Business Tax Burdens and Tax Reform James R

Business Tax Burdens and Tax Reform James R. Hines Jr. University of Michigan and NBER Brookings Institution September 8, 2017

Business tax reform options. • Possible business tax reform directions: ▫ Restructure business taxes in a revenue neutral manner. ▫ Reduce business tax rates and therefore tax collections. ▫ It is also possible to restructure and reduce business taxes. • While the first of these clearly has the potential to improve resource allocation, it would have little effect on aggregate business tax burdens. • To be clear, reducing statutory tax rates and making up for the lost revenue by expanding the business tax base will not (much, if at all) improve aggregate business incentives – because it is not possible to reduce all marginal tax rates while keeping average tax rates unchanged.

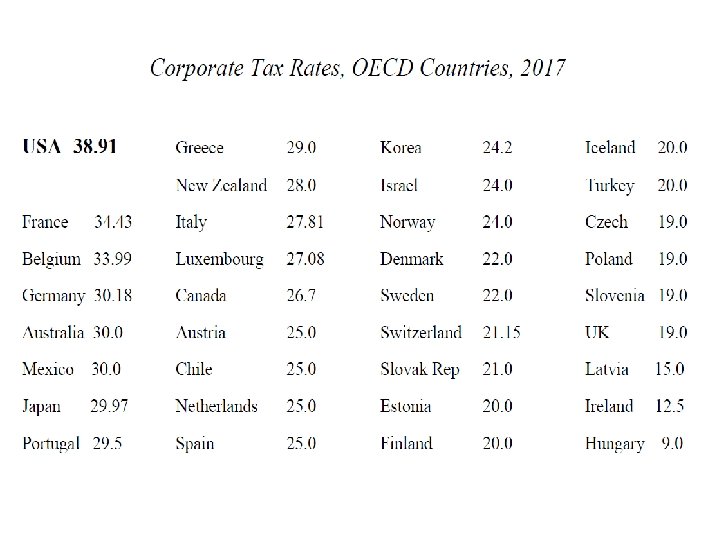

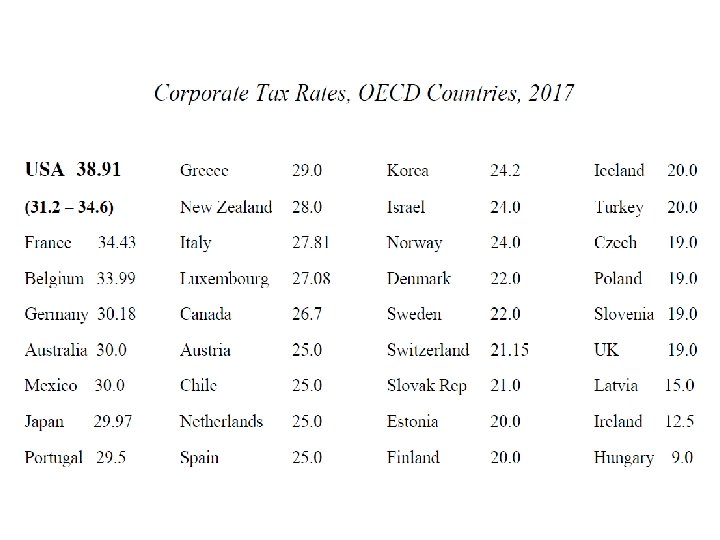

Tax rates, here and there. • The 35% U. S. federal corporate tax rate is the highest among OECD countries; adding average state corporate taxes makes it 38. 9%. • Only three other OECD countries have tax rates above 30%: France, 34. 4%; Belgium, 34. 0; and Germany, 30. 2%. • Non-OECD countries also have lower tax rates (e. g. China, 25%). • Tax burdens can differ for reasons other than just statutory tax rates: there are important exclusions, deductions, and tax credits. • These favorable tax provisions are collectively known as “tax expenditures. ” Prominent U. S. corporate tax expenditures are: ▫ ▫ ▫ Favorable depreciation of capital investment, particularly equipment. Favorable treatment of R&D expenses. Domestic production activities deduction. Low-income housing tax credit. Deferral of U. S. taxation of most unrepatriated foreign income (appears as a U. S. tax expenditure only because the U. S. unlike other countries attempts to tax the foreign incomes of its resident companies).

