AUDIT 4 2015 AUDIT EVIDENCE EVIDENCE Support for

1. Auditor’s personal knowledge")

• Representation letter -")

• Reconciliation of schedules")

: • Large accounts, expected errors, or items")

: – The combined assessed level of inherent")

- Slides: 74

AUDIT 4 - 2015

AUDIT EVIDENCE

EVIDENCE Support for audit opinion Is all the information the auditor uses to arrive at the conclusions on which the audit is based. To support auditor’s opinion Must be obtained to support: – Risk assessment procedures – Tests of controls – Substantive procedures – Other audit procedures

Types of Audit Evidence – Accounting records – books & records (analytical, recalculation, & reconciliation) – Corroborative evidence – checks, invoices, sales orders, PO, contracts, minutes, confirmations, observation, inquiry & inspection – gives validity to the accounting data – Evidence in electronic form – consider the time during which information exists

Sufficient Appropriate Audit Evidence Must persuade the auditor that the ending balances are fairly presented Reasonable assurance only Persuasive rather than conclusive The auditor must exercise professional judgment Cost-benefit alone is not a valid basis

Sufficiency of Evidential Matter The auditor’s decision regarding the sufficiency of the evidence is influenced by the following: – The risk of material misstatement – (greater risk = more evidence) – Quality – less audit evidence may be required when that evidence is of higher quality

Appropriateness of Audit Evidence Must be reliable and relevant. • Circumstances under which it is gathered • Source of the evidence • Nature of the evidence

Appropriateness of Audit Evidence • Auditor’s direct personal knowledge – provides persuasive evidence than evidence obtained indirectly (observation, recalculation, inspection) • External evidence – provides greater assurance than internally generated evidence. – Sent directly to the auditor (confirmations, legal letters, bank cut-off statements) – Received and held by the client (bank statements, contracts, invoices) • Internal evidence (purchase orders, sales orders, receiving reports) – internal controls • Oral evidence – least reliable form of evidence

Hierarchy of Audit Evidence (From most reliable to least reliable) 1. Auditor’s personal knowledge 2. External evidence 3. Internal evidence 4. Oral evidence

Evaluation of Audit Evidence – Evaluate management assertions – Detect material misstatements The evaluation of audit evidence must take into consideration the achievement of audit objectives

Substantive Procedures = $ balances Tests of details – to gather evidence to support the account balances as reflected in the F/S – Performed on ending balances – Performed on the details of transactions Analytical procedures – ratios, %, comparisons. The auditor looks for unusual relationships, discrepancies, or variances. – Planning – required (understanding) – Substantive tests – Not required (audit evidence) – Final review – required (overall reasonableness)

Analytical Procedures Documentation requirements: – Auditor’s expectation – Factors considered in the development – Results of the comparison – Additional procedures performed in response to significant unexplained differences – Results of such additional procedures Types of analytical: – Vertical / horizontal analysis – Ratio analysis

Limitations: Analytical Procedures – Differences do not necessarily indicate errors or fraud. – Differences simply indicate the need for further investigation

Substantive Procedures – Tests of Details A. Directional testing – If a test starts with items in the accounting records, the proper assertion is most likely to be existence (vouching). – If a test starts with source documents, it is most likely related to the completeness assertion (tracing).

