Chapter 05 Receivables and Sales Mc GrawHillIrwin The

Chapter 05 Receivables and Sales Mc. Graw-Hill/Irwin © The Mc. Graw-Hill Companies, Inc.

Participation Questions Chapter 5 ¡ If I complete all of the assignments for this class, I have a better chance of earning the grade I desire. l ¡ Based on the Wall Street Journal Article, what percentage of all cash holdings of public companies does Apple Computers hold? l ¡ True or False Accounts receivable is considered to be a more liquid asset than inventory. l ¡ 1%, 5%, 15%, or 10% Sales returns and sales allowances are expense accounts, so they do not reduce the revenue number shown on the income statement. l ¡ True or False How many methods are there for recording uncollectible A/R? l 1, 2, 3, or 4

Announcements ¡ Handouts – Pgs. 69 (also, under Chapter 5 in Class Materials as a handout) ¡ Assignments – Due 10/18/15 l Chapter 5 Homework (Connect) – unlimited attempts l Participation questions for Chapter 5 (Webcourses) – 1 attempt ¡ Exam Review 1 - go into Calendar at the top of Webcourses, click on Scheduler, and then click on. Exam 1 Review Appointment. From there you can reserve any of the available spots, which are 30 minutes for each review. ¡ Instructor Tutorial Videos (3 – 8 minutes) – Webcourses class materials and discussion boards

Chapters 4 - 10

$147 billion cash pile accounts for")

APPLE COMPUTERS CASH POSITION Apple's (AAPL +0. 33%) $147 billion cash pile accounts for 10 percent of the overall cash held by U. S. corporates, according to Moody's Investors Service, up from 9. 5 percent at the end of 2012. U. S. corporates held a total of $1. 48 trillion in cash as of June 30, up 2 percent from the previous record $1. 45 trillion at the end of 2012. The survey covers 1, 067 non-financial companies based in the U. S. and rated by Moody's. The technology sector is the most cash-flush of all industries, with the top four cash kings -- Apple, Microsoft (MSFT +1. 01%), Google (GOOG +0. 11%), Cisco (CSCO +0. 34%) -- holding a collective $329 billion. Yet Apple's cash hoard is almost double that of Microsoft, for example, which has $77 billion. (Microsoft owns and publishes Top Stocks, an MSN Money site. ) Apple has been active in returning cash to shareholders over the past 18 months. In April, the company pledged to spend $60 billion in buying back its stock by the end of 2015. By June, it had repurchased $16 billion worth of its stock.

")

Apple Balance Sheet (Partial)

Questions to be Answered Overall - What is financial reporting’s role in today’s American society? Chapters 4 – 10 – dive deeper into each area of accounts to understand the associated accounting rules and the impact to the income statement and balance sheet. Chapter 5 – What is the relationship between Revenue and Accounts Receivable, and how might selling our products on credit (on account) impact our earnings (income statement)?

Part A Sales and Recognition of Accounts Receivable 5 -9

Gross Sales versus Net Sales ¡ ¡ ¡ Sales Discounts – reduction")

1. ) Gross Sales versus Net Sales ¡ ¡ ¡ Sales Discounts – reduction in the amount our customer pays on their A/R based on early payment of a sale previously recorded. Sales Allowances – reduction or partial refund of the sales price after the sale has been recorded. Sales Returns – customer returns a product after the sale has been recorded.

¡ Apple Computers

Sales Discounts, Allowances, and Returns Contra Revenue Accounts Always after revenue has been recognized.

LO 2 Calculate net revenues using discounts, returns, and allowances Sales Discount o Not a reduction in sales price before revenue is recognized. o It’s a discount to the amount paid (our A/R owed by customer), intended to provide incentive for quick payment. o The amount of the discount available to our customers and the available time period are communicated in short-hand terms such as 2/10, n/30. o “ 2/10” indicates the customer will receive a 2% discount if the amount owed is paid within 10 days. o ‘n/30, ” means that if the customer does not take the discount, full payment is due within 30 days. 5 -13

