AGN International World Congress 2009 Tuesday October 20

AGN International World Congress 2009 Tuesday, October 20, 2009 9: 00 am – 12: 30 pm Chicago, Illinois

Presented by: Allan D. Koltin, CPA President & CEO PDI Global, Inc. Chicago, Illinois

Industry Update

How Fast the Pendulum Swung! Factor 2007 2008 Mass layoffs at the Big 4, targeted layoffs at other firms 2009 Human Capital If only we could find the people. Profitability We’d better Many, many CPA It seemed like brace for a tough firms realized “just 2008. record profits in yesterday…” 2008. Growth The last 5 years have been the best for growth since I’ve been in the profession. “The phones have stopped ringing – we need to get our partners back on the street. ” More résumés? Did we just go full circle on the “commodity thing? ”

What are Firms doing to Cope with Today’s Recession? • Multiple rounds of staff layoffs • No salary increases • Across-the-board salary reductions (possibly with additional paid time off) • Termination of partners • Major cost-cutting initiatives • Mandatory time off (PTO) during the summer months • Pushing out start dates of new recruits and/or reducing starting salaries/rescinding offers • Better WIP/AR management/work stoppage and payment plans

Average Net Revenue Growth for the Nation’s Largest Firms

The 2009 IPA Top 100 By The Numbers… (qualities of firms in the top quartile) • • More aggressive on projected rate increases (4. 7% v. 4. 0%) Higher budgets per professional for training ($2, 776 v. $2, 330) Higher realization rates (93% v. 88%) Better utilization of the partner group (more charge hours – 1, 124 v. 1, 056; same work hours – 2, 380; greater charge hour percentage - 47% v. 45%) Better handle on personnel costs (41. 3% of net fees v. 45. 8%) Consistently higher billing rates at all levels Greater utilization of administrative staff (one administrative staff for every 4. 9 professionals v. one per 3. 6 professionals)

The 2009 IPA Top 100 By The Numbers… (qualities of firms in the top quartile) Which leads to: • • • Higher net income per partner ($548, 000 v. $439, 610) Higher net fees per partner ($1. 75 million v. $1. 62 million) Higher net fees per charge hour ($188 v. $169) Higher net fees per employee ($209, 000 v. $180, 660) Greater profit margin (31. 6% v. 29. 1%) Average compensation for all partners ($612, 000 v. $452, 000)

Top Challenges Facing the Top 100 Firms Top Firm Challenges Top Client Challenges • Acquiring New Business • Preserving Existing Clients • Hiring Quality Staff • Economy / Recession • Collections • Economy • Cash Flow / Collections • Increased Regulatory Compliance • Health Care Costs • Credit / Financing

The Big Four and the “Middle Market”

What’s Happening With the Top 100 Firms • • Grant Thornton BDO Seidman RSM Mc. Gladrey/Mc. Gladrey & Pullen Crowe/Horwath CBIZ/MHM Smart/LECG Virchow Krause/Baker Tilly Mega Regionals (J. H. Cohn, Amper, Marcum, Parente and Beard, UHY Advisors, Weiser, etc. ) • Large Locals, etc.

The 7 Mega. Trends of Change • • Client sophistication Governance Connectivity Transparency Modularization Globalization Commoditization Source: Ross Dawson, CEO, Advanced Human Technologies

")

2009 Rosenberg MAP Survey Multi-Partner Firms Over $10 M in Net Fees (95 Firms) $2 -$10 M in Net Fees (204 Firms) Under $2 M in Net Fees (37 Firms) 435, 247 332, 934 212, 570 Fees per Partner 1, 536, 657 1, 066, 447 540, 011 Fees per Person 162, 974 151, 727 134, 662 Fee Growth – ’ 08 (incl mergers) 9. 0% 7. 8% 6. 9% Est. Fee Growth – ’ 09 (excl mergers) 3. 9% 2. 7% 3. 0% Realization 82. 5% 87. 1% 87. 9% 321 256 206 Average Partner Charge Hours 1, 093 1, 189 1, 271 Average Staff Charge Hours 1, 483 1, 524 1, 573 Income per Partner Average Partner Billing Rate Source: The Rosenberg Associates and The Growth Partnership Based on 2008 Numbers

