ACCOUNTING FOR LABOUR Introduction Direct and indirect labour

ACCOUNTING FOR LABOUR

Introduction

Direct and indirect labour costs • All costs of indirect workers (i. e. those not directly involved in making products, such as maintenance staff and supervisors) are indirect costs. • For workers directly involved in making products: – Direct costs are their basic pay, and any overtime premium paid for a specific job at the customer’s request. – Indirect costs are general overtime premiums, bonus payments, idle time, and sick pay

Remuneration methods • There are three basic remuneration methods; – time work, – piecework, and – bonus schemes

i. Time work • Wages are paid on the basis of hours worked. • For example, if an employee is paid at the rate of $5 per hour and works for 8 hours a day, • Total pay = 5*8 = $ 40

• For example, an employee is paid a normal rate of $5 per hour and works 4 hours overtime for which he is paid at time-and-a half. • The amount paid for the overtime will be 4 x 1. 5 x $5 = $30.

Example 1

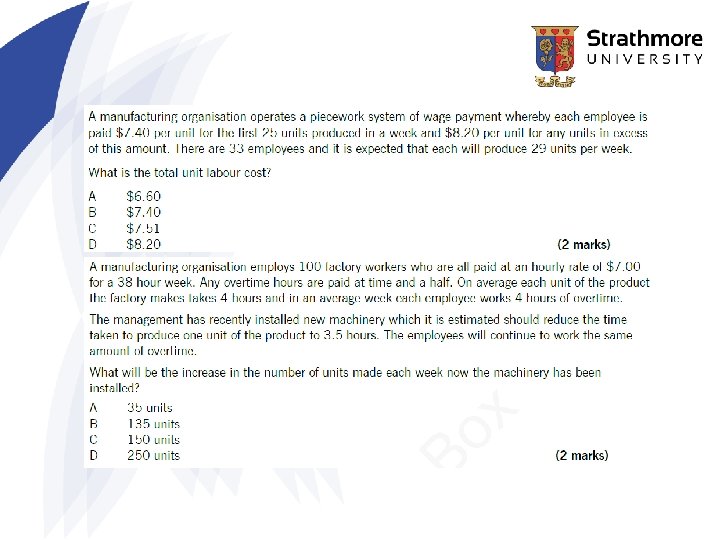

ii. Piecework • Wages are paid on the basis of units produced • For example an employee is paid $0. 20 for every unit produced, with a guaranteed minimum wage of $750 per week. • In week 1, they produce 5, 000 units and so the; • Pay will be = 5, 000 x $0. 20 = $1, 000

• In week 2, they only produce 3, 000 units; the pay will be? • Pay = 3, 000 x $0. 20 = $600. • However, since this is below the guaranteed minimum the employee will receive $750 for the week.

schemes • There are many different ways in which a")

iii. Bonus (or incentive) schemes • There are many different ways in which a bonus scheme can operate, but essentially in all cases the employee is paid a standard wage but in addition receives a bonus if certain targets are achieved,

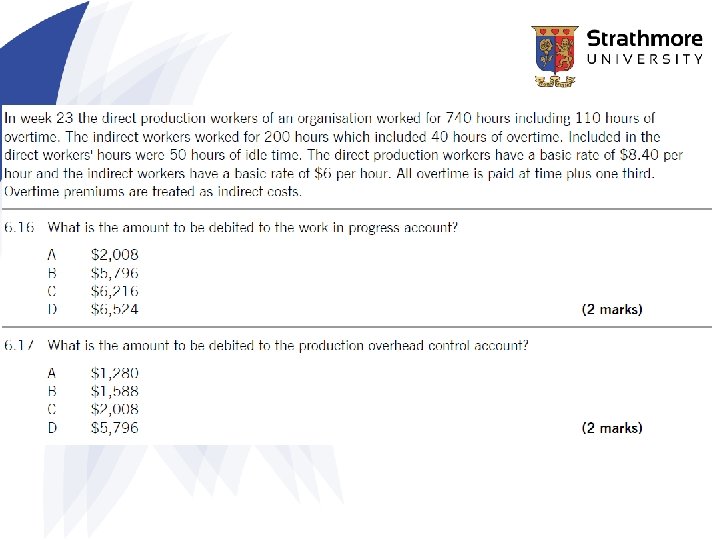

Example: overtime and idle time • Given below are the labour costs incurred by a manufacturing business for the week commencing 23 July 20 X 5. – Direct production workers 120 hours at $6. 40 per hour – Direct production workers overtime hours 20 at $9. 40 per hour – Indirect workers 40 hours at $5. 20 per hour – Indirect workers overtime hours 5 at $8. 00 per hour – Of the hours paid to the direct production workers 4 of these were idle time hours. • What is the total for direct labour and indirect labour for the week?

