ANALYSIS AND INTERPRETATION OF FINANCIAL STATEMENTS Financial Statement

u")

(2) (3)")

Newspapers (e. g.")

")

× 100% = 48. 9%")

and operating expenses")

ratio ·Acid-test (quick) ratio")

Ratios » Equity (stockholders’ equity) ratio")

Ratio #1 Current Ratio = Current Assets Current Liabilities Current Ratio")

Ratio #2 Acid-Test = Ratio Quick Assets Current Liabilities Quick assets are")

Ratio #2 Acid-Test = Ratio Quick Assets Current Liabilities Norton Corporation’s quick")

Ratio #2 Acid-Test = Ratio Quick Assets Current Liabilities $50, 000 $42,")

#8 Return on Stockholders’ = Equity Net")

- Slides: 65

ANALYSIS AND INTERPRETATION OF FINANCIAL STATEMENTS

Financial Statement Analysis l Non-accounting majors, especially, should relate well to this module It looks at accounting information from users’ perspective l What is financial statement analysis? ”Tearing apart” the financial statements and looking at the relationships

Financial Statement Analysis Who analyzes financial statements? Internal users (i. e. , management) u External users (emphasis of module) u Examples? Investors, creditors, regulatory agencies & … stock market analysts and auditors

Financial Statement Analysis l What do internal users use it for? Planning, evaluating and controlling company operations l What do external users use it for? Assessing past performance and current financial position and making predictions about the future profitability and solvency of the company as well as evaluating the effectiveness of management

Financial Statement Analysis Information is available from u Published annual reports (1) (2) (3) (4) (5) u Financial statements Notes to financial statements Letters to stockholders Auditor’s report (Independent accountants) Management’s discussion and analysis Reports filed with the government

Financial Statement Analysis Information is available from u Other sources (1) Newspapers (e. g. , Graphic, Times, etc ) (2) Periodicals (3) Financial information organizations such as: Moody’s, Standard & Poor’s, Dun & Bradstreet, Inc. , and Data Bank, Strategic African Securities (4) Other business publications

Methods of Financial Statement Analysis l Horizontal l Vertical Analysis l Common-Size l Trend l Ratio Statements Percentages Analysis

Horizontal Analysis Using comparative financial statements to calculate cedi or percentage changes in a financial statement item from one period to the next

Vertical Analysis For a single financial statement, each item is expressed as a percentage of a significant total, e. g. , all income statement items are expressed as a percentage of sales

Common-Size Statements Financial statements that show only percentages and no absolute cedi amounts

Trend Percentages Show changes over time in given financial statement items (can help evaluate financial information of several years)

Ratio Analysis Expression of logical relationships between items in a financial statement of a single period (e. g. , percentage relationship between revenue and net income)

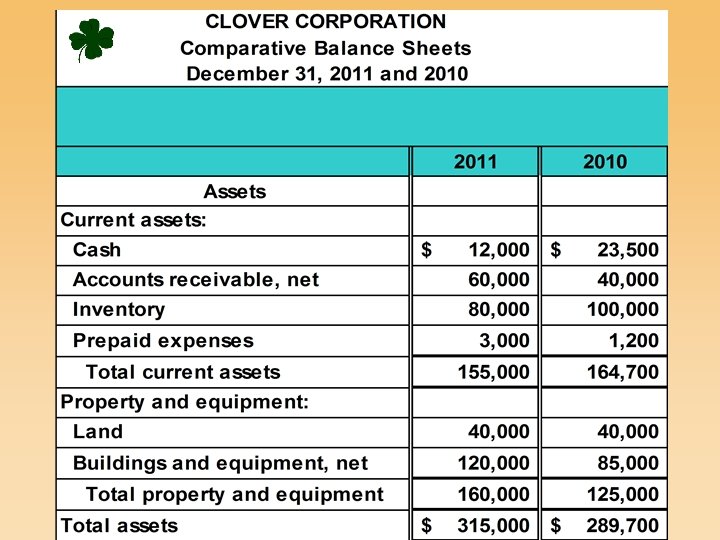

Horizontal Analysis Example The management of Clover Company provides you with comparative balance sheets of the years ended December 31, 2010 and 2011. Management asks you to prepare a horizontal analysis on the information.

Horizontal Analysis Example Calculating Change in Dollar/Cedi Amounts Cedi Change = Current Year Figure – Base Year Figure

Horizontal Analysis Example Calculating Change in Cedi Amounts Cedi Change = Current Year Figure – Base Year Figure Since we are measuring the amount of the change between 2010 and 2011, the cedi amounts for 2010 become the “base” year figures.

