CA SURBHI D KHIWANSARA B COM CS FAFP

CA SURBHI D. KHIWANSARA B. COM, CS, FAFP, NATIONAL GST FACULTY

Means any return")

DEFINITION UNDER GST Sr. No. Term Section Definition 1. Return 2(97) Means any return prescribed or otherwise required to be furnished by or under this Act or the rules made thereunder. 2. Tax Period 2(106) Means the period for which the return is required to be furnished. 2(117) Means a return furnished under Sec. 39(1) on which self-assessed tax has been paid in full. 3. Valid Return

RETURNS UNDER GST Periodicity Due Date in Succeeding Month Section/ Return Rule Furnishing Details of Outward Supplies Monthly 10 th S. 37 Rule -1(1) 2 Filing of Monthly Details of Inward Supplies Monthly 15 th S. 38(2) Rule -2(1) 3 Monthly Return Monthly 20 th S. 39(1) Rule -3 4 Composition Taxable Person Quarterly 18 th S. 39(2) Rule – 4 5 Return For Non-Resident Taxable persons Monthly 20 th S. 39(5) Rule -5 Details of Supplies of OIDAR Services provided by person located outside India to a nontaxable in India. Monthly 20 th Rule -5 A Form GSTR Nature of Compliance/ Category of tax Payer 1 5 A

RETURNS UNDER GST Form GSTR Nature of Compliance/ Category of tax Payer Periodicity Due Date in Succeeding Month Section/ Return Rule 6 Return for Input Service Distributors Monthly 13 th S. 39(4) Rule -6 7 TDS Return Monthly 10 th S. 39(3) Rule -7 8 Statement of TCS Monthly 10 th S. 52(4) Rule -8 11 Inward Supply statement by UIN holders Monthly - Rule-23 Annual 31 st December S. 44 Rule -21 9 Annual Return

RELAXATION FOR FIRST 2 MONTHS §For the first two months (i. e. for July and August), the tax would be payable based on a simple return= Form GSTR-3 B. §Form GSTR-3 B = Summery of outward and Inward supplies, which will be submitted before 20 th of the succeeding month. §Due date for submitting invoice wise details in regular GSTR 1 for the months July and August 2017 will be as follows. Month GSTR-3 B GSTR-1 GSTR-2 (Auto Populated from GSTR-1) July, 2017 20 th August 1 st -5 th September 6 th -10 th September 16 th -20 th September 21 st -25 th September Aug, 2017 20 th September * No late fees and penalty would be levied for the interim period

RETURN PROCESS UNDER GST Upload GSTR-1 Communication of details modified in form GSTR-2 to supplier in GSTR 1 A Auto Drafted GSTR 2 A Based on details from GSTR-1 filed by other Suppliers Supplier to accept modifications by 17 th But not before 15 th Generate GSTR-2 by accepting / rejecting / modifying details from GSTR 2 A Filing of GSTR-3 by 20 th

AUTO-GENERATED RETURNS Periodicity Due Date in Succeeding Month Section/ Return Rule 2 A Auto Drafted details of supplies to the Recipient (Paying tax U/s. 9) Monthly After 10 th S. 37 Rule -1(3) 1 A Communication of auto drafted details of supplies to the Supplier Monthly After 15 th S. 38(3)(4) Rule -1(4) 4 A Auto drafted details to Recipient being a Composition Tax Payer Monthly After 10 th S. 37 Rule -1(3) 6 A Auto Drafted details recipient being an ISD Monthly After 10 th S. 37 Rule -1(3) Form GSTR Nature of Compliance/ Category of tax Payer 7 A TDS Certificate to After payment of Within 5 days TDS to Govt S. 51(3)(4) Rule - 7

AUTO-GENERATED RETURNS Form GSTR Nature of Compliance/ Category of tax Payer 9 A Simplified Annual Return – Composition Dealer 9 B Furnishing of Annual Statement of TCS by Ecommerce Operator 9 C Reconciliation Statement (To whom Audit under GST Liable) Periodicity Due Date in Succeeding Month Section/ Return Rule Annual 31 st December S. 44 Rule -21 Annual 31 st December S. 52(5) Rule 21(2) Annual 31 st December S. 35(5) Rule 21(3)

IMPORTANT POINTS Every registered person to furnish returns Submission of return - Through online mode Return to be filed even if there is no business activity during the return period i. e. nil return Error or omission may be rectified but no revision of returns B 2 B transactions proposed on invoice level – GSTIN, Invoice No. and date, Value, Description, rate of tax and value of Tax.

