Accounting for Value Chain Analysis Value chain concept

")

to one that")

- Slides: 22

Accounting for Value Chain Analysis: §Value chain concept §Value Added analysis and Value Chain analysis §Porter’s value chain framework §Management accounting systems in the value chain framework.

Value-chain concept: what is it and what does it offer? . A value chain describes the linked set of value-creating functions that are required to bring a product or service to the customer. It begins with basic raw materials from suppliers, moving to a. series of value-added activities involved in producing and marketing a product or service and ending with distributors getting the final products or services into the hands of the ultimate customers. Michael Porter. (1950, 1985) has developed this valuechain concept as a tool to help businesses analyse their cost stru-iures and identify competitive strategies. A value-chain ir. a'ysis emphasises th r costs occur, not merely in manufacturing, but across the business. It provides a useful perspective for understanding non-manufactuting cost classifications. Supplying and manufacturing activities are described as 'upstream' segments of a value chain, while marketing and distribution activities are 'downstream' segments of a value chain.

Value-added analysis and value-chain analysis: how do they differ? Value-added analysis involves classifying activities as valueadded or non-value- added. This concept is adopted to identify which activities to keep and which to eliminate. The following activities in organisations tend not to add value to the core activities: preparation time; waiting time; unnecessary process steps; overproduction; rejects; set-up times; transportation/ distribution; process waste; materials waste; communications; administration/decision-making; untidiness; bottlenecks; and timing.

Value-chain analysis places emphasis on understanding the total value of all operations across the business, as well as the industry. By considering the value chain organisations, can determine areas where cost can be minimized (for cost-leadership strategy) and areas where customer value can be enhanced (for product differentiation strategy). The value chain of a business focuses on the set of valuecreating activities that range from the receipt of raw materials from suppliers and research and development of products and processes, to the sale of the product to the customer and the provision of after-sales customer support. Customer value refers to the characteristics of a product or service that a customer perceives as valuable.

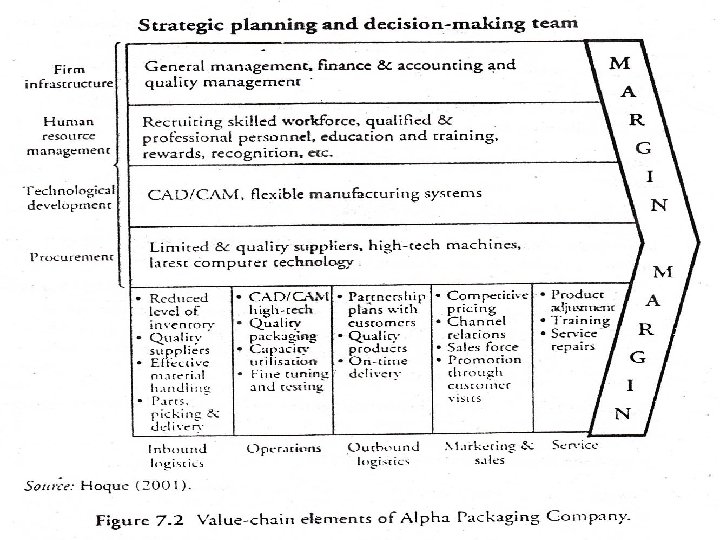

Porter's value-chain framework: applying it to the business for excellence Porter proposes that a firm's value chain is composed of nine categories of interrelated activities. These activities are 1. Primary activities and, 2. Support activities.

Primary activities include: 1. Inbound logistics activities involve managing inbound items such as raw materials handling and warehousing. 2. Operations activities involve the transformation of inbound items into products suitable for resale, for example research and development, product design and manufacturing. 3. Outbound logistics activities involve carrying the product from the point or manufacturing to the buyer such as warehousing and distribution.

4. Marketing and sales activities involve informing buyers about products and sen-ices with a reason to purchase, such as distribution strategy and promotional activities, including advertising. 5. Service includes all activities required to keep the product or service working effectively for the buyer, after it is sold and delivered. Examples of such activities include installation, repair, after-sales service, warranty claims and answering customer inquiries.

Support activities In support of the above primary activities of the value chain, Porter proposes four support activities: (1) procurement (purchasing), (2) human resource management (HUM), (3) technology development (R&D) and (4) the firm's infrastructure (accounting, finance, strategic planning, etc. ). These activities feed into each stage of the primary activities.

Porter has identified five forces, that can affect the profitability of the firm: (1) The threat of new entrants; (2) The threat of substitute products and services; (3) The rivalry among existing organisations within the industry; (4) The bargaining power of suppliers; and (5) The bargaining power of consumers.