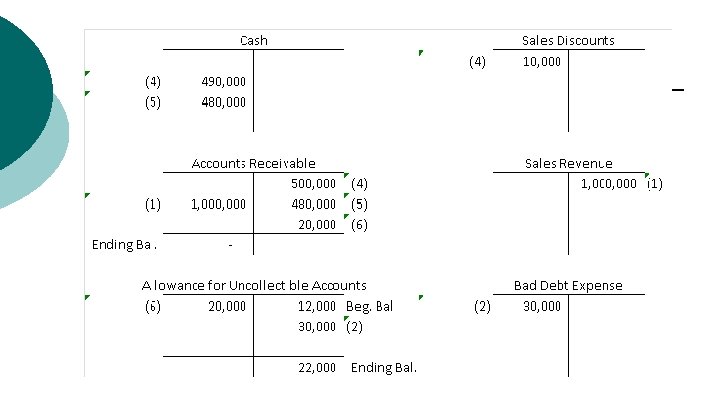

Sales Discount Example #1 Steps used to calculate and record sales discounts. • When the payment is received for a previous credit sale, calculate if a sales discount is due based on ‘terms’ provided. • 2/10 net 30 equals a 2% discount on the gross sales number. • When recording the payment, • Debit cash for the amount received. • Debit Sales Discounts (contra account) for the amount of the discount. • Credit A/R for the gross amount owed to remove amount owed by customer.

Example #2 - First scenario, assume Dee pays on March 10 th, which is within the 10 -day discount period: $400 sale – terms 2/10 n 30 5 -15

First scenario, assume Dee pays on March 10 th, which is within the 10 -day discount period 5 -16

Second scenario, assume that Dee waits until March 31 to pay, which is not within the 10 -day discount period Link’s Dental records the following entry at the time he collects cash from Dee. Notice that there is no indication in recording the transaction that the customer does not take the sales discount. This is the typical entry to record a cash collection on account when no sales discounts are involved. 5 -17

Sales Return and Allowances Sales Return If a customer returns a product it is sales return. After a sales return, o we reduce the customer’s account balance if the sale was on account or o we issue a cash refund if the sale was for cash. Sales Allowances If a customer does not return a product, but the seller reduces the customer’s balance owed or provides at least a partial refund because of some deficiency in the company’s product or service, we call that a sales allowance 5 -18

Sales Return Example - $400 sales is recognized Steps used to record sales returns: • When a customer returns an item, the full amount of the return is recorded in the following manner – • Debit Sales Returns (contra account) for the amount of the return. • Credit A/R for the full amount of the return to show that the customer no longer owes that money. Important - The amount of the actual revenue account is left unchanged and then customer returns product/service

Sales Allowance Example - $400 sale and $50 allowance Steps used to record sales allowances: • When a company issues a sales allowance after revenue has been earned and recorded, the full amount of the allowance is recorded in the following manner – • Debit Sales Allowance (contra account) for the amount of the allowance. • Credit A/R for the full amount of the allowance to show that the customer owes less money. Important - The amount of the actual revenue account is left unchanged

Sales Allowance Example On March 5, after Dee gets her teeth cleaned but before she pays, she notices that another local dentist is offering the same procedure for $350. Dee brings this to Dr. Link’s attention and because his policy is to match any competitor’s pricing, he offers to reduce Dee’s account balance by $50. Link’s Dental records the following sales allowance entry. 5 -21

Part B Valuation of Accounts Receivable Are they all Collectible? What amount should be shown on the Balance Sheet? 5 -22

Receivables – Accounts or Notes ¡ ¡ Third most liquid asset – after cash and short-term investments Acquired mainly by: l l l Selling goods and services (accounts/trade receivable) Lending money via formal contracts (notes receivable) Other (loans to officers/employees) Copyright © 2010 Pearson Education Inc. Publishing as Prentice Hall. 23

Accounts Receivable ¡ ¡ ¡ 24 Amounts collectible from customers Balance in general ledger l Control account ¡ Summarizes total amount due from all customers ¡ Should be same amount as total in subsidiary ledger Subsidiary ledger l Separate account for each customer l Total of all customer accounts should be same as control account in general ledger

Accounts Receivable - Amounts collectible from customers Subsidiary Ledgers Customer 1 General Ledger Control Account $3, 000 Accounts receivable $10, 000 Total $10, 000 Customer 2 $4, 800 Customer 3 $2, 200

are paying")

Accounts Receivable Aging Process of determining which customers (in the subsidiary ledgers) are paying on time, which are not, and how far behind they are behind the due date. This analysis assists in estimating uncollectible amounts and in establishing credit guidelines. Example: Apple Computers – Accounts Receivable Aging (in thousands). Sales made on January 1 st to the following customers: • Walmart $15, 000 • Target $10, 000 • Costco $5, 000

January 31 st General Ledger Balances for Accounts Receivable/ Sales Accounts Receivable Aging

February 28 th General Ledger Balances for Accounts Receivable/ Sales Accounts Receivable Aging