IMPORTANT POINTS B 2 C invoice wise only for transaction above INR 2. 5 lakh and is interstate. HSN Codes – Goods and Accounting Codes – Services Separate Tables for Debit / Credit Notes / Input Service Distributor Credit / TDS etc. Common e-Return for CGST, SGST/ UTGST and IGST Shall not be allowed to furnish a return for a tax period if the return for any of the previous tax period has not been furnished by him.

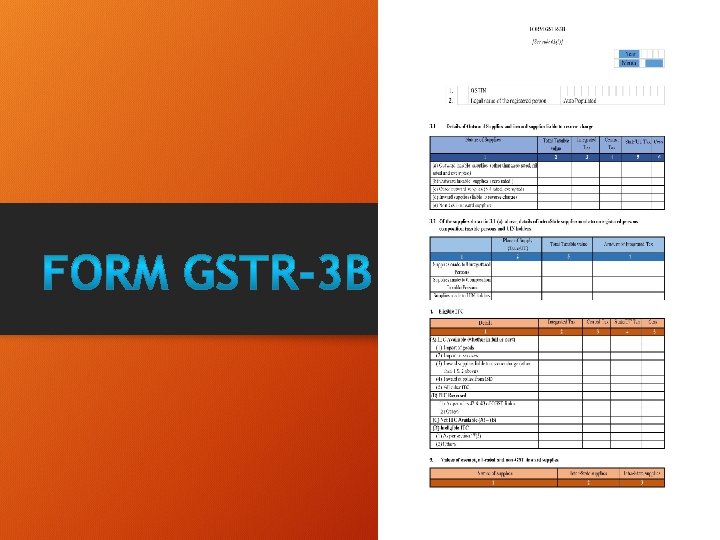

Details of O/w Taxable, Zero rated, Nil rated, exempted, Non-GST o/w Supplies (Taxable value net of sales return and advances recd) TDS/TCS Credit Payment of Tax Details of I/w Supplies liable to reverse charge FORM GSTR -3 B Inter-State supplies made to Unregistered person, Composition taxable person and UIN holders Eligible ITC Value of exempt, nilrated and non-GST inward supplies plus inward supply from compositions dealer.

FORM GSTR-3 B §Where the time limit for furnishing of details in Form GSTR-1 u/s. 37 and in Form GSTR-2 u/s. 38 has been extended and the circumstances so warrant, return in form GSTR-3 B, in lieu of Form GSTR-3, may be furnished. §Form GSTR-3 B required to file for July, 2017 and August, 2017 returns (Refer Slide No. 7) §Value of Taxable Supplies = Value of Invoices + Value of Debit Notes- Value of Credit Notes+ Value of advances received for which invoices have not been issued in the same month- value of advances adjusted against invoices.

