the enactment date.

Check-up… 1. If I have a balance of $10, 000 in the deferred revenue account and I provide the services to earn 50% of this balance, what journal entry do I record? 1. 2. 3. 4. Debit cash for $5, 000 and credit deferred revenue for $5, 000 cash for $10, 000 and credit deferred revenue for $10, 000 revenue for $5, 000 and credit deferred revenue for $5, 000 and credit revenue for $5, 000 2. I take out a $100, 000 loan (and I receive the cash) payable in equal installments (10% of principal each year) over the next 10 years. How do I record the initial transaction? 1. Debit Cash for ______, Credit CPLTD for ________, and Credit LTD for _______. 3. I make a $100 sale of merchandise and also collect an additional 10% in sales tax. How much revenue do I recognize for the sale? 1. 2. 3. 4. $100 $110 $90 None

Part B Estimates: Contingencies 8 -34

LO 5 Apply the appropriate accounting treatment for contingencies Contingent – definition: Subject to chance Contingent liability: o An existing, uncertain situation that might result in a loss. o Examples: Lawsuits, product warranties, or environmental problems. 8 -35

LO 5 Apply the appropriate accounting treatment for contingencies o Three possible actions for a contingent liability o Record the loss (Journal entry and post to general ledger account) and denote in the Financial Statement Notes. o Impacts the income statement and balance sheet of the company. o Report in a Financial Statement Note ONLY o Does NOT impact the income statement and balance sheet of the company – only the notes to the financial statements. o Do not report or record o For any contingent liabilities Based on the ensuing criteria, the organization will select one of these three courses of action. 8 -36

Contingent Liabilities The answers to step 1 & 2 below will dictate which action to take for contingent liabilities: 1. Step #1 – Likelihood of payment - Estimate: I. Probable—likely to occur II. Reasonably possible—more than remote but less than probable; or III. Remote—the chance is slight 2. Step #2 – Estimate of the payment amount: I. Known or reasonably estimable; or II. Not reasonably estimable. 8 -37

Contingent Liabilities – 1 of 2 charts Likelihood of Payment Step 1 Probable Step 2 Estimate Amount Reasonably Possible REPORT Known or reasonable estimate Not reasonably estimable RECORD REPORT Remote NO ACTION

Accounting Treatment of Contingent Liabilities – 2 of 2 charts Circumstance ¡ Payment is probable and l l Can be reasonably estimated Cannot be reasonably estimated Action Req. Record Report ¡ Payment is reasonably possible Report ¡ Payment is remote No Action

¡ Legal contingencies We are exposed to claims and")

Contingent Liabilities – Target (Notes) ¡ Legal contingencies We are exposed to claims and litigation arising in the ordinary course of business and use various methods to resolve these matters in a manner that we believe serves the best interest of our shareholders and other constituents. Historically, adjustments to our estimates have not been material. We believe the recorded reserves in our consolidated financial statements are adequate in light of the probable and estimable liabilities. We do not believe that any of the currently identified claims or litigation matters will have a material adverse impact on our results of operations, cash flows or financial condition. However, litigation is subject to inherent uncertainties, and unfavorable rulings could occur. If an unfavorable ruling were to occur, there may be a material adverse impact on the results of operations, cash flows or financial condition for the period in which the ruling occurs, or future periods.

Contingent Liabilities o We RECORD a liability if the loss is probable and the amount is at least reasonably estimable. o How to record a contingent liability - debit to a loss (or expense) account and a credit to a liability. JOURNAL Date Accounts and explanation Loss Contingent Liability Probable Loss on lawsuit 41 Debit Credit 50, 000

https: //www. youtube. com/watch? v=Hrzhq. XG cm 68

Warranties o o o Based on the matching principle, the company needs to record warranty expense in the same accounting period as the sale. A warranty represents an expense and a liability at the time of the sale, because it meets the criteria for recording a contingent liability. o Step 1 – likelihood: probable, step 2 – payment: amount can be estimated. When recording warranty expense and warranty payable, the amount is usually estimated as a % of sales. Steps: o At the time of sale o Calculate warranty estimate o Debit warranty expense and credit warranty payable (creates an account balance used later to actually offset the warranty work when it occurs months or years later). o When warranty work is completed o Debit warranty payable and typically credit cash or inventory. 8 -43

