B ASIC B OOKKEEPING B ASIC B OOKKEEPING

B ASIC B OOKKEEPING

B ASIC B OOKKEEPING Starting up a small business? Working as an office administrator? Bookkeeping responsibilities can be overwhelming! In this course we will teach you the basics of bookkeeping. Learn what your accounting responsibilities are, basic accounting terminology, the basics of financial statements and how to prepare your files for year end

B USINESS O RGANIZATION T YPES Proprietorship Partnership Corporation

T HE F ISCAL Y EAR A Fiscal Year is an accounting time period that is one year long Fiscal year ends may vary from the calendar year Corporate Tax returns are due 6 months after the corporations fiscal year end

A CCOUNT TYPES Accounts track all of your accounting transactions and allow you to categorize your transactions There are standard account types which are the main categories that all businesses follow Assets, Liabilities, Equity, Revenue, Expense

– include bank accounts, petty")

A CCOUNT TYPES o Asset Accounts (What you own) – include bank accounts, petty cash, equipment, buildings and land o Can be liquidated for cash o Are generally valued over $500. 00 and usable for more than one year o The balances in asset accounts carry forward from year to year until the asset is liquidated o For tangible assets the value of the asset is amortized or spread out over multiple years

– include loans, mortgages, lines of")

A CCOUNT TYPES Liability Accounts (What you owe) – include loans, mortgages, lines of credit, account’s with suppliers, payroll expenses payable, GST and taxes payable, and your accounts payable account Your accounts payable account tracks all of your outstanding bills; tracked by vendor name

– the difference between")

A CCOUNT TYPES o Equity Accounts (Value of the Business) – the difference between what a businesses owns and what it owes o Equity accounts include owner or shareholder’s contributions, draws, and retained earnings which are profits left in a business o At the end of each year the net profits (or losses) from a business are transferred into the retained earnings or owner’s equity account

– Revenue or Income is earned through business")

A CCOUNT TYPES Income Accounts (Revenue) – Revenue or Income is earned through business activities such as the sale of merchandise or services Some businesses earn all their revenue by selling products, others offer services, and many offer both products and services

– Expenses are")

A CCOUNT TYPES Expense Accounts (The Costs of Running a Business) – Expenses are tracked through 2 main categories; cost of goods sold and operating expenses The expense accounts will vary between businesses but often are very detailed so that a company can evaluate its profitability effectively

P RACTICE Let’s practice recognizing account types by completing the exercise in your handout on page 3

P RACTICE

P RACTICE

T HE C HART OF A CCOUNTS Because each company is different, the types of accounts they have and how many of each type of account they have are also different The Chart of Accounts lists the accounts for a specific business Accounts are often assigned numbers that identify where the accounts are in the ledger or list of accounts

T HE C HART OF A CCOUNTS General Accounting Principle’s state that the accounts be organized in the following manner to create consistency amongst businesses. This order is also useful when preparing financial statements. 1. Assets are listed First; when numbered, begin with the number 1 2. Liabilities are listed Second; when numbered, begin with the number 2 3. Equity Accounts are listed Third; when numbered, begin with the number 3 4. Revenue accounts are listed Fourth; when numbered, begin with the number 4 5. Expense accounts are listed last; when numbered, begin with the number 5 or greater

T HE C HART OF A CCOUNTS

W HAT ARE MY RESPONSIBILITIES AS A BOOKKEEPER Accounts Payables A/P Transactions record expenses for your company Bills and Cheques are the main ways company’s record expenses. Credit Card transactions are also popular Expenses are tracked by Vendors ?

W HAT ARE MY RESPONSIBILITIES AS A BOOKKEEPER ? Inventory is goods on hand which a company intends to sell or use for their services Inventory is a unique type of expense account as it is often referred to as Cost of Goods Sold which measures the direct cost of a company’s income

W HAT ARE MY RESPONSIBILITIES AS A BOOKKEEPER Accounts Receivables A/R Transactions record revenue or income for your company Invoices and Sales Receipts are the main ways company’s record revenue Income is often tracked by Customer ?

W HAT ARE MY RESPONSIBILITIES AS A BOOKKEEPER Payroll are expenses incurred by a company to hire staff Payroll expenses include wages paid to employees as well as payroll liabilities ?

