Bonds and Related Issues kicheon changyahoo co kr

Bonds and Related Issues kicheon. chang@yahoo. co. kr 1

Contents Topics Contents Numerical Method 보간법 행렬연산 Simulation Solver/Optimization Bond Price/Duration/Convexity Immunization Finding YTM Term structure 이론 Bootstrapping Fitting the yield curve Bond Futures 채권선도(FRA) 국고채선물 이론가 계산 2

Preface • “Theory Excel VBA” Type – Memorize it in your hand rather than in your head!! • Engineering Approach – 수학적 엄밀성보다는 직관적 이해 – (ex) • A bird in the hand is worth two in the bush – Do not hesitate to raise your hand whenever questionable – Use the break time, e-mail etc. . • Two way vs One way 3

Numerical Methods 4

Numerical Method & Finance 5

(Polynomial, Spline) Interpolation, Finite Difference")

Numerical Method/Simultaneous equations • Why simultaneous equations? – (ex) (Polynomial, Spline) Interpolation, Finite Difference Method, Bootstrapping… • How to do? 6

Numerical Method/Cholesky Decomposition • Why? – We know – What is • How? • Where(application)? – Generating correlated random variables 7

Numerical Method/Linear Interpolation Linear interpolation Log interpolation Exponential interpolation 8

note 9

Numerical Method/ Polynomial interpolation N+1 equations N+1 unknowns 10

Numerical Method/Polynomial Interpolation Example 11

Base function(1) Lagrange polynomial interpolation 12")

Numerical Method/ Polynomial interpolation Base function(0) Base function(1) Lagrange polynomial interpolation 12

Numerical Method/ Polynomial interpolation Lagrange polynomial interpolation 13

Numerical Method/Polynomial interpolation the problem 14

Numerical Method/Spline interpolation 15

Numerical Method/spline interpolation 2차 스플라인 보간법 3차 스플라인 보간법 16

Numerical Method/2 D interpolation 17

Numerical Method/Optimization: Solver 18

Numerical Method/Bisection method 19

Numerical Method/Newton method Algorithm 20

Caution! • There is no panacea! – Try possible Initial values – 함수의 전반적 형태파악 • 단조증가/감소함소 21

Numerical Method/Simulation/ Uniform Random Variable RND 22

Numerical Method/Simulation/Uniform RV Examples Calculating PI 23

Numerical Method/Simulation/ Transforming RV • 12 난수법 – – Definition: Why 12 RVs? Central Limit Theorem: Does CLT really work? FREQUENCY(samples, 구간) 24

, Norm.")

Numerical Method/Simulation/ Transforming RV • Transform method – Idea – Functions: Norm. SDist(x), Norm. SInv(p) – test Transform 25

