Agenda Introduction of Capital The Evolution of Basel

Agenda Introduction of Capital The Evolution of Basel Accord Pillar I – Credit Risk – Standardized Approach Pillar I – Credit Risk – IRB Approach Capital Requirements for Other FIs Pillar I , Pillar II and Comments

Agenda Introduction of Capital The Evolution of Basel Accord Pillar I – Credit Risk – Standardized Approach Pillar I – Credit Risk – IRB Approach Capital Requirements for Other FIs Pillar I , Pillar II and Comments

Function of capital l l To absorb unanticipated losses with enough margin to inspire confidence and enable the FI to continue as a going concern To protect uninsured depositors, bondholders, and creditors in the event of insolvency and liquidation To protect FI insurance funds and taxpayers To protect the FI owners against increase in insurance premiums To fund the branch and other real investments necessary to provide financial services

= market value of assets –market value of")

Capital Economist’s definition Capital (net worth) = market value of assets –market value of liabilities Market value accounting Accountant’s defined Capital = book value of assets – market value of liabilities Book value accounting

credit risk effect on market value TABLE 20 -1 Assets Long-term securities Long-term loans $80 20 $100 Liabilities (in millions of dollars) Liabilities $90 Net worth 10 $100 TABLE 20 -2 Assets Long-term securities Long-term loans $80 12 $92 Liabilities (in millions of dollars) Liabilities $90 Net worth 2 $ 92 1. The loss of asset value is charged against the equity owners’ capital or net worth 2. The liability holders (depositors) are fully protected in that the total market value of their claims is still 90 3. Because debt holders legally are senior claimants and equity holders are junior claimants to an FI’s assets

Interest risk effect on market value TABLE 20 -1 Assets Long-term securities Long-term loans Table 20 -24 Assets Long-term securities Long-term loans $80 20 $100 $75 17 $ 92 l l Liabilities (in millions of dollars) Liabilities (short-term , floating- $90 rate deposits) Net worth 10 $100 Liabilities (short-term , floating- $90 rate deposits) Net worth 2 $92 Rising interest rates reduce the market value of the FI’s long-term fixed-income securities and loans Because all deposit liabilities are assumed to be short-term floating-rate deposits, their market values are unchanged at $90 the net worth loss from 10 to 2 Only if the fall in market value of assets exceeds 10 are the liability holders adversely affected

conclusion Market valuation of their balance sheet produces an economically accurate picture of the net worth l As long as the owners’ capital or equity stake is adequate , or sufficiently large, liability holders are protected against insolvency risk l If an FI were closed by regulators before its economic net worth became zero , neither liability holders nor those regulators guaranteeing the claims of liability holders would stand to lose l

The book value of capital usually comprises the following four components : 1. 2. 3. 4. Par value of shares Surplus value of shares Retained earnings Loan loss reserve

the book value of capital and credit risk TABLE 20 -5 Assets Long-term securities Long-term loans TABLE 20 -6 Assets Long-term securities Long-term loans Liabilities $80 20 $ 100 Liabilities Net worth $90 10 $100 Liabilities $80 17 $ 97 Liabilities Net worth $90 7 $97 FIs have greater discretion in reflection or timing problem loan loss recognition on their balance sheets l Try to present a more favorable picture to depositors and regulators l Only pressure from regulators such as bank, thrift, or insurance examiners may force loss recognition and write downs in the values of problem assets l

the book value of capital and interest rate risk TABLE 20 -5 Assets Long-term securities Long-term loans l Liabilities $80 20 $ 100 Liabilities Net worth $90 10 $100 The rise in interest rates has no effect on the value of assets , liabilities, or the book value of equity, the balance sheet remains unchanged

support (market value) 1. It is")

Arguments against market value accounting Against (market value) support (market value) 1. It is difficult to implement 1. error resulting from the use of market valuation is less serious 2. It introduces an unnecessary degree of variability into an FI’s earnings , especially they hold loans and other assets to maturity 2. FI’s are increasingly trading, selling, and securitizing assets rather than holding them to maturity 3. FIs are less willing to accept longerterm asset exposures

Agenda Introduction of Capital The Evolution of Basel Accord Pillar I – Credit Risk – Standardized Approach Pillar I – Credit Risk – IRB Approach Capital Requirements for Other FIs Pillar I , Pillar II and Comments

Basel II Accord Pillar 1 Minimum Required Capital Credit Risk Pillar 2 Supervisory Market Risk Standardized Approach IRB Approach Pillar 3 Disclosure Operational Risk

