Acct 316 Acct 316 Chapter 2 Overview of

file. . . Acct 316 . . .")

- Slides: 71

Acct 316 Acct 316 Chapter 2 Overview of Business Processes Acct 316 UAA – ACCT 316 Information Systems Accounting Dr. Fred Barbee

Learning Objectives Acct 316 1. Explain the three basic functions performed by an accounting information system (AIS). 2. Describe the documents and procedures used in an AIS to collect and process transaction data.

Learning Objectives 3. Discuss the types of information that can be provided by an AIS. Acct 316 4. Describe the basic internal control objectives of an AIS and explain how they are accomplished.

Meet the players at S&S Hi, I’m Susan. Pleased to meet you! Acct 316 I’m Scott and I’m pleased to meet ya too!

Meet the players. . . Scott, our grand opening is only two weeks away! Acct 316 Yeah, it’s a good thing we hired an accountant!

Meet the Accountant. . . Hi folks, Ashton Fleming here! Among other things, I’m responsible for creating the accounting information system for S&S.

WOW! I have a lot of questions! Where do I start? How am I going to organize things? What information does S&S need?

How do I organize all the data that will be collected? How am I going to collect and process data about all the types of transactions that S&S will engage in?

How should I design the AIS so that the information is reliable and accurate?

Acct 316 Acct 316 Acct 316 The Three Basic Functions of an Accounting Information System

Basic AIS Functions Collect and store data Acct 316 Provide information useful for decision making Provide adequate controls

Detour. . . Transaction Cycles

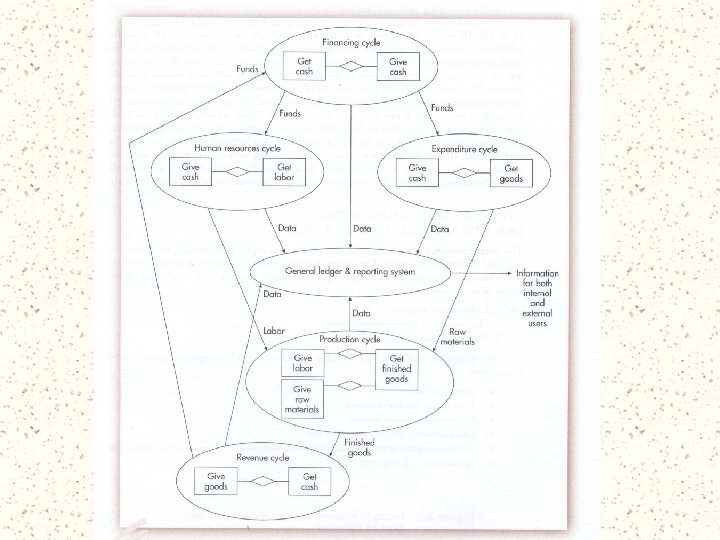

Transaction Cycles Acct 316 A transaction processing cycle combines one or more types of transactions having related features or similar objectives.

Transaction Cycles Acct 316 A transaction cycle consists of a set of transactions leading to the recognition of a major economic event on the financial statements

Transaction Cycles Acct 316 It is through the study of transaction cycles that we gain a clear view of a firm’s processing framework. (See Figure 2 -1 p. 25)

Let’s. . . At Something Familiar

Cost Flows in a Manufacturing Firm Product Costs Manufacturing Costs DM DL MOH Balance Sheet Unused Used d e i l App WIP Income Statement she Dr. Fred Barbee COGS = Gross Margin - S&A = Unfinished Fini Sales - DM Inv. Net Income WIP Inv. d FG Inv. Sale Sold Period Costs 18

Materials Plant Customers Cash Fin. Goods Cash Labor EXPENDITURE CYCLE CONVERSION CYCLE REVENUE CYCLE Subsystems Purchasing & A/P Cash Disbursements Payroll Subsystems Production Planning and Control Cost Accounting Subsystems Fin. Goods Cash Sales Order Processing and Cash Receipts