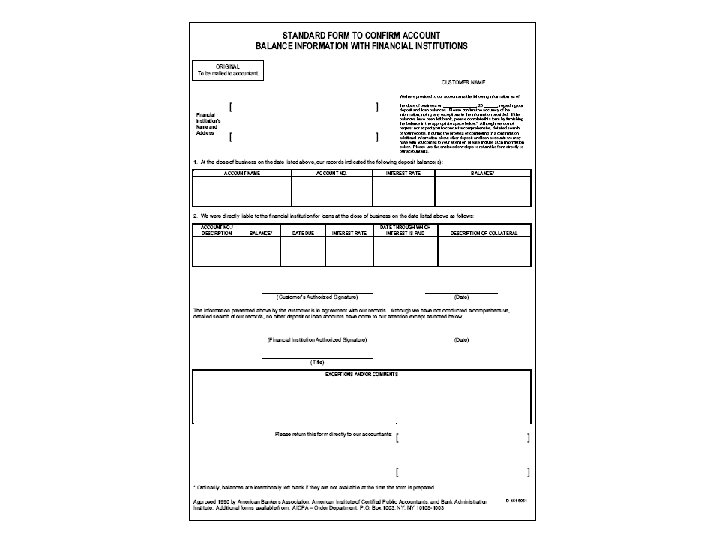

Substantive Procedures – Tests of Details B. External confirmation – Direct written response from a third party • Positive vs. negative – The auditor should maintain control – Non responses – Oral responses – Exceptions – difference reported

• • C. Standard Auditing Procedures Footing, crossfooting, and recalculation – math accuracy Valuation Inquiry – both internal sources & external sources (attorneys & bankers) – Presentation & disclosure Vouching –support for what has been recorded- Existence Examination/Inspection – careful examination of documents & records (minutes, contracts, invoices) 0 Existence Confirmation – written verification - Existence Analytical procedures - Completeness Reperformance – Valuation

Standard Auditing Procedures • • Reconciliation – substantiates the existence & valuation of accounts. It involves comparing financial amounts from two independent sources for agreement. Observation – direct personal knowledge. (existence or occurrence) Tracing – starts with the source documents and traces forward to provide assurance that the event is being given proper recognition in the books & records (completeness) Cutoff review of year end transactions –Completeness, Rights & obligations

Standard Auditing Procedures • Auditing related accounts simultaneously (LTD/ Interest) • Representation letter - Presentation and disclosures • Subsequent events review - Valuation

Relevant Assertions 1. Account balances – Completeness – Valuation – Existence – Rights and obligations

Relevant Assertions 2. Transactions and events – Completeness – Cut-off – Valuation – Existence – Understandability & classification

Relevant Assertions 3. Presentation & disclosure – Completeness – Valuation – Rights and obligations – Understandability and classification

Selection of Items 1. Selecting all items – small number of high dollar value items 2. Selecting specific items – all items that have a specific characteristic 3. Audit sampling – less than 100% (to be discussed in chapter #5)

Procedures to Assertions • Completeness • Tracing from source documents to the financial statements • Analytical review procedures • Observation of processes and procedures

Procedures to Assertions • Cut-off procedures

Procedures to Assertions • Allocation & Valuation • Recalculation (allowance) • Reconciliation of schedules to G/L

Procedures to Assertions • Existence • Confirmations • Observation, inspection, and examination

Procedures to Assertions • Rights & Obligations • Inspection of documentation supporting transactions, inspection of contracts

Procedures to Assertions • Understandability and classification • Review of all related disclosures for compliance with GAAP • Inquiry of management regarding disclosures for the account

Audit Procedures by Transaction Cycle

Cycles Revenue Sales revenues, receivables, and cash receipts Expenditure Purchases, payables, and cash disbursements Inventory Perpetual inventory, physical counts, and manufacturing costs Investments in debt and equity, and the income from investments Property, plant & equipment Acquisitions and disposals, and depreciation expense Payroll & personnel Financing Debt & equity financing, repayment, interest expense, and dividends

Revenue Cycle – Fraud Risk 1. 2. 3. 4. 5. 6. Early revenue recognition Holding books open Fictitious sales Failure to record sales returns Side agreements to sell more inventory than needed Understating the allowance

Revenue Cycle Sales Department – Receipt of a customer purchase order – Serially numbered sales order – Sent to credit department for approval Credit Department – Approval of sales order – Copy sent to: • Shipping department • Billing department • Accounting department

Revenue Cycle Shipping Department – A serially numbered bill of lading is prepared – Copy is sent to customer – Goods are shipped and a receivable arises Billing Department – Prepares a serially numbered sales invoice – Shipping documents, sales order & invoices are compared for completeness & mathematical accuracy – Invoice is sent to customer and to A/R Dept