March 31 st General Ledger Balances for Accounts Receivable/ Sales Accounts Receivable Aging

April 30 th General Ledger Balances for Accounts Receivable/ Sales Accounts Receivable Aging

Kramer – write-off http: //www. youtube. com/watch? v=XEL 65 gyw w. HQ&index=1&list=RDXEL 65 gyww. HQ ¡

")

Apple Balance Sheet (Partial)

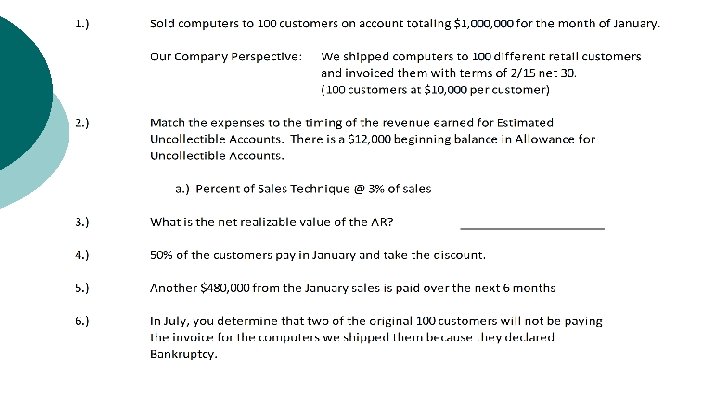

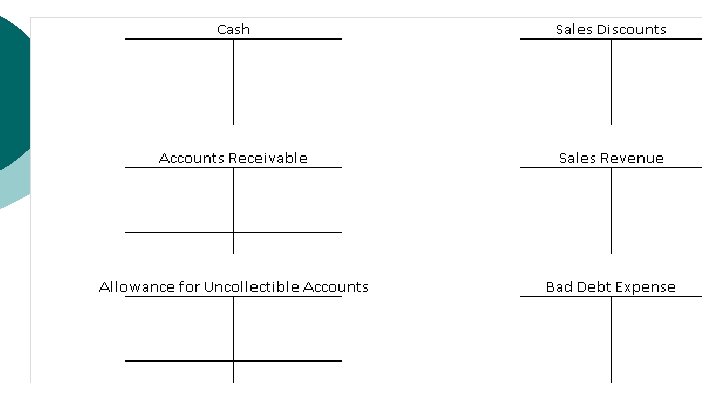

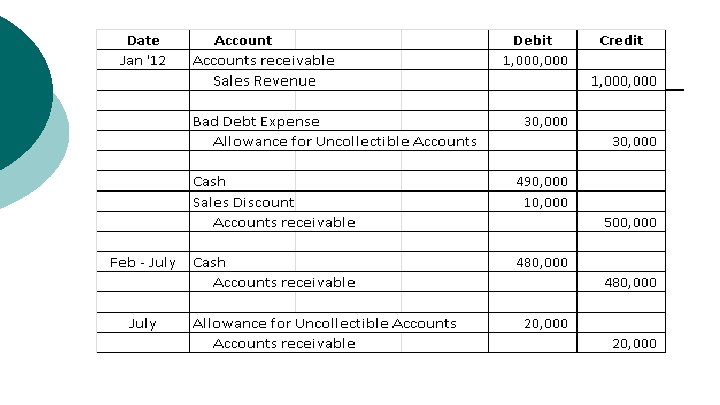

Issue – How do you record A/R that is determined to be uncollectible? Select the METHOD for recording uncollectible A/R (ONLY TWO METHODS!) l Direct write-off method (Method #1) ¡ Non GAAP ¡ The amount of the write-off is known and occurs many months after revenue is earned, which is in opposition to the matching principle. l The Allowance method (Method #2) ¡ GAAP ¡ The amount of the write-off is estimated and occurs in the same period as the revenue is earned, which is in accordance to the matching principle.