Horizontal Analysis Example Calculating Change as a Percentage Change = Cedi Change Base Year Figure × 100%

Horizontal Analysis Example $12, 000 – $23, 500 = $(11, 500)

Horizontal Analysis Example ($11, 500 ÷ $23, 500) × 100% = 48. 9%

Horizontal Analysis Example

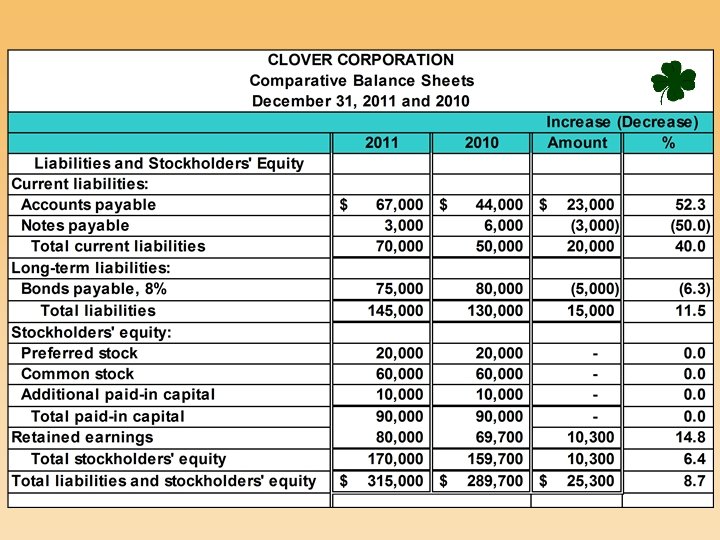

Horizontal Analysis Example Let’s apply the same procedures to the liability and stockholders’ equity sections of the balance sheet.

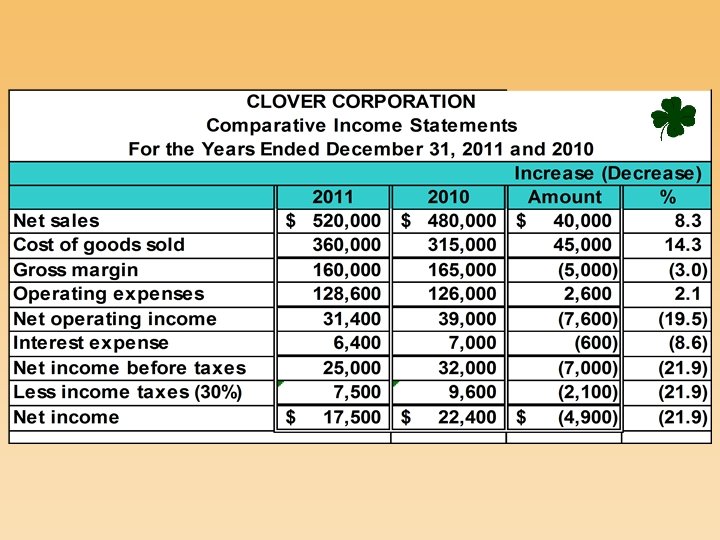

Horizontal Analysis Example Now, let’s apply the procedures to the income statement.

Sales increased by 8. 3% while net income decreased by 21. 9%.

There were increases in both cost of goods sold (14. 3%) and operating expenses (2. 1%). These increased costs more than offset the increase in sales, yielding an overall decrease in net income.

Vertical Analysis Example The management of Sample Company asks you to prepare a vertical analysis for the comparative balance sheets of the company.

Vertical Analysis Example

Vertical Analysis Example $82, 000 ÷ $483, 000 = 17% rounded $30, 000 ÷ $387, 000 = 8% rounded

Vertical Analysis Example $76, 000 ÷ $483, 000 = 16% rounded

Trend Percentages Example Wheeler, Inc. provides you with the following operating data and asks that you prepare a trend analysis.

Trend Percentages Example Wheeler, Inc. provides you with the following operating data and asks that you prepare a trend analysis. $1, 991 - $1, 820 = $171

Trend Percentages Example Using 2007 as the base year, we develop the following percentage relationships. $1, 991 - $1, 820 = $171 ÷ $1, 820 = 9% rounded

Ratios can be expressed in three different ways: 1. Ratio (e. g. , current ratio of 2: 1) 2. % (e. g. , profit margin of 2%) 3. $ (e. g. , EPS of $2. 25) CAUTION! “Using ratios and percentages without considering the underlying causes may be hazardous to your health!” lead to incorrect conclusions. ”

Categories of Ratios l Liquidity Ratios Indicate a company’s short-term debt-paying ability l Equity (Long-Term Solvency) Ratios Show relationship between debt and equity financing in a company l Profitability Tests Relate income to other variables l Market Tests Help assess relative merits of stocks in the marketplace