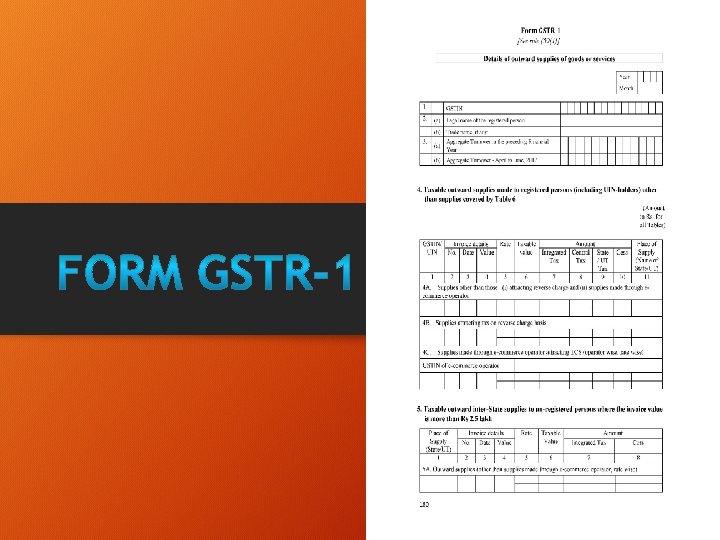

FORM GSTR-1 : - DETAILS OF OUTWARD SUPPLIES The process of return filing under GST shall commence with Form GSTR-1 A registered Person (to whom form is furnish details of all O/w Supplies. applicable) shall Form GSTR-1 includes : (a) Invoice wise Details & (b) Consolidated Detail (c) Debit or Credit note, if any issued during the month for invoices issued previously Details of GSTR-1 auto populated in GSTR 2 A/4 A/6 A

GSTIN NO. For Table")

FORM GSTR-1 : - DETAILS OF OUTWARD SUPPLIES Table No. 1)GSTIN NO. For Table 4 to 13 2) (a) Legal Name of the Registered Person 3) (a) Aggregate Turnover in the Preceding F. Y. (b) Trade name, if any (b) Aggregate Turnover- April to June, 2017 Refer Excel Sheet

REPORTING OF HSN CODE Sr. No. Annual Turnover in the Preceding Financial Year Number of Digits of HSN Code 1. Upto Rs. 1. 50 Cr. 2. More than Rs. 1. 50 Cr. and upto Rs. 5 Cr 2 3. More than Rs. 5 Cr. 4 NIL

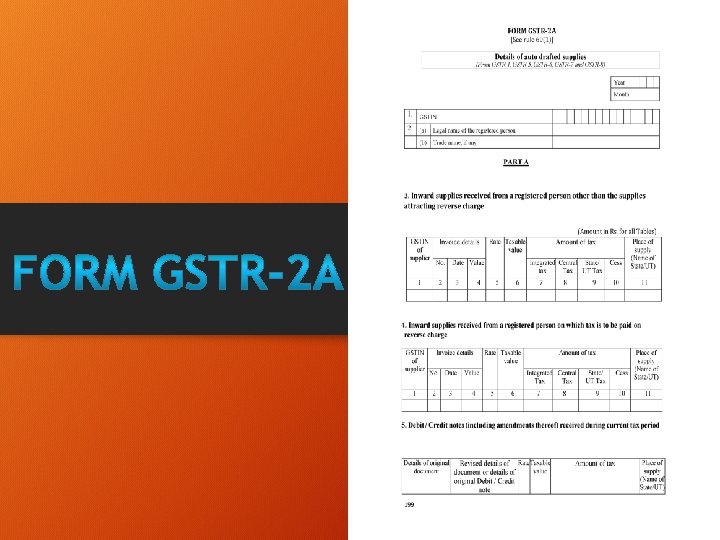

FORM GSTR-2 A Auto drafted details of o/w supplies furnished by n-number of suppliers shall be communicated to respective registered person in form GSTR-2 A Shall be made available to recipient after 10 th of the month following tax period on the common portal. Also include auto drafted details furnished in GSTR -5, 6, 7 and 8

FORM GSTR-2 A Details which were auto generated in GSTR 2 A/4 A/6 A can be modified by Receiver in 4 ways Keep transaction pending for action Addition Correction Deletion

DETAILS CONTENT –GSTR 2 A Table Contents Source Return PART A 3. Inward supplies received from a registered person (other than RCM) GSTR 1/5 4. Inward Supplies received from a registered person on which tax is to be paid on reverse charge GSTR 1/5 5. Debit/Credit Notes including amendments thereof received during current tax period GSTR -1 PART B 6. ISD Credit (Including amendments thereof ) received GSTR-6 PART C 7. TDS/TCS Credit (Including amendments thereof) GSTR-7/8

