BUDGETING IN ROMANIA Den Haag the Netherlands 11

BUDGETING IN ROMANIA Den Haag, the Netherlands 11 November 2004 Michael Ruffner Administrator Budgeting and Management Division

Background • In 1998, OECD started “reviewing” country budget systems • System reviews using functions of budget and stages of budget as base • Learning device – principally descriptive • Romania first non-OECD non-observer country to be reviewed

General Comments • System in movement – Structures and Processes • Impressive reforms over a short period of time – Reforms similar to other countries • Strongly legalistic tradition with ex-ante control

Fiscal Rules • Government Programme – Broad political consensus about EU accession and high level macro-economic goals – Generally successful – lower inflation, general 3% of GDP deficit limit on expenditures, 29% of GDP Debt • Not passed in law

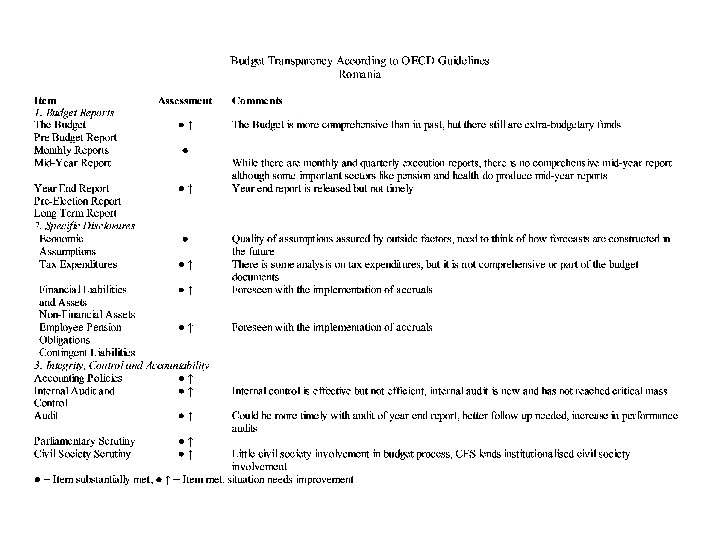

The Budget First things, first … • More comprehensive – fewer off budget funds, quick privatisation • Budget Year + 3 year MTEF – Looks realistic • Economic Assumptions – Good performance, recently – Some steps to ensure independence

Budget Reporting • Monthly, quarterly, annual • No Mid-year Report – Update of economic situation (already provided by National Forecast Commission • Timeliness of annual report

Specific Disclosures • Room for Improvement – Contingent Liabilities – Tax expenditures – Asset registry (How far, linked to accruals) • Privatisation lowers risks -- Where are the ties to budgets? Loan guarantees?

Role of Parliament • Lengthened but still relatively short time frame for action • Rights to amend budget, can’t increase deficit • Does have access to specialised staff – Two chambers work together • Two tiered Committee Structure – Sectoral review followed by budget committee

Budget Execution • Treasury system with 3 levels of credit holders (Ministry, Program, Street level) • Ex-ante Control – “Own” control and “Delegated” control • Tight rules on virement (transfers) • New Internal Audit – just starting • Still ability to overspend

External Audit • Audit Court produces report by December • Previously longer delays, but timing is still not optimal • Court has improved its interaction with media • Court reports to parliament, but there is no audit committee • Capacity for performance audit is being developed • Main audit report discussed in a joint sitting of both houses • Formal vote on budget execution • Parliamentary process largely formalistic

– Very high standard")

Civil Society • Institutionalised consultations through Economic Social Council (CES) – Very high standard (consensus/near consensus) – Other tri-partite discussions • Some academic review – especially in macroeconomic assumptions

Conclusion • Solid Base of Transparency – Improvements happening rapidly – Time needed to implement and judge success of reforms • Internal audit, program budgeting, accruals • New disclosures – Contingent liabilities, Mid year update to parliament, reconciliation line in MTEF

- Slides: 13