T HE T RIAL B ALANCE A Trial Balance is a list of Accounts and their balances at a specific time In accounting some account types will have a debit balance and others will have a credit balance In the Trial Balance Report the total of all debits will equal the total of all credits

T HE T RIAL B ALANCE

D EBITS VS C REDITS Assets, Equity Drawings and Expense Accounts: Debit to Increase Credit to Decrease Liabilities, Equity Contributions and Income Accounts: Credit to Increase Debit to Decrease This is so that all journal entries are balanced equations.

G ENERAL J OURNAL E NTRIES Any accounting entry results in a Journal Entry Most entries in a computerized accounting environment will be completed automatically in the background of the program as the user will enter their information through forms When recording a complex accounting transaction a manual journal entry is completed When completing a manual journal entry you must remember that all debits must equal all credits

G ENERAL J OURNAL E NTRIES The following 5 steps will help you through drafting a manual journal entry: 1. Determine all of the Accounts within your Chart of Accounts that will be effected by the entry. 2. Next determine what type of accounts the identified accounts are. 3. Determine for each account used will the account receive a DEBIT or a CREDIT. 4. For each account determine the amount for the entry. 5. Finally, draft your General Journal Entry

G ENERAL J OURNAL E NTRIES This is a sample General Journal Entry. The sample entry records a loan payment.

G ENERAL J OURNAL E NTRIES PRACTICE DRAFTING A GENERAL JOURNAL ENTRY FOR THE FOLLOWING SCENARIO Scenario: Your company purchases a new company vehicle from your local car dealership. You issue the dealership a $10, 000 cheque for the down payment on the vehicle and the remainder of the cost is financed through Ford Credit as a vehicle loan. The cost of the vehicle is $60, 000. 00 plus $3, 000. 00 GST.

G ENERAL J OURNAL E NTRIES Step One: Determine all of the Accounts within your Chart of Accounts that will be effected by this purchase; there are 4 in this example. 1. Chequing Account 2. Ford Credit Loan Account 3. GST Paid 4. Fixed Asset – Company Vehicle

G ENERAL J OURNAL E NTRIES Step Two: Now you will need to think about what type of accounts these are. Account Type Chequing Account Asset (Bank) Ford Credit Loan Account Liability (Loan) GST Paid Liability (GST Owing) Fixed Asset – Company Vehicle Asset (Fixed Asset)

G ENERAL J OURNAL E NTRIES Step Three: Next determine for each account used will the account receive a DEBIT or a CREDIT. Account Debit or Credit Chequing Account Credit Ford Credit Loan Account Credit GST Paid Debit Fixed Asset – Company Vehicle Debit

G ENERAL J OURNAL E NTRIES Step Four: Now for each account determine the amount for the entry. Account Amount Chequing Account $10, 000. 00 Ford Credit Loan Account $53, 000. 00 GST Paid $3, 000. 00 Fixed Asset – Company Vehicle $60, 000. 00

G ENERAL J OURNAL E NTRIES Step Five: Finally, Draft your General Journal Entry Account Debit Credit Chequing Account $10, 000. 00 Ford Credit Loan Account $53, 000. 00 GST Paid $3, 000. 00 Company Vehicle $60, 000. 00

G ENERAL J OURNAL E NTRIES Here is a sample of what the previous General Journal Entry may look like in a computer software program such as Quick. Books.

R ECONCILING A CCOUNTS Reconciling Accounts Reconciliations should be prepared for all bank accounts and credit card accounts Account Reconciliations keep your accounting records accurate, complete and up to date Bank Reconciliations will help you identify: Outstanding Cheques and Deposits Errors to entries Bank Errors

R ECONCILING A CCOUNTS Steps to Reconciling Accounts 1. You will need your bank or credit card account statement 2. Enter your Opening and Closing Balances 3. Next you will go line by line, checking to ensure your accounting records from your bank or credit card accounts ledger match your statement 4. Adjust any incorrect entries 5. Enter any transactions that have not yet been entered 6. When your records match your bank statement - your account has been reconciled

