ASSET TRACKING AND INVENTORY MANAGEMENT PINELLAS COUNTY SCHOOLS

- Slides: 9

ASSET TRACKING AND INVENTORY MANAGEMENT PINELLAS COUNTY SCHOOLS

• $1000 or more • Includes all types of equipment and technology UNCAPITALIZED TECHNOLOGY TAGGED FIXED ASSETS ASSET CATEGORIES • $200 and $999. 99 • Laptops, desktops, tablets, drones • Equipment other than technology valued between $300 and $999. 99

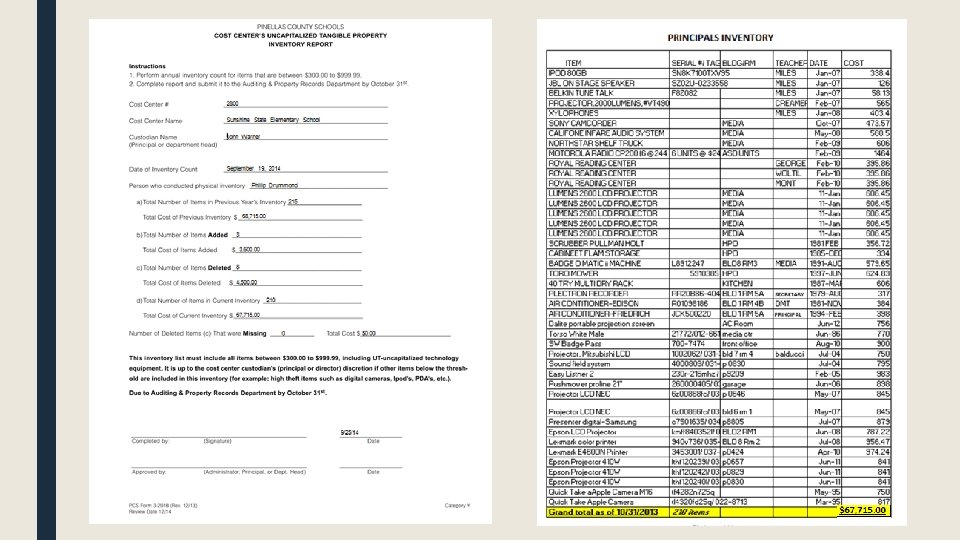

BOARD POLICY 7450 – INVENTORIES AND PROPERTY RECORDS ■ $1000 or more shall be tagged and inventoried annually by District personnel ■ The principal, director, or department head shall be responsible for taking inventories of properties valued between $300 and $999. 99 ■ Cost Center’s Uncapitalized Tangible Property Inventory Report (PCS 3 -2918) is due by October 31 annually

Uncapitalized Inventory and Reporting Requirements • A physical inventory of items ranging from $300. 00 to $999. 99 must be completed. • A itemized perpetual inventory spreadsheet of these items must be submitted on a shared folder. • A Cost Center’s Uncapitalized Property Inventory Report (PCS 3 -2918) is due to Auditing and Property Records Department annually no later than October 31 st. • The total cost/items of previous years report should be the beginning balance on this years report. • The value of items on the spreadsheet must balance with the dollar value listed on the report.

THE IMPACT

Inventory Process Property Control conducts physical inventory of fixed assets A sample of 20 uncapitalized technology is verified Initial Unlocated List Initial Visit Final Inventory Report Principal responds to any deficiencies

Unlocated Fixed vs Uncapitalized Technology UNCAPITALIZED TECHNOLOGY FIXED ASSETS 2014 -15 2015 -16 2016 -17 Total Items Inventoried 88, 693 73, 761 M 1's (Missing 1 st year) 411 309 384 M 2's (Missing 2 nd year) 177 128 105 0. 66% 0. 59% 0. 69% 219 200 206 57 71 83 104 116 125 Percentage of Missing Items Total Procedural Deficiencies Total Repeat Deficiencies Total Perfect Inventory Reports 70, 673 2015 -16 2016 -17 Total Items Inventoried 4574 21911 M 1's (Missing 1 st year) 189 563 Percentage of Missing Items 4. 13% 2. 57% Total Procedural Deficiencies 22 67 Total Repeat Deficiencies 0 7 Total Perfect Inventory Reports 0 2

Procedural Deficiencies ■ Proper Segregation of duties procedures are clearly defined and are being followed. ■ Temporary Property Removal Contracts have been completed and updated annually. ■ Equipment Assignment Lists have been completed and updated for all staff members. ■ Annual physical inventories are being conducted by the site. ■ Perpetual inventory records are maintained and updated annually. ■ Asset transfers are completed and updated timely. ■ Damage and/or Loss of Property Reports have been completed and submitted as needed.