")

2009 Rosenberg MAP Survey Multi-Partner Firms Over $10 M in Net Fees (95 Firms) $2 -$10 M in Net Fees (204 Firms) Under $2 M in Net Fees (37 Firms) 6. 4 4. 8 2. 4 Prostaff Turnover 16. 7% 13. 8% 11. 2% Utilization % 50. 6% 53. 5% 55. 2% Billing Rate Multiple 4. 2 4. 0 3. 9 Months of A/R + WIP 3. 1 3. 4 3. 2 Overall Net Firm Billing Rate 144. 26 128. 58 111. 51 Salaries as % of Fees 46. 8% 42. 7% 36. 2% % of Firms Offering Investment Advisory Services 53. 7% 36. 3% 35. 1% Staff to Partner Ratio Source: The Rosenberg Associates and The Growth Partnership Based on 2008 Numbers

")

2009 Rosenberg MAP Survey Multi-Partner Firms Over $10 M in Net Fees (95 Firms) $2 -$10 M in Net Fees (204 Firms) Under $2 M in Net Fees (37 Firms) Written Performance Evals for Partners 56. 8% 27. 6% 10. 8% Upward Partner Evals by the Staff 46. 3% 32. 4% 18. 9% Typical Buy-in for New Partner 113, 167 136, 154 110, 717 Male/Female Staff Breakdown 45%/55% 39%/61% 33%/67% Percentage of Female Partners 15. 8% 14. 1% 11. 9% Percentage Casual Dress all the Time 76. 6% 66. 5% 54. 1% 50. 7 51. 4 52. 7 Percentage of Partners Over Age 50 54. 0% 59. 5% 58. 5% Average Valuation of Goodwill 76. 6% 79. 6% 83. 3% Average Age of Partners Source: The Rosenberg Associates and The Growth Partnership Based on 2008 Numbers

Firm Challenges/Opportunities

The Year’s Most Common Question? Door #1 Door #2 Door #3 Ground Hog Day Major Reconstuctive Surgery Let’s Merge Up into Someone Else’s Playbook No Pain – No Gain Will look better, but at what cost? Interestingly, the results from doors 2 & 3 are the same

")

Succession Planning Challenges Cruisers v. Dynamos Types of Services (Type 1 v. Type 2) Market Share/Desire to Expand Geographically Relationship v. Service-based Partner Future Survival of the Firm Size of Firm Leadership Talent First v. Multi. Generation Firm Rainmaker “Lite”

The Critical Ingredients of a Great Firm

Resolve the Corporate Culture Question Source: Journal of Accountancy, April 2007