Agenda Introduction of Capital The Evolution of Basel Accord Pillar I – Credit Risk – Standardized Approach Pillar I – Credit Risk – IRB Approach Capital Requirements for Other FIs Pillar I , Pillar II and Comments

l L=Core Capital /Total Assets Core Capital Ø Ø Ø")

Capital-Assets Ratio (Leverage Ratio) l L=Core Capital /Total Assets Core Capital Ø Ø Ø common equity(book value) qualifying cumulative perpetual preferred stock minority interests in equity accounts of consolidated subsidiaries

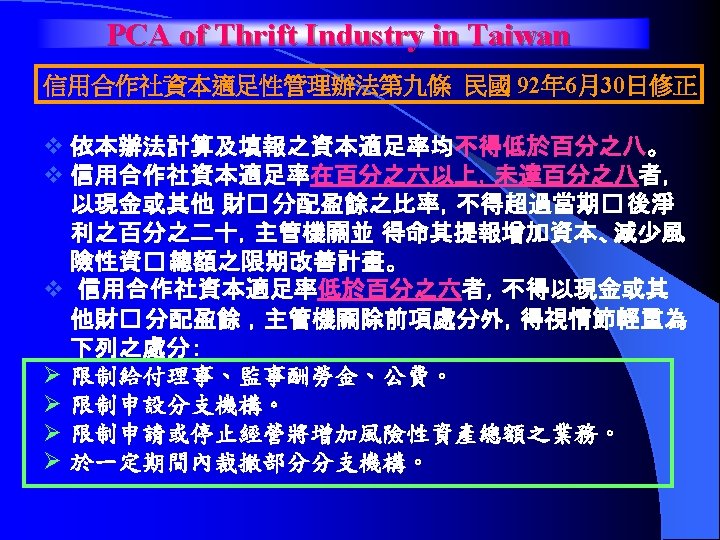

Specifications of Capital Categories for PCA Prompt Correction Action must be taken if a bank falls outside zone 1 Receivership is mandatory

PCA of FDICIA of 1991

PCA of FDICIA of 1991

Problems of using Leverage Ratio as a measure of capital adequacy l Market Value: 2% book leverage ratio could be consistent with a massive negative market value net worth l Asset Risk: fails to take into account the different credit, interest rate and other risks of the assets that comprise total assets l Off-Balance-Sheet activities

Pillar I Minimum Capital Requirement In the Commercial Banking and Thrift Industry

Minimum capital requirement l There are no change in market risk computation from Basel I to Basel II. Methods in measuring credit risk & operational risk Credit risk Operational risk Standardized Approach Basic Indicator Approach Foundation IRB Approach Standardized Approach Advanced IRB Approach Advanced Measurement Approach

Standardized & IRB Approach l Standardized Approach Basel I: Fixed Risk weight is given according to the counterparty Basel II: Fixed Risk weight is corresponding to each supervisory category and make use of external credit assessments( OECD export agencies, private rating agencies, eg Standard & Poors ). IRB Approach IRB approach substantially differs from the standardized approach in that bank’s internal assessments of key risk drivers serve as primary inputs to the capital calculation. IRB Approach is more risk-sensitive , but with much higher development cost.

Credit Risk Standardized Approach

Credit")

Risk-Based Capital Ratios l Total risk-based capital ratio= Total Capital(Tier I +Tier III-Deduction) Credit risk-adjusted assets Tier I (Core) capital ratio= Core Capital(Tier I) Credit risk-adjusted assets It has been argued that capital requirement may induce higher not lesser risk. ≧ 8% ≧ 4%

Credit Risk→Calculating Capital l Tier I capital- primary or core capital linked to a bank’s book value of equity reflecting the concept of the core capital contribution of a bank’s owners. l Tier II capital- supplementary capital broad array of secondary capital resources Tier III capital- to support market risk

Credit Risk→Calculating Capital

Credit Risk→Calculating Capital Data source for Tier III: Over View Of The Amendment To The Capital Accord To Incorporate Market Risk January 1996

Example

The Calculation of Credit-Risk Based Capital On-Balance-Sheet Assets Off-Balance-Sheet Activities Guaranty Type & Contingent contracts Derivative or Market Contracts

Credit Risk→Calculating Credit Risk-Adjusted On-Balance-Sheet Assets l The risk-adjusted value of the bank’s onbalance sheet assets(under Basel I) would be: Σ Wi. Ai where Wi = Risk Weight of the ith asset Ai = Dollar(book)Value of the ith asset on the balance sheet

