AMERICAN AND EUROPEAN OPTION KINDA SUMLAJI PUT Option

- Slides: 17

AMERICAN AND EUROPEAN OPTION KINDA SUMLAJI PUT

Option Style The most popular options are either European or American A European option may be exercised only at the expiration date of the option. An American option may be exercised at any time before the expiry date.

Put Option Contract between two parties to exchange an asset, at a specified price (the strike K), by a predetermined date (the expiry or maturity T). The buyer of the put, has the right to sell the asset at the strike price by the future date, while the seller of the put, has to buy the asset at the strike price if the buyer exercises the option. Payoff at maturity

Put Option If ST < , then the option will be exercised, the holder of this option will buy the underlying stock at a price of ST and exercise his right to sell it to the writer at the strike price of K, to make a profit of If ST > , In this case, exercising the right to sell the underlying asset would result in a loss. If the option is not exercised by maturity, it expires worthless.

Option’s parameters

Option Pricing Black-Scholes Model

Option Pricing Binomial options pricing model Valuation is performed iteratively, starting at each of the final nodes, and then working backwards through the tree towards the first node (valuation date). The value computed at each stage is the value of the option at that point in time. Option valuation using this method is, as described, a three-step process: � price tree generation, � calculation of option value at each final node, � Sequential calculation of the option value at each preceding node.

Binomial options pricing model STEP 1: Create the binomial price tree

Binomial options pricing model STEP 2: Find Option value at each final node At each final node of the tree, the option value is equal to:

Binomial options pricing model STEP 3: Find Option value at earlier nodes

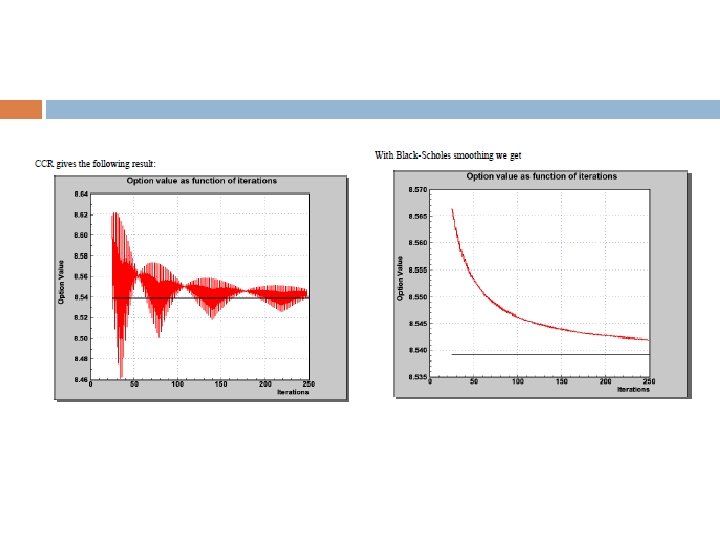

Binomial options pricing model The Cox-Ross-Rubenstein model Black-Scholes smoothing

Example

1 45 2. 2 2 64 29 825 14 82 87. 5 5 57 62 685 17 27 77. 3 4 39 04 345 20 45 00. 7 5 75 11 268 24 53 59. 6 6 69 16 394 29 06 75. 3 0 77 35 032 34 33 93. 9 4 77 11 911 41 55 86. 6 1 20 85 967 49 08 58. 6 03 53 14 79 59 1 5. 1 64 553 68 36 70 15 68. 4 8 80 87 971 83 13 45. 9 2 70 92 076 10 07 0 1 12 19. 2 46 12 166 14 36 90 1. 5 67 93 485 16 26 04 9. 8 58 79 483 20 09 37 1. 7 52 70 074 23 48 88 9. 29 75 67 39 28 17 5 11 651. 63 80 34 16 41 0. 0 66 90 827 40 82 51 5. 9 99 44 668 48 67 07 3. 6 41 10 181 57 28 46 5. 6 02 05 760 68 73 51 5. 6 48 99 658 81 18 61 6. 9 69 67 125 65 Option Value 100 90 80 70 60 50 40 30 20 10 0 Stock S

1 12 19. 2 46 12 166 14 36 90 1. 5 67 93 485 16 26 04 9. 8 58 79 483 20 09 37 1. 7 52 70 074 23 48 88 9. 29 75 67 39 28 17 5 11 651. 63 80 34 16 41 0. 0 66 90 827 40 82 51 5. 9 99 44 668 48 67 07 3. 6 41 10 181 57 28 46 5. 6 02 05 760 68 73 51 5. 6 48 99 658 81 18 61 6. 9 69 67 125 65 1 45 2. 2 2 64 29 825 14 82 87. 5 5 57 62 685 17 27 77. 3 4 39 04 345 20 45 00. 7 5 75 11 268 24 53 59. 6 6 69 16 394 29 06 75. 3 0 77 35 032 34 33 93. 9 4 77 11 911 41 55 86. 6 1 20 85 967 49 08 58. 6 03 53 14 79 59 1 5. 1 64 553 68 36 70 15 68. 4 8 80 87 971 83 13 45. 9 2 70 92 076 10 07 0 Option Vlaue 100 90 80 70 60 50 40 30 20 10 0 Stock S

10 9 American value- European value 8 7 6 5 4 3 2 1 0 816. 6169 9125 6765 340. 4166 0827 9082 141. 9067 5485 9326 Stock S 59. 1 5553 6436 6815 24. 6 5969 6394 1606

. 2 4 14 56. 5 42 8 8 17 75 25. 3 75 29 7 6 20 73 85 82. 7 94 62 0 3 24 07 45 27. 6 55 04 5 2 29 96 68 45. 3 96 11 7 3 34 57 94 53 7 1. 9 9 00 6 41 37 32 06. 6 74 35 86 91 3 49 20 11 3. 6 19 1 59 58 67 55. 1 53 85 5 0 70 55 37 08. 4 36 91 6 4 83 88 36 41 0 6. 9 45 897 815 70 18 20 71 76 3 11 92 9. 1 07 14 24 1. 62 9 1 10 16 06 66 0 9. 75 12 0 4 20 45 85 36 1. 88 93 37 48 2 23 52 37 6 9 70 9 28. 88 74 09 5. 75 70 7 2 34 65 93 48 0. 11 96 4 1 40 16 80 71 5. 60 63 5 8 48 19 27 16 3. 99 90 0 6 57 74 68 82 5. 16 44 4 1 68 60 81 67 2 1 5. 5 67 0 81 14 60 28 6. 86 05 61 65 73 69 89 91 91 25 8 67 65 12 Option Value 100 90 80 70 60 50 40 Americant 0. 5 30 European t 0. 5 20 10 0 Stock S