AILG Training Seminar for Elected Members Local Authority

AILG Training Seminar for Elected Members Local Authority Finance & Budgets Tom Moylan

AILG - Local Government Finance Training Module Local Authority Finance & Budgets - Key messages for Elected Members 1. 2. 3. 4. 5. Changes to Commercial Rates for 2015 The Budget Documents – A guide for the Elected Member Determination of Annual Rate on Valuation (ARV) Annual Financial Statement (AFS) Schedule of Municipal District Works Note: Ø It should be noted that the umbrella term “municipal district” includes all other variations of this type of formation as set out in Part 3 A section 22 A of the Local Government Act 2001 (as inserted by the Local Government Reform Act 2014) e. g. metropolitan or borough districts. Ø In the case where a local authority does not have municipal districts, the requirements relating to municipal districts will therefore not apply, e. g. Galway City Council.

1. Ø Ø Changes to Commercial Rates for 2015 Commercial rates – key messages for elected members Significant contribution to the funding of local government – Rates account for between 9% and 61% of total funding for local services at individual local authority level, averaging over 35% nationally Elected members are legally required to adopt an Annual Rate on Valuation (ARV) at the annual budget meeting. This ARV is applied to the valuation of each property as determined by the Valuation Office to determine the amount of rates that each individual rate payer is required to pay. Local Government Reform Act 2014 dissolved a number of rating authorities and provided that each county, city or city and county council will now constitute a single rating authority for the whole of that area. As a result, the differing ARVs that have prevailed across former rating authority areas (i. e. former town councils etc. ) must be harmonised. The 2014 Act provided a mechanism for the harmonisation of ARVs within counties over a ten year period with the use of a Base Year Adjustment (BYA). The Act now requires that each local authority (that now encompasses former rating authorities where differing ARVs applied) must, in addition to the ARV, adopt a Base Year Adjustment for each former rating authority area.

1. Changes to Commercial Rates for 2015 Commercial rates – key messages for elected members Ten year adjustment period beings in 2015 In 2015, the BYA is calculated as the difference between the 2014 ARV and the new 2015 ARV – neutralises any increase/ decrease in rates due in 2015 that would otherwise occur as a result of the ARV struck by the members for the amalgamated authority as a whole, i. e. rate payers will pay no more or no less in 2015 than they did in 2014: arithmetic exercise in 2015 From 2016 on, members continue to adopt an ARV; however, the ARV cannot be increased until BYA has been eliminated. Members should also adopt a BYA for each former rating authority - each BYA must be reduced annually to become closer to zero until it is eliminated 2014 Act requires that there is consultation with MD members in the area of the former rating authority (s 29(4)) prior to the adoption of the BYA

1. Changes to Commercial Rates for 2015 Commercial rates – key messages for elected members Vacancy refunds Legislation determines that owners of vacant premises are entitled to a refund of rates if their property was vacant on the date of the making of the rate. The Local Government Act 1946 provides that the owner of vacant premises is entitled to a 100% refund in most local authority areas. Separate legislation governs refunds in the cities of Dublin, Limerick and Cork, where the same criteria for refunds apply but only 50% of the rates paid is refundable. Local Government Reform Act 2014 provides local authorities with the discretion to vary the rate of refund (0 -100%) that applies in individual local electoral areas. The Local Government (Financial and Audit Procedures) Regulations 2014 provide that the decision to alter the rate of refund should be taken at the annual budget meeting and that the rate of refund decided in respect of the relevant local electoral area shall apply to eligible persons for the year to which the budget relates. The absence of a decision to vary the refund means that the existing legislative provisions regarding the rate of refunds apply (either 100% or 50% as set out above).