10 Ratios You Must Know Liquidity Ratios ¶Current (working capital) ratio ·Acid-test (quick) ratio u Cash flow liquidity ratio ¸Accounts receivable turnover ¹Number of days’ sales in accounts receivable ºInventory turnover u Total assets turnover

10 Ratios You Must Know Equity (Long-Term Solvency) Ratios » Equity (stockholders’ equity) ratio u Equity to debt

10 Ratios You Must Know Profitability Tests Return on operating assets ¼Net income to net sales (return on sales or “profit margin”) margin” ½Return on average common stockholders’ equity (ROE) ROE u Cash flow margin ¾Earnings per share u Times interest earned u Times preferred dividends earned u

10 Ratios You Must Know Market Tests Earnings yield on common stock ¿Price-earnings ratio u Payout ratio on common stock u Dividend yield on preferred stock u Cash flow per share of common stock u

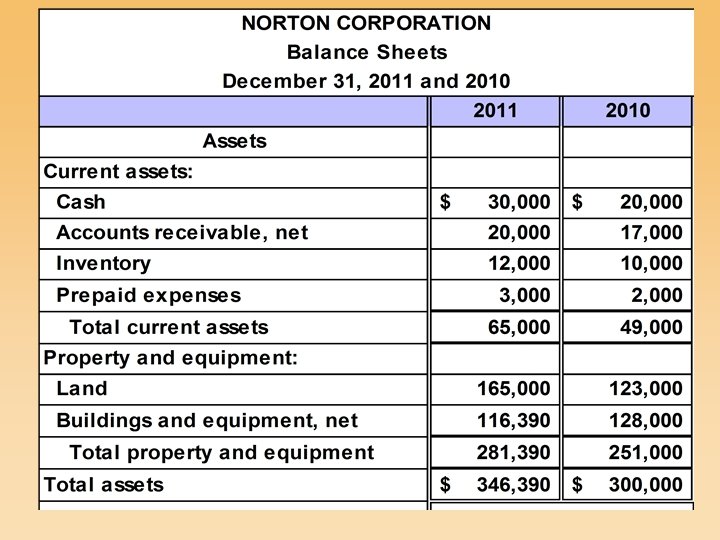

Now, let’s calculate the 10 ratios based on Norton’s financial statements.

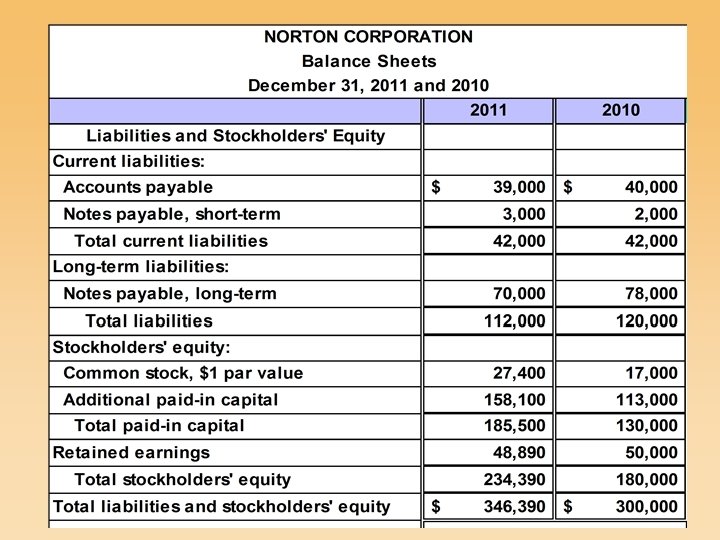

We will use this information to calculate the liquidity ratios for Norton.

Working Capital* The excess of current assets over current liabilities. * While this is not a ratio, it does give an indication of a company’s liquidity.

Current (Working Capital) Ratio #1 Current Ratio = Current Assets Current Liabilities Current Ratio = $65, 000 $42, 000 = 1. 55 : 1 Measures the ability of the company to pay current debts as they become due.

Acid-Test (Quick) Ratio #2 Acid-Test = Ratio Quick Assets Current Liabilities Quick assets are Cash, Marketable Securities, Accounts Receivable (net) and current Notes Receivable.

Acid-Test (Quick) Ratio #2 Acid-Test = Ratio Quick Assets Current Liabilities Norton Corporation’s quick assets consist of cash of $30, 000 and accounts receivable of $20, 000.

