ABLE A Deeper Look at 4 New ABLE

Moderator:")

ABLE: A Deeper Look at 4 New ABLE Programs (MI, KY, OR, VA) Moderator: Michael Morris, J. D. Executive Director, National Disability Institute ablenrc. org

Slide 2 This webinar is brought to you by the ABLE National Resource Center and sponsored by ablenrc. org

Slide 3 Listening to the Webinar • The audio for today’s webinar is being broadcast through your computer. Please make sure your speakers are turned on or your headphones are plugged in. • You can control the audio broadcast via the audio broadcast panel • If you accidentally close the panel, you can re-open by going to the Communicate menu (at the top of the screen) and choosing Join Audio Broadcast ablenrc. org

If you do not have sound capabilities on your computer or prefer to listen by phone, dial: Slide 4 Listening to the Webinar, continued 1 -650 -479 -3207 1 -855 -244 -8681 (Toll-Free Number) Meeting Code: 660 066 350 Note: You do not need to enter an attendee ID. ablenrc. org

Slide 5 Captioning • Real-time captioning is provided during this webinar. • The captions can be found in Media Viewer panel, which appears in the lower-right corner of the webinar platform. • If you want to make the Media Viewer panel larger, you can minimize other panels like Chat, Q&A, and/or Participants. ablenrc. org

Slide 6 Submitting Questions • For Q&A: Please use the Q&A box to submit any questions you have during the webinar and we will direct the questions accordingly during the Q&A portion. • If you are listening by phone and not logged in to the webinar, you may also ask questions by emailing questions to nmatthews@ndi-inc. org. Please note: This webinar is being recorded and the materials will be placed on the ABLE National Resource Center website at: http: //www. ablenrc. org/events/deeper-look-4 -newable-programs ablenrc. org

Slide 7 Technical Assistance • If you experience any technical difficulties during the webinar, please use the chat box to send a message to the host NDI Admin, or you may also email nmatthews@ndi-inc. org. ablenrc. org

Slide 8 Moderator and Panelists • Moderator o Michael Morris, J. D. , Executive Director, National Disability Institute • Presenters o o o Chris Rodriguez, ABLE National Resource Center Scott de Varona, Mi. ABLE Program O. J. Oleka, STABLE Kentucky David Bell, Oregon ABLE Savings Plan Mary Morris, ABLEnow ablenrc. org

Slide 9 Agenda • ABLE Basics • State ABLE Presentations o Mi. ABLE Program o STABLE Kentucky o Oregon ABLE Savings Plan o ABLEnow • Questions and Answers ablenrc. org

Slide 10 The ABLE Act is Law The Stephen Beck, Jr. Achieving a Better Life Experience (ABLE) Act o became law on December 19, 2014 o creates a new option for some people with disabilities and their families to save for the future, while protecting eligibility for public benefits. Presentation is based on what we know or presume now ablenrc. org

Slide 11 What is an ABLE Account? • • ABLE accounts: o Are established in the new Section 529 A Qualified ABLE Programs o Are qualified savings accounts that receive preferred federal tax treatment o Enable eligible individuals to save for disability related expenses o There are currently 16 ABLE programs enrolling qualified individuals (most of which are enrolling nationwide) Assets in and distributions for qualified disability expenses will be disregarded or given special treatment in determining eligibility for most federal means-tested benefits ablenrc. org

Slide 12 What are some important requirements of ABLE accounts? • • Each eligible individual may have only one ABLE account. • There is no longer a federal residency requirement related to establishing an ABLE account (unless otherwise established by a given program, ). • Total annual contributions may not exceed the federal gift tax contribution, which is currently $14, 000 (this will periodically be adjusted for inflation). • • Multiple individuals may make contributions to an ABLE account. “Designated beneficiary” is the account owner (although another person such as a parent or guardian may be allowed signature authority over the account). Aggregate contributions may not exceed the state limit for 529 savings accounts, typically set at over $250, 000. ablenrc. org