Multi-variable case • From uncorrelated RVs to correlated RVs 26

Bonds 27

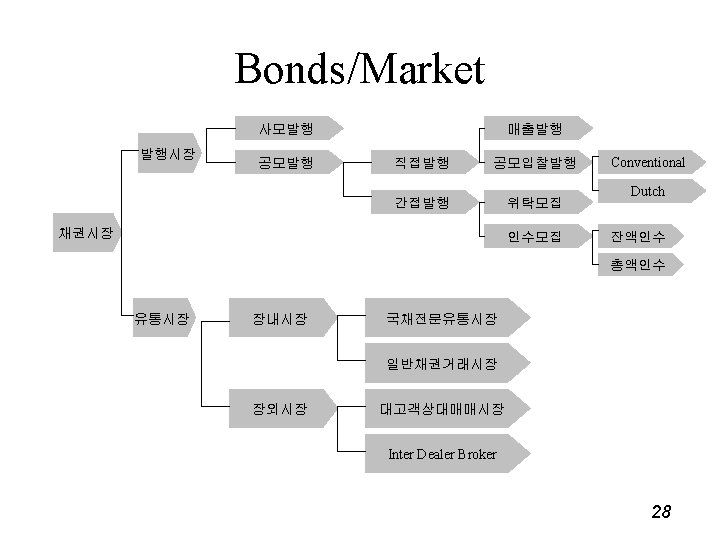

Bonds/Market 자료: www. ksdabond. or. kr 29

Bonds/Market 자료: www. ksdabond. or. kr 30

Bond/price 31

Bond/Price Example 32

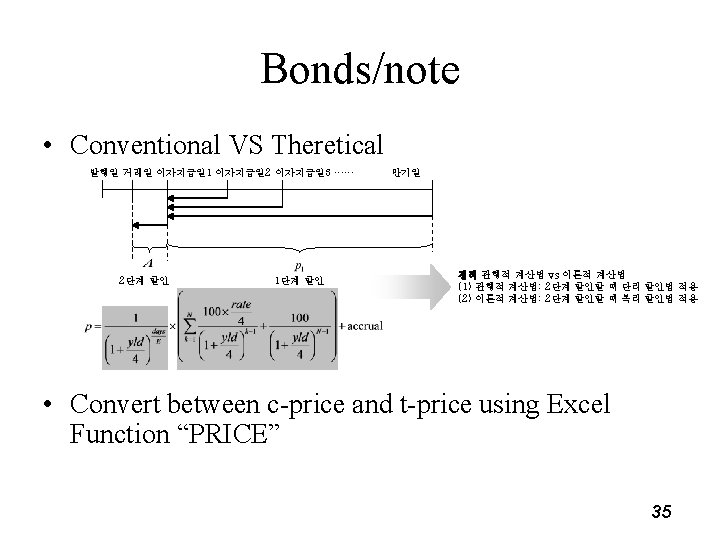

Bonds/Terminology • Conventional price • Theoretical price • Dirty price – Cash price – Invoice price • Clean price – Quoted price 34

Bonds/Day count convention 36

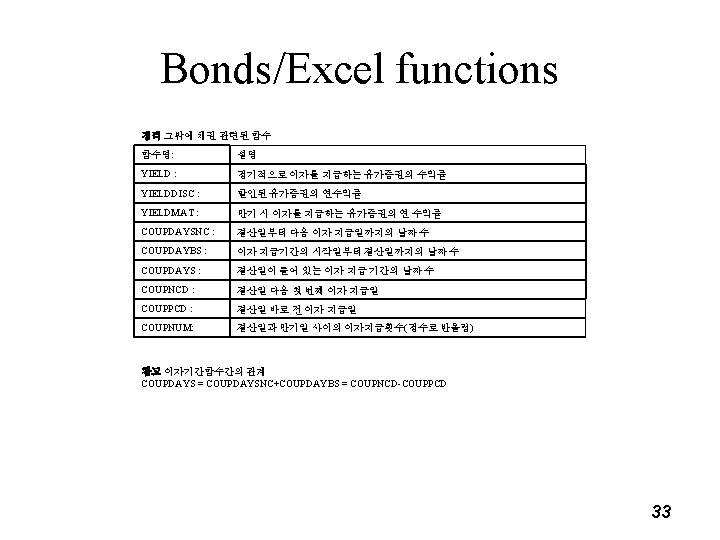

Bonds/User Defined Function Test Numbers 37

Bonds/Duration • History of bond sensitivity – Maturity – CF Weighted Average Term to Maturity – PV Weighted Average Term to Maturity • Meaning of Macauley Duration – Investment Horizon → Immunization – Sensitivity → Modified Duration 38

Bonds/Modified Duration • What we want to know is… – What if the yield moves up 1%p? • Mac. Duration does not give the answer • Modified Duration 39