Risk Categories of On-Balance-Sheet Items Under Basel I

Example

+ 0. 2*(10 m+20")

Example l Credit risk-adjusted on-balance-sheet assets =0*(8 m+13 m+60 m+50+42 m)+ 0. 2*(10 m+20 m)+ 0. 5*(34 m+308 m)+ 1. 0*(10 m+55 m+75 m+390 m+108 m+22 m) =$849 m

Risk Categories of On-Balance-Sheet Items Under Basel II

Risk Categories of On-Balance-Sheet Items Under Basel II

Risk Categories of On-Balance-Sheet Items Under Basel II Data source: Consultative Document of The New Basel Capital Accord July, 31 2003

Example

+ 0. 2*(10 m+20")

Example l Credit risk-adjusted on-balance-sheet assets =0*(8 m+13 m+60 m+50+42 m)+ 0. 2*(10 m+20 m+10 m+55 m)+ 0. 5*(34 m+308 m+75 m)+ 1. 0*(390 m+108 m+22 m)+ 1. 5*10 m =$764. 5 m

Credit Risk→Calculating Credit Risk-Adjusted Off-Balance-Sheet Assets l Off-Balance Sheet items was divided into two types→ Guaranty type contracts vs. Derivative or market contracts Credit risk-adjusted assets of OBS Guaranty Contracts = Σ Credit Equivalent Amount*Risk Weight = Σ (OBS activity i* Conversion factor*Risk weight)

Example

Example

Example Under Basel I , the appropriate risk weight in each case Under Basel, risk weight depends on the underlying counterparty to the OBS activity treatment is the same as such as a municipality, a government, or a corporation. on-balance-sheet items. .

Credit Risk→Calculating Credit Risk-Adjusted Off-Balance-Sheet Assets The credit or default risk of exchange-traded derivatives is approximately zero because when a counterparty defaults on its obligations, the exchange itself adopts the counterparty’s obligations in full. Credit risk-adjusted assets of OBS Market Contracts = Credit Equivalent Amount* Risk Weight =( Potential Exposure+Current Exposure )*Risk Weight

Credit Risk→Calculating Credit Risk-Adjusted Off-Balance-Sheet Assets The potential exposure component reflects the credit risk if the counterparty to the contract defaults in the future. l The current exposure reflects the cost of replacing a contract if the counterparty defaults today. The bank calculates this replacement cost or current exposure by replacing the rate or price initially in the contract with the current price or rate for a similar contract and recalculates all the current and future cash flows that would have been generated under current rate or prices. l

Credit Risk→Calculating Credit Risk-Adjusted Off-Balance-Sheet Assets l If replacement cost is positive, the current exposure equals replacement cost. l If replacement cost is negative, the current exposure is set to be 0.

Example FX were far more volatile than interest rate. Conversion Factor Credit Equivalent Amount Gross Potential Exposure Net Current Exposure Gross Current Exposure

Example Under Basel I, counterparties to these contracts are assumed to be low credit risk entities. Basel II assigns these Contracts a risk weight of 100%.

Calculating Risk-Based Capital Ratio

Netting l BIS allows netting of off-Balance-Sheet derivative contracts as long as the bank has a bilateral netting contract that clearly establishes a legal obligation by the counterparty to pay or receive a single net amount on the different contracts. Credit equivalent amount =Net Potential Exposure+Net Current Exposure l Net Current Exposure=Sum of all replacement cost Ø Net Potential Exposure=(0. 4*Gross potential exposure)+(0. 6*NGR*Gross potential exposure) Ø NGR=The ratio of net current exposure to gross current exposure Ø

Example l Following the preceding example Ø Net Current Exposure=$3 m-$1 m=$2 m Gross Current Exposure=$3 m+$0 m=$3 m Gross Potential Exposure=$0. 5 m+$2 m=$2. 5 m NGR = 2/3 Net Potential Exposure =(0. 4*$2. 5 m)+(0. 6*2/3*$2. 5 m)=$2 m Credit equivalent amount =$2 m+$2 m=$4 m Ø Ø Ø

Calculating Risk-Based Capital Ratio After Netting

Agenda Introduction of Capital The Evolution of Basel Accord Pillar I – Credit Risk – Standardized Approach Pillar I – Credit Risk – IRB Approach Capital Requirements for Other FIs Pillar I , Pillar II and Comments

