Bright Directions 529 College Savings Program The Bright

Bright Directions 529 College Savings Program The Bright Directions College Savings Program is part of the Illinois Savings Pool and is designed to qualify as a qualified tuition program under the provisions of Section 529 of the Internal Revenue Code. The Bright Directions College Savings Program is sponsored by the State of Illinois and administered by the Illinois State Treasurer, as Trustee. Union Bank & Trust Company serves as Program Manager, and Northern Trust Securities, Inc. , acts as Distributor. An investor should consider the investment objectives, risks, and charges and expenses associated with municipal fund securities before investing. The Program Disclosure Statement (issuer’s official statement) is available online at Bright. Directions. com or from your financial advisor and should be read carefully before investing. Investments in the Bright Directions College Savings Program are not guaranteed or insured by the State of Illinois, the Illinois State Treasurer, Union Bank & Trust Company, Northern Trust Securities, Inc. , the Federal Deposit Insurance Corporation, or any other entity. Distributor Trustee & Administrator Program Manager

Increasing College Costs and the Value of a College Degree

College Costs Average Published Charges for Full-Time Undergraduates Public Four-Year In-State Private Nonprofit Four-Year 2016 - 2017 2016 – 2017 Tuition and Fees $9, 650 Tuition and Fees $33, 480 Room and Board $10, 440 Room and Board $11, 890 Tuition, Fees, Room and Board $20, 090 Tuition, Fees, Room and Board $45, 370 Source: The College Board – Trends in College Pricing (2016)

Median Weekly Earnings of Full-Time Workers Age 25 and older $1, 500 $1, 447 $1, 152 $1, 000 $779 $700 $504 $0 Less Than a High School Diploma High School Graduate Some College or Bachelor's Degree Advanced Degree Associates Degree Source: Bureau of Labor Statistics, U. S. Department of Labor, News Release (October 20, 2016)

Unemployment Rates for Recent College Graduates and Other Percent Groups Sources: U. S. Census Bureau and U. S. Bureau of Labor Statistics, Current Population Survey. Federal Reserve Bank of New York (Volume 20, Number 1, 2014) Notes: Rates are calculated as a twelve-month moving average. All workers are those aged 16 to 65; college graduates are those aged 22 to 65 with a bachelor’s degree or higher; recent college graduates are those aged 22 to 27 with a bachelor’s degree or higher; young workers are those aged 22 to 27 without a bachelor’s degree or higher. All gures exclude those currently enrolled in school. Shaded areas indicate periods designated recessions by the National Bureau of Economic Research.

Saving for College

Several Common Ways to Save for College ü Bank or Investment Account ü UTMA Account ü Coverdell Education Savings Account ü 529 College Savings Account

Bank or Investment Account ü Familiar with these accounts ü Can be used for any purpose ü Low interest rate environment currently ü Pay taxes each year on the interest, dividends and capital gains

UTMA Account ü No contribution limits ü Funds can be used for college and other purposes ü Custodian controls the account until the child attains age 21 – then the child controls ü Taxable account – typically taxed at the child’s or the parents tax rate based on the amount of the earnings

Coverdell Education Savings Account ü $2, 000 contribution limit per beneficiary ü Funds can be used for college and K-12 expenses ü Some age and income limitations (ie: age 18 and 30 and income limitations on depositor) ü Tax–deferred growth and tax-free withdrawals for qualified expenses

529 College Savings Account ü Can be used at colleges nationwide ü Account owner maintains control of the account ü No income limitations on contributors ü Contributions may be state income tax deductible ü Tax–deferred growth and tax-free withdrawals for qualified expenses* * Withdrawals for other purposes subject to income tax and an IRS 10% penalty tax

Bright Directions 529 College Savings Program

Bright Directions 529 College Savings Program ü Can be used at qualified colleges in Illinois, nationwide, and even some foreign schools ü Illinois State Income Tax Deduction for Contributions up to: ü $20, 000 married filing jointly ü $10, 000 for individual filers ü Account owner maintains control of the account

Illinois Tax Deduction An individual who files an individual Illinois state income tax return will be able to deduct up to $10, 000 per tax year (up to $20, 000 for married taxpayers filing a joint Illinois state income tax return) for their total, combined contributions to the Bright Directions College Savings Program, the Bright Start College Savings Program, and College. Illinois! during that tax year. The $10, 000 (individual) and $20, 000 (joint) limit on deductions will apply to total contributions made without regard to whether the contributions are made to a single account or more than one account. The amount of any deduction previously taken for Illinois income tax purposes is added back to Illinois taxable income in the event an Account Owner takes a Nonqualified Withdrawal from an Account or if such assets are rolled over to a non-Illinois 529 plan. If Illinois tax rates have increased since the original contribution, the additional tax liability may exceed the tax savings from the deduction.