Revenue Cycle Accounts Receivable Department – Sales is entered into the sales journal, and a receivable is recorded – Periodically, an independent person should reconcile the G/L and the A/R subsidiary records – When payment is received, the receivable is eliminated – Uncollectible are sent to Credit Manager follow up – Treasurer should authorize write-offs – Serially numbered receiving report may be used as to sales returns – Sales discounts procedures and records should be reviewed to ensure that discounts are properly given and recorded

Cash Receipts Collection of cash receipts Incoming mail must be opened by a person who does not have access to the A/R ledger Receipts should be listed in detail – A copy & actual receipts sent to the cashier for bank deposit – Another copy to the A/R Dept. for entry in the A/R ledger – Another copy to the accounting dept. for entry into the G/L Cash collections should be restrictively endorsed upon receipt and deposited daily Devices such as cash registers or lock boxes should be used as safeguards

Substantive Procedures - Revenue Cycle 1. Auditing accounts receivable – – Completeness – obtain an aged trial balance of accounts receivable & trace the total to the general ledger control account – Valuation, allocation & accuracy – examine the results of confirmations and test the adequacy of the allowance – Existence & occurrence – confirm a sample of accounts receivable – Rights & obligations – review bank confirmations and debt agreements for liens. Also, inquire management

Substantive Procedures - Revenue Cycle 2. Auditing sales transactions – – – Completeness – trace a sample of shipping documents to the sales invoices, and to the sales journal and accounts receivable ledger Cut-off – compare a sample of invoices from shortly before and after year end with the shipment dates & with the dates the sales were recorded Valuation, allocation & accuracy – compare prices on a sample of invoices with price lists and terms Existence & occurrence – vouch a sample of sales transactions from the sales journal to the customer order and shipping documents Understandability & classification – examine a sample of invoices for proper classification into revenue accounts

A/R - Confirmations is considered a required procedure unless: – Receivables are immaterial – Confirmation would be ineffective – Inherent & control risks are very low & evidence provided by other procedures is sufficient Provides evidence regarding existence and rights & obligations

Evidential Procedures – A/R Positive confirmations (existence): • Large accounts, expected errors, or items in dispute, and when internal control is weak. • May be blank confirmations / detail • Confirmations received electronically • Non responses should be followed up with 2 nd and 3 rd requests • Alternative procedures – Subsequent collections – Invoices / shipping documents

Evidential Procedures – A/R Negative confirmations (existence): – The combined assessed level of inherent & control risk is low – A large # of small account balances are being confirmed – There is no reason to expect that recipients of the requests will be unlikely to give them consideration

Expenditure Cycle Purchases • Purchase requisition – should be approved and pre-numbered • Purchase orders – prepared only after proper approval. Should be sent to: – Requisitioning department – Vendor – Receiving department – Accounting department

Expenditure Cycle Receiving Department The PO serves as an authorization to accept the goods when they arrive Forced to count A pre-numbered receiving report is prepared

Expenditure Cycle Accounts payable Department Recording the payable after comparing PO, RR & invoice Records as inventory and records a payable After matching and close to due date, documents are sent to the Treasurer

Expenditure Cycle Treasury Department Treasurer prepares, signs, and mails the checks and cancel all supporting documents after payment. Paid vouchers are returned to the accounting department for posting of the payment and filing of the documents

Substantive Audit Procedures - Expenditures 1. Auditing accounts payable • Completeness – – – • Agree accounts payable listing to G/L Obtain a sample of vendor statements and agree to the vendors accounts Perform a search for unrecorded liabilities Valuation, allocation, & accuracy – Foot the A/P listing and agree totals to the general ledger – Obtain a sample of vendor statements and agree to the vendors accounts – Review the results of accounts payable confirmations

Substantive Audit Procedures – A/P • Existence and occurrence – – • May confirm accounts payable balances (not required) Vouch selected amounts to the voucher packages Rights & obligations – Review a sample of voucher packages for the presence of the purchase requisition, purchase order, receiving report, and vendor invoice to verify ownership