G OODS AND S ERVICES T AX - GST Goods and Services Tax GST is a type of tax charged by businesses that register for a GST number and meet the eligibility requirements by Revenue Canada for a GST Account See Revenue Canada’s Website www. ccra. gc. ca for information on whether your business qualifies for a GST Account or not

G OODS AND S ERVICES T AX - GST Goods and Services Tax Assuming your company has a GST Account here are your responsibilities: You must charge your customers and report GST on all taxable products and services You must record and report all GST your company pays on eligible expenses You must prepare and file your GST report and remittance either quarterly or annually, a personalized GST 34 form will be mailed to you by the CRA GST Remittance amounts that are due must be paid within 30 days of the filing period end date to avoid penalties and interest charges

M ANUAL B OOKKEEPING O PTIONS Manual Bookkeeping Options Although most businesses utilize accounting programs such as Quick. Books®, Simply Accounting®, Ag. Pro®, and Acc. Pac® to name a few often small businesses begin by utilizing a manual bookkeeping system Manual bookkeeping is the paper-based and traditional way of bookkeeping. Business transactions are recorded manually by hand using manual or paper book of accounts, such as journals books, ledger books and worksheets

M ANUAL B OOKKEEPING O PTIONS Manual Bookkeeping Options Many opt for manual bookkeeping because it is cheaper and easier to maintain Double Entry Accounting is a term often references when referring to manual bookkeeping Double Entry Accounting introduces the concept of debits and credits, which means that for every transaction there is something received (debit) and given up (credit), as such, each recorded transaction affects two or more accounts

M ANUAL B OOKKEEPING O PTIONS Below is a sample ledger that could be set up in a notebook or as a spreadsheet.

M ANUAL B OOKKEEPING O PTIONS Here are points to consider when setting up a manual ledger or bookkeeping system: 1. Most businesses have a separate spreadsheet for each month 2. Income transactions are entered as a positive amount and Expense transactions are often entered as a negative amount 3. By subtotalling each column you can check your work and ensure that you balance

M ANUAL B OOKKEEPING O PTIONS Here are points to consider when setting up a manual ledger or bookkeeping system: Separating the GST collected column from the GST paid column makes preparing and filing a GST return simple Remember to only record the Subtotal amount under the income and expense columns You can have as many income and expense columns as you need however often its best to keep it as simple as possible. Columns should not be created for vendors or customers only general expense or income types

P RACTICE Complete the exercise on page 12 of your handout by entering in the ledger below each of the following transactions. As a final task prepare a GST Filing for May 2013. Date Transaction Description Amount GST Subtotal May 4, 2013 Staples Purchase of pens, paper & ink 214. 00 10. 20 203. 80 May 6, 2013 Weekly store sales are recorded 1575. 00 1500. 00 May 8, 2013 Insurance is paid to AMA Insurance 430. 00 May 9, 2013 Lightbulbs are purchased at Wal. Mart 5. 25 0. 25 5. 00 May 10, 2013 Consulting Work for a client complete 315. 00 300. 00 May 12, 2013 Accounting Fees are due 525. 00 500. 00 May 13, 2013 Weekly store sales are recorded 2730. 00 130. 00 2600. 00 Line 101 Sales Line 103/105 GST Collected

P RACTICE Month of May Date Description GST Total Income GST Collected GST Paid Subtotal 4 Staples -214. 00 6 Weekly sales 1575. 00 8 Insurance -430. 00 -5. 25 -0. 25 -5. 00 9 Walmart 10 Consulting Sales 315. 00 12 Accounting -525. 00 13 Weekly sales 2730. 00 TOTALS 3445. 75 -10. 20 75. 00 Consulting Office Professional Repairs & Retail Sales Services Insurance Supplies Fees Maintenance -203. 80 1500. 00 15. 00 300. 00 -25. 00 130. 00 Expenses 430. 00 5. 00 300. 00 -500. 00 2600. 00 220. 00 -35. 45 3261. 20 4100. 00 300. 00 430. 00 203. 80 500. 00 5. 00

P RACTICE Prepare the GST filing for May 2013 Line 101 Sales $4400. 00 Line 103/105 GST Collected $220. 00 Line 106/108 GST Paid (ITC’s) Line 109 Net Tax $35. 45 $184. 55