Bright Directions 529 College Savings Program ü One Account Owner per account ü Important to name a successor account owner ü One beneficiary per account (no age limitations) ü No required annual or minimum contribution

Bright Directions 529 College Savings Program ü Financial Aid Treatment ü Treated as a parental asset (when the parent owns) ü Has minimal impact on financial aid (5. 64% inclusion)

Bright Directions 529 College Savings Program ü Tax-Free Withdrawals for qualified higher education expenses ü Tuition and fees ü Room & board (if enrolled at least half-time) ü Books, supplies, and equipment required for enrollment ü Computer, related peripheral equipment, certain computer software, Internet access ü Expenses for special needs services needed by a special needs beneficiary must be incurred in connection with enrollment or attendance at an eligible educational institution.

Bright Directions 529 College Savings Program ü The following are not considered qualified expenses ü Personal expenses ü Transportation ü Repayment of student loans If the money is used for other purposes (ie: non-qualified withdrawal), the earnings portion is subject to federal and state income tax and a 10% federal penalty tax.

Bright Directions 529 College Savings Program ü What if the beneficiary does not go to college or does not use all of the funds? ü You can change the beneficiary to a “member of the family” (ie: brother, sister, mother, father, niece, nephew, first cousin – see Program Disclosure Statement for complete listing) ü Leave the funds in the program and name a new beneficiary at the appropriate later date ü Take the funds back – if they are not used for college it is considered a non-qualified withdrawal (earnings would be taxable and subject to an IRS 10% penalty) If the money is used for other purposes (ie: non-qualified withdrawal), the earnings portion is subject to federal and state income tax. Possible recapture of any previously claimed Illinois tax deductions, and a 10% federal penalty tax.

Bright Directions 529 College Savings Program ü Out-of-State 529 Plans can be Rolled into Bright Directions ü The contribution portion is eligible for the Illinois state income tax deduction ü Review the out-of-state plan provisions with your financial advisor in the event they have any type of charges or fees ü The IRS allows one same beneficiary rollover per 12 month period Illinois Taxpayers: The Illinois Administrative Code provides that in the case of a rollover from a non-Illinois qualified tuition program, the amount of the rollover that is treated as a return of the original contribution to the prior qualified tuition program (but not the earnings portion of the rollover) is eligible for the deduction for Illinois individual income tax purposes. There may be potential adverse tax consequences if the rollover/transfer is not a qualified rollover. Please review all factors with your tax and financial advisor. Check with your financial advisor for assistance and the steps needed to complete this process.

Bright Directions 529 College Savings Program ü Investment Choice and Flexibility ü 2 investment changes allowed per calendar year ü Quality fund families

Bright Directions 529 College Savings Program 3 Age-Based Tracks 7 Target Portfolios 32 Individual Fund Portfolios