Porter suggests that the initial step for a firm's strategic analysis is to define its value chain. It is suggested that competitive advantage, irrespective of whether the firm adopts a cost leader or differential strategy, be achieved in the marketplace by giving value for money, that is competitive advantage comes from carrying out the valuecreating activities more cost-effectively than one's competitors. According to Porter, ‘The value chain desegregates a firm into its strategically relevant activities in order to understand the behavior of costs, and the existing and potential sources of differentiation. ’ A firm gains competitive advantage by performing these activities more cheaply or better than its competitors. '

Porter's value-chain analysis has several distinctive characteristics. One of these attributes of value-chain analysis insists on the complex linkages and interrelationships both between the strategic business unit and its customers and suppliers as well as those found internally. If these linkages are exploited, a firm is more likely to gain a competitive advantage. This necessitates management having to refocus, looking not only at the activities internal to the firm, but also at those activities external to the firm. This in turn highlights opportunities for the firm to work with suppliers and end-customers, which in turn should lead to increased competitive advantage. Value-chain analysis also recognizes that activities internal to the firm are interdependent rather than independent. A firm's history, its strategy, its approach to implementing its strategy and the underlying economics of its situation arc reflected in the Porter value-chain framework.

Corporate value chain: what is it and how does it differ from an individual product's value chain? Steps in a corporate value-chain analysis: • Examine each product line's value chain and consider its strengths and weaknesses. • Examine the 'linkage' within each product line's value chain. Linkages are connections between the way one value-added activity (e. g. marketing) is performed and the cost of performance of another activity (e. g. quality control). • Examine the potential synergies among the value chains of different product lines or business units. Each value element (e. g. advertising or manufacturing) has an inherent economy of scale in which activities are conducted at the lowest possible cost per unit of output (i. e. sharing resources by two separate products in the corporate value chain).

Management accounting systems in the value-chain framework According to Porter , a value-chain cost management methodology involves the following steps: • Identify the value chain, then assign costs, revenues and assets to value activities. • Diagnose the cost drivers regulating each activity. • Develop sustainable competitive advantage, either through controlling cost drivers better than competitors, or by reconfiguring the value chain.

Within the value-chain framework, costs are classified into two was 1. Structural and 2. Executional. Structural cost drivers derive from a company's choices about its Underlying economic structure. These choices drive cost positions for any given product group.

Structural cost drivers derive from a company's choices about its Underlying economic structure. These choices drive cost positions for any given product group. There at least five strategic choices that a firm must make about its underlying economic structure: 1. Settle- the size of the investment in manufacturing, R&D and marketing resources. 2. Scope— the degree of vertical integration. 3. Experience - how many items in the past has the firm already created and what is it doing again? 4. Technology - what process technologies are used in each step of the firm's value chain? 5. Complexity — how wide a line of products or services is being offered to customers?

Executional cost drivers are the determinants of a firm's cost position that hinges on its ability to 'execute' them successfully. These cost drivers may include: • workforce involvement; • total quality management; • capacity utilisation; • plant layout efficiency; • product configuration; • linkage with suppliers and customers.

Traditional management accounting Vs. Strategic management accounting Traditional management accounting systems have been criticized for a greater internal focus within which a key theme is to maximize the difference (that is, the value added) between purchases and sales. There is the view that traditional management accounting does not give adequate information on non-financial and external factors crucial to the long-term survival of the firm. Management accounting moving away from a traditional 'managerial cost analysis' to a forward thinking 'strategic cost analysis' or 'strategic management accounting‘.

Accounting in the value chain covers more than the conventional concept of value added which ignores important linkages with both suppliers and customers by focusing only on value added within the firm. From a strategic approach value added has problems because it starts too late and finishes too soon. Starting cost analysis with purchases misses all the opportunities for taking advantage of the firm's suppliers. That is, firms need to develop good relations with suppliers and investigate how costs can be reduced for both the firm and its suppliers, e. g. through ordering, freight and quality

A change from a traditional accounting system (such as standard costing) to one that better fits with the organisation's strategy can be advantageous. Costs are assigned to each value activity comprising the chain in an organisation and cost drivers are identified for each activity. The final step is to build a sustainable competitive advantage either operating on the cost drivers to reduce costs or by rearranging the value chain, focusing on those activities in which the firm has a competitive advantage.

Accounting in the value chain covers more than the conventional concept of value added which ignores important linkages with both suppliers and customers by focusing only on value added within the firm. From a strategic approach value added has problems because it starts too late and finishes too soon. Starting cost analysis with purchases misses all the opportunities for taking advantage of the firm's suppliers. That is, firms need to develop good relations with suppliers and investigate how costs can be reduced for both the firm and its suppliers, e. g. through ordering, freight and quality.

Porter's value-chain analysis provides the better basis for strategic management accounting design. Life-cycle costing relies on value-chain analysis as explicit attention to postpurchase costs by the customer can lead to more effective market segmentation and product positioning. Similarly, JIT relies on value-chain analysis as it considers supplier relationships.