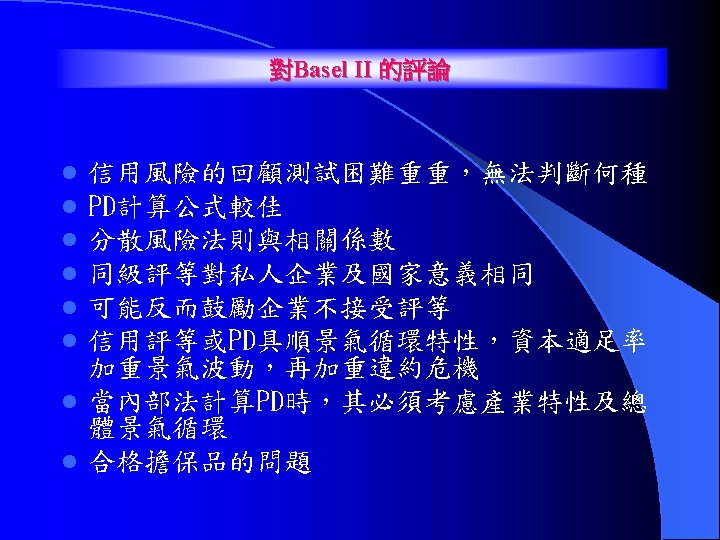

Criticisms of the Risk-Based Capital Ratio l l l Risk weights based on external credit rating agencies Portfolio aspects DI specialness Other risks Competition

Internal Ratings-Based Approach Banks that qualify for the IRB approach may rely on their own internal estimates of risk components in determining the capital requirement for a given exposure. l Advantages : l – Effective credit risk management – Potential cost reduction l Two approach – Foundation Approach – Advanced Approach

Trend of Capital Adequacy IRB Advanced Approach IRB Foundation Approach IRB Advanced Approach Standardized Approach

Internal Ratings-Based Approach Minimum requirements Classification of exposures for IRB approach Risk components Risk weight functions

Composition of minimum requirements (b) Compliance with minimum")

Minimum requirements for IRB approach (a) Composition of minimum requirements (b) Compliance with minimum requirements (c) Rating system design (d) Risk rating system operations (e) Corporate governance and oversight (f) Use of internal ratings (g) Risk quantification (h) Validation of internal estimates (i) Supervisory LGD and EAD estimates (j) Calculation of capital charges for equity exposures (k) Disclosure requirements

Classification of exposures Corporate Sovereign Bank Retail Equity

Risk components PD : probability of default LGD : loss given default EAD : the exposure at default M : effective maturity

Risk Components Estimates - Corporate Foundation Approach PD LGD Advanced Approach One-year default probability based on historical experience or credit scoring model ≥ 0. 03% Senior claims → 45% Subordinated claims → 75% Secured by collateral n Banks rely on own estimates EAD = CCF × primitive amount EAD M (CCF : credit conversion factor) Follow the standardized approach and adjust by regulation Repo-style transaction →M = 6 month Others → M = 2. 5 year n Banks use their own internal estimates of CCFs n Required to measure for each facility by regulation

Risk weight functions no • EAD × PD × LGD = 預期損失金額 default = 風險資產應計提資本 EAD reclaimed • Capital / Risk Asset = 8% default • Risk Asset. PD =風險資產應計提資本 / 8% LGD loss Risk-weighted assets = EAD × PD × LGD/8%? ?

= 0. 24")

Risk weight functions for Corporate , Sovereign , Bank Correlation (R) = 0. 24 - 0. 12 × (1 -e (-50 × PD) ) / (1 -e (-50 ) ) l Maturity adjustment (b) = (0. 08451. 0. 05898 × log (PD))2 l Capital requirement (K) = l LGD×N [(1 – R)- 0. 5 × G ( PD ) + (R / (1 - R))0. 5 × G (0. 999) ] ×(1 - 1. 5 × b)-1 × (1 + (M - 2. 5) × b ) l Risk-weighted assets (RWA) = EAD × K ÷ 8%

")

Risk weight functions for Corporate - Adjustment l For small- or medium-sized entities (SME) l Firm’s reported sales is less than € 50 million l Correlation (R) = 0. 24 - 0. 12 × (1 -e (-50 × PD) ) / (1 -e (-50 × PD) ) – 0. 04 × (1 - (S-5)/45) *S= sales (million €)

Risk weight functions for retail l. R a. Residential mortgage b. Qualifying revolving retail c. Others – a. 0. 15 – b. 0. 11 - 0. 09 × (1 -e (-50 × PD) ) / (1 -e (-50 ) ) – c. 0. 17 - 0. 15 × (1 -e (-35 × PD) ) / (1 -e (-35 ) ) l. K – a、c. LGD×N [(1 – R)- 0. 5 × G ( PD ) + (R / (1 - R))0. 5 × G (0. 999) ] – b. LGD×{ N [(1 – R)- 0. 5 × G ( PD ) + (R / (1 - R))0. 5 × G (0. 999) ] – 0. 75 PD } l RWA = EAD × K ÷ 8%

Risk weighted functions for equity exposures l Market-Based l PD/LGD approach.

