Answer 5 4 18 Answer cont 5 4

5. 4 · 19")

5. 4 · 20")

- - - 5. 4 · 21")

5. 4 · 25")

- 5. 4 · 26")

- - - 5. 4 · 27")

- Slides: 34

Answer 5. 4 · 18

Answer (cont) 5. 4 · 19

Answer (cont) 5. 4 · 20

Answer (cont) - - - 5. 4 · 21

Answer 5. 4 · 24

Answer (cont) 5. 4 · 25

Answer (cont) - 5. 4 · 26

Answer (cont) - - - 5. 4 · 27

IS: Profit b 4 tax Notes Interest payable. The payment is accounted for subsequently. We add back because we only want to examine cash from operations Changes In CA Interest paid in the year is equal to the expense recorded Notes Half of the tax expenses for each of the two years is paid in the current

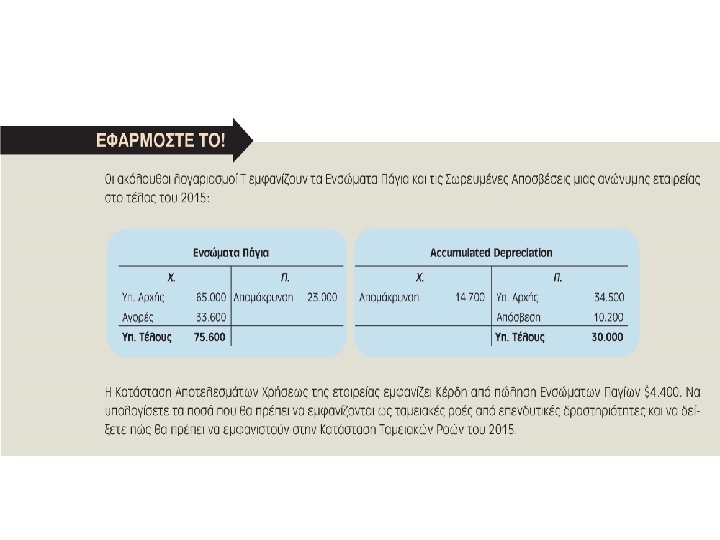

Since there were no disposals, the depreciation charges must be the difference between the start and end of the year’s non-current asset values, adjusted by the cost of any additions. Therefore: 172 + x – 10 – 12 = 186 => x = 36

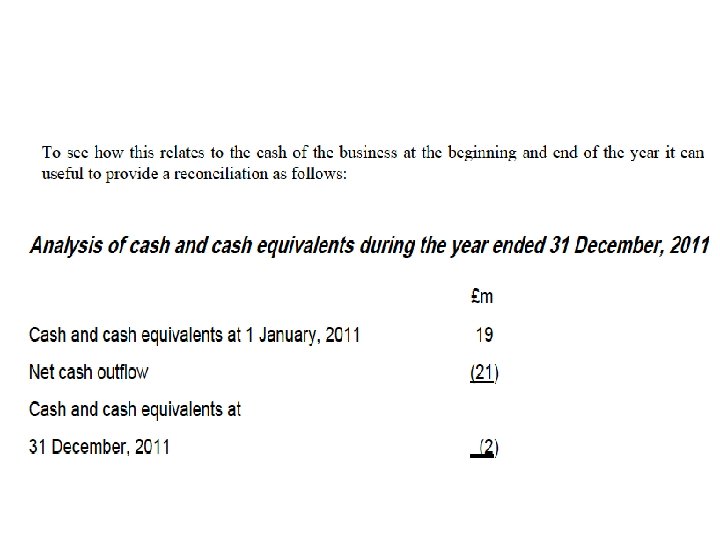

Total Cash change in the year Cash at the beginning of the year Negative cash so need to recognise a current liability of an overdraft in order to continue operating

Exercise 5. 4 – Chapter 5