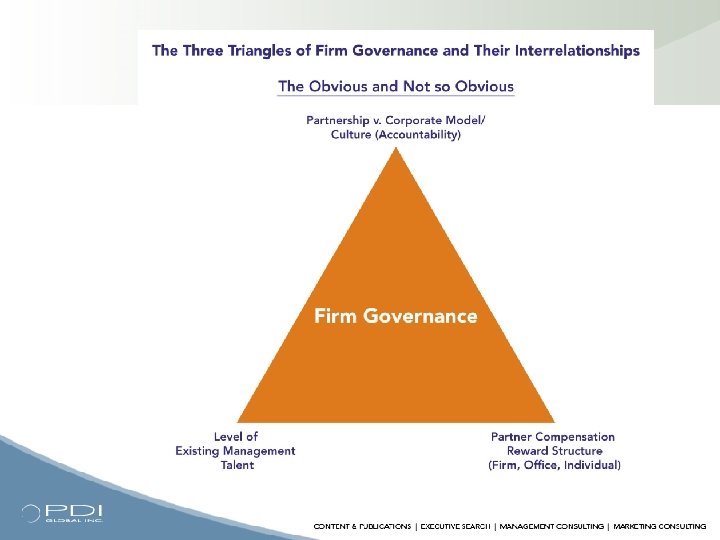

How Much Time Do You Spend In These Areas? Leadership Management Administration CEO/ COO $$$ $$ $ Executive Committee $$$ $$ $ Dept. Heads/PICs $$$ $$ $ v. What value do you place on each of these areas? v. How hard do you want to “push the gas pedal? ” v. What kind of management talent do you really have?

? 1) What professional characteristics would you")

Who Will Be Your Firm’s Future MP (leader)? 1) What professional characteristics would you want to see in the next MP? 2) What personal characteristics would you want to see in the next MP? 3) As you reflect on the biggest challenges facing the firm over the next 5 years, what are they? 4) How should the MP’s performance be measured? 5) Do you envision the structure of the MP position potentially changing in any way? 6) Would this person be interested, have the backing of the other partners and give up their workload to make this position successful?

Managing Partner Position • Set and influence the strategic vision/ direction of the firm • Lead the firm’s 1 - and 5 -year targets for growth and profitability • Create an environment that positions firm as the “Employer of Choice Firm” throughout the Region • Help coach and monitor the PICs’ performance in a manner consistent with the “One Firm” concept

Managing Partner Position - cont • Lead the Executive Committee and provide clarity and accountability for their roles • Provide counsel and cohesion to the firm’s management team • Rally the partners to greater performance and provide for a culture of “connectivity” • Be a leader in the communities that the firm services

Role of Executive Committee • • Five-year strategic plan “Heavy lifting” – major issues effecting firm Mergers and acquisitions Hiring of lateral partners to the firm Litigation and business risk Advisor to the Managing Partner Ideas for new product and service lines Ambassador to carry the “Firm” message to other partners and associates

Partner-in-Charge Position • PIC would manage region in the following areas: § § § § § Growth – organic, mergers and lateral hires Individual partner performance People issues – recruitment & retention of talent Development and implementation of regional growth and profit strategies Resolve conflicts and issues in region Determine partner compensation within region Determine appropriate staffing and scheduling issues Promote the “One Firm” concept Integrate Firm specialties and functional areas of management into regional strategies

Should the Heads of Tax and A&A be “true CEOs” or Simply “Department Administrators”? Tax Department Leader – Job Description 1) Empowered with overall responsibility to manage growth, profitability and overall resources of the Tax Department. 2) Recruitment of new tax talent to the firm. 3) Mentoring and development of existing tax staff and partners. 4) Responsible for leading new product/service department ideas for the Tax Department. 5) Oversight of tax training and technical issues as they relate to members of the Tax Department. 6) Oversight of utilization scheduling and realization of Tax Department members. 7) Establishment of tax members’ billing rates, as well as helping establish fees on larger tax engagements. 8) Meets monthly (or quarterly) with tax partners and managers to coach and counsel them on individual performance. 9) Responsible for overall client satisfaction (both internal and external clients of the firm). 10) Helps promote the cross selling of tax services firm-wide, and also promotes cross selling of non-tax services within the Tax Department.

Is Your Firm a Book-of-Business Firm? Originating Partner CLIENT Relationship Partner Service Partner

Ten Passions for Engagement Profitability Engagement Budget START FINISH Engagement Planning Staffing & Scheduling Client Acceptance The Client Satisfaction Collections Engagement Management/ Utilization Relationship Management Billing Surprises/ Change Orders/ Revisions of Completion Date

Top Reasons for Low Realization/Utilization • Billing rates not set high enough • Poor scheduling and job control system • Wrong people on the job (i. e. no industry expertise) • Continual staff turnover • Lack of standardization • No adherence to Firm policies (daily time reporting) • Staff “eat” time • Not good with change orders • Partners don’t believe they’re worth their rate/scared to bill • Not accountable to someone “upstairs” • Compensation program doesn’t penalize low realization • Lack of communication between offices • Clients change schedules last minute and leave us “hanging” • Too much left in WIP/ inefficient staff