Acid-Test (Quick) Ratio #2 Acid-Test = Ratio Quick Assets Current Liabilities $50, 000 $42, 000 = 1. 19 : 1

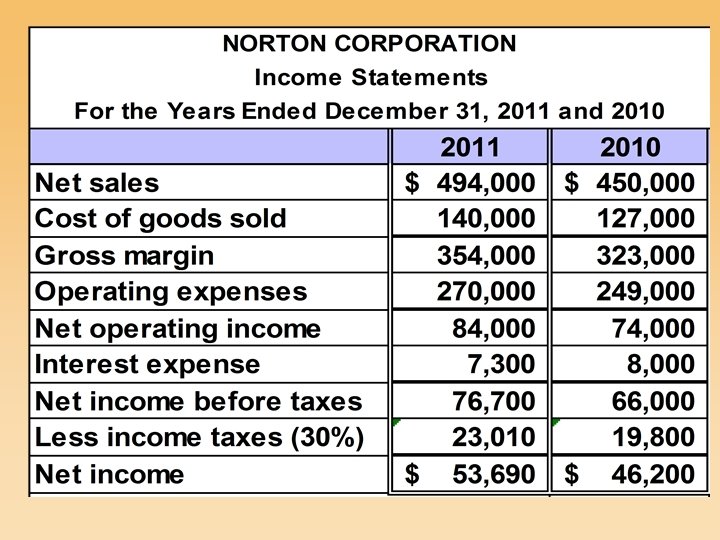

Accounts Receivable Turnover Net, credit sales Accounts Receivable = Turnover #3 Average, net accounts receivable Sales on Account Average Accounts Receivable Accounts $494, 000 = 26. 70 times Receivable = ($17, 000 + $20, 000) ÷ 2 Turnover This ratio measures how many times a company converts its receivables into cash each year.

Number of Days’ Sales in Accounts Receivable #4 Days’ Sales in Accounts = Receivables 365 Days Accounts Receivable Turnover 365 Days 26. 70 Times = 13. 67 days Measures, on average, how many days it takes to collect an account receivable.

Number of Days’ Sales in Accounts Receivable #4 Days’ Sales in Accounts = Receivables 365 Days Accounts Receivable Turnover 365 Days 26. 70 Times = 13. 67 days In practice, would 45 days be a desirable number of days in receivables?

Inventory Turnover #5 Inventory Turnover = Cost of Goods Sold Average Inventory $140, 000 = = 12. 73 times ($10, 000 + $12, 000) ÷ 2 Measures the number of times inventory is sold and replaced during the year.

Inventory Turnover #5 Inventory Turnover = Cost of Goods Sold Average Inventory $140, 000 = = 12. 73 times ($10, 000 + $12, 000) ÷ 2 Would 5 be a desirable number of times for inventory to turnover?

Equity, or Long–Term Solvency Ratios This is part of the information to calculate the equity, or long-term solvency ratios of Norton Corporation.

Here is the rest of the information we will use.

Equity Ratio #6 Equity = Ratio Stockholders’ Equity Total Assets $234, 390 $346, 390 Measures the proportion of total assets provided by stockholders. = 67. 7%

Net Income to Net Sales A/K/A Return on Sales or Profit Margin #7 Net Income = to Net Sales $53, 690 $494, 000 = 10. 9% Measures the proportion of the sales dollar which is retained as profit.

Net Income to Net Sales A/K/A Return on Sales or Profit Margin #7 Net Income = to Net Sales $53, 690 $494, 000 = 10. 9% Would a 1% return on sales be good?

Return on Average Common Stockholders’ Equity (ROE) #8 Return on Stockholders’ = Equity Net Income Average Common Stockholders’ Equity $53, 690 ($180, 000 + $234, 390) ÷ 2 Important measure of the income-producing ability of a company. = 25. 9%

Earnings Per Share #9 Earnings Available to Common Stockholders Earnings = Weighted-Average Number of Common per Shares Outstanding Earnings $53, 690 = per Share (17, 000 + 27, 400) ÷ 2 = $2. 42 The financial press regularly publishes actual and forecasted EPS amounts.

Earnings Per Share l What’s new from EPS Weighted-average calculation Earnings available to common stockholders EPS of common stock = ____________ Weighted-average number of common shares outstanding l Three alternatives for calculating weighted-average number of shares

Earnings Per Share l What’s new ; Weighted-average calculation Earnings available to common stockholders EPS of common stock = ____________ Weighted-average number of common shares outstanding Alternate #1

Earnings Per Share Alternate #2 Alternate #3

Price-Earnings Ratio A/K/A P/E Multiple #10 Price-Earnings = Ratio Market Price Per Share EPS Price-Earnings = Ratio $20. 00 $ 2. 42 = 8. 3 : 1 Provides some measure of whether the stock is under or overpriced.