Internal Ratings-Based Approach

Market Risk and Risk-Based Capital The standardized model proposed by regulators The DI’s own internal market risk model Operational Risk and Risk-Based Capital The Basic Indicator Approach The Standardized Approach The Advanced Measurement Approach

")

Minimum Capital Requirement Capital Credit Risk Asset +( Market Risk + Op. Risk ) × 12. 5 ≥ 8%

Agenda Introduction of Capital The Evolution of Basel Accord Pillar I – Credit Risk – Standardized Approach Pillar I – Credit Risk – IRB Approach Capital Requirements for Other FIs Pillar I , Pillar II and Comments

Capital Requirements for Other FIs l Securities l Life Firms Insurance l Property-Casualty Insurance

Securities Firms l The capital requirements for broker-dealers set by the SEC’s Rule 15 C 3 -1 in 1975 are close to a market value accounting rule l Broker , dealers must calculate a market value for net worth on a day-to-day basis and ensure that their net worth-assets ratio exceeds 2 percent

Securities Firms l Net worth = A Book value – L Book value l Deduction: – Assets such as fixed assets not really convertible into cash – Securities that cannot be publicly offered or sold – Haircuts reflecting potential market value fluctuations in assets ex : haircut on illiquid equities : 40% debt securities : 0%~9%

scheme •")

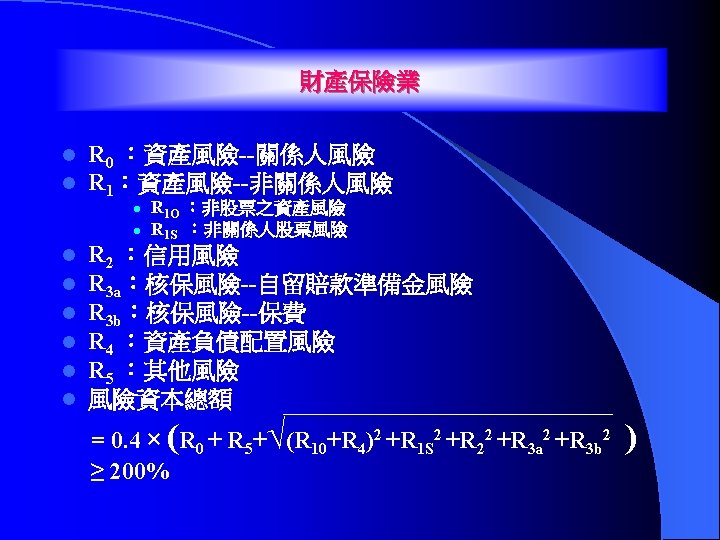

Life Insurance In 1993 the life insurance industry adopted a Risk-Based (RBC) scheme • Ifmodel A and B are perfectly. Capital independent (ρ= 0) recommended by NAIC ( National Association 2 2 1/2 σ(A+B) = ( σA + σB ) of Insurance Commissioners ) A and B are four perfectly correlated ( ρthe = 1)life insurer l • If. Identifying risks faced by l σ–(A+B) σA 2 +risk σB 2 + 2 σA σB ) 1/2 = ((σA + σB )2 ) 1/2 C 1 == (Asset – C 2 = Insurance risk = σA + σB – C 3 = Interest rate risk – C 4 = Business risk

+ 2")

Life Insurance l. RBC l = ( C 1+C 3 2 ) + 2 C 2 + Total surplus and capital RBC C 4 1

