Booklet 3 FOREIGN EXCHANGE Foreign exchange is The

• Booklet 3

FOREIGN EXCHANGE Foreign exchange is… • The buying and selling of currencies used in other countries. • Foreign exchange (also shortened to ‘forex’, or ‘FX’) rate is the price that you pay for buying or selling that currency. For example, if you were going to the United States, you would need US dollars (USD, or US$) instead of pounds sterling (GBP, or £). If the exchange rate were 1 GBP = 1. 67 USD, £ 100 would buy US$167.

WHAT USE IS THAT TO ME? The main time when you will see this is when you go on holidays abroad. You will take your £s and exchange them at a given rate for $, € or other international currency. However, foreign exchange also impacts our personal finances. International trade plays a huge part in our national economy. International trade is made up of import and export business. • • Imports – buying things from outside of the UK Exports – selling things from inside of the UK

WHAT USE IS THAT TO ME? Foreign exchange may affect you through… • • • Price of exchanging your money into Euros to go on holiday Buying goods online from overseas (to be delivered here) Owning a business may involve buying and sell things abroad Sending money to family abroad Buying a house abroad (we can dream!) Getting money out of a cash machine when abroad As well as the accepted symbol for a currency, such as £ or $, there is an assigned abbreviation for each currency. This usually comprises a two-letter country code abbreviation and the first letter of the currency name.

FOREIGN EXCHANGE ON HOLIDAY The foreign exchange rate compares the value of one currency to the value of another. You can exchange currencies at any Bureaux de change. This is how much £ 1 buys. If you come back and sell your foreign currency back, they’ll give you less! You have to buy money, so that you can use the medium of exchange (type of money) that is accepted in that particular country. Did you know? Last year each of these exchange rates were better. We now get less of every currency for £ 1 than we did 1 year ago.

BUREAUX DE CHANGE Bureaux de changes are all profit making businesses. They make their money in two ways; • Commission (a one-off, flat fee for using their service) Many will have signs showing “No Commission” to try and attract more customers • Calculating the different prices for different currencies Currency prices change hourly and daily. To counteract this, the BDC sets the price slightly above the accepted price. This protects them from any fluctuations that may occur short term, as well as making them additional profit.

The biggest impact of foreign exchange rates is in terms of international trade – or exporting and importing goods. Every country imports and exports, and has companies that conduct business overseas. When a country or company imports something, it has to pay for that item in the currency of the country from which it is buying it. So it buys the currency; then it buys the item. This type of foreign exchange is generally done automatically through a bank.