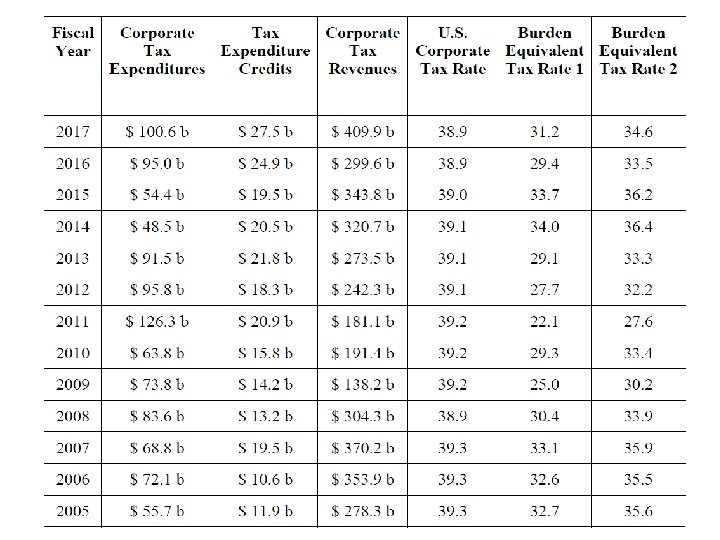

U. S. corporate tax burdens. • It is possible to compare business tax burdens by adjusting corporate tax rates for favorable tax provisions. • The paper offers a method of doing so, which produces lower-bound and upper-bound tax rate estimates based on published corporate tax expenditure numbers. ▫ Lower bound: if businesses do not respond to tax reductions by increasing the favored activity. ▫ Upper bound: if businesses respond so much that all of the favored activity is due to tax benefits. • The 2017 U. S. estimates: 31. 2 – 34. 6%. • In other years the implied U. S. rates are higher still. • This places the U. S. almost at the top of the OECD even if other countries had no corporate tax expenditures.

• It is clear that U.")

Analysis of burden (…or, burden of analysis…. ) • It is clear that U. S. corporate taxes are high compared to any other country’s corporate taxes. • The high tax burden together with a worldwide tax system makes the United States particularly unattractive from a tax standpoint for multinational firms. ▫ Leads to corporate inversions. ▫ And much more importantly, it produces inversion-like outcomes in which US firms cede foreign business to foreign firms. • This pattern also raises the question of whether, even absent international competition, the current extent of business taxation makes sense. • Diamond/Mirrlees (1971): it is more efficient to tax individuals directly than to do so indirectly through business taxes. • Business taxes are also less equitable than tax alternatives that are available with a progressive individual income tax.

Efficient business taxes. • For any given aggregate business tax burden, efficient taxes: ▫ Address market failures. ▫ Impose relatively lighter burdens on more tax-responsive activities. • Both probably justify the favorable tax treatment of R&D. • To clarify: the current tax treatment encourages R&D in two ways: ▫ Encourages firms to use R&D-intensive production. ▫ Encourages R&D-intensive firms and industries to expand production. • Other current policies such as the domestic production activities deduction (a 9% exclusion of manufacturing-like income) make sense in the context of the tax-responsiveness and international mobility of these activities. • And the U. S. must join the rest of the world in exempting foreign income. • It is important to bear in mind that an efficient tax system does not generally level the playing field. • This reflects the second best nature of taxation. • So tax reform efforts should be loath to remove tax provisions that reduce burdens on mobile and otherwise responsive business activities. • And something must be done about the heavy current U. S. tax burdens.

- Slides: 9