Brief Comments and Observations • No “one right way” to manage a firm • The answer appears to rest somewhat on the skills, wants and desires of the managing partner • Still the exception: § § The use of high-level, non-CPA management The use of co-managing partners Firms that are run by committee The use of independent Directors on CPA firm Boards

Brief Comments and Observations • Single-office firms have significantly fewer “headaches” and conflict in their world! • Some firms look one way on paper, but… § Are run completely different (The Wizard of Oz!) § Should be run completely different! • Mixed bag on various leadership selection processes: § § How is Managing Partner/CEO determined? How is the Board of Directors selected? How are the above positions structured (roles and responsibilities)? What is the length of term (if any) of the above positions?

Partner Challenges/Opportunities

Various Partnership Structures in Today’s CPA Firm • One tier § equity only • Two tiers § equity, income • Three tiers § equity, limited equity, income • Four tiers § equity, limited equity, income, principal • Five tiers § equity, limited equity, income, principal, retired • Six tiers § equity, limited equity, income, principal, retired, contract • Seven tiers § equity, limited equity, income, principal, retired, contract, special* *has not ‘officially’ retired but, based on performance, one would think they ought to!

What is the Difference Between Income and Equity Partners? • • Greater Compensation? Book of Business? Voting Rights? Capital Contribution? Deferred Compensation/Retirement Benefits? More Accountability? Limited Liability - Indemnification from Lawsuits?

Background on Lateral and Merged-in Partners • More activity in last 5 years than in last 20 years • National firm partners have successfully integrated into local, regional and middle-market national firms • Many merged-in partners have thrived and assumed leadership roles in new firms • Lateral and/or merged-in partners have become the #1 growth strategy of many Top 100 CPA firms!

Why Would a Firm Hire a Lateral and/or Merged-in Partner? • • • Rainmaking skills Leadership/management abilities Can assume someone else’s book of business Can help to leverage another partner’s book of business Has a unique or specialty expertise that the firm doesn’t have or wants to expand upon

Why Would a Firm Hire a Lateral and/or Merged-in Partner? • Firm is trying to fill in age or experience gaps in certain places • Improving holes in diversity (i. e. women partners) • Ability to take partner book and cross sell other services • Ability to better service lateral or merged-in partner’s book of business

Tricky Issues with Lateral and Merged-in Partners • Do they have the same client service mentality that we do (high leverage v. hands on)? • Is their billing philosophy and value proposition similar to ours? • Do they treat staff the same way we do (highly respected v. replaceable, fungible goods)?

Tricky Issues with Lateral and Merged-in Partners • When it comes to partner compensation, are we philosophically aligned (what comes first – the firm, the office or the individual’s performance)? • Do we measure performance the same way (strict formula v. a mixture of qualitative and quantitative goals)? • Was “accountability” and one’s “willingness to be managed” the same in the prior firm as it is in the current firm?

Partner Compensation

The Journey Called “Partner Compensation” Unified Firm* Strategy/ Vision Individual Partner Goals Firm Governance/ Accountability Performance. Based Partner Compensation *Includes Department, Office and Industry Team Goals

The good news about a lot of firms’ growth strategies is that… “Average partner compensation will increase, but for the average partner, it will probably stay the same. ” Daryl Ritchie, CEO of Meyers Norris Penny LLP

Partner Compensation OLD SCHOOL NEW SCHOOL • What is your book of business? • How much new business did you bring in? • How many billable hours did you have? • Who did you recruit to the firm last year? • On the upward evaluation, how many people identified you as the reason they are with the firm? • How many current and future partners would identify you as their “sponsor”?

