BUSINESS MANAGEMENT PRESENTATION ON TRADITIONAL TECHNIQUES OF CONTROLLING

BUSINESS MANAGEMENT PRESENTATION ON TRADITIONAL TECHNIQUES OF CONTROLLING

TRADITIONAL TECHNIQUES OF CONTROLLING Traditional techniques of controlling refer to the techniques that has been used by business organisations for a longer period of time and which are still in use. Although in present environment these have became outdated, still many companies are using them.

THE VARIOUS TYPES OF TADITIONAL TECHNIQUES : 1. Personal observation 2. Good organization structure 3. Unity of objectives, policies, procedures and methods 4. Statistical reports and analysis 5. Budgetary control 6. Profit and loss control 7. External audit control 8. Overall control criteria

1. Personal observation Observation of actual operations at the workplace is the most effective and the oldest method of control. It also has a psychological impact on the employees. It is the most direct and undistorted means of control. However, personal observation is a time consuming process and a manager cannot afford personal observation all the time. One more negative impact is that , enlightened and self-motivated employees do not like to be closely supervised. Even, the bias of the observer may affect the evaluation.

2. Good organization structure In a good organization structure everybody know the part he has to play and how his role relates to those of others. Such a healthy system of rules and relationships helps to improve productivity and removes obstacles to performance. However, organisations are fallible systems as they are operated in a changing environment by human beings conscious direction and integration of efforts is necessary to counteract such tendencies. In this sense, a sound organization facilitates managerial control.

3. UNITY OF OBJECTIVES, POLICIES, PROCEDURES AND METHODS - When the objectives of the organization are integrated with the objectives of employees, the cooperation and loyalty of people can be secured. - Policies provide a unified direction to operation. Control becomes easier to the extent policies of an enterprise are consistent with each other. - Procedures and methods serve as operational guides in the daily routine of an organization. Standard methods are helpful in ensuring efficient utilization of resources.

4. STATISTICAL CONTROL REPORTS Statistical reports and analyses are an important instrument of control. Analysis of statistical data in the form of averages, percentages, ratios, correlation, etc. , is helpful in control of production, quality, inventory, etc. Statistical reports are analytical documents in the form of tables, graphs, etc. They provide factual data and trends useful for managerial control. These reports reveal whether prescribed policies are being followed or not.

5. BUDGETARY CONTROL Budgetary control is a system of management control in which all operations are planned ahead in the form of budgets and actual results are compared with budgetary standards and necessary actions are taken to ensure the attainment of organizational objectives. Budgets express the objectives and targets of the enterprise in financial and quantitative terms.

TYPES OF BUDGETS • • • Master Budget Functional Budgets Capital and Revenue Budgets Fixed and Flexible Budgets Zero-base Budgeting

1. Master Budget: It is the summary budget incorporating all function budgets. It gives a comprehensive picture of the proposed activities and anticipated results for the entire organization. It is finally approved by the top management. 2. Functional Budgets: A functional or operating budget describes the programme and responsibility of one particular department of the enterprise. Some of the important functional budgets are: a) Sales Budget b) Production Budget c) Materials Budget d) Labour Budget e) Cash Budget f) Production Overheads Budget g) Distribution Overheads Budget h) Administrative Overheads Budget

3. Capital and Revenue Budgets: Capital expenditure budgets gives estimated expenditure on fixed assets like building, plant and machinery, furniture etc. On the other hand, revenue budget shows estimates of income and expenditure on routine operations. 4. Fixed and Flexible Budgets: A fixed budget is prepared for a given level of activity and remains unchanged irrespective of the level of activity actually attained. The main purpose of fixed budgeting is to coordinate sectional activities. A flexible budget shows the cost behavior at various levels of activity. It is very useful as comparisons of actual expenditure with budgeted expenditure can be made at different levels of operations. 5. Zero-base Budgeting: The concept of zero-base budgeting is based on the belief that the future is not a mere projection of the past. It requires thorough and rational analysis of budget commitments. It offers greater flexibility in allocating resources. But it is a very timeconsuming and difficult exercise

6. PROFIT AND LOSS CONTROL Profit and loss control implies control through comparison and analysis of profit or loss of different departments or divisions or branches of the enterprise. A separate proforma profit and loss statement is prepared for each product line or branch. The actual expenses are then compared with the estimates. Any deviations are analyzed and suitable actions are taken. However, it involves much paperwork and duplication of accounting records. Moreover, it is a time-consuming and expensive exercise.

7. EXTERNAL AUDIT CONTROL External audit control involves audit of the financial accounts of an enterprise by a qualified and independent chartered accountant. The external auditor is appointed by the shareholders and he conducts a close and careful examination of the books of account and other relevant documents of the company. He is also expected to certify that the balance sheet gives a true and fair value of the financial health of the company on the specific date. External audit control helps to ensure the accuracy of financial accounts but it does not consider operational aspects of business.

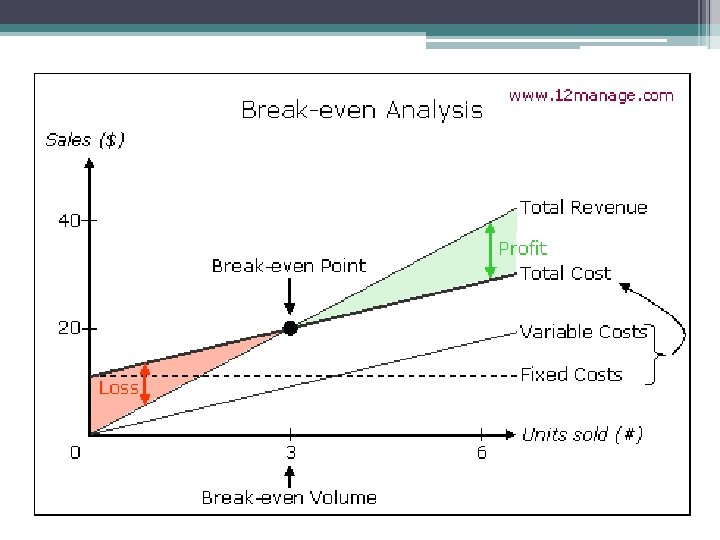

ANALYSIS Break-even point is the point at which total revenue")

8. BREAK-EVEN POINT (BEP) ANALYSIS Break-even point is the point at which total revenue is equal to total cost. It involves analysis of inter-relationships between costs, sales volumes and profits. Therefore, it is also known as cost-volume-profit analysis. Break-even point is very useful in determining profitable volume of output and sales. However, it is based on the assumption that it is possible to identify the fixed and variable components of total cost. Moreover, it changes with the changes in technology, factor prices etc. , and it is not fixed.

9. OVERALL CONTROL CRITERIA Most of the control techniques are designed to regulate specific aspects like costs, profits, etc. such piecemeal control measures are not sufficient for a business enterprise. Control of overall performance is required to judge the total effectiveness of an organization. Such control evaluates management’s total efforts. Moreover control of overall performance helps to overcome weakness of partial control measures.

Some of the important tools of controlling overall performance are as follows: a. Budget summaries b. Comparative reports c. Inter-firm comparisons d. Internal audit e. Ratio analysis f. Value analysis g. Control through key result areas

Rahul(581) Giridharan(582)")

THANK YOU Done by: Sriram(580) Rahul(581) Giridharan(582)

- Slides: 18