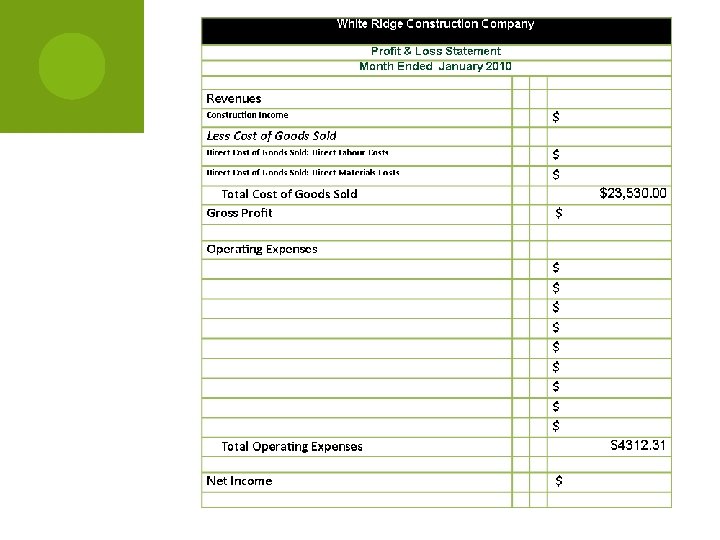

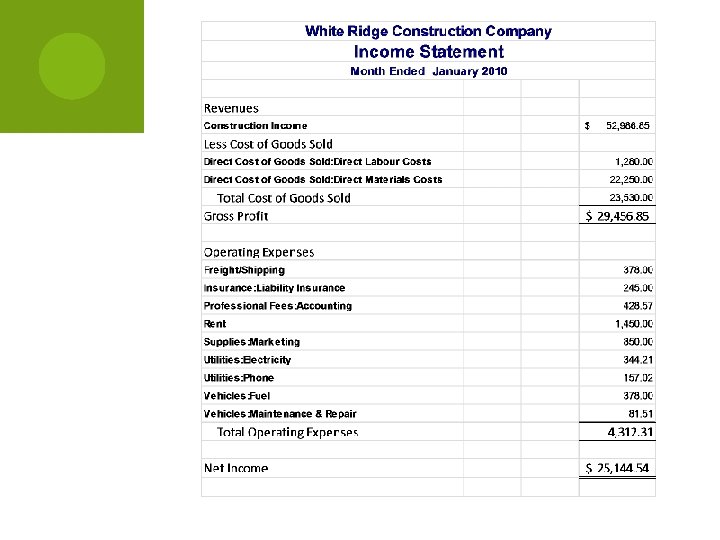

U NDERSTANDING B ASIC F INANCIAL S TATEMENTS Income Statement or Profit and Loss Statement presents the revenues and expenses, and the resulting net income or net loss for a specific period of time Revenue and Expense accounts are accounted for within a company’s fiscal year and the balances of these accounts are not brought over to future years If you were to look at a Trial Balance Report you would use all Revenue and Expense accounts and their corresponding values to generate an Income Statement or Profit and Loss Statement