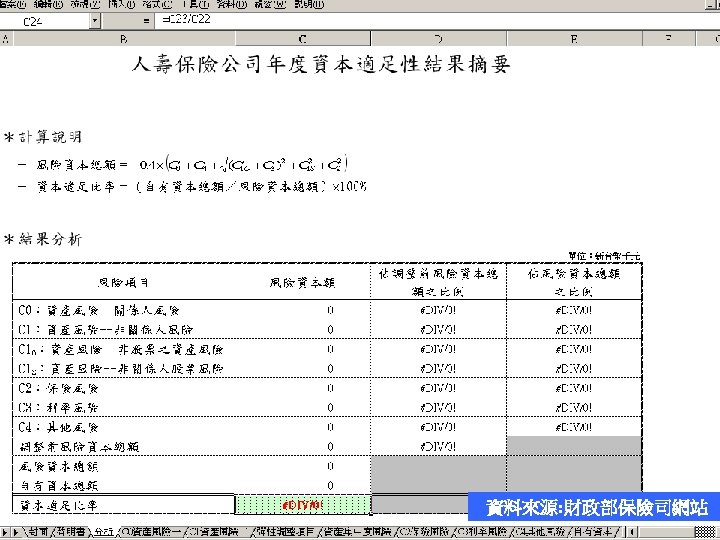

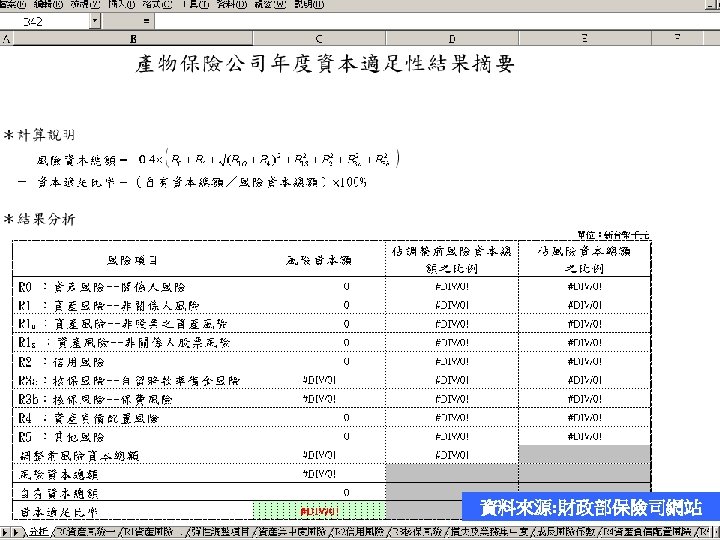

Property-Casualty Insurance l Similar to the life insurance industry’s RBC – introduced by the NAIC l Except that there are six risk categories , including three separate asset risk categories

")

Property-Casualty Insurance Risk Type R 0 Asset RBC for investments( common and preferred ) in property-casualty affiliates R 1 Asset RBC for fixed income R 2 Asset RBC for equity-includes common and preferred stock ( other than in property-casualty affiliates) and real estate R 3 Credit R 4 Underwriting RBC for loss and loss (LAE) adjustment expense reserves plus growth surcharges R 5 Underwriting RBC for written premiums plus growth surcharges Description RBC for reinsurance recoverables and other receivables

Property-Casualty Insurance l RBC l =R 0 + R 12 +R 22 +R 32 +R 42 +R 52 Total surplus and capital RBC ≥ 100%

Risk-Based Capital Factors for Selected Assets Asset Life Property-Casualty 0. 0% NAIC 1 : AAA-A* 0. 3 NAIC 2 : BBB 1. 0 NAIC 3 : BB 4. 0 2. 0 NAIC 4 : B 9. 0 4. 5 NAIC 5 : CCC 20. 0 10. 0 NAIC 6 : In or near default 30. 0 Residential mortgages ( whole loans ) 0. 5+ 5. 0 Commercial mortgages 3. 0+ 5. 0 Common stock 30. 0 15. 0 Preferred stock-bond factor for same NAIC category plus 2. 0 Bonds U. S. government

Agenda Introduction of Capital The Evolution of Basel Accord Pillar I – Credit Risk – Standardized Approach Pillar I – Credit Risk – IRB Approach Capital Requirements for Other FIs Pillar I , Pillar II and Comments