What is the Most Valuable Use of Time for You and Your Firm? Billable Hours __ Technical Knowledge __ Book of Business __ Firm Management __ Business Origination __ Human Capital __ Please rate from highest to lowest

ØAgree on worth ØDoesn’t always make sense ØValues can change annually ØOccasionally have to over pay ØIndividualized off-season training ØIndividual goals & measurements differ

Common Partner Compensation Issues • Too formulatized – “one size doesn’t fit all” • Doesn’t cause partners to exploit their strengths • Doesn’t drive partner performance that is consistent with the firm’s strategic goals and values • The current program isn’t transparent enough to communicate “why we received what we received. ”

Common Partner Compensation Issues - continued • No partner goal setting up front • No ongoing evaluations, feedback, coaching and accountability • More people need to drive partner performance and, hence, compensation • It would be great if we could get a “report card” highlighting strengths and deficiencies

Selected Observations & Concerns • CPA firm life cycles – second generation challenges • Too many partners for the current revenue base (based on comparatives of other top performing firms of similar size). • First firm I’ve seen where no one has over 1, 000 billable hours annually (way too many non-billable hours!). • We have underperforming partners who need to be counseled on how to improve (or potentially leave the firm). • “Good to great” Syndrome. Partners are doing “some” of the right things “some” of the time. • The firm appears to be “rainmaker-lite” – serious concerns about commitment to growth and existing talent level to “drive” organic growth engine.

Selected Observations & Concerns • Partners aren’t performing in a “highest and best use of time” principle. • Individual partner goal setting process needs improvement: § The firm and partners need to better assess where partners can help the firm § Partners are involved in too many tasks, which dilutes their overall effectiveness § Partners need to determine if they are a rainmaker, service, or relationship partner and focus on fewer, better defined goals § We need to make sure that partner performance specifically rewards partner success

Selected Observations & Concerns • Partner Compensation Program – Structure & Process § Too much of the partner compensation pool is allocated as salary/draw and not enough is left over for the incentive portion § We need to create an incentive or bonus program that rewards partners who achieve and exceed their individual goals § Lack of clarity on how partners can obtain (or lose) additional units. Some partners suggest we follow the “good harmony” approach to allocating units § The firm should move from open to a partially-closed system of compensation. Approximately 90% of Top 100 CPA firms use this approach as a “best practice. ” Partners need to forget about “relative” partner income and focus more on what ‘they’ can do to improve their own performance (and value for the firm)

Mergers & Acquisitions

a big year for")

2008 – 2009 Annual M&A Update • 2008 was (surprisingly) a big year for M&A • Some of the biggest deals actually were the ones that didn’t happen! • Some deals in 2008 saw the return of “cold hard cash” • Despite the present economy, 2009 will probably have more mergers than 2008 • Bottom Line! Mergers (if done for the right reasons) really do work and have been a great growth strategy for expanding the firm’s talent, resources and geography.

Firms don’t merge – people do! Remember")

Some Take-Aways from 2008 M&A Activity 1) Firms don’t merge – people do! Remember to “drill down” to everyone’s personal agendas 2) One size doesn’t fit all (cash for some, equity for others, a job for some!) 3) Pick one! a) Fact: The more people involved in the merger discussion, the greater chances of it happening. b) Fiction: The more people involved in the merger discussion, the lesser the chance of it happening. c) See #1 (Clue – Do whatever it takes to “get the train running”!)

Be careful what you wish for. Examples:")

Some Take-Aways from 2008 M&A Activity 4) Be careful what you wish for. Examples: v Corporate v. Entrepreneurial Models v “Troops on the ground” v. Flagship status v How will life be different (if at all) on Monday morning? 5) Don’t sweat the small stuff!

How is the “Multiple” Determined?

•")

Types of Retirement Plans* • Multiple of salary • Ownership percentage (times revenue) • Agreed upon fixed price *Also needs to address length of payout, vesting, payment restrictions, non-compete provisions, etc.