Let’s. . . At Another Approach

Merchandising Shipments Sale of Merchandise Cash Receipts GL & Fin Rpt Cycle Purchase of Mdse, & Labor, Etc. PP&E, Investments Cash Disbursements Merchandise Receipts

The Revenue Cycle 47

Merchandising Shipments Sale of Merchandise Cash Receipts GL & The Revenue Cycle PP&E, Fin Rpt Investments Spans activities from “Sale” to Cycle “Receipt of Cash Purchase of Mdse, & Labor, Etc. Key Cash Transactions: Disbursements Merchandise Sales Receipts Cash Receipts

The Revenue Cycle Includes transactions surrounding the recognition of revenue. Acct 316 Sales Accounts Receivable Inventory (some) General Ledger (some)

The Revenue Cycle Capturing and recording of customer orders; Acct 316 Shipment of the goods and the recording of the cost of goods sold.

The Revenue Cycle. Acct 316 The billing process and the recording of sales and accounts receivable; The capturing and recording of cash receipts.

The Expenditure Cycle 47

The Expenditure Cycle Spans activities from the “need” for Merchandising Shipmentsto “payment” for resources/services that resource/service Sale of Merchandise Cash Receipts Key Transactions: GL & Purchases PP&E, Fin Rpt Investments Cash Disbursements Cycle Purchase of Mdse, & Labor, Etc. Cash Disbursements Merchandise Receipts

The Expenditure Cycle Includes the transactions surrounding the recognition of expenditures. Acct 316 n Purchases n n Accounts Payable n n Cash Disbursements Inventory (some) General Ledger (some)

The Expenditure Cycle The preparation and recording of purchase orders; Acct 316 The receipt of goods and the recording of the cost of inventory; The receipt of vendor invoices and the recording of accounts payable;

The Expenditure Cycle The preparation and recording of cash disbursements. Acct 316 The cycle also includes the preparation of employee paychecks and the recording of payroll activities.

Back to. . . Basic AIS Functions

Cl o s e er And p AIS Function Up Collect and store data about the organization’s business activities and transactions efficiently and effectively

AIS Function #1 – Up Close Capture transaction data on source documents. Acct 316 Record transaction data in journals, which present a chronological record of what occurred.

AIS Function #1 – Up Close Acct 316 Post data from journals to ledgers, which sort data by account type.

Data Processing Cycle The resources affected by that event. The agents who participate in that event. The Event of Interest

Data Files Input Output Process Feedback Loop Control Sensor

Capture Transaction Data on Source Documents Purchase Order Sales Order Acct 316 O Source documents are special forms used to capture transaction data. Sales Invoice

Capture Transaction Data on Source Documents Acct 316 Control over data collection is improved by prenumbering each source document. Accuracy and efficiency in recording transaction data can be further improved if source documents are properly designed.

System - Inputs Input documents can be categorized into three types. . . Acct 316 Source Documents Product Documents Turn-around Documents

Creation of a Source Document Order Data Collectio n Source 11 Document 2 3 Sales Order Customer Sales System

A Product Document Order Data Collectio n Source 1 Document 2 3 Sales Order Customer Bill Remittance Advice Product Document Sales System

A Turnaround Document Data Collection Order Source 1 Document 2 3 Sales Order Customer Check 1 Bill Remittance Advice Product Document 1 Remittance Advice Sales System Cash Receipts System

Common Source Documents & Functions Source Document Function Sales Order Record Customer Order Delivery Ticket Record Delivery to Customer Remittance Advice Receive Cash Deposit Slip Record Amounts Deposited Credit Memo Support Adjustments to Customer Accounts Revenue Cycle

Common Source Documents & Functions Source Document Function Purchase Requisition Request that purchasing department order goods. Purchase Order Request goods from vendors. Receiving Report Record receipt of merchandise. Check Pay for items. Expenditure Cycle

Common Source Documents & Functions Source Document Function Collect employee W 4 forms withholding data. Record time worked by Time cards employees. Record time spent on Job time tickets specific jobs. Human Resource Cycle

Common Source Documents & Functions General Ledger and Reporting System Record entry posted to Journal Voucher general ledger. General Ledger & Reporting System

Data Files Input Output Process Feedback Loop Control Sensor

Data Processing Acct 316 Updating previously stored information about the resources affected by the event and agents who participated in the activity.