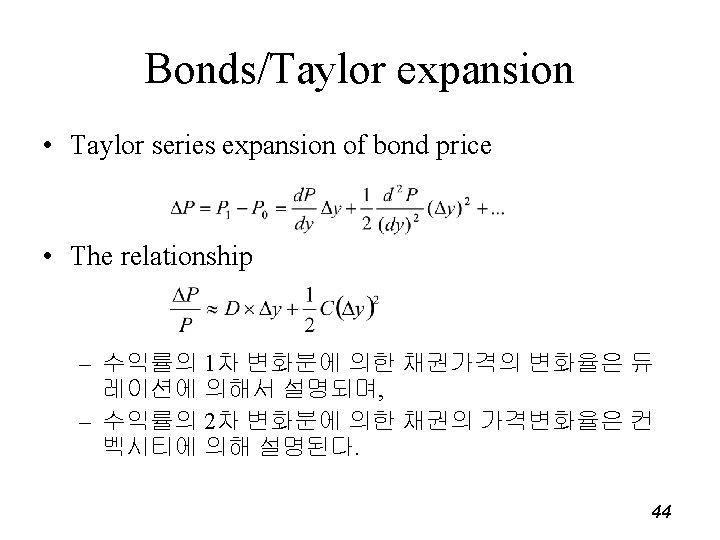

Bonds/Convexity • If we hedged the bond’s duration, then what happens to the value of our portfolio when yield moves? • Convexity – 듀레이션 헤지된 포트폴리오의 손익변화 측정에 사용 – See the Taylor Expansion 40

Bonds/Numerical Convexity Difference approximation 41

42")

note (Excel 2007에서는 위 설정없이 “Application. price”로 사용가능) 42

any function to “polynomial functions” • How")

Bonds/Taylor Expansion • We want to decompose(analyse) any function to “polynomial functions” • How to find the coefficients – Above equation should hold when x=0 – Differentiating and inputting x=0 still hold equality – and so on 43

Bonds/Summary 45

Bonds/Summary 46

Bonds/Immunization Request Alternatives 47

Bond/Immunization Example Scenario Analysis Check “Macauley duration” 48

• Why numerical method? • Bisection Method 49")

Bond/Finding YTM(1) • Why numerical method? • Bisection Method 49

Bond/Finding YTM VBA code 50

yield 51")

Bond/Finding YTM(2) yield 51

Term structure of Interest rates 52

TS/Terminology • Zero rate – Definition: • Par yield – Definition: such that • Forward rate(Implied forward rate, Forward rate agreement) – see FRA for pricing – Relationship between spot rate and forward rate • Discount factor – _ 53

Term structure of interest rates 54

")

Term structure of interest rates • Which one? (in terms of modeling yield curve) – Yield of zero coupon bond is not enough – Zero price • Cubic functions – Forward rate • Nelson-Seigel function 55

Term Structure of Interest rates 56

TS/Why yields differ? 57

TS/Issues • Finding the current term structure of interest rates – Fitting Yield Curve – To price illiquid bonds • Estimating the future term structure of interest rates – Economics/Econometrics – To trade bonds • Modeling the future term structure of interest rates – Finance – To price Fixed Income Derivatives 58

Finding Yield Curve • Bootstrapping and Interpolation – 다양한 만기의 이자율 상품의 가격이 고시되는 경우 – Interest Rate Swap Market • Functional Approach – Function types • Cubic function • Piece-wise cubic function • Nelson-Seigel function 59

TS/Bootstrapping 60

TS/Bootstrapping Example 행렬을 이용하는 방법 61

TS/Bootstrapping More considerations Available prices Bootstrapping formula 62

TS/Bootstrapping/more consideration Example 63

TS/Bootstrapping/more consideration Example 64

TS/Bootstrapping/summary 65

TS/Fitting the yield curve 66

TS/Functional Forms 67

Polynomial Model/Cubic Function • Yield curve function – Model: – No Arbitrage condition • Bond price • Find coefficients 68

Polynomial Model/Cubic Function/ Data 자료: Bloomberg 69

Polynomial Model/Cubic Function Example Function cubic. F(t, b 0, b 1, b 2, b 3) cubic. F = b 0 + b 1 * t + b 2 * t ^ 2 + b 3 * t ^ 3 End Function 70

Spline: Piece-wise polynomial • More freedom More accurate one Zero price • Bond price T • Continuity Condition+1 st & 2 nd differential condition • Find coefficients 71