Warranty Example ¡ ¡ Warranties are estimated at 1% of Sales =January Sales = $10, 000. Warranty claims can be handled in a number of ways, here are two common methods: l Issuing new product (inventory) l Repair old product through certified repair centers (cash paid to repair center) Exercise: 1. Calculate Warranty Estimate and record expense 2. Calculate and record actual warranty work ($100, 000) throughout the year based on the following percentages: l 25% are new product issued (inventory) l 75% are repairs paid to certified repair centers (Cash)

Estimated Warranty Payable ¡ Warranty expense is estimated in the year product is sold l Matching principle JOURNAL Date Accounts and explanation Debit Warranty expense 100, 000 Warranty payable Credit 100, 000 Estimate warranty liability for the period Warranty payable 45 100, 000 Inventory 25, 000 Cash 75, 000

FORD Motors – Warranty Payable

In-class Exercise ¡ ¡ ¡ 47 Beginning Balance in Est. Warranty Payable = $3, 000 Sales for 2016 = $161, 000 (1) Estimated Warranty Expense = 7% of Sales (2) During 2016 Paid $8, 000 in warranty claims (cash) Record journal entry for recognizing (1) warrant expense and (2) warranty payments.

In the News… Quality and recall problems continued to weigh on the bottom line. Auto Maker had to shell out an extra $314 million last quarter on top of continuing costs related to warranty and recall repairs -- an expense that lowered its pretax margins in North America by about two percentage points. (WSJ)

Contingent Gains o We do not record contingent gains until the gain is CERTAIN. o Though firms do not record contingent gains in the accounts, they sometimes disclose them in notes to the financial statements 8 -49

Check-up’s 1. Auto Air Bag issues – warranty or contingent loss? 2. Our company stocks and sells bicycle parts in the bicycle part vending machine in UCF’s student Union building. There is a $10 warranty claim 10 months after a part was purchased by a UCF student. We send out a new part to the student - how do we record this transaction? 1) Debit warranty expense 2) Debit warranty payable 3) Credit cash 4) Debit warranty expanse

Notice of Class Action Settlement Regarding Groupon Vouchers To file a claim go to: https: //grouponvouchersettlement. com/ An Important Notice About a Class Action Settlement Involving Groupon Vouchers IF YOU PURCHASED A GROUPON VOUCHER BETWEEN NOVEMBER 1, 2008 AND DECEMBER 1, 2011, YOU MAY BE ELIGIBLE FOR BENEFITS FROM THE SETTLEMENT A proposed settlement has been reached in class action litigation concerning Groupon vouchers, In re Groupon, Inc. Marketing and Sales Practices Litigation, No. 3: 11 -md 02238 -DMS-RBB, and the related state court action, Dremak v. Groupon, Inc. , No. 11 CH-0876 (Ill. Cir. Ct. , Kane County). You may be a member of the class whose rights may be affected by this lawsuit. The purpose of this notice is to inform you of the lawsuit and the settlement so that you may decide what steps to take in relation to it.

Questions to be Answered Chapter 8 – How are currently liabilities used in an organization to finance the operating cycle – how do they impact the financial statements?

Participation Questions – Chapter 8 ¡ ¡ ¡ Which publicly traded company was showing a negative working capital in their 2012 financial results? l Walmart; Eastman Kodak; Apple Computers; or Ford Motors Current liabilities are usually due in more than one year. l True or False What account is “air traffic liability” shown on Southwest Airlines balance sheet similar to? l Sales tax payable; Deferred taxes; Unearned revenue; or Accounts Payable Which public company did we review the contingent liabilities for in class? l Southwest Airlines; Target; Apple Computers; or Eastman Kodak Which publicly traded company was included as an example for their warranty payable estimate? l Southwest Airlines; Eastman Kodak; Apple Computers; or Ford Motors

End of chapter 08 8 -60

- Slides: 60