How to Handle Uncollectible Accounts Step 1 - Select method for recording Uncollectible Receivables 1. ) Direct Write Off Method (Non-GAAP) Step 2 – how to calculate the amount of bad debt OR 2. ) Allowance Method (GAAP) Percentage of Sales Percentage of Accounts Receivable (aging)

METHOD 1 - Direct Write-Off Method ¡ ¡ Records expense when a specific account determined to be uncollectible (many months after revenue is earned) l Amount is KNOWN l Required for tax purposes (WHY? ? ? ) Inferior to Allowance method – not GAAP l Poor matching of uncollectible-account expense against revenue JOURNAL Date Accounts and explanation Bad Debt Expense Accounts Receivable Write off customer account Debit Credit 10, 000

METHOD 2 - Allowance Method The amount of the write-off is estimated based on the company’s collection experience and occurs in the same period as the revenue is earned, which is in accordance to the matching principle. This process introduces two new accounts: Allowance for Uncollectible Accounts & Bad Debt Expense. 1. 2. Bad Debt Expense – the estimated uncollectible amounts are debited to “Bad Debt Expense” during the period the revenue is earned. ‘Allowance’ for Uncollectible Accounts is credited to set up ‘fund’ the write-off that actually take place in the future. 1. Contra-asset (companion account is Accounts Receivable) 2. Net effect is to show amount of receivables that are expected to be collected 1. AKA “net realizable value” 36

New Account - Bad Debt Expense o Represents the cost of estimated future bad debts charged to the current period on the Income Statement. o The amount of the adjustment to the allowance for uncollectible accounts will equal the bad debt expense in the journal entry. 5 -37

Net Realizable Value Balance Sheet Current assets: Accounts receivable – Gross Less: Allowance for uncollectible accounts Accounts receivable, net $100, 000 (5, 000) $95, 000 Balance Sheet Current assets: Accounts receivable, less allowance of $5, 000 $95, 000 Balance Sheet – must show only amount that is collectible, which is net realizable value. Formula: Net Realizable Value (Net A/R) = Gross A/R - Allowance

Method #2 – Allowance ¡ Steps 1. 2. 3. Company sells $100, 000 product (revenue) and agrees that customer will pay them at a later date (accounts receivable, AR). See transaction ‘a’ below. In order to match expenses to revenue, the $2, 500 in estimated bad debt is expensed (debit) and the contra asset account is set up to reduce the amount reported for accounts receivable (Allowance for uncollectible accounts). See transaction ‘b’ below. When actual amounts due company are deemed uncollectible – for this example, $2, 500, the AR account is reduced and it is offset by the amount that was estimated to uncollectible in the allowance account. See transaction ‘c’ below.

the Uncollectible Amounts? Percent-of-sales • %")

Allowance Method – How do you Estimate (Calculate) the Uncollectible Amounts? Percent-of-sales • % is applied to EVERY $ of sales and added to allowance contra account. • % Based on Collection Experience Aging-of-receivables • Total allowance balance is based solely on A/R aging quality – age of receivables. • Based the Quality, the total Target Balance of Uncollectible is estimated.

Allowance Method – Calculations to Estimate Uncollectible Accounts Percent-of-sales • % is applied to EVERY $ of sales and added to allowance contra account. • % Based on Collection Experience

Allowance Method – Calculations to Estimate Uncollectible Accounts Aging-of-receivables • Total allowance balance is based solely on A/R aging quality – age of receivables. • Based the Quality, the total Target Balance of Uncollectible is estimated.

Allowance Estimate Calculation #1 - Percent of Sales ¡ Allowance based on estimated Bad Debt Expense as a percent of sales. ¡ Calculated uncollectible amount is always added at full value to Allowance for Uncollectible Accounts. Steps: 1. Calculate the estimated bad debt expense (Sales * % estimated to be uncollectible. 2. Debit amount to Bad debt expense 3. Credit amount to the Allowance account. Example – September sales = $100, 000; 3% of sales are estimated to be uncollectible based on prior experience. Beginning balance in Allowance for Uncollectible Accounts = $2, 000. $2, 500 Written-off at the end of September. ¡

Percent-of-Sales Calculation Estimated % uncollectible credit/total sales Credit or Total Sales Bad Debt Expense JOURNAL Date Accounts and explanation Bad Debt Expense Allowance for uncollectible accounts Recorded uncollectible accounts expense Debit Credit 3, 000

Allowance Estimate Calculation #2 - Aging-of. Receivables ¡ Allowance is based on estimated collectability (Quality) of amounts contained in Accounts Receivable based on the age of each receivable. l Aging schedule ¡ TARGET BALANCE – the total amount calculated as uncollectible based on the A/R aging quality. The Target Balance becomes the Ending Balance in the Allowance for Uncollectible Accounts. The entry to the Allowance account needs to consider the beginning balance to ensure the target balance is achieved. ¡ Steps: 1. Calculate the target balance for the allowance account 2. Subtract the beginning balance in the allowance account from the target balance to estimate the debit to bad debt expense 3. Credit the same amount to the Allowance account.