Changes effect on remuneration methods and productivity on unit labour costs • To increase competitiveness, employers will try to reduce unit costs and will often attempt to do this by offering employees productivity payments. • Employers need to look at the-before and after costs.

Illustration • Current scheme: – $7/hour, 40 hour week. – Overtime premium = time and a half. – Usually 400 units are produced in 50 hours • Proposed scheme: – rates as above, but in addition; – the overtime premium is paid on any hours saved. – Assume that 500 units are now made in 44 hours • Evaluate the proposal

Example 2

Example 3

Example 4

Gross and net earnings • Gross pay: the total amount earned by the employee • Net pay: the amount paid to the employee after the employer makes deduction for income tax and certain statutory amounts. • Total labour cost to employer: employees’ gross pay plus any additional payroll taxes (and perhaps pension costs) that the employer has to bear.

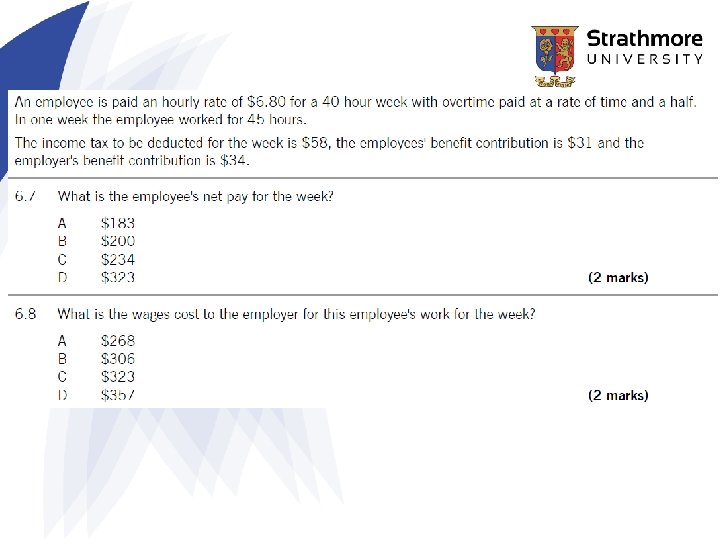

Example: gross pay to net pay • An employee is paid at; – an hourly rate of $7. 00 for a 35 hour week – with any overtime hours paid at time and a half. – During week 22 the employee worked for 41 hours. • The income tax to be deducted was $55, the Employee's benefit contributions for the week were $28, and the Employer's benefit contributions were $29. • What is the employee's net pay? • What is the labour cost to the employer for this employee for the week?

Production and productivity • Production is the quantity or volume of output produced. • Productivity is a measure of the efficiency with which output has been produced. • An increase in production without an increase in productivity will not reduce unit costs.

Example • An employee is expected to produce three units in every hour that they work. The standard rate of productivity is three units per hour, and one unit is valued at 1/3 of a standard hour of output. If, during one week, the employee makes 126 units in 40 hours of work, determine; – The production – The productivity ratio

• Other measures of labour activity include the following: – Production volume ratio, or activity ratio – Efficiency ratio (or productivity ratio) – Capacity ratio

Efficiency ratio • The efficiency ratio measures the efficiency of the labour force by comparing equivalent standard hours for work produced and actual hours worked.

Capacity Utilisation ratio • The capacity utilisation ratio compares actual hours worked and budgeted hours, and measures the extent to which planned utilisation has been achieved.

Production volume ratio • The production volume ratio compares the number of standard hours equivalent to the actual work produced and budgeted hours.

Example • ABC Co. budgets to make 25, 000 standard units of output (in 4 hours each) during a budget period of 100, 000 hours. • Actual output during the period was 27, 000 units which took 120, 000 hours to make. • Required • Calculate the efficiency, capacity and production volume ratios.

Ledger accounting for labour costs • The gross pay is debited to the wages control account and the; • Direct cost element is then transferred to the work in progress account whilst the ; • Indirect cost element is transferred to the production overhead control account.

In double entry, the system is as follows • Dr. Work-in-progress with the gross wages, direct cost • Cr. Wages control account with the gross wages • Dr. Work-in progress with the employer’s payroll tax • Cr. Wages control account with the employer’s contributions to payroll tax • Dr. Wages control account • CR. Cash as employee paid the net amount • CR. Cash as the revenue authorities are paid employee deductions and employer contributions.

- Slides: 30