Accounting Practices in Nepal Concept Accounting Information System

Internationally not")

are set")

• Accounting and reporting for all")

������� �������")

������� �������")

- Slides: 38

Accounting Practices in Nepal Concept, Accounting Information System, Accounting Practices, recent development in Nepal Presented by: Sundar Shrestha Amrit Shrestha (CA, CPFA Affil. )

Contents of Course - Outline Session 1 General Accounting concept Accounting procedures Types of accounting bases Accounting standards (Recent changes) Session 2 Financial statement (NPSAS based) Practical Cases (e. g Third party payments, Intergovernment transaction) Practical Examples

Session 2

Reform process Aabi Working note NPSAS FS

Need of NPSAS Go. N sector did not have financial statements (GPFS) Internationally not accepted as FS Financial audit was not happening Economic decision could be taken on the basis of Aa. Bi Information were scattered, to get a complete picture every thing needs to be worked out again Narrative disclosure were not available

Accounting standard adoption model Accounting Standard Profit oriented entities Government Entities IAS IFRS IPSAS NFRS NPSAS

Introduction – IPSAS & Implementation Concept International Public Sector Accounting Standards (IPSAS) are set of accounting standards issued by International Public Sector Accounting Standards Board (IPSASB) Board IPSASB is an independent standard setting board for public sector entities supported by the International Federation of Accountants (IFAC). Objective IPSASB issues IPSAS, guidance, and other resources that harmonises accounting and reporting across the globe Implementati on Almost more than 100 countries of the world have adopted or are in process of implementing IPSAS. Pakistan, Sri-Lanka, Malaysia, Jordan, Vietnam, etc. have successfully adopted IPSAS. Implemented since 2000 OECD 1 st body to comply, EC on 2005, Common wealth and NATO 2007, WFP 2008, and across many countries world wide History of implementati on

What is NPSAS cash basis ? NPSAS = Nepal Public Sector Accounting Standard- cash basis Applicable to Public Sector = Government accounting controlled entities IPSAS=IPSAS cash basis & IPSAS accrual basis IPSAS cash basis = NPSAS cash basis NPSAS practices meaningful financial reporting practice so that an entity’s total receipts, payments & fund position can be easily known. NPSAS report is useful to donors and stakeholders for decision making purpose. NPSAS financial is in international parameter so government can easily compares with other countries performance Previous reporting is based on different OAG Forms like form no. 9, 193, 194, 17, 208, 210 etc. And there is no total fund position and no records for third party transactions.

NPSAS’s Main Focus on : Preparation of “General Purpose Financial Statements” “

Structure of NPSAS Cash Basis Part 1 (Mandatory) • Accounting and reporting for all cash receipts and payments • Statement for Budget Comparison (for budgetary entities) • Disclosures through Notes to Account and Accounting Policies. Part 2 (Encouraged additional disclosure) • This part focus on additional important disclosure of assets, liabities, receivables , payables, commitments, etc. • It’s not a mandatory requirement but such additional disclosures provides foundation for future accrual implementation.

Reporting Entities Budgetary Entities Controlled entities which have budget expenditures like Road Department, ministries itself, etc. Extra Budgetary Entities Controlled entities which have own incomes like Road Board. Government Business Enterprises Controlled entities which are government Trading organization like NOC, Railway Corporation, etc. Consolidation is for Budgetary, Extra Budgetary and GBEs as Consolidated Financial Statement Reporting Entities Spending Units

Flow of Information during financial statement preparation Trial balance • Data entry prepares trial balance Notes to account (Schedules) Annual Statement R/P Consolidated Statement R/P • Figures are linked with trial balance and forms schedules • Inter entity transaction are eliminated here • Third party transaction are presented Accounting policies & Notes to Accounts • Disclosure on significant items and relevant for understanding FS

Information to be obtained to FS preparation Part 1: Trial Balance ( Revenue reports(OAG 113), Expenditure reports (OAG 225 & 213), Deposit reports (OAG 607), Third Party Transactions: Direct payments (OAG 216) Pure-Budgeted Reports Elimination of interdepartment, interentity transaction to avoid duplication of entry and Final Consolidation of reports Finalized FS of extra -budgeted entity and GBE’s as per mapping policy Other mapping entities’ Reports Budget Information and addiitional info for notes to accounts Additional disclosures in notes to accounts Final Consolidation