Accounts Receivable Aging – Terms 2/10 n 30 No payments have been made for the following sales: 11/1/12 – $1, 000 sale to Jones Co. 1/1/13 - $2, 000 sale to Jones Co. 1/31/13 - $3, 000 sale to Jones Co. 2/2/13 - $4, 000 sale to Jones Co. 3/5/13 - $5, 000 sale to Jones Co. What is the likelihood of collecting the money as the date of the receivable “ages”? Copyright © 2010 Pearson Education Inc. Publishing as 46

")

Accounts Receivable - Aging (Cont. )

Age of Account Customer A 1 -30 days 31 -60 days $100 Over 90 days Total Balance $500 Customer B All others 61 -90 days $600 400 5, 000 1, 500 600 400 7, 500 $5, 100 $1, 900 $1, 100 $400 $8, 500 Est. percent uncollectible 1% 3% 8% 20% Allowance balance should be: $51 $57 $88 $80 Totals Allowance for Uncollectible Accounts $31 Balance before adjustment $245 Adjustment needed $276 48 Target balance (ending) equals aging schedule $276

Aging-of-Receivables JOURNAL Date Accounts and explanation Debit Bad Debt Expense 245 Allowance for uncollectible accounts 245 Recorded uncollectible accounts expense Copyright © 2010 Pearson Education Inc. Publishing as Credit 49

Main Difference between % of sales and % of A/R aging % of Sales % of A/R Aging Record full amount of Estimate calculation to Allowance account Record amount to reach Target Balance considering the Beginning Balance

Writing Off Uncollectible Accounts ¡ WRITE OFF UNCOLLECTIBLE AMOUNTS l When our customers do not pay their invoices and we have extinguished our options available to us for collection, we must admit that the monies will not be collected and write off the balance owed to us. ¡ Does not include and/or increase to Bad Debt Expense because that was already debited in the original transaction to set up the allowance account

JOURNAL Date Accounts and explanation Debit Allowance")

Writing Off Uncollectible Accounts (2 nd Example) JOURNAL Date Accounts and explanation Debit Allowance for Uncollectible Accounts Credit 900 Accounts Receivable 900 Write off customer account Allowance for Uncollectible Accounts $900 $3, 000 Bal. Accounts Receivable Bal. $50, 000 $49, 100 $900 No impact on Income Statement 52 $2, 100

Impact of Write-Off Balance Sheet – Before Write Off Current assets: Accounts receivable $50, 000 Less: Allowance for uncollectible accounts Accounts receivable, net (3, 000) $47, 000 Balance Sheet – After Write Off Current assets: Accounts receivable $49, 100 Less: Allowance for uncollectible accounts Accounts receivable, net Copyright © 2010 Pearson Education Inc. Publishing as (2, 100) $47, 000 53

What are we Doing? ? ¡ ESTIMATE UNCOLLECTIBLE AMOUNTS l ¡ Estimating how many of our customers will not pay us for the goods or services we provided to them. We want to estimate this amount and match it to the time frame of the revenue we earned (GAAP). WRITE OFF UNCOLLECTIBLE AMOUNTS l When our customers do not pay their invoices and we have extinguished our options available to us for collection, we must admit that the monies will not be collected and write off the balance owed to us.

Meerkat https: //www. youtube. com/watch? v=XECyt 6 u _r. SY

On September 30, Hilly Mountain Party Planners had a $30, 000 balance in Accounts Receivable During October, the store made credit sales of $161, 000. October collections on account were $137, 000. Uncollectible-account expense is estimated as 4% of revenue. Write-offs of uncollectible receivables totaled $2, 300. JOURNAL Date Accounts and explanation Copyright © 2010 Pearson Education Inc. Publishing as Debit 56 Credit

On September 30, Hilly Mountain Party Planners had a $30, 000 balance in Accounts Receivable During October, the store made credit sales of $161, 000. October collections on account were $137, 000. Uncollectible-account expense is estimated as 4% of revenue. Write-offs of uncollectible receivables totaled $2, 300. 57

JOURNAL Date Accounts and explanation Debit Oct Accounts Receivable 161, 000 Revenue Credit 161, 000 Cash 137, 000 Accounts Receivable 137, 000 Bad Debt Expense 6, 440 Allowance for Uncollectible Accounts Receivable 6, 440 2, 300 58

Percentage of AR Example On December 31, 2012, Darci’s travel has an accounts receivable balance of $250, 000. Allowance for Doubtful accounts has a credit balance of $9, 000 before the year-end adjustment. Estimate the allowance for doubtful accounts based on the percent of accounts receivable method. Use T accounts to show the ledger balances for all of these accounts after the year-end adjustment. 59