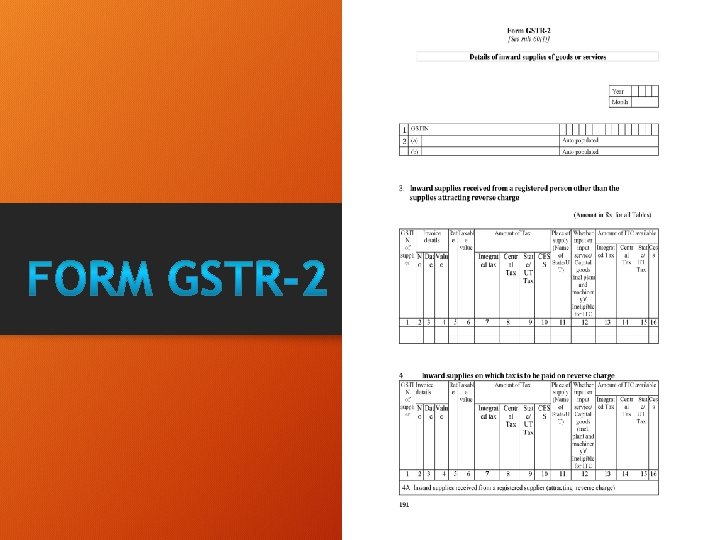

FORM GSTR-2 : - DETAILS OF INWARD SUPPLIES After taking the action in form GSTR-2 A, recipient taxpayer will have to mention whether he is eligible to avail credit or not. The eligible credit relating to inward supplies to be populated in the Electronic Credit Ledger on submission of its return in form GSTR-3 Recipient can claim less ITC on an invoice depending on its use i. e. Whether for business purpose or non-business purpose. For detail content refer excel sheet

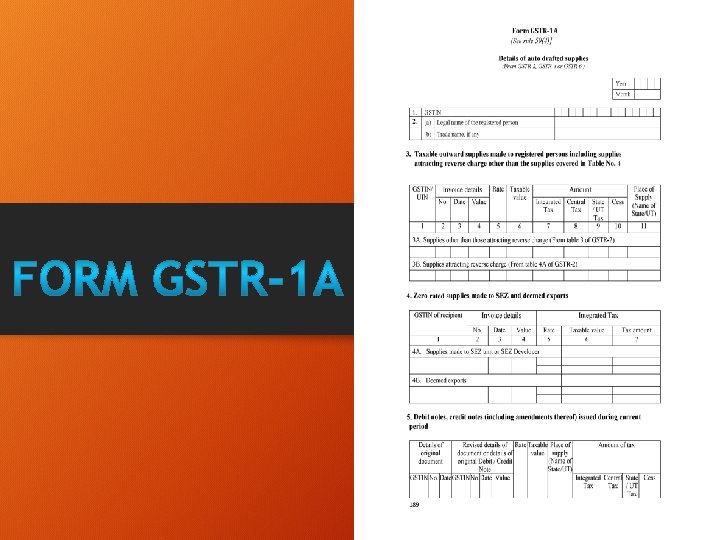

FORM GSTR-1 A Details of Inward Supplies as added, corrected or deleted by the recipients shall be communicated to the supplier in form GSTR-1 A • • Supplier is provided only details of unmatched transactions in GSTR-1 A. • Source of details appearing in GSTR-1 A is GSTR-2, GSTR-4 or GSTR-6 • The Supplier is required to accept or reject the details contained in GSTR-1 A after 15 th but on or before the 17 th of the month succeeding the tax period.

FORM GSTR-1 A If the supplier does not accept the change made by the recipient, it shall qualify as an unmatched transaction in the hands of the recipient. • • GSTR-1 shall contain details of mismatch in respect of : q Taxable supplies to registered person other than RCM. q. Taxable RCM. supplies to registered person attracting q. Zero rated supplies made to SEZ units or developer and deemed exports. q. Debit/Credit notes including amendments there of