Bright Directions 529 College Savings Program

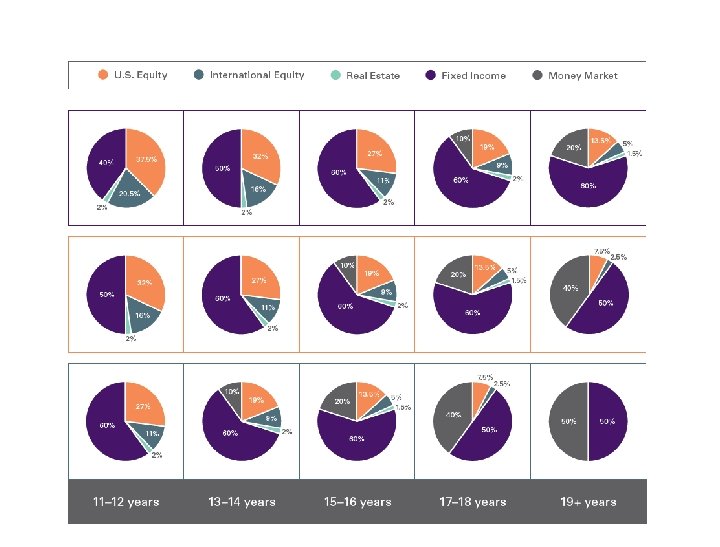

Bright Directions Age-Based Portfolios

Bright Directions 529 College Savings Program A Word About Risk: You can lose money by investing in a portfolio. Each of the age-based, target, and individual fund portfolios involves investment risks, which are described in the Program Disclosure Statement and which should be considered before investing. For example, international investing, especially in emerging markets, has additional risks such as currency fluctuation, economic and political risks, and market volatility. Investing in small, medium, and international companies may increase the risk of fluctuations in the value of your investment and involves greater risks than investing in more established companies. Portfolios that invest in specific industries or sectors, such as real estate, have industry concentration risk. As an example, the portfolios that invest in real estate may perform poorly during a downturn in the real estate industry. Portfolios that invest in bonds are subject to risks such as interest rate risk, credit risk, and inflation risk. In particular, as interest rates rise, the prices of bonds generally will fall which can impact performance. It is important to note that the value of your account will fluctuate with market conditions. When you withdraw funds you may have more or less than your actual investment. For more information on the portfolios and the underlying funds in which they invest see the Program Disclosure Statement. Not FDIC Insured | May Lose Value | No Bank Guarantee

Others Can Contribute to Your Account Invite others to make a gift electronically with Gift. ED. Gift Cards and Deposit Coupons make it easy for others to contribute

Next Steps

The Next Steps § When we sit down we will: § Review the program materials § Determine an amount to save § Select an investment strategy § Complete the enrollment form

My Contact Info NOT FDIC-INSURED. NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY. NOT GUARANTEED BY THE BANK. MAY GO DOWN IN VALUE.

Helping them achieve their dreams: You’re taking that First Step Today!

Illinois Tax Deduction An individual who files an individual Illinois state income tax return will be able to deduct up to $10, 000 per tax year (up to $20, 000 for married taxpayers filing a joint Illinois state income tax return) for their total, combined contributions to the Bright Directions College Savings Program, the Bright Start College Savings Program, and College. Illinois! during that tax year. The $10, 000 (individual) and $20, 000 (joint) limit on deductions will apply to total contributions made without regard to whether the contributions are made to a single account or more than one account. The amount of any deduction previously taken for Illinois income tax purposes is added back to Illinois taxable income in the event an Account Owner takes a Nonqualified Withdrawal from an Account or if such assets are rolled over to a non-Illinois 529 plan. If Illinois tax rates have increased since the original contribution, the additional tax liability may exceed the tax savings from the deduction.

Important Legal Information The Bright Directions College Savings Program is part of the Illinois College Savings Pool and is designed to qualify as a qualified tuition program under the provisions of Section 529 of the Internal Revenue Code. The Bright Directions College Savings Program is sponsored by the State of Illinois and administered by the Illinois State Treasurer, as Trustee. Union Bank & Trust Company serves as Program Manager and Northern Trust Securities, Inc. , acts as Distributor. Investments in the Bright Directions College Savings Program are not guaranteed or insured by the State of Illinois, the Illinois State Treasurer, Union Bank & Trust Company, Northern Trust Securities, Inc. , the Federal Deposit Insurance Corporation, or any other entity. An investor should consider the investment objectives, risks, and charges and expenses before investing. This and other important information is contained in the Bright Directions Program Disclosure Statement, which can be obtained from your financial professional and at Bright. Directions. com and should be read carefully before investing. You can lose money by investing in a portfolio. Each of the portfolios involves investment risks, which are described in the Program Disclosure Statement. Before you invest, consider whether your or the beneficiary’s home state offers any state tax or other benefits that are only available for investments in that state’s 529 plan. Investment Products: Distributor Not FDIC Insured No Bank Guarantee Trustee & Administrator May Lose Value Program Manager

- Slides: 35