1. Ø Changes to Commercial Rates for 2015 Commercial rates – key messages for elected members Summary of rates decisions to be taken at the annual budget meeting Ø In 2015, Councils will be required to - Ø adopt ARV for the county/ city as a whole (this cannot be increased until harmonisation has been achieved); and Ø decide if they want to alter vacancy refunds available in 2015 and if so, what rate and for which LEAs. Ø From 2016, Councils will be required to – Ø adopt ARV for the county/ city as a whole (this cannot be greater that the ARV adopted for 2015 until harmonisation has been achieved); Ø reduce the BYA that applies in each former rating authority area; and Ø decide if they want to alter vacancy refunds available for each specific year and if so, what rate and for which LEAs.

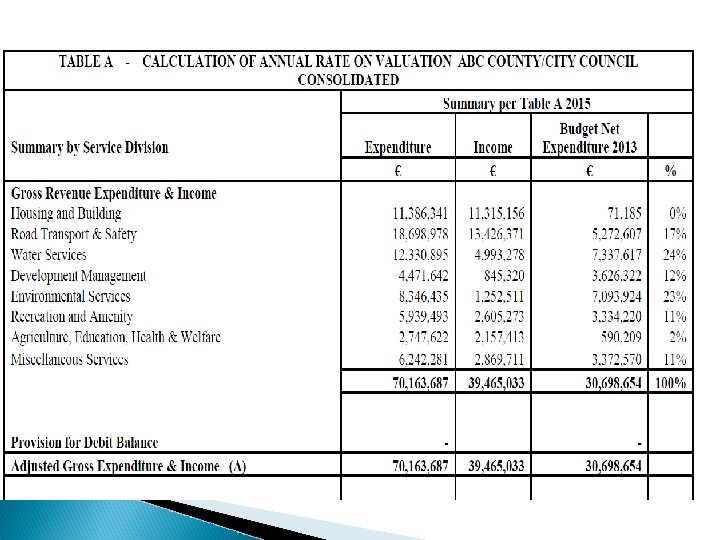

2. The Budget Documents – A guide for the Elected Member Ø There are six statutory tables included in the budget documents (Tables A-F). 1) Table 2) Table 3) Table 4) Table 5) Table 6) Table Ø Ø A– B– CD– E– F- Calculation of Annual Rate on Valuation Including BYA Detailed Expenditure & Income Rates information including BYA (updated format for 2015) Analysis of Budget Income from Goods & Services Analysis of Budget Income from Grants & Subsidies Detailed Expenditure and Income by Division New Structure to Budget Format/Documents was introduced in 2009 with a move to a service costing based structure (Service Support Costs – Full cost disclosure for delivery of each service) Services and Sub Services are rolled up into 8 Division Groups

2. The Budget Documents – A guide for the Elected Member Table B & F – Detailed Expenditure & Income Ø 8 No. Divisions (A-H) & Central Management Charge Division 1. Division A – Housing & Building 2. Division B – Road Transport and Safety 3. Division C – Water Services 4. Division D – Development Management 5. Division E – Environmental Services 6. Division F – Recreation and Amenity 7. Division G – Agriculture, Education, Health & Welfare 8. Division H – Miscellaneous 9. Division J – Central Management Charges

2. The Budget Documents – A guide for the Elected Member Division Description Current Expenditure Current Income A Housing & Building LA Housing Repairs & Maintenance Costs Traveller Accommodation Estate Management Assistance to persons housing themselves (Housing Loans & Grants) RAS Programme Loan Charges Service Support Costs - Direct Salaries & Staff Costs - Direct O/Heads - Central Management Charge - Indirect O/Heads Housing Rents Recoupable Salaries Recoupable Grants RAS Payments Recoupable Payments B Road Transport & Safety Road Upkeep & Maintenance Costs Road/Footpath Improvements Public Lighting Road Safety & Traffic Management & Control Loan Charges Service Support Costs Central Management Charge Road Grants – DOE Fund Parking Fees Road Opening Fees Hackney Licences Recoupable Salaries /Grants C Water Services Public water & sewerage supply – Service Level agreement with Irish Water Public Conveniences Group Water Schemes Service Support Costs Central Management Charge Irish Water Income – Service level agreement Grants – DOE Fund Recoupable Grants/Salaries