Some of My Involvement in the 2008 -2009 M&A Arena Acquirer Fee Volume Acquiree CBIZ $500 M Mahoney Cohen $55 M CBIZ $500 M Tofias $40 M BKD $322 M The Hanke Group $12 M BKD $322 M Smith Turner & Reeves $5 M J. H. Cohn $215 M Good Swartz Brown & Berns $22 M Marcum $182 M Margolis LLP $10. 5 M Cherry Bekaert & Holland $77 M Massey + Pittman $2 M Amper Politziner & Mattia $72 M Goldenberg Rosenthal $24 M

Some Figures Worth Sharing 2006 – 2008 v 50 Potential Mergers v 42 Never made it to the alter v 8 Got married v 1 Got divorced

Some Results Worth Sharing v 84% of Potential Mergers Didn’t Happen v 16% of Potential Mergers Did Happen v Only 12. 5% of Mergers that Happened Failed! Bottom Line – Do your homework up front and don’t be afraid to ask the hard questions!

Firm Name 2) Governance/Accountability 3)")

Top 10 Reasons Why Potential Mergers Didn’t Happen 1) Firm Name 2) Governance/Accountability 3) Ego 4) Culture, culture! 5) Too many people can say “no”. 6) The “myths” are stronger than the “reality” 7) Worried about perceived risk 8) Compensation programs too dissimilar 9) Other firm did a better job of selling “their franchise” 10) Financial terms

Why do Firms Merge? * • Fix a problem • Expand into new markets • Geographic expansion of services • Leadership • Country v. Country Club • Improve profitability • Expand upon existing specialty • Service larger clients • Unfunded retirement obligations • Succession planning issues • No longer having ‘fun’ • To better service clients • Upgrade firm weaknesses • Offer clients more products and services OR Simply to Cash Out! *Often times there are multiple reasons (some of which are hidden)

Who will still be a")

The M&A Puzzle – 10 Things to Consider 1) Who will still be a partner after the merger? • • • Equity Income Retired or Contract 2) What about our present lease? 3) Who will lead the new office? 4) What will our compensation look like after the sale/how will it be determined? • Formula v. subjective

How will they value our")

The M&A Puzzle – 10 Things to Consider 5) How will they value our firm? • • • Deferred compensation program Cash v. stock Length and structure of financial terms Contingency/”Clawbacks”/Guarantees Who keeps the balance sheet/what are the capital requirements? 6) Who (if anyone) might not be here after the merger? 7) Are we culturally compatible?

Do we have compatible client")

The M&A Puzzle – 10 Things to Consider 8) Do we have compatible client bases? 9) Are we getting married or just “living together” – Honeymoon Clause 10) Who do we tell and when? !

Memorable Comments from The Advisory Board M&A Forum Successful mergers can be summed up in one phrase – compatible cultures! (Tim Christen) Forget about cost savings as a reason to do a merger. (Tom Marino) You should evaluate a merger based on three factors: what’s best for the clients, what’s best for the staff and, lastly, what’s best for the partners. (Steve Levin) “Mix and match” staff early to eliminate the “we and they”. (Bob Gibble) Gut counts a lot – do they pass “the beer” test? (Carl George) How will the merged-in firm use our platform to make more money? (Tom Marino) Don’t underestimate the importance of systems integration – it’s significant. (Greg Barber)

Memorable Comments from The Advisory Board M&A Forum The best merger we could do in today’s market would be with a firm of 50 staff and no clients. (Jim Smart) If a practice is in trouble or the culture is significantly different, we’ll take a pass. (Cono Fusco) It’s better to do psychological testing before the merger than looking silly after the merger. (Ken Baggett) Make sure you can answer, “How will the merger improve client service? ” (Tony Argiz) Cross-pollinate people on Day One. (Howard Allenberg) Don’t let the lawyers have too much input into the business deal or else they’ll screw it up. (Eddie Sams) I simply picked up the phone and asked to speak with the CEO. (Bob Glaser)

