Capital Account Convertibility in India Capital account is

Capital Account Convertibility in India • Capital account is made up of both the shortterm and long-term capital transactions such as investments in financial and non-financial assets • The Capital Transaction may be Capital outflow or capital inflow • Capital account convertibility (CAC) or a floating exchange rate means the freedom to convert local financial assets into foreign financial assets and vice versa at market determined rates of exchange • Capital account convertibility allows anyone to freely move from local currency into foreign currency and back

is the freedom to convert local financial assets")

• Capital Account Convertibility (CAC) is the freedom to convert local financial assets into foreign financial assets at market determined exchange rates. • Referred to as ‘Capital Asset Liberation’ in foreign countries, it implies free exchangeability of currency at lower rates and an unrestricted mobility of capital • India, at present has partial capital account convertibility with certain limits and caps on FDI • In India there are conflicting views regarding whether to move towards full convertibility of capital account or not • CAC and SS Tarapore Committee

• CAC is related with flows of portfolio capital, FDI flows, flows of borrowed funds and dividends and interest payable on them. • Under CAC, a currency is freely convertible into foreign currency and vice-versa at market determined exchange rate • Convertibility of rupee on capital account means those who bring in foreign exchange for purchasing stocks, bonds in Indian stock markets or for direct investment can get them freely converted into rupees without taking any permission from the government

• Dividends, interest, capital gains earned on direct investment can be converted into foreign currencies at market determined exchange rate between these currencies and repatriate them • Capital convertibility is risky, makes foreign exchange rate more volatile. It is introduced only some time after the introduction of convertibility on current account when exchange rate is relatively stable, deficit in balance of payments is well under control and enough foreign exchange reserves are available with the Central Bank

1. Availability of large funds to")

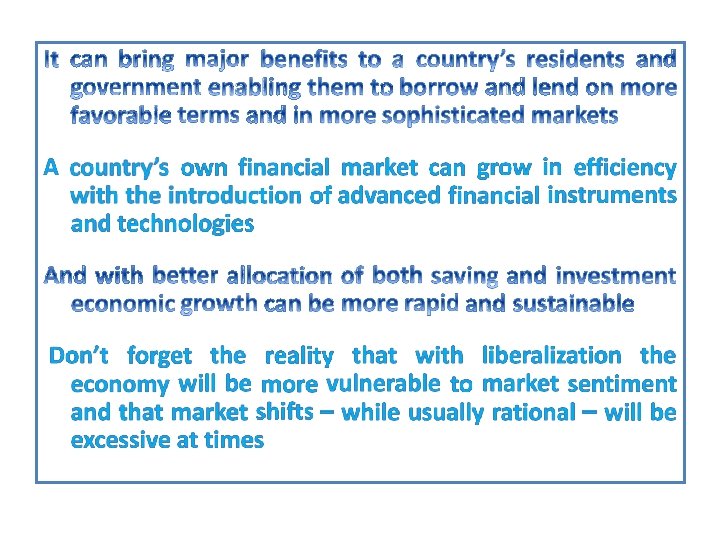

The Benefits of Capital Account Convertibility (Tarapore Committee) 1. Availability of large funds to supplement domestic resources and thereby promote economic growth. 2. Improved access to international financial markets and reduction in cost of capital 3. Incentive for Indians to acquire and hold international securities and assets 4. Improvement of the financial system in the context of global competition

1. Encouragement to exports increasing profitability. 2. Encouragement to import substitution 3. Incentive to send remittances from abroad: 4. A self – balancing mechanism to correct BOP 5. Specialization in accordance with comparative advantage 6. Integration of World Economy

was")

At the time of independence the Foreign Exchange Regulation Act 1947 (FERA) was enacted with the object of regulating certain dealings in foreign exchange and the import and export of currency and bullion The focus of this act was on dealings in Foreign exchange and payments which directly affect foreign exchange resources. This act was later replaced by the Foreign Exchange Regulation, Act, 1973, which we call FERA. Later FERA was laid to rest and its successor is now FEMA

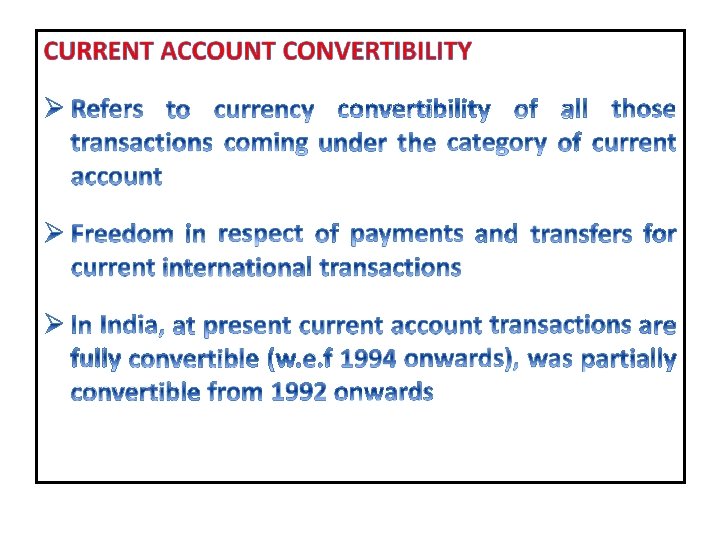

Full Convertibility of Rupee on Current Account • In 1992, Government announced intention to introduce the full convertibility on the current account in 3 to 5 years • Full convertibility means no RBI dictated rates and a unified market determined exchange rate regime • Encouraged with the success of the LERMS, the government introduced the full convertibility of Rupee in Trade account (means only merchandise trade no service trade) from March 1993 onwards • With this the dual exchange rate system got automatically abolished and LERMS was now based upon the open market exchange • The full convertibility of Rupee was followed by stability in the Rupee Rate in the next many months coming up

• In August 1994, declared full convertibility of Rupee on Current account with announcing some relaxations as per requirements of the Article VIII of the IMF These were: • Repatriation of the income earned by the NRIs and overseas corporate bodies of NRIs in a Phased manner in 3 years period • Ceiling for providing foreign exchange foreign tours, education, medical treatment, gifts and services was made just an indicative • Above this ceiling, foreign exchange could be obtained for payments, while making a reference to RBI • Principal amount on the NRNR (Non Resident Non Repatriable) Accounts was non repatriable, the interest was made repatriable

1. Encouragement to exports 2. Encourages import substitution 3. Incentive to remittances from abroad 4. Reduction in Malpractices 5. A self – balancing mechanism

- Slides: 12