U NDERSTANDING B ASIC F INANCIAL S TATEMENTS

U NDERSTANDING B ASIC F INANCIAL S TATEMENTS

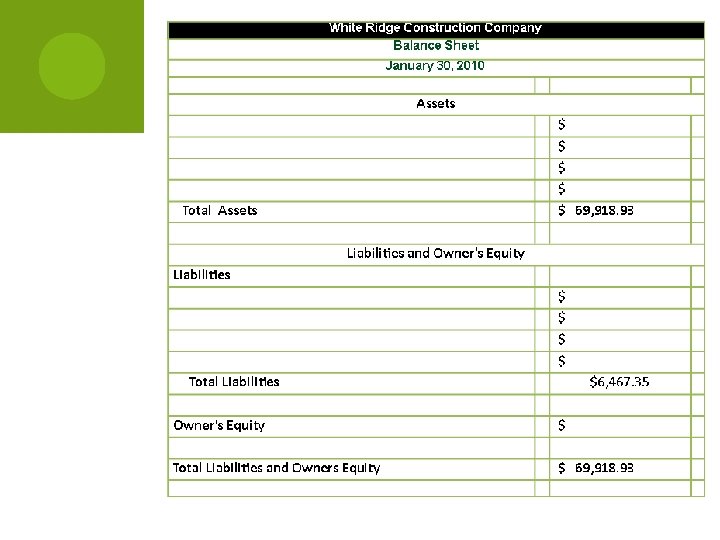

U NDERSTANDING B ASIC F INANCIAL S TATEMENTS Balance Sheet A Balance Sheet reports the assets, liabilities, and owner’s equity at a specific date After a company’s yearend is completed all Revenue, Expense and Drawings accounts are cleared as the Owner’s Equity Account is updated A Balance Sheet report summarizes the company’s activity from year to year. The report calculates how much your business is worth (your business's equity) by subtracting all the money your company owes (liabilities) from everything it owns (assets) If you were to look at a Trial Balance Report you would use all Asset, Liability and Equity accounts and their corresponding values to generate a Balance Sheet

U NDERSTANDING B ASIC F INANCIAL S TATEMENTS

U NDERSTANDING B ASIC F INANCIAL S TATEMENTS

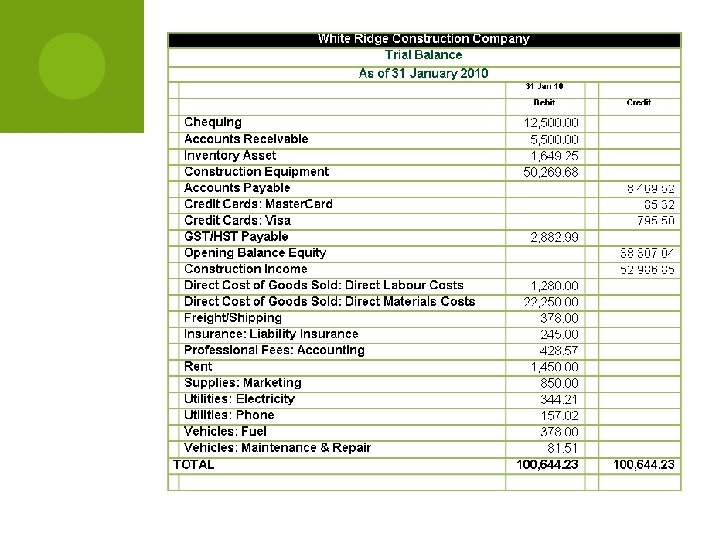

U NDERSTANDING B ASIC F INANCIAL S TATEMENTS PRACTICE PREPARING BASIC FINANCIAL STATEMENTS Using the Trial Balance Report from the sample company: White Ridge Construction Company ; fill in the blanks for the Profit and Loss Statement and the Balance Sheet

pg 13")

25, 144. 54 Opening balance equity Net Income (from P & L) pg 13

Y EAR E ND Preparing your Files for Year End -Whether your accounting files are going to an auditor, tax prepare or accountant here are the documents that you should have in order to prepare for year end.

Y EAR E ND Year End Checklist ¨ Accounts Receivables Listing ¨ Accounts Payables Listing ¨ New Asset Files ¨ New Loans Files ¨ Bank Reconciliations ¨ Revenue and Expense Files ¨ Chart of Accounts ¨ Sales Tax Files ¨ Payroll T 4 and Remittance Files ¨ Year End Trial Balances from Previous Year and End of Current Year ¨ Backup Copy of your computerized Accounting File or Your Manual Ledger/Spreadsheet