Example of Payment of AR after it has already been written off - $1, 000

Notes Receivable ¡ ¡ More formal than accounts receivable Written promise to pay a sum at the maturity date l ¡ 61 Plus interest at stated rate Also called promissory notes

Notes Receivable ¡ ¡ 62 Can be current, long-term or both Terms Creditor Party to whom money is owed; Lender Debtor Party that borrowed and owes money; Maker, borrower Interest Cost of borrowing money; stated as annual percentage rate Maturity date Date when debtor must pay note Maturity value Sum of principal and interest Principal Amount borrowed by debtor Term Length of time from when note was signed to when payment must be made

Principal Date Interest Starts PROMISSORY NOTE $3, 000 Amount June 1, 2013 Date For value received, I promise to pay to the order of Principal Payee (Creditor) Second National Bank Three thousand no/100 s------------ Dollars Maturity Date -------On March 1, 2014 plus interest at the annual rate of 6 percent Patricia Alexander 63 Maker (Debtor)

Interest – for our examples, interest is paid at maturity. ¡ ¡ ¡ 64 Interest rates are usually expressed as an annual percentage rate (APR) For time periods less than a year, a fraction is applied to the APR l # months until loan due date/12 Often interest is computed based on days l Denominator would be days/365 ¡ Banks often use 360 days

and interest are")

6/1/14 $3, 000 note issued at 6% annual interest. Note (principal) and interest are all due 3/1/15. Prepare original and adjusting entry at year-end. Steps: 1. Record the original transaction. 2. Record the adjusting entry to recognize the interest due our organization 1. Debit Interest Receivable and Credit Interest Revenue.

and all interest")

6/1/14 $3, 000 note issued at 6% annual interest. Note (principal) and all interest are due 3/1/15. Prepare final journal entry at receipt of final payment. Steps: 1. Record payment at Maturity 1. Debit cash received. 2. Close out Note Receivable with a credit. 3. Recognize and record interest revenue from current period. 4. Close out Interest Receivable with a credit.

Accounting for Notes Receivable JOURNAL Date Accounts and explanation Debit Credit 2014 6 -1 Notes receivable 3, 000 Cash 3, 000 12 -31 Interest receivable 105 Interest revenue 105 2015 3 -1 Cash 3, 135 Notes receivable 3, 000 Interest receivable 105 Interest revenue 30 67

JOURNAL Date Accounts and explanation Debit Credit

Kelly's Jewelry reported the following amounts at the")

Chapter 5 Practice Problems (Cont. ) Kelly's Jewelry reported the following amounts at the end of the year: total jewelry sales = $621, 000; sales discounts = $13, 100; sales returns = $39, 200; sales allowances = $19, 900. Compute net sales.

At the end of the year, Dahir Incorporated's")

Chapter 5 Practice Problems (Cont. ) At the end of the year, Dahir Incorporated's balance of allowance for uncollectible accounts is $1, 400 (debit) before adjustment. The company estimates future uncollectible accounts to be $9, 900 based on the A/R aging calculation.

During 2012, its first year of operations, Pave")

Chapter 5 Practice Problems (Cont. ) During 2012, its first year of operations, Pave Construction provides services on account of $145, 000. By the end of 2012, cash collections on these accounts total $95, 000. Pave estimates that 25% of the uncollected accounts will be bad debts.

The Physical Therapy Center specializes in helping patients regain motor skills after serious accidents. The center has the following balances on December 31, 2012, before any adjustment: Accounts Receivable = $116, 000; Allowance for Uncollectible Accounts = $1, 200 (credit). The center estimates uncollectible accounts based on an aging of accounts receivable as shown below.

Debit Balance in Allowance Account? January sales = $100, 000. Estimated bad debt = 1% of sales. End of January wrote off $1, 500 bad debt.

Participation Questions Chapter 5 ¡ If I complete all of the assignments for this class, I have a better chance of earning the grade I desire. l ¡ Based on the Wall Street Journal Article, what percentage of all cash holdings of public companies does Apple Computers hold? l ¡ True or False Accounts receivable is considered to be a more liquid asset than inventory. l ¡ 1%, 5%, 15%, or 10% Sales returns and sales allowances are expense accounts, so they do not reduce the revenue number shown on the income statement. l ¡ True or False How many methods are there for recording uncollectible A/R? l 1, 2, 3, or 4

- Slides: 78