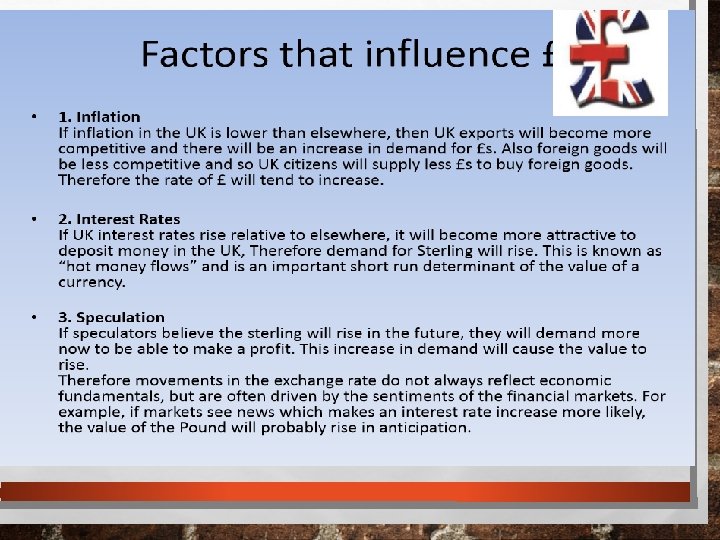

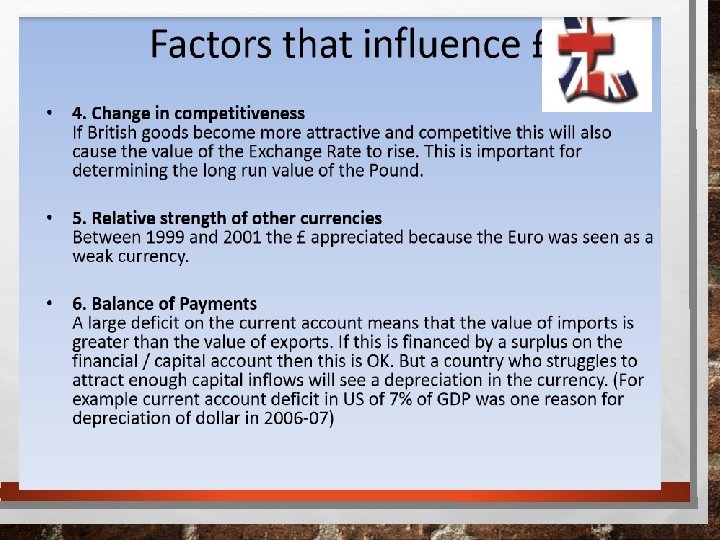

EXCHANGE RATES • Exchange rates are set on the basis of how much people buy and sell a particular currency (through international trade, imports and exports, moving currency internationally). • As the exchange rate is constantly changing, a currency is either strong or weak in relation to others. If a lot of people, organisations or governments are buying a particular currency (in order to pay for imports), the demand will push up the price of that currency. If a lot of different countries were to import goods from the United States, for example, the US dollar would be in demand would be strong.

STRONG CURRENCY • A strong currency means that its value against other currencies is high, owing to high demand • When strong, people then buy more of it - to keep hold of to sell later or to buy goods from that country

1. Strong currency 2. Imported goods are cheaper 3. Exports are more expensive • Why does a strong currency mean that imported good are cheaper? • If imported good are cheaper, why does that mean local businesses may suffer? • How will this impact the other areas? Cheap imports can make it difficult for local businesses to compete: they may have much higher costs than foreign suppliers and may be unable to make a profit at the price at which the foreign supplier is selling their goods.

While it may seem that a strong currency is ideal, it is actually better to have a stable currency (one that is not too strong and has an exchange rate that does not change very much) A stable currency helps exporters and so helps the country in general. Foreign customers need to know what the cost of the goods they buy will be in terms of their own currency. If they are confident that the price will not change, they are likely to buy more – and this leads to a growing economy.

WEAK CURRENCY • A weak currency means that its value against other currencies is low, due to low demand. Using the STRONG currency diagram as a starter, draw your own to represent the impacts of a WEAK currency on the economy and society

WEAK CURRENCY • Increased demand for local goods and services (Imports are more expensive in comparison) • Increased levels of employment (Businesses need more staff due to demand) • Increases the gross domestic product (GDP) of the country. More people in work, paying more tax = Higher GDP

EXCHANGE RATES AND TRADE

EXCHANGE RATES AND TRADE The impact of exchange rates A strong currency • • • Impact on countries Foreign trade may be cheaper to buy in (imports) Impact on society: Economic hardship could occur if businesses are unable to sell their goods Impact on individuals Less spent on holiday costs; incomes could decrease as it becomes cheaper for businesses to buy imports from abroad, therefore spending less on local products A weak currency • • • Impact on countries Foreign trade (imports) may be more expensive, so people buy local instead Impact on society: More jobs may be created locally as demand for local products increases and holidays become less common. Impact on individuals More spent on holiday costs, other costs could decrease as businesses fight to remain competitive. Income could increase as people are needed to produce more goods and services.

• Lesson 2

FINANCIAL PLANNING AND MONEY MANAGEMENT Why should we manage our finances and money? • In Charles Dicken’s famous Victorian novel, David Copperfield, annual income was twenty pounds. This was close to a realistic income in 1850. In Victorian times, people who couldn’t pay debts could be sent to debtor’s prison.