R EVIEW Use your Glossary on page 19 of your handout to review the accounting terms you have learned GLOSSARY Accounts Payables a record that shows how much a company owes suppliers for the purchase of goods or services on credit Accounts Receivables a record that shows how much is owed to a company by customers who have purchased goods or services on credit Assets The property that is owned by an organization. The items on a balance sheet that constitute the total value of an organization Balance Sheet a statement showing the assets and liabilities of a company or institution at a particular time Bookkeeping the activity or profession of recording the money received and spent by a person, business, or organization Chart of Accounts a chart explaining the numerical codes identifying the ledger accounts in an accounting system Corporation A company recognized by law as a single body with its own powers and liabilities, separate from those of the individual members. Cost of Goods Sold the cost of materials and labour required to build a product or offer a service Customer a person or company that buys goods or services Double Entry Bookkeeping Double Entry Accounting introduces the concept of debits and credits, which means that for every transaction there is something received (debit) and given up (credit), as such, each recorded transaction affects two or more accounts. Equity the value of a piece of property over and above any mortgage or other liabilities relating to it Expense the value of a resource that has been used during the current accounting period and can be charged against revenues for that period Fiscal Year a 12 -month period at the end of which all accounts are completed in order to provide a statement of a company's, organization's, or government's financial condition, or for tax purposes. A fiscal year does Financial Statement A financial statement (or financial report) is a formal record of the financial activities of a business, person, or other entity Generally Accepted Accounting Principles (GAAP) is a term used to refer to the standard framework of guidelines for financial accounting used in any given jurisdiction; generally known as Accounting Standards. GAAP includes the standards, conventions, and rules accountants follow in recording and summarizing transactions, and in the preparation of financial statements Income the amount of money received over a period of time either as payment for work, goods, or services, or as profit on capital Income Statements (Profit & Loss Reports) a financial statement showing the profit or loss sustained by a company during a particular period, including all items of income and expenditure Inventory the merchandise or stock that a store or company has on hand Liabilities all debts and other financial obligations that appear on a balance sheet Partnership the relationship between two or more people or organizations that are involved in the same business activity Payroll the total sum of money to be paid to employees at a given time Proprietorship the owner of a commercial enterprise or establishment such as a store, hotel, or restaurant Revenue money that comes into a business from the sale of goods or services Trial Balance a statement used to check that the debits and credits in a double-entry bookkeeping ledger are equal Vendor somebody who sells something

E XTRA P RACTICE Prepare a Profit & Loss Statement for April, 2013 using the manual bookkeeping example on page 11 Month of April 2013 Date Description GST Total Income GST Collected GST Paid Subtotal 1 Weekly Sales 1575. 00 1 Building Rent -630. 00 -600. 00 3 Bank Fees -12. 50 0. 00 -12. 50 7 Weekly News -93. 45 -4. 45 -89. 00 8 Rona Hardware -17. 64 -0. 84 -16. 80 Consulting 8 Income 8 Weekly Sales 12 Staples 75. 00 682. 50 32. 50 2016. 00 96. 00 -48. 30 15 Weekly Sales Store stock 1008. 00 -2. 30 -1775. 00 17 Legal Fees -525. 00 -500. 00 18 Canadian Tire -72. 45 -3. 45 -69. 00 22 Weekly Sales 2415. 00 115. 00 446. 25 21. 25 -840. 00 2730. 00 130. 00 6769. 66 517. 75 TOTALS Bank Fees Office Supplies Professional Fees Rent Repairs & Maintenance 600. 00 89. 00 16. 80 650. 00 -46. 00 960. 00 -88. 75 29 Weekly Sales Advertising 12. 50 650. 00 48. 00 27 Accounting Fees Inventory Purchased 1920. 00 -1863. 75 Consulting Services 1500. 00 16 purchased 23 Income Retail Sales Expenses 46. 00 960. 00 1775. 00 500. 00 69. 00 2300. 00 425. 00 -40. 00 425. 00 -800. 00 2600. 00 -194. 79 6446. 70 9280. 00 1075. 00 1775. 00 89. 00 12. 50 46. 00 1300. 00 600. 00 85. 80

E XTRA P RACTICE Profit & Loss Statement Month Ended April 2013 Revenues Retail Sales $ 9280. 00 Consulting Services $ 1075. 00 Total Revenue $ 10, 355. 00 Expenses COGS: Inventory Purchased $ 1775. 00 Advertising $ 89. 00 Bank Fees $ 12. 50 Office Supplies $ 46. 00 Professional Fees $ 1300. 00 Rent $ 600. 00 Repairs & Maintenance $ 85. 80 Total Expenses Net Income $ 3908. 30 $ 6446. 70

Thank You! C OURSE E VALUATION F ORMS A VAILABLEAT WWW. BUSINESSIQTRAINING. COM

- Slides: 63