2. The Budget Documents – A guide for the Elected Member Divisio n Description Current Expenditure Current Income D Development Management Planning Control & Enforcement Taking in Charge of Estates Urban/Village Renewal Tidy Towns Community & Enterprise Tourism Development Local Enterprise Offices Local Community Development Committee Service Support Costs Central Management Charge Planning App. Fees Licence Fees Urban Renewals Grants Recoupable Grants/Salaries F Recreation & Amenity Op. Costs – Recreational Centres , Libraries , Public Amenities Community, Sport & Recreation Development Maintenance of Parks / Open Spaces Arts/Cultural Centres Arts Programme Heritage Service Support Costs Central Management Charges – Recreation Centres Libraries & Public Amenities Recoupable Grants/Salaries G Agriculture, Education, Health & Welfare Land Drainage River Cleaning Veterinary Service Support Costs Central Management Charge Recoupable Salaries /Grants

2. The Budget Documents – A guide for the Elected Member Divisio n Description Current Expenditure Current Income H Miscellaneous Financial Management Costs for Collection of Rates Legal, Printing & Stationery Irrecoverable Rates Elections & Audit fees Admin of Justice/Consumer - Coroners Fees Food Safety Councillors & SPC Costs Motor Tax Operation Service Support Costs Central Management Charge Sale of Election Registers Licences (Dog Licences) Recoupable Grants/Salaries – Motor Tax J Central Management Charge Corporate Building Costs Corporate Services Information Technology Print/Post Room Human Resources & Finance Function Pensions District Offices

Table F Division A - HOUSING AND BUILDING - Pg 1 Expenditure by Service and Sub-Service Adopted by Council Code A 0101 Maintenance of LA Housing Units A 0102 Maintenance of Traveller Accommodation Units A 0103 Traveller Accommodation Management A 0104 Estate Maintenance A 0199 Service Support Costs Maintenance/Improvement of LA Housing Units A 0201 Assessment of Housing Needs, Allocs. & Trans. A 0299 Service Support Costs Housing Assessment, Allocation and Transfer A 0301 Debt Management & Rent Assessment A 0399 Service Support Costs Housing Rent and Tenant Purchase Administration A 0401 Housing Estate Management A 0402 Tenancy Management A 0403 Social and Community Housing Service A 0499 Service Support Costs Housing Community Development Support € 1, 567, 72 5 60, 13 8 168, 54 9 - 734, 71 5 2, 531, 12 7 57, 50 0 357, 91 5 415, 41 5 176, 34 4 298, 17 9 474, 52 3 55, 00 0 9, 40 0 10, 00 0 176, 96 9 251, 36 9 Table F Division A - HOUSING AND BUILDING - Pg 2 Expenditure by Service and Sub-Service Code A 0501 Homeless Grants Other Bodies A 0502 Homeless Service A 0599 Service Support Costs Administration of Homeless Service A 0601 Technical and Administrative Support A 0602 Loan Charges A 0699 Service Support Costs Support to Housing Capital Prog. A 0701 RAS Operations A 0702 Long Term Leasing A 0799 RAS Service Support Costs RAS Programme Adopted by Council € 186, 00 0 111, 74 4 22, 84 4 320, 58 8 85, 74 8 1, 535, 90 6 341, 93 7 1, 963, 59 1 2, 765, 50 0 400, 54 0 316, 39 8 3, 482, 43 8

