ACCOUNTING 1 Recording Adjusting and Closing Entries for

")

. The temporary accounts")

- Slides: 16

ACCOUNTING 1 Recording Adjusting and Closing Entries for a Service Business Chapter 8

ACCOUNTING CYCLE FOR A SERVICE BUSINESS 1 2 8 3 7 4 6 5 1. 2. 3. 4. 5. Analyzes transactions Journalize Post Prepare work sheet Prepare financial statements 6. Journalize adjusting and closing entries 7. Post adjusting and closing entries 8. Prepare post-closing trial balance

Advanced organizer of our unit objective:

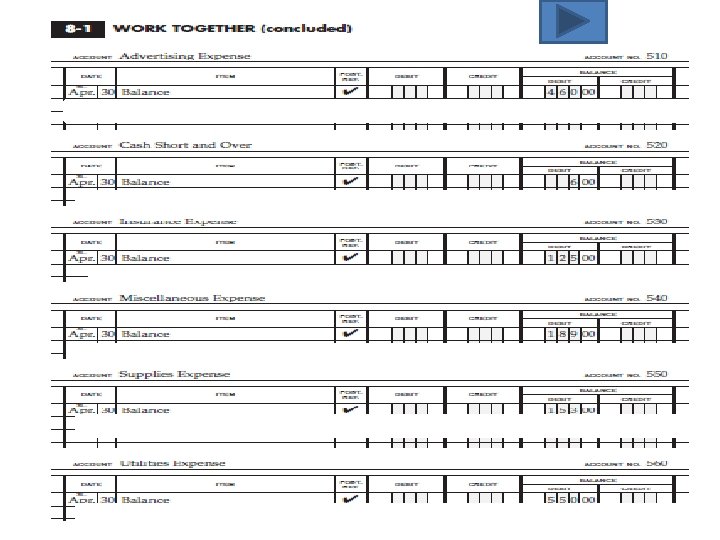

TEMPORARY ACCOUNTS • Accumulate information for a specific accounting period • All accounts not on the balance sheet – Revenues – Expenses – Drawing • These accounts are CLOSED

PERMANENT ACCOUNTS • All accounts reported on the balance sheet – Assets (including contra-assets) – Liabilities – Capital account • Contain the results of all transactions since the business started • These accounts are NOT CLOSED

THE CLOSING PROCESS • Gives temporary accounts zero balances so they are prepared to accumulate new information for the next accounting period • Involves four closing journal entries 1. 2. 3. 4. Close Income Statement accounts with a CREDIT balance. Close Income Statement accounts with a DEBIT balance. Close the INCOME SUMMARY and Record NET INCOME/LOSS Close the DRAWING account to the owner’s capital • The income summary account is used to aid in the closing process

NEED FOR THE INCOME SUMMARY ACCOUNT Like an Income Statement, Income Summary represents the normal balance or Revenues and Expenses + normal Revenue - - + normal

• Involves four closing journal entries 1. 2. 3. 4. Close Income Statement accounts with a CREDIT balance. Close Income Statement accounts with a DEBIT balance. Close the INCOME SUMMARY and Record NET INCOME/LOSS Close the DRAWING account to the owner’s capital 4. 1. 2. 3.

What is the balance of Income Summary we need to close out? Income Summary 1483 2160 bal 677

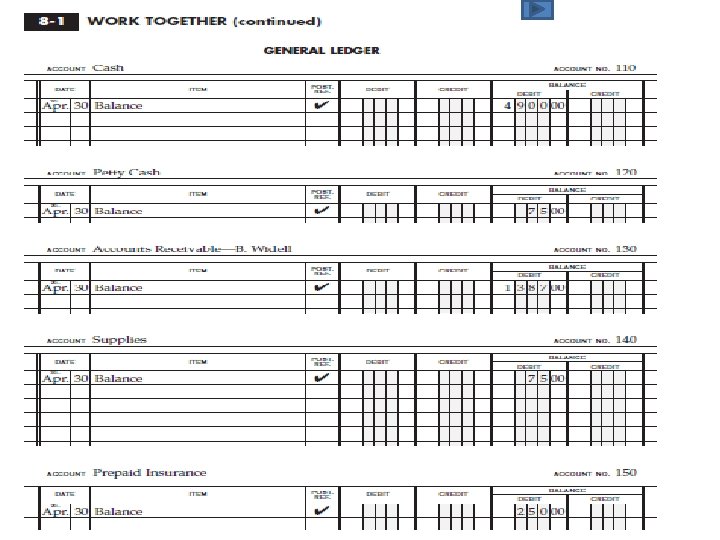

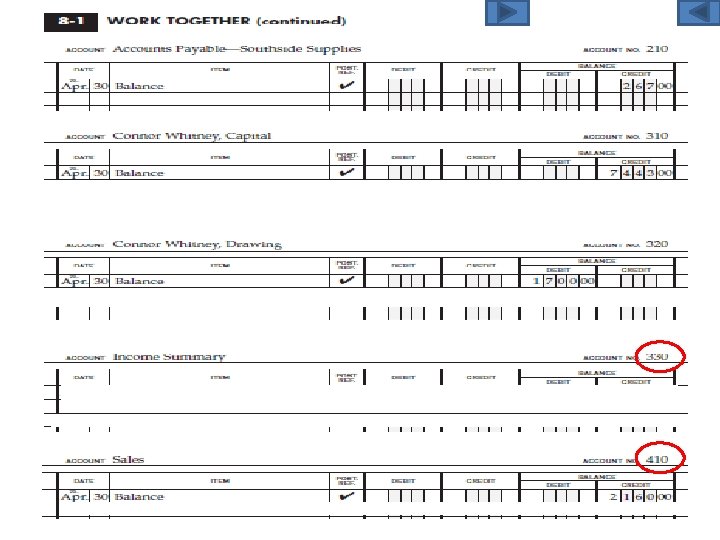

POST-CLOSING TRIAL BALANCE Only general ledger accounts with balances (permanent accounts). The temporary accounts should have closed to zero and are not included. 4 1 3 2 6. Totals 7. Record totals 8. Double rule 6 5 7 1. Heading 2. Account titles 3. Account balances 4. Single rule 5. Compare totals 8

ACCOUNTING CYCLE FOR A SERVICE BUSINESS 1 2 8 3 7 4 6 5 1. 2. 3. 4. 5. Analyzes transactions Journalize Post Prepare work sheet Prepare financial statements 6. Journalize adjusting and closing entries 7. Post adjusting and closing entries 8. Prepare post-closing trial balance