Memorable Comments from The Advisory Board M&A Forum The day the merger closes is the day the real work begins. (Alan Litwin) Communicate, communicate and then communicate some more. (Steve Levin) Bigger isn’t Better – Better is better! (Tim Christen) Don’t underestimate the value of one-on-one, ‘get to know you’ meetings before the merger. (Tom Marino) If you’re merging with a firm in a new market, make sure there’s a competent leader to rally the troops. (Rick Stein) You will go down before you go up. (Greg Barber) Was he negotiating in good faith or was he negotiating for himself? (Carl George) It is better to acknowledge a failed merger than to live in denial. (Hugh Parker)

Developing Future Leaders

Why Does Talent go Elsewhere*? • • • Work / life balance No future No connection “A partner (or manager) is a jerk!” Money *Business Week Article – Highest Pay, Quickest Advancement and Best Training

Where Oh Where Have All The Future Leaders Gone? • What is your leadership quotient? On a scale of one to ten (with 10 being the highest) how would you rate yourself: • A risk taker ___ • One who dares to be different ___ • Ability to make the tough calls ___ • A schizophrenic communicator ___ • Self-confident ___ • Gets results through others ___ • Great motivator ___ • Would rather work “on” the business versus “in” the business ___ • Trusted by others in the firm ___ • Respected by others in the firm ___ Total Score: ___

Why the Confusion at Firms on How to Become a Partner? • Even though there may be a document that spells out how to become a partner, keep in mind: § Senior Manager A and B probably have different goals and, hence, paths for what it would take to become a partner § These Senior Managers’ mentors are probably different and giving them different input and advice along the way § Sometimes the Senior Managers may not want to hear what they’re being told (things they need to improve upon) § Making partner is like being inducted into the Hall of Fame – you may qualify, but it may not be this year!

5 Facts I Wish Someone Had Told Me About Clients #1 The Wine Bottle Concept

5 Facts I Wish Someone Had Told Me About Clients #2 People don’t care how much you know… Until they know how much you care!

5 Facts I Wish Someone Had Told Me About Clients #3 Clients don’t like… SURPRISES!

5 Facts I Wish Someone Had Told Me About Clients #4 The Business Goals are important, but… “If we were meeting here, three years from today, and you were looking back over those three years - back to today what has to have happened over those three years, both personally and professionally, for you to feel happy with your progress? ” Dan Sullivan

5 Facts I Wish Someone Had Told Me About Clients #5 The Client’s Imaginary Report Card The client can’t really differentiate between an A- and B+ work product (nor do they care) • Reliability § “Can your clients really judge the quality of the work product? ” • Assurance § You’re in good hands with “All-State” • Tangibles § Why appearances and messy office are important! • Responsiveness § Who calls who? You, or the client? • Empathy § Fortunately, we’re not as bad as the doctors.

5 Things I Will Do To Be Worth More To My Clients Next Year Investment v. Income Time METRIC YOU Billable Time Your Billable Time Total Working Hours Your Total Working Hours

5 Things I Will Do To Be Worth More To My Clients Next Year Income Statement v. The Balance Sheet What did I earn last year? v. How much did my balance sheet grow last year?

5 Things I Will Do To Be Worth More To My Clients Next Year Do you service Customers, Clients or Cheerleaders? • • • Suspect Prospect Customer or Purchaser Client Cheerleader 1 List clients and referral sources that come to mind in each of the above levels. 2 What is your game plan to convert each group to the next level? 3 For each cheerleader that you identified above, how many referrals have you received from that person in the past year?

5 Things I Will Do To Be Worth More To My Clients Next Year Criteria for “Famous Persons” Recognition 1) Serves at least 10 significant clients in the industry, or have completed at least 10 significant engagements in the technical area where “fame” is claimed. 2) Involved in their industry’s trade association and have frequently published, or presented at trade association meetings. 3) To the extent the industry is served by specialized credit, legal and other communities, the individual should be well known and referenceable among those communities. 4) Competitors in the industry or technical area should know the individual.