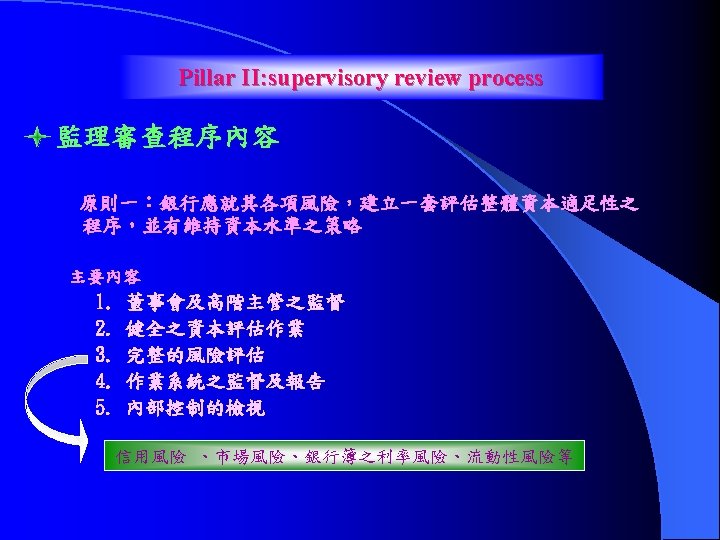

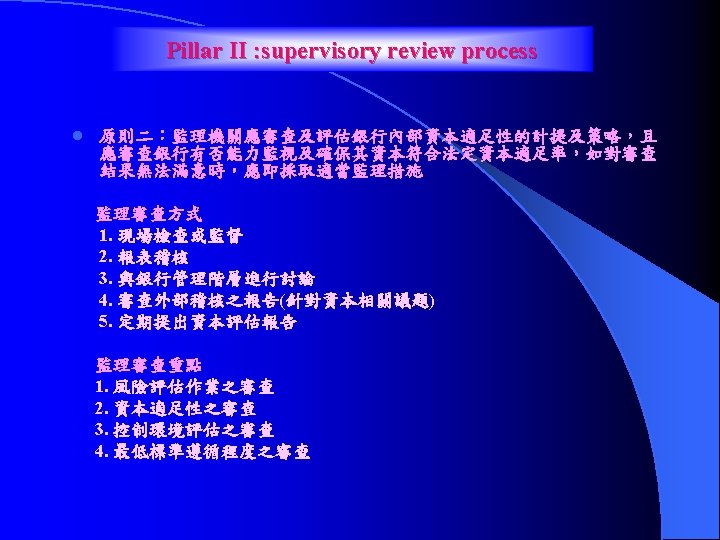

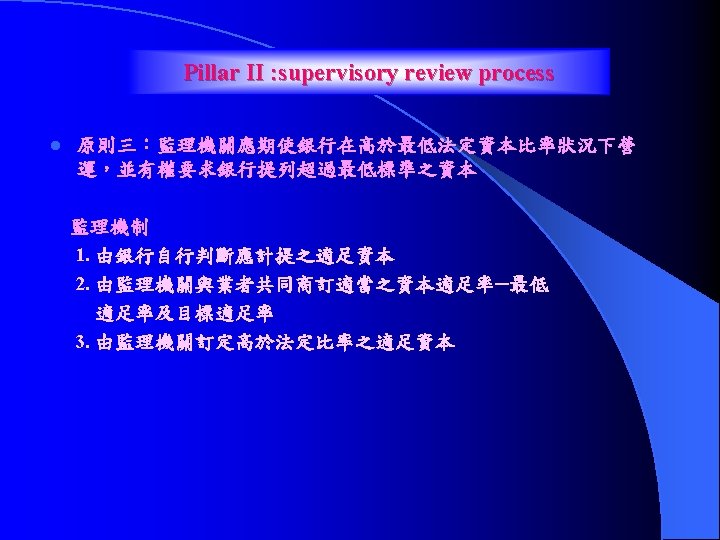

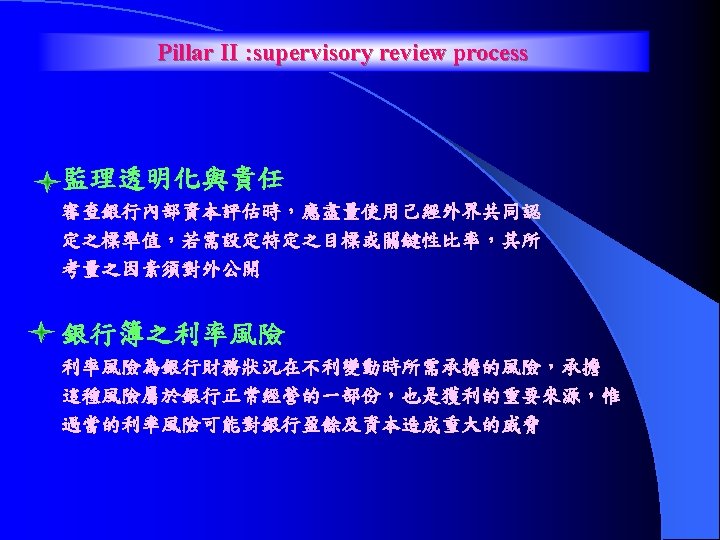

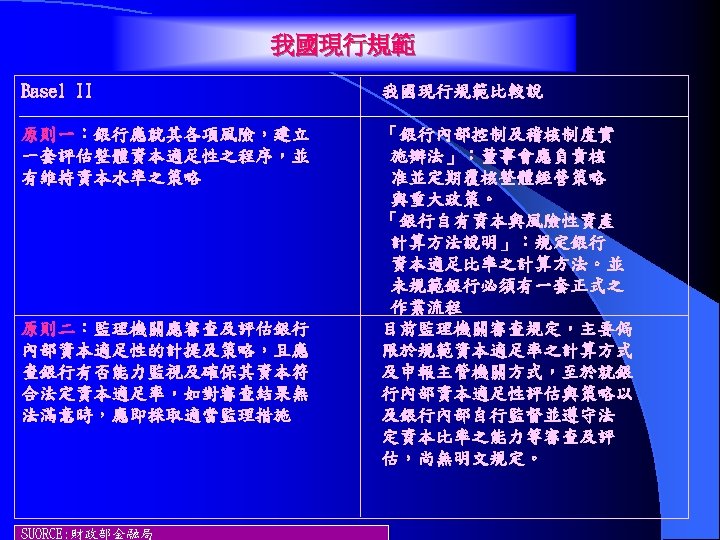