Areas of Concern on NPSAS FS Mapping of entity Defining control of entity Third Party transaction Intergovernmental transactions Conversion of Accrual to cash basis Control of cash identification Disclosure preparation

Mapping and Control Mapping refers to identification of controlled and controlling entities In simple language it is identification of all entities controlled by the reporting entity Control is established through power to govern financial and operating policies

Third Party payments One of major disclosure requirement in NPSAS, it shall be presented in face of the financial statements. Generally off budget off treasury items, it can be obtained through 3 method � Direct payment � Technical Assistance � Commodity assistance Examples: TA support provided by DP’s, Turnkey Projects, Vehicles & medicine donated by DP’s Doesn’t takes into account (I/NGO’s)

NPSAS on Federal structure Due to new political scenario of Federal Structure of Government Nepal, there are three tiers of government, but no significant changes implementation on NPSAS as the accounting rules are same for all governments.

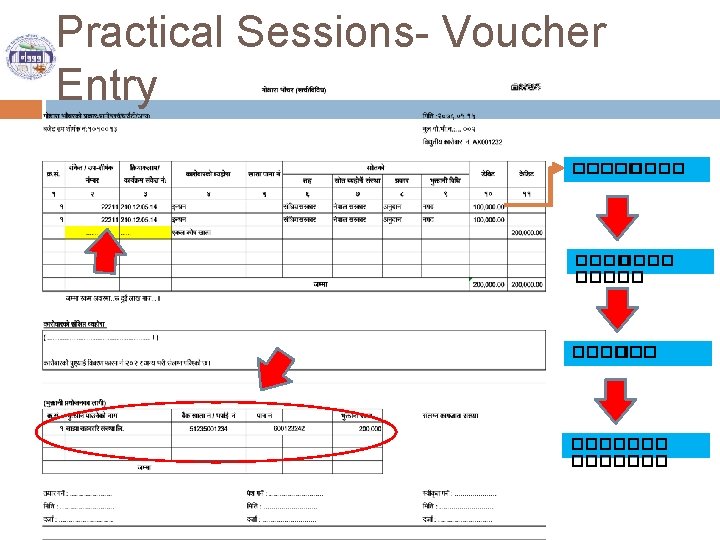

Practical Sessions LMBIS entry = अखत य र

Budgetary control

Practical Session-Ledger Balances �������

Practical Session-Trial Balances �����

Schedules

Practical session-NPSAS (Receipt and Payment Account) ������� �������

Practical session-NPSAS (Receipt and Payment Account) ������� �������

Budget Comparison

Disclosure

Cash Balance Analysis

Concept of Materiality and Professional judgement

Preparation of Notes to accounts notes are important disclosures that further explain numbers on the financial statements. The reason for these notes are to fulfilling the needs of the external users of the financial statements.

Simple Fundamental of NPSAS Particulars Schedu le This Year Amount 1. Cash Receipts 1000 2. Less: Cash Payments (800) 3. Cash Balance for the period (1 -2) 200 4. Add/(Less)Other cash Balances 50 5. Opening Cash Balance 300 Previous Year Amount 6 Net Closing Cash Balance Schedules Provided for justification of the Net Cash 550 Position at Year end, (3+/-4+5)notes to accounts and disclosures ( Budget comparison is must, through supported by third party payment disclosures )

Existing Consolidated Financial statements Phatwari are prepared on regular basis Kendriya Arthik Bibaran will be prepared on regular basis. However they will be part of working and will be a major supporting documents New Approved OAG form has recognized NPSAS based Financial statement as final financial statement which will be audited by OAGN

Reporting Intergovernmental Fiscal Arrangement act 2075 chapter 8 Financial discipline and Transparency to be maintained. (U/s 30) Accounting as prescribed by Nepal Government (U/s 31) Periodic reporting (U/s 32) (Quarterly) � by province within 30 days after end of period. � by Local government within 15 day after end of period Federal government consolidated financial statement within poush end of each year

THANK YOU