KEY TERMS • Money management • The process of managing money, including budgeting, banking, saving, investing and paying the minimum amount of tax legally required • Budgeting • Part of money management. Making sure your day to day money is managed and that you have enough to pay bills, buy food etc. • Financial planning • Another part of money management. It looks at the person’s needs and objectives (short term and long term) and how best to achieve them

FINANCIAL PLANNING AND MONEY MANAGEMENT Financial Objectives People set objectives to have targets they hope to achieve. In a financial planning context, these come down to two closely linked types: Personal objectives What the individual wants to achieve. Buying a holiday home, going to the Caribbean, buying a new car Financial objectives How the individual will provide the money to reach the personal objective. How much money do you need in 5 years in order to achieve this?

FINANCIAL PLANNING AND MONEY MANAGEMENT Why should we manage our finances and money? • Emergency funds • You never know when your car breaks down or a boiler needs replacing. The suggestion is that between 3 to 6 months essential is an appropriate amount. This would be best stored in a building society. • Make better financial decisions • Avoid unnecessary debt • Help make decisions on savings, spending and progress in reaching goals • Provides a blueprint for families (children) to follow • Helps show what you have to do to get to where you want to be

PLANNING FOR NOW, PLANNING FOR THE FUTURE Short term to long term planning • It is all about managing your NEEDS and your WANTS Short – between 1 week and 12 months Budgeting, saving for short term goals Medium – between 1 year and 5 years Deposit for house, special holiday, college or university, wedding planning Long – longer than 5 years retirement, purchase of “life long” goods (house, mortgage)

There is a need to adjust and review financial plans • Priorities change when moving from one stage of life cycle to another • Anticipating foreseen and unforeseen events will ensure that you have the resources to deal with any emergencies • Plan should be fluid due to the unpredictability of factors that can impact your financial situation

FINANCIAL PROVIDERS: BANKS Banks are ‘proprietary’ organisations, which means they are business owned by, and responsible to, shareholders. They have three main roles: • • • Provide a safe place for people to keep their money Provide a way for account holders to receive payments and pay bills Provide loans and mortgages for those who need to borrow money

BUILDING SOCIETIES Historically building societies have been a place for people to put their savings and receive interest, and the funds raised were used to provide loans for their members to buy a house or pay for other needs. • They now also provide current accounts, other investments and other services like a bank. • The key difference is that they are owned by members, rather than profit driven shareholders.

INSURANCE COMPANIES • Provide insurance policies to help businesses and people reduce financial risk caused by a number of events. They are designed to pay out money to help people who suffer loss from specific events covered in the policy (such as death, serious illness, damage to buildings/vehicles) • You pay into an insurance policy on a monthly/annual basis. If you claim on that policy you receive a pay-out. The reward for the company is if you don’t claim on the policy, they receive your money with no pay-out. INVESTMENT COMPANIES • Invest money for people with a view to making a profit for them. The company has experts who will invest efficiently in stocks and shares of companies that are expected to grow in value. • These represent risk as there is no guarantee of a profit.

Each of these financial providers offer a range of products that you may choose to use. Many of these we have discussed throughout these units

FINANCIAL PRODUCTS: CURRENT ACCOUNT Offered by banks and many building societies. Customer’s money is held in a safe place and is well protected by regulations. Designed for day to day finances, and provide the following main features: • Receive salaries, pensions and other regular payments • Payment of regular bills through direct debits (automatic payments you can set up) • A debit card, allowing the holder to buy things in shops or online, and allows you to take money out of an automatic teller machine (ATM or cash machine)

CONTINUED • Cheque books, allowing you to write cheques which can be cashed. These are far less common with the technology advancements in debit cards. • Online banking allowing you to check your balance and manage payments online or through apps • Interest paid on your balance (money in the account) • Some overdraft options, allowing you to temporarily go into a negative balance. This is a short term measure and usually charges interest • Printed bank statements to show account holders all of the inflows and outflows of the account.

• Savings account Allow you to collect interest (at a larger rate that a current account) on the balance. These can’t be used as day to day accounts and may have restrictions on how often you can withdraw money. • Borrowing products • Insurance products provide a pay-out in case of certain events, such as: Car insurance, death, serious illness or injury, medical treatment, damage or theft of home/business property, medical treatment for pets, motor accidents or theft Did you know? It’s illegal to drive without car insurance.