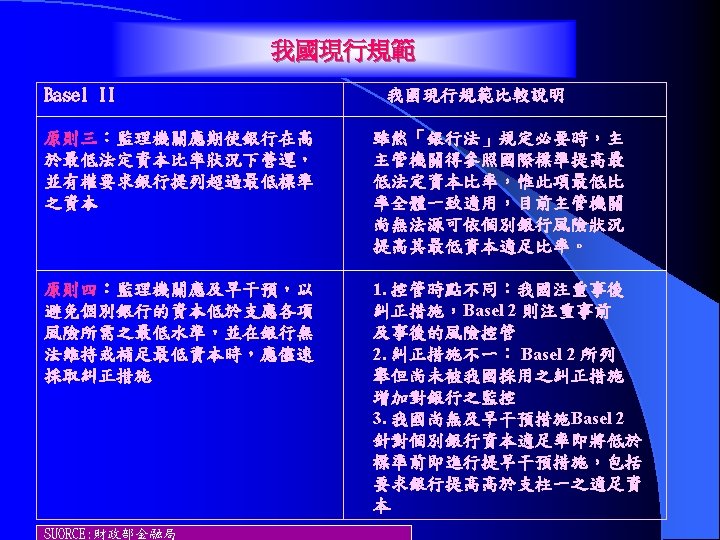

Pillar II Supervisory Review of Capital Adequacy l監理審查程序內容 l監理透明化與責任 l銀行簿之利率風險

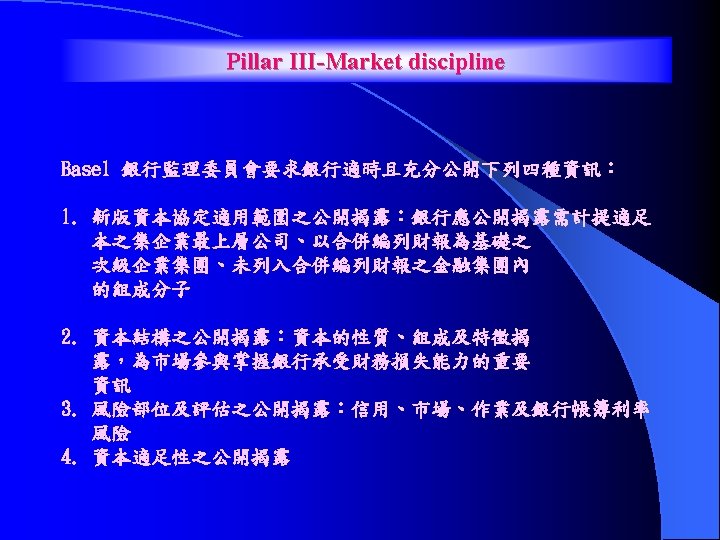

Pillar III Public Disclosure

Thanks for your attention

- Slides: 121