Auditing Purchase Transactions A/P • Completeness – • • Trace a sample of vouchers to the purchase journal Cut-off Valuation, allocation, & accuracy – Recompute mathematical accuracy of a sample of vendors invoices • Existence – Test a sample of vouchers for authorization and the presence of a receiving report • Understandability & classification – Verify the account classification of a sample of purchases

Auditing Presentation & Disclosure A/P • Completeness – – • Payables by type Purchase contracts & commitments RPT Expenses by segment Valuation, allocation, & accuracy – Determine whether the info is accurate and presented at the appropriate amounts • Rights & obligations – Compare disclosures to other audit • Understandability & Classification – Read all notes to make sure they are understandable

CASH Fraud Risk Lapping – theft is concealed by failing to account for cash receipts – Prevent using a lock-box system Kiting – to cover a cash shortage or to pad a company’s cash position – Detect preparing a “Bank Transfer Schedule”

CASH Audit Procedures 1. Auditing the ending cash balance – Completeness, valuation & existence • • • Bank confirmation Bank reconciliation Cut-off bank statement 2. Auditing cash receipts and disbursements – Completeness – trace a sample of remittance advices to the cash receipts journal and deposit slips – Cut-off – perform tests – Valuation – Foot the deposit slips and agree to the cash receipts journal and bank statement

CASH Audit Procedures 3. Auditing Presentation & Disclosure – Completeness - ensure disclosure of: • • • Policy defining cash and cash equivalents Restrictions Compensating balances – Valuation – read the footnotes – Rights & obligations – compare disclosures to other evidence – Understandability & classification – read the disclosure

Evidential Procedures - Inventory Internal control - segregation of purchasing, receiving, storage, and shipping functions Observation is an auditing procedure. Alternative procedures can be used. Well-kept perpetual inventories – before, during, or after the end of the audit period (internal control)

Substantive Procedures – Inventory Balance Completeness – Inventory observation – Tracing test counts Valuation – Test math accuracy of listing – Inquire about obsolete or slow moving – Examine vendors invoice – Perform price tests Existence – Verify existence at the observation Rights & obligations – Analyze consigned goods Cut-off – To verify proper period Understandability & classification – Disclosures

Evidential Proc. - LTI Completeness – Confirm securities or count securities – Test dividend and interest income Valuation – Obtain listing – foot & trace to G/L – Compared values to prices published – Recalculate ending values – Evaluate impairment – Recalculate gain / losses Existence – Confirm securities and/or count securities Rights & obligations – Verify ownership Cut-off – To verify proper period Understandability & classification - disclosures

Evidential Proc. – PP&E Internal controls: Acquisition, subsidiary ledgers, physical security, written policies, disposition Audit procedures: – Completeness • • • – Cut-off • – Review purchases and dispositions near year end Valuation • – Review depreciation / amortization / gain or losses / impairment Existence • – Obtain & foot fixed asset schedule & trace to G/L Review the Repairs & Maintenance expense account Trace sample of purchase requisitions to receiving reports and the fixed asset subsidiary ledger Vouch a sample of purchases to receiving report & invoice Understandability & classification - disclosures

Substantive Proc. - Payroll Completeness – Test completeness of accruals Valuation – Recalculate year end payroll accruals – Compare total recorded payroll with total checks issued – Test extensions and footings – Verify pay rates – Recalculate gross and net • Existence – Vouch amounts from the client’s calculation of the payroll accrual to supporting documentation Rights & obligations – Verify that the payroll accrual is an obligation of the entity Cut-off – Trace a sample of time cards to the payroll register

Evidential Proc. – Debt & Equity Completeness – Review Board of Directors minutes – Obtain new debt agreements – Trace all to financials – Review interest expense Valuation – Examine new debt agreements for proper recording – Recompute any interest payable & recompute amortization Existence – Confirm with creditors Rights & obligations – Examine agreements to verify Cut-off – Proper period

Evidential Proc. - Capital Completeness: – – Confirmations Examine stock certificate book Valuation – – Recompute the value assigned to stock transactions Retained earnings – analyze movement. Existence – Vouching transactions to minutes Understandability & classification – Review restrictions on retained earnings resulting from loans, agreements, or state laws.