BUDGETING Everything we have learned about in these units is connected. When one aspect of the economy changes, others are impacted. The same is true of our own personal finances and these financial services and products form part of this budgeting • In order to ensure that we are financially secure, we need to ensure that we use BUDGETING and FINANCIAL PLANNING

BUDGETING A budget is… Part of a financial plan to achieve particular short-term, medium-term and / or long-term goals • Involves estimating money coming in and going out over a certain period of time and making plans to ensure that spending doesn’t exceed income over that period • Then… checking these estimates against actual inflows and outflows • And… accounting for times when you will spend more (family birthdays, Christmas, etc. ) Draw a basic flow diagram to represent how budgeting works

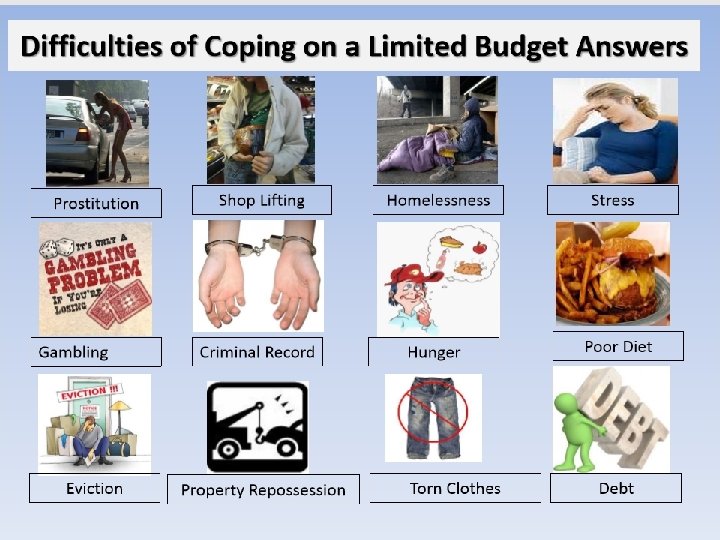

WHY BUDGET? If we do not budget effectively as part of our financial planning it could lead to a number of negative consequences such as; • Overspending Write down as many negative consequences of overspending that you can think of for; Individual Economy Businesses

IMPACT OF YOUR PERSONAL SPENDING HABITS Impact of personal spending on society Can stimulate economy • Every £ 1 you spend on a product in a shop pays to allow that business to run. It allows the business to pay for utility bills, rent and wages. • These wages allow this person to have a quality of life, make spending decisions and spend in other businesses. • Businesses make profits, allowing the business to expand • This can create more jobs = reduced unemployment • Opportunities for further economic growth

THE COST OF OVERSPENDING Consequences of overspending on an individual • Overdraft interest / bank charges etc • Debt / increased borrowing (and therefore paying interest) • Loss of property E. g home/car if cannot pay back debts • Bankruptcy • Less disposable income/money spent • Less money saved • Poor credit rating = higher interest rates in the future

THE COST OF OVERSPENDING Consequences of personal overspending on an economy • People save less, so banks have less money to invest/make profit • People then spend less in the economy due to tighter finances • Less spending = less tax collected = decreased public services • Less spending = lower demand = increased unemployment • Banks can lend less money • This could lead to increased interest rates of borrowing such as mortgage rates increasing

PERSONAL BUDGETS- SPENDING CHOICES Budgeting involves making basic calculations to help you decide on your spending choices. When budgeting, you ask yourself; • Can I afford this now or do I need to save first? • What are my options to pay for something I need now if I don’t have the money right now? Loan? Long term/short term/pay day? Store credit (buy now pay later)? Credit card?

HOW TO WORK OUT A BUDGET Key terms we need to know • Net income – the amount of income received after tax and other deductions are taken off • Regular expenditure – what we spend each month on a regular basis • Net disposable income – what is left after taking away regular expenditure from net income, i. e. what is left after the bills are paid!