25 Ways and Reasons to Keep in Touch • • • • Phone Calls Letters Introductions Clip and send Newsletters Items of interest News Useful Information Entertaining Gifts Cards Faxes E-mail • • • Meetings Coffee Breakfast Lunch Cocktails Events Industry meetings/ conferences Offer continuing education programs Co-sponsor an event Co-present at a seminar Pass along an opportunity Pass along an idea

The Networking Process Thank You Letter Legal Update Letter With Attachment Phone Contact Send Newsletter Lunch Date Holiday Gift/Card Letter with Attachment Legal Update Lunch Date Training Workshop Send Newsletter Letter with Attachment Promo/ Information Piece Referral Sources Letter with Attachment Lunch Date Promo/ Information Piece Follow-up Letter Send Newsletter Seminar Invitation Promo/ Information Piece Inactive Clients Letter with Attachment Send Newsletter Promo/ Information Piece Follow-up Letter Send Newsletter Letter with Attachment Promo/ Information Piece Active Clients Target Clients

Why Clients Change Firms Didn’t spend enough time Wasn’t friendly Didn’t answer questions completely Wasn’t knowledgeable and competent Didn’t explain problems simply Wasn’t up to date Didn’t treat you with respect Wasn’t always available when needed Fees weren’t reasonable 51% 42% 40% 37% 30% 29% 27% 25%

Working the Wheel • The Client’s Management Team § § § § Banker Corporate attorney Estate attorney Insurance agent Commercial/industrial leasing agent Other consultants Financial planners/wealth advisors

The Move to Own the Client and Make it Difficult for them to Leave A recent survey of clients that receive services from their financial services provider shows. . . • Number of Services Used § 1 service § 2 services § 3 services § 4 services § 5 services • Probable Retention Rate § 12% § 24% § 63% § 81% § 98% Mandatory shift – from “renting” clients to actually “owning” them.

Defining Your ‘Core’ – Getting Out of Your Comfort Zone and Defining Your Unique Sales Strategy

Me at the University of Wisconsin* They taught")

What They Taught (and didn’t teach!) Me at the University of Wisconsin* They taught me: § Accounting, auditing and tax What they didn’t teach me: § § § How to build relationships How to communicate How to take risk How to make money How to manage the clock How to play with passion *Recent CEO Survey of Fortune 500 Companies

What They Didn’t Teach Me How to build long-lasting relationships: § With clients, staff and referral sources § The Balance Sheet v. the Income Statement § How to move ‘customers’ to ‘clients’ and move ‘clients’ to ‘cheerleaders’

What They Didn’t Teach Me How to communicate: § § § § Active listening Ability to read people Positive energy Take criticism Constructive confrontation Ability to negotiate Ability to compromise Ability to “sell” your ideas

What They Didn’t Teach Me How to take risk: § § § Create work for others Develop new niches and service areas Willingness to incur debt/borrow from the bank Don’t “climb down” the corporate ladder It’s okay to be a little paranoid and insecure!

What They Didn’t Teach Me How to make money: § “Let’s just pretend for a moment that we’re in business to make money!” § Profitability is the lifeblood of the firm § You only get to play the game called “business” once!

What They Didn’t Teach Me How to manage the clock: § § § Use of investment time Disciplined goals Ability to think quick on your feet Ability to manage stress Ability to execute “No matter what” attitude!

What They Didn’t Teach Me How to play with passion: § § § § How to become famous at something How to believe you’re worth your billing rate Wanting it more than the next guy Willingness to play injured Push yourself when no one is looking It’s not always fair It’s not how you celebrate the highs, it’s how you bounce back from the lows

Thank you for attending To Contact Allan: 455 N. Cityfront Plaza Drive, Suite 1000 Chicago, IL 60611 312. 245. 1930 (phone) 312. 245. 1935 (fax) akoltin@pdiglobal. com

- Slides: 107