Table F Division A - HOUSING AND BUILDING - Pg 3 Expenditure by Service and Sub-Service A 0801 Loan Interest and Other Charges A 0802 Debt Management Housing Loans A 0899 Service Support Costs Housing Loans Division A - HOUSING AND BUILDING - Table F - Income Adopted by Council € 334, 47 6 - 198, 40 0 532, 87 6 1, 200, 00 0 A 0901 Disabled Persons Grants A 0902 Loan Charges DPG/ERG A 0903 Essential Repair Grants A 0904 Other Housing Grant Payments 14, 000 A 0905 Mobility Aids Housing Grants - A 0999 Service Support Costs 16, 15 0 - 184, 01 4 Income by Source € Government Grants & Subsidies Environment, Community and Local Government Total Grants & Subsidies (a) 6, 013, 469 Income from Goods and Services Rents from houses 4, 739, 200 Housing Loans Interest & Charges 222, 054 91, 753 3, 500 Housing Grants Superannuation Agency Services & Repayable Works A 1101 Agency & Recoupable Service - Local Authority Contributions A 1199 - Other income Service Support Costs Agency & Recoupable Services - Total Goods and Services (b) Service Division A Total - Housing & Building 11, 386, 091 6, 013, 469 1, 414, 16 4 Adopted by Council Total Income c=(a+b) - 245, 180 5, 301, 687 11, 315, 156

ØTable A Cont’d Financed by Other Income/Credit Balances Provision for Credit Balance Local Government Fund /General Purpose Grant/LPT 16, 228, 046 Pension Related Deduction 1, 108, 226 + / - Base Year Adjustment - Dissolved Rating Authorities -202, 862 Sub - Total (B) 17, 133, 410 Net Expenditure to be Financied by Commercial Rates 13, 565, 244 Amount of Rates to be Levied C=(A-B) 13, 565, 244 Net Effective Valuation D 228, 886 General Annual Rate on Valuation C/D 2015 59. 27 General Annual Rate on Valuation - 2014 % Increase in ARV Commercial Property with a Ratable Valuation of € 100 - 2015 Rates - - 59. 27 0% € 100 x 59. 27 = € 5, 927

ØTable C Base Year Adjustment 2015 - Former Town Councils Revised Table C B A C D E F Base Year Adjustment Net Effective Valuation Value of Base Year Adjustment Effective ARV 2015 Annual Rate on Valuation 2014 A -B C x D € € € Name of County ABC County Council Annual Rate on Valuation 2015 59. 27 Name of Town 59. 27 123, 304 - 59. 27 Town Council - D 57. 68 59. 27 - 1. 59 58, 624 - 93, 212 57. 68 Town Council - E 57. 13 59. 27 - 2. 14 39, 500 - 84, 530 57. 13 Town Council - F 55. 90 59. 27 - 3. 37 7, 458 - 25, 120 55. 90 TOTAL - 202, 862 - 7. 10 228, 886 Commercial Property in former town council area D with Ratable Valuation of € 100 - 2015 Rates 2015 Valuation € 100 x 59. 27 € 5, 927 BYA Credit € 100 x -1. 59 -€ 159 2015 Rates Due € 5, 768

Ø Ø Ø Annual Financial Statements (AFS) - End")

4. Annual Financial Statement (AFS) Ø Ø Ø Annual Financial Statements (AFS) - End of Year Accounts AFS – Actual Income & Expenditure & Balance Sheet (Details of all Fixed Assets owned by the Local Authority) Annual AFS are audited by Local Government Auditor deals with: • Verification of accounts as shown in AFS • Prevention/Detection of fraud/error • Value for money AFS & Auditors Reports are submitted to Council Chief Executive & Audit Committee for consideration and have authority to seek a meeting with Local Government Auditor. AFS & Auditors Reports are submitted to members for approval and Local Government Auditor has authority to seek a meeting with the elected members to discuss if they so wish.

5. Ø Schedule of Municipal District Works – January 2015 Ø Following the adoption of the budget, a schedule of proposed works in each municipal district shall be prepared under the direction of the Chief Executive. Ø The schedule of municipal district works shall be considered by the municipal district members concerned and be adopted by resolution, with or without amendment.

AILG - Local Government Finance Training Module AILG Training Seminar for Elected Members Local Authority Finance & Budgets Questions? ?

- Slides: 19