Net income – the amount of income received after tax and other deductions are taken off

Regular expenditure – what we spend each month on a regular basis

Net disposable income – what is left after taking away regular expenditure from net income, i. e. what is left after the bills are paid! This leads you to one of three outcomes A balanced budget – when income and expenditure are equal A budget surplus – when income is more than expenditure A budget deficit – when expenditure is more than income

• Mandatory expenditure – bills that must be paid by law (council tax, tv license, car insurance, road tax) • Essential expenditure – bills essential to a family’s way of life (rent, mortgage payments, essential clothes, insurance, utility bills) • Discretionary expenditure – things we might like to buy if we have the money but aren’t essential (CDs, meals out, books, hobbies)

CASH FLOW FORECASTING Cash flow is simply money in and money out of an account. This can apply to individuals, budgets or any business. This looks at not only how much comes in and goes out… but whether you will have the cash coming in before your cash goes out (otherwise you can’t pay it…)

WHAT TO DO IF… • A balanced budget – when income and expenditure are equal • A budget surplus – when income is more than expenditure • A budget deficit – when expenditure is more than income A balanced budget is better than a deficit budget. However, it means you are spending exactly what you have coming in. This could potentially cause you financial planning problems in the future. Give an example of a factor which may turn a balanced budget into a deficit budget?

• What are some negative consequences of being in a deficit for the individual AND the economy?

I’M IN A DEFICIT…HELP! If you find that you have a budget deficit, what could you do in order to try and reduce your REGULAR monthly outgoings? E. g bills, mortgage, petrol costs etc What about your non regular expenditure E. g going out for dinner, buying clothes Write down some ways in which you could try and reduce your expenditure

BUDGETING- THINGS TO CONSIDER 1. Are you getting “value for money” (Paying a fair price for a product) Branded clothing suppliers charge high prices because of a logo and there is often no real difference between their quality and that of cheaper substitutes. Can you swap? In other instances, low cost brands are low cost for a reason – they’re made of low quality materials and suffer from poor quality control

PRICE COMPARISON WEBSITES 2. You can use price comparison websites to search for cheaper prices or deals from other providers. • You can do this for regular expenditure such as gas and electric bills • You can also compare the prices of items online

AVOID HIDDEN CHARGES Hidden charges mean that the total price may not be as it originally seems to be. This can also be the case where there are “special offers” • Online shopping / teleshopping additional charges: • postage and packing; • booking fees; • service charges • When purchasing products online or through the telephone (Distance Selling) you are protected by Distance Selling Regulations, which state: • Seller must publicise delivery arrangements and cancellation rights • Goods much arrive within the time frame agreed • Buyer has the right to cancel the order at any time • If goods are faulty or don’t match the given description • If goods are returned, the seller must refund the delivery costs

REDUCE UNNECESSARY SPENDING 4. Is your net expenditure at a sustainable level? Are there areas you can cut back on? • Buying new clothes/luxury items • Reducing standard of living • Smoking habit is extremely expensive! • Holidays • Fuel consumption- could you walk/cycle to work? Are you leaving the heating on when out?

I’M IN A SURPLUS! If you have a surplus every month, you could choose to do a number of things with this money: • Put money into a savings account to earn interest • Invest money in bonds/stocks and shares • Invest in something which you think may increase in price E. g a house • Increase standard of living

Main saving options • Deposit accounts / savings accounts • Subject to two financial regulators – the Prudential Regulation • Authority (PRA) and the Financial Conduct Authority (FCA) Put your money in, collect the interest • Annual Equivalent Rate (AER) • Some rates of interest assume that interest is paid once, at the end of the year. Some accounts pay more often that, such as monthly or quarterly. Compounding means that if you get paid interest of 5 p on your balance one month, your next month’s interest will also pay interest on that 5 p as it is added to your balance.

WHERE DO I FIND THE INFORMATION TO BUDGET? Actively monitoring your finances is important in budgeting, making spending choices and remaining financially secure. You will have a range of document which will help you do this: • Bank statements • Bills • Checking balance regularly • Online/telephone/mobile banking • Tracking expenditure (mandatory, essential and discretionary) • Cash flow forecasts • Tracking savings

USING TOOLS TO MANAGE MONEY In order to manage their money, people need to have up-to-date and relevant information in their accounts, and ways to carry out a range of transactions. Paper/electronic statements Arrive through the post or email and can be used to monitor spending and create a cash flow forecast. They list transactions both in and out of an account in date order.