Polynomial Model/Nelson-Siegel Instantaneous forward rate discount factor 72

note 73

Polynomial Model/Nelson-Seigel Example 74

Dim A As Double,")

Polynomial Model/Nelson-Seigel Example Function df_Nelson. Seigel(a_, b_, c_, alpha, t) Dim A As Double, B As Double, C As Double A = AA(b_, c_, alpha) B = BB(a_) C = CC(c_, alpha) df_Nelson. Seigel = Exp(-A - B * t - (A + C * t) * Exp(-alpha * t)) End Function AA(b_, c_, alpha) AA = b_ / alpha + c_ / (alpha * alpha) End Function BB(a_) BB = a_ End Function CC(c_, alpha) CC = c_ / alpha End Function 75

Graphs: polynomial vs Nelson-Seigel 76

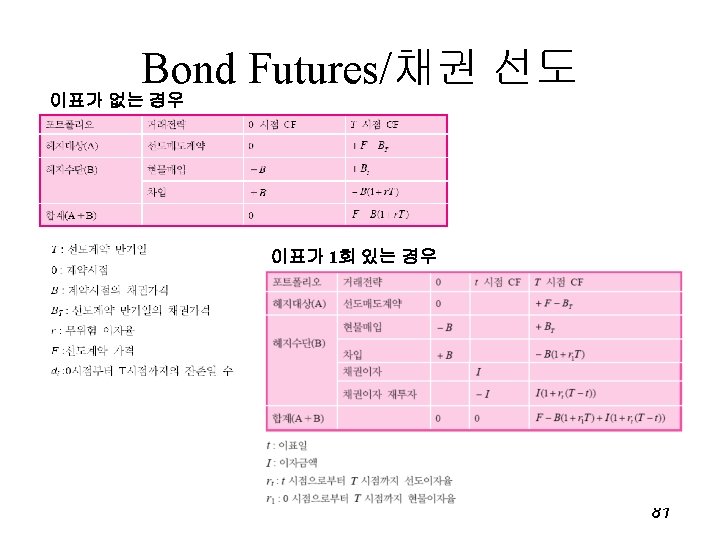

Bond Futures/Forward 77

Bond Futures/주식선도 78

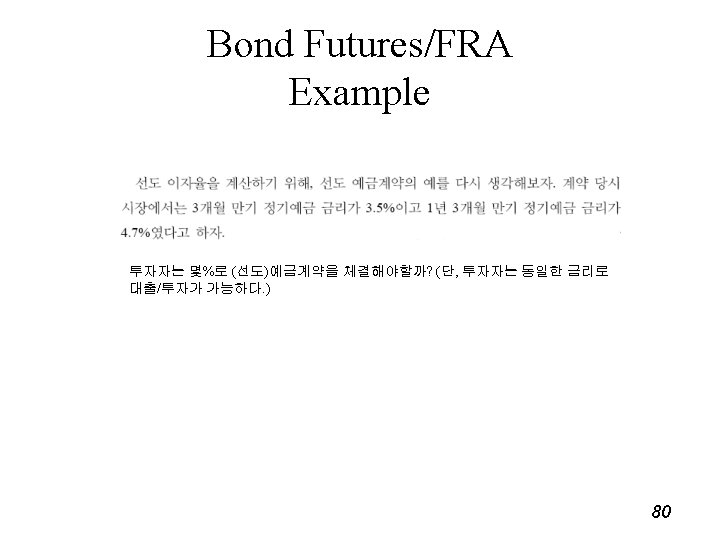

79")

Bond Futures/이자율 선도(FRA) 79

Bond Futures/UDF 82

KTB Futures/Market 83

KTB Futures Check 84

KTB Futures/Market 85

KTB Futures/이론가 계산 87

KTB Futures/functions 88

KTB Futures/functions 89

KTB Futures Example 90

Note: Excel functions DSC=coupdaysnc 기준일부터 다음 이자지급일까지의 날수 E=coupdays A=coupdaybs N=coupnum 91

bonus • Convexity adjustment 92

Thank you! 94

- Slides: 94