Data Processing Acct 316 Periodic updating of the data stored is referred to as batch processing. Immediate updating as each transaction occurs is referred to as on-line, real-time processing.

What is an Audit Trail? Acct 316 An audit trail provides a means to check the accuracy and validity of ledger postings.

Data Files Input Output Process Feedback Loop Control Sensor

Storage. . . Acct 316 Ledgers and files provide storage of data in both manual and computerized systems. The General Ledger The Accounts Payable Ledger The Accounts Receivable Ledger

Storage. . . A ledger is. . . Acct 316 . . . a book of financial accounts, which reflect the financial effects of the firm’s transactions after they are posted from the various journals.

Flow of Information From the Economic Event to the General Ledger Order Sales Order Journal Entry Sales Journal Customer Post AR Sub Ledger Periodically reconcile subsidiary ledger to General Ledger Post General Ledger

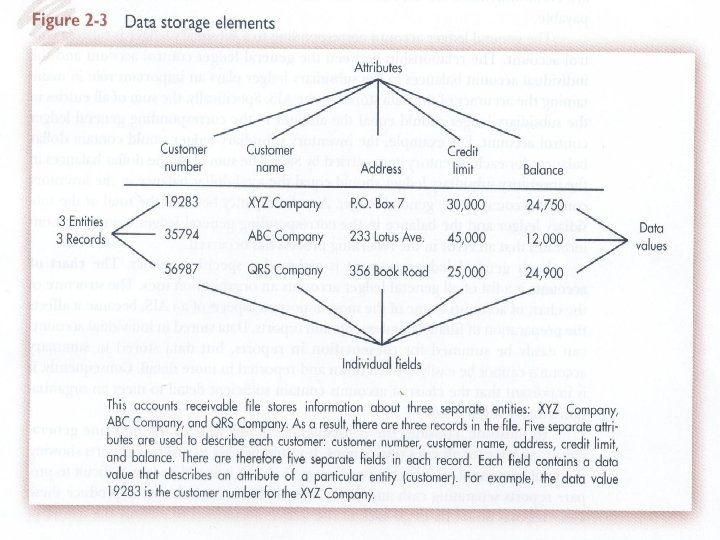

Storage. . . A file is an organized collection of data. Acct 316 Files may be Manual Computer (magnetic)

Storage. . . A transaction file is. . . Acct 316 . . . a collection of transaction input data - normally temporary in nature.

Storage. . . A master file is. . . Acct 316 . . . a collection of data that are of a more permanent or continuing interest

Storage. . . A reference (table) file. . . Acct 316 . . . contains data that are necessary to support data processing

Cl o s e er And p AIS Function Up To provide management with information useful for decision making.

AIS Function #2 – Up Close Acct 316 This information is provided in the form of reports that fall into two main categories: financial statements managerial reports

Cl o s e er And p AIS Function Up Provide adequate controls to ensure that data are recorded and processed accurately

AIS Function #3 – Up Close Acct 316 Ensure that the information produced by the system is reliable. Safeguard organizational assets.

AIS Function #3 – Up Close Acct 316 Ensure that business activities are performed efficiently and in accordance with management’s objectives.

Internal Control Considerations What are two important methods for accomplishing these objectives? Acct 316 Provide for adequate documentation of all business activities. Design the AIS for effective segregation of duties.

Adequate Documentation Acct 316 Documentation allows management to verify that assigned responsibilities were completed correctly.

What is Segregation of Duties? Acct 316 Segregation of duties refers to dividing responsibility for different portions of a transaction among several people.

What is Segregation of Duties? What functions should be performed by different people? Acct 316 – authorizing transactions – recording transactions – maintaining custody of assets

Segregation of Duties Authorization Recording Custody

Types of Internal Controls Preventive Detective Corrective