TOOLS TO MANAGE MONEY Internet and telephone banking including statements to mobiles • This allows you to check balances to assist budgets and to transfer money to other accounts • Branch / face-to-face banking • Allows you to withdraw, deposit and transfer money, as well as manage direct debits to ensure bills are paid on time

USING TOOLS TO MANAGE MONEY Tools for transferring money from one account to another • Debit cards – used to access money from an ATM or in a Chip and Pin machine • Contactless payments - can be used to pay for payments of up to £ 30 instantly, without having to enter a PIN (Personal Identification Number) • Cheques • Mobile apps • Benefits of use: quick; easily accessible; easily monitored

TOOLS FOR MANAGING MONEY • Direct debit – setting up a regular monthly payment by filling in a form and authorising the bank to make the transaction for you automatically • Standing order – similar to a direct debit, but the amount is fixed. This proves unhelpful when the bill amount is likely to change (such as electricity bills which may vary depending on usage) • Pay. Pal – a website allowing you to use a range of bank account cards to make a transaction between you and another user Did you know? Pay. Pal once accidentally made a US citizen the richest man in the world by crediting his Pay. Pal account with $92, 233, 720, 368, 547, 800… which is close to £ 60 quadrillion.

THE BUDGET – OVERALL ECONOMY “The budget” • In November 2018 Phillip Hammond (The Chancellor of the Exchequer) presented the budget for the whole of the Great British economy. • It looks at the income of the UK’s government and the spending decisions that must be made. • This could be reducing spending on certain public services or changing taxes.

WHAT AFFECTS THE BUDGET? • Interest rates • Fluctuation in savings and repayments • • As interest rates increase you may need to pay more back in loan repayments, affecting your expenditure Alternatively you may receive more interest on any savings, which could lead to meeting a financial objective quicker • Adjust budget accordingly • Be aware of changes in the interest rates that affect you • Inflation rates • If prices rise by 5%, how much does your income need to rise by in order to maintain your quality of life? • Foreign exchange • Fluctuation in costs of holidays when the GB Pound increases in value or • decreases in value Adjust budget accordingly

THE PERSONAL LIFE CYCLE Powerpoint • The stages of the personal life cycle • Comprises the stages through which we pass • No matter what is happening with the economy, the biggest impact on your finances will be the stage of life that you are at. • Events in each stage differ for every person • Likely types of income and expenditure for each stage Birth infanthood childhood teenager young adult mature adult middle age old age/retirement

THE PERSONAL LIFE CYCLE Income will change at different stages of the life cycle, for a number of reasons. What does this graph show about the effect of your job on salary earned?

• In a non-professional career, such as a waiter, the hourly rate earned will likely not change drastically over a number of years unless you earn a promotion • On the other hand, in a professional career (doctor, teacher, accountant, lawyer) the salaries start off higher and increase over time. People usually study for a number of years to qualify in this profession. On average, people who graduate from University in the UK earn an extra £ 200, 000 over their career compared with those who don’t have a degree level qualification.

THE PERSONAL LIFE CYCLE How do attitudes about risk and responsibility change as you go through the personal life cycle? • Physical risks; emotional risks; financial risks • Certain events more likely to happen at certain life stages • People are more likely to get married and buy houses at certain points • People are also living longer, therefore money has to last longer

DIFFERENT PLANS FOR DIFFERENT PEOPLE Where can we get advice to help our planning? • Advisory services • Citizens Advice Bureaux, a registered charity that assists in legal and financial issues • Money Advice Service, an independent body set up by government to give advice on financial affairs • Paid-for advice from financial advisors • Peers and family • Financial service providers • Banks • Building societies

DIFFERENT PLANS FOR DIFFERENT PEOPLE • What personal factors influence the plans we make? For each of the age categories annotate how their circumstances may differ. Think about; - Where their incomes from and amount What their expenditures may be What factors may be causing them to spend more money at different stages What their priorities might be Birth infanthood childhood teenager young adult mature adult middle age old age/retirement

ATTITUDE TO RISK • People have different attitudes towards risk. This is especially important when thinking about saving or investing. You must consider risk v reward. • The theory is simple, the higher you risk, the higher the potential reward. However, the higher the risk, the more likely you are to lose your investment.