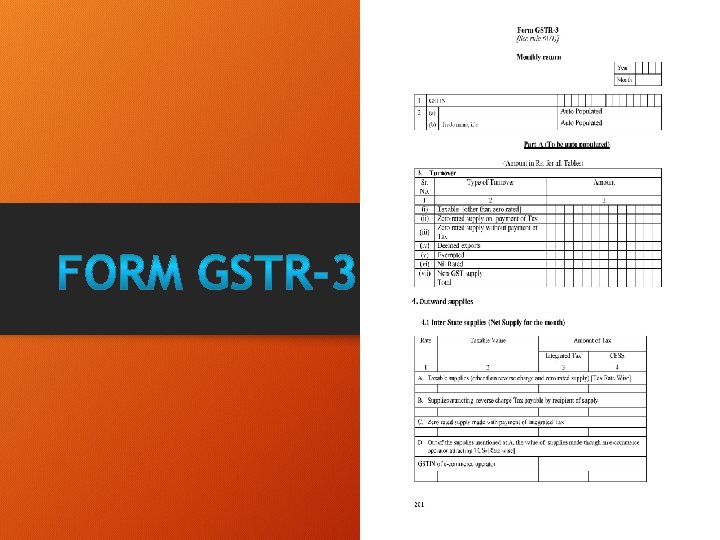

HIGHLIGHTS OF FORM GSTR-3 Form GSTR 3 can be generated only when GSTR -1 & GSTR-2 of the tax period have been filed Automatic updating of Electronic Liability Register, Electronic cash & credit ledger. Part-A of GSTR-3 is auto populated on the basis of GSTR 1, GSTR-1 A and GSTR-2 Part-B relates to payment of tax, interest, late fee etc. GSTR-3 filed without discharging complete liability will not be treated as valid return.

Provision First Return Final Return Annual Return 40 45 44 Section - GSTR-10 GSTR-9; GSTR 9 A(Composition Tax payer); 9 B(E-Comm) Applicability Every Person Every Registered Person required to file return U/s. 39(1) and whose registration has been cancelled. Every Registered Person other than ISD, person paying tax u/s. 51/52, casual taxable person, NR taxable person. Compliance Furnish details of O/w supplies made between date he become liable for registration till the date of grant of registration Furnish Final Return. 1) Furnish annual return in prescribed form for every financial year. 2) In audit cases, furnish audited accounts and reconciliation statement in GSTR-9 C Normal Due Date 3 months from date of cancellation or date of order of cancellation, whichever is later. On or before 31 st December following end of the financial year. Form Due Date Registered

MATCHING Details of inward supply furnished by a receiver to be matched with details of output supplies furnished by corresponding supplier Matching of claims relating to reduction in output tax (e. g. Credit Notes) REVERSAL Details not matching resulting in excess to be communicated to both supplier and receiver Details communicated but not rectified by supplier to be added to the output tax liability of recipient Duplication resulting in excess also to be added to output tax liability of recipient RECLAIM Recipient entitled to reduce output tax liability if supplier rectifies the return within prescribed timelines

MATCHING, REVERSAL AND RECLAIM OF ITC • The Claim shall be matched : - With corresponding details of O/w supply furnished by the concerned supplier in the same or earlier month, following details shall be matched. a) GSTIN of Supplier b) GSTIN of Recipient c) Invoice or Debit Note No. d) Invoice or Debit Note Date e) Tax Amount • • • With the IGST paid on Import of goods by him For Duplication of Claims of ITC

Allowed till Due date of furnishing of return for the month")

RECTIFICATION (Sec. 39) Allowed till Due date of furnishing of return for the month of September following the end of the F. Y. or furnishing of Annual Return whichever is earlier. NON-FILING Cancellation of registration for non-filing of returns for 3 consecutive tax periods for tax payers under Composition Scheme or 6 months for other taxable person. BLACKLISTING OF DEALERS Compliance rating to be introduced. Fall below prescribed level would lead to blacklisting. LATE FEE (Sec. 47) Nature of Compliance Nature of Default Amount of late fee Furnishing of details required u/s. 37 or 38 or returns u/s. 39 or 45 Details or returns not furnished within due date Furnishing of annual return U/s. 44 Return not furnished Rs. 100 per within due date day Rs. 100 per day Maximum Late Fee Rs. 5000 ¼% of turnover in the state /UT

surbhijain 3012@outlook. com 9405911942

- Slides: 40