OTHER AUDIT PROCEDUES

Related Party Transactions Related party transactions – responsible for identifying any related party transactions encountered & for determining whether the transactions are given proper disclosure. Determining existence of RPT’s: • • • Evaluating the company’s procedures for identifying & accounting for Asking management for the names and activities during the year Reviewing filings & other regulatory reports Reviewing material transactions for RPT evidence Reviewing prior years’ audit documentation or predecessor

Evidential Proc. – RPT’s Once a related party transaction has been identified, the auditor should obtain an understanding of the business purpose of the transaction and test the amounts to be disclosed (per GAAP). Indicative of a RPT: – – – Compensatory balances Loan guarantees Unusual non-recurring entries Non monetary transactions Not in the ordinary course of business

Evidential Proc. – Estimates Auditor’s Responsibilities: – – Assess written policies & practices regarding the development and use of estimates Verify that all material estimates have been developed Determine that the accounting estimates are reasonable Ensure that estimates are properly disclosed in accordance with GAAP Procedures: – – – Review & test procedures used by management Develop an independent estimate Review subsequent events & transactions

Evidential Proc. – Fair Values Management is responsible for making fair value measurements & disclosures in accordance with GAAP Auditor’s responsibility: – – – – Understand the entity’s process and controls Assess risk of material misstatements Evaluate conformity with GAAP, including disclosures Consider need for a specialist Test fair value measurements & disclosures Evaluate the sufficiency, competency, & consistency of evidence Obtain management representations Communicate relevant matters to the audit committee

Evidential Proc. – Fair Values The auditor may: – – – Determine whether significant assumptions provide a reasonable basis for fair value measurements. Consider intent and ability. Evaluate the valuation model. Test the underlying data for accuracy, completeness, relevancy, and consistency Develop independent fair value estimates Review subsequent events and transactions

Evidential Proc. – Litigation The auditor must obtain competent evidential matter pertaining to litigation, claims, and assessments. Inquiry to management Review documents, such as minutes, invoices from lawyers, contracts, loan agreements, leases, correspondence from tax authorities. Legal letter (signed by client, received by auditor) – – – Substantial attention Refusal to respond Refusal to permit inquiry

Evidential Proc. – Litigation Specific inquiry: • • Nature of the matter, including period of occurrence. The progress of the case to date. The degree of possibility of an unfavorable outcome. The amount or estimate of potential loss.

Evaluating Audit Findings Perform analytical review procedures Evaluate audit findings – professional judgment – Size of misstatement – Effects – Aggregate of known and likely – Prior period adjustments – Qualitative considerations

Communication to Management All misstatements – Distinguish between known & likely – Request management to make appropriate corrections – Reevaluate the misstatement, after management has made adjustments Documentation requirements: – Materiality & tolerable misstatements – Known & likely misstatements – A summary of uncorrected misstatements

Reviewing the Work of Others Consideration of whether: 1. In accordance with applicable standards 2. Significant findings need further consideration 3. Appropriate consultation 4. Procedures are appropriate 5. Supports the conclusion 6. Evidence is sufficient and appropriate 7. The objectives have been achieved

Reviewing the Work of Others Engagement partner review – Critical areas – Significant risks – Other important areas Documentation requirements – Who performed the work and when – Who reviewed the documentation and the date

Engagement Quality Review - PCAOB Partner not otherwise associated with the engagement – Hold discussions with the audit team & review – Evaluate judgments – Evaluate assessments – Evaluate independence – Review financials and report – Evaluate communications – Evaluate documentation in general

Engagement Quality Review - PCAOB Approval only if no significant deficiencies – Failed to obtain appropriate evidence – Reached an inappropriate conclusion – Report is not appropriate – Not independent

Preguntas?