ECONOMIC CYCLES AND DEMOGRAPHICS As with changes in your personal life cycle, the economy changes over time as well. • Changes in the economy over time can be unforeseen and therefore difficult to plan for. These movements in the economy are called economic cycles. • Predicting these movements is difficult – but easier in the short term than long term. This makes planning for financial decisions more difficult. If you take out a loan and can afford the interest, half way through repayments your interest rate could rise, which might make it difficult or impossible for you to meet loan payments. What could you do to make sure you are equipped to cope with this?

ECONOMIC CYCLES AND DEMOGRAPHICS This economic cycle shows how an economy goes through ups and downs over time. This cycle tends to follow an upward trend in the long term, as our society becomes bigger and more advanced, but in the short term has more dips.

. This is the")

ECONOMIC CYCLES AND DEMOGRAPHICS This graph measures GDP (gross domestic product). This is the value of total national income in an economy. It measures the value of all goods and services produced by the UK’s economy. Every haircut, every loaf of bread, every car.

ECONOMIC CYCLES AND DEMOGRAPHICS • Economic cycles • The Government want their economy to grow at a stable rate. When this doesn’t happen, and instead the amount we produce falls, we can have a recession (such as 2008/2009). • Government also has two other aims: • • That prices rise at a stable rate (i. e. not too much more than people’s incomes) That unemployment levels are low (more people working = more tax and less benefits to pay) • The short term and long term effects of economic cycles • Easier short-term planning as the economy won’t change drastically over a short period of time (i. e. months) • Can impact negatively on long-term planning: e. g. when taking out a mortgage, long-term economic cycles (e. g. increases in interest rates) are not always planned for and can result in financial difficulty in later stages of life cycle

ECONOMIC CYCLES AND DEMOGRAPHICS The impact of demographic changes on personal finance Demography is the study of a population and its different groups by: • Age • Ethnicity • Gender • Family type • Income bracket What is the current make up of the UK population?

ECONOMIC CYCLES AND DEMOGRAPHICS The three biggest demographic impacts • Geographic distribution (where people live) The majority of the UK live in cities • Patterns of migration Internal migration (people moving to cities from rural areas or urbanisation) International migration (people moving to the UK from other countries) • Ageing population More older people proportionately

AN AGING POPULATION

SUMMARY Personal finance is how you use your money – ie what you earn, and how you decide to spend and save it. This is known as ‘money management’. Good money management entails many things. It means borrowing to buy items that will help us to reduce our living costs (such as a washing machine so that we don't have to buy new clothes all the time) and / or which are likely to increase in value (such as our own home), and being able to repay our debts on time. Poor financial choices are the opposite of these. Poor financial choices involve high risk and instability, leaving people without the means to survive when they run into difficulties, and with little or no security in old age. This, in turn, affects the economy as a whole, because these people will need help from the benefits system.

SUMMARY 2 • How individuals manage their money is closely connected to the economic system as a whole. • Both good and poor personal financial choices have particular effects on the economy and society. • ✔ The main effects of good financial choices are: ■ less ‘bad debt’ in the economy; ■ less borrowing overall; and ■ increased spending and increased saving, because when people borrow less, they repay less from their earnings.

THE REAL COST OF SPENDING • The true cost of spending • Government tax levied on goods and services: buyer pays seller’s price plus tax • VAT • Value Added Tax is a tax charged on most goods and services that VAT-register businesses provide in the UK • • • standard rate; 20% reduced rate; 5% and applied to certain goods and services, including gas and electricity suppliers, children’s car seats etc zero rate; no VAT charged, such as foods, books, and newspapers, children’s clothing and shoes, and fares on public transport

THE REAL COST OF SPENDING • VAT example:

- Slides: 81