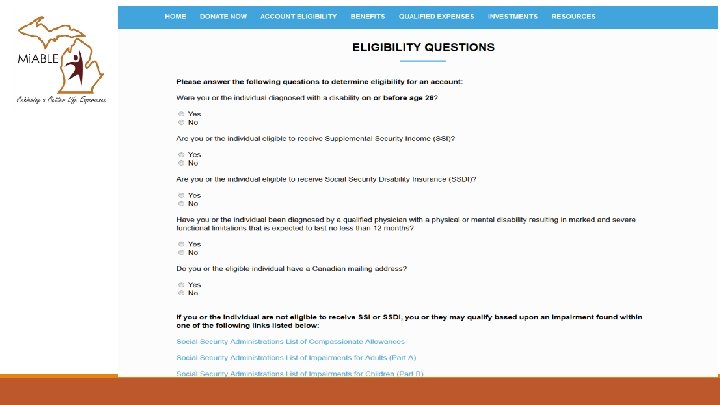

Slide 13 Who is eligible to be an ABLE account beneficiary? To be eligible, individuals must meet two requirements: 1) Age requirement: must be disabled before age 26 2) Severity of disability: • Have been determined to meet the disability requirements for Supplemental Security Income (SSI) or Social Security disability benefits (Title XVI or Title II of the Social Security Act) and are receiving those benefits, OR • Submit a “disability certification” assuring that the individual holds documentation of a physician’s diagnosis and signature, and confirming that the individual meets the functional disability criteria in the ABLE Act (related to the severity of disability described in Title XVI or Title II of the Social Security Act)*. ablenrc. org

Slide 14 What may funds from an ABLE account be used for? • • • Distributions from an ABLE account may be made for “qualified disability expenses”. “Qualified disability expenses” are expenses that relate to the designated beneficiary’s blindness or disability and are for the benefit of that designated beneficiary in maintaining or improving his or health, independence, or quality of life. The term “qualified disability expenses” should be broadly construed to permit the inclusion of basic living expenses and should not be limited to: • • expenses for items for which there is a medical necessity, or which provide no benefits to others in addition to the benefit to the eligible individual. ablenrc. org

o o o Education Housing Transportation Employment training and support Assistive technology and personal support services Health, prevention, and wellness Financial management and administrative services Legal fees Expenses for oversight and monitoring Basic Living Expenses (NPRM) Funeral and burial expenses Any other expenses approved by the Secretary of the Treasury under regulations consistent with the purpose of the program Distributions for non-qualified expenditures will be subject to tax consequences and may affect eligibility for federal means tested benefits. ablenrc. org Slide 15 Qualified disability expenses may include the following:

Slide 16 How do ABLE account assets impact eligibility for federal benefits? ABLE assets will be disregarded or receive favorable treatment when determining eligibility for most federal means-tested benefits: • Supplemental Security Income(SSI): For SSI, only the first $100, 000 in ABLE account assets will be disregarded. • SSI payments (monthly cash benefit) will be suspended if the beneficiary’s account balance exceeds $100, 000, but SSI benefits (eligibility) will not be terminated. Funds above $100, 000 will be treated as resources. • Housing expenses intended to receive the same treatment as all housing costs paid by outside sources. However, new SSA instructions (POMS) will treat housing expenses as resources only if distributed in one month and held until the following month. (more later) ablenrc. org

• Medicaid: ABLE assets are disregarded")

Slide 17 Impact on Federal Benefits (cont. ) • Medicaid: ABLE assets are disregarded in determining Medicaid eligibility o Medicaid benefits are NOT suspended if the ABLE account balance exceeds $100, 000 (that is only applicable to the SSI cash benefit) o Medicaid Payback: Any assets remaining in the ABLE account when a beneficiary dies, subject to outstanding qualified disability expenses, can be used to reimburse a state for Medicaid payments made on behalf of the beneficiary after the creation of the ABLE account (the state would have to file a claim for those funds)* o For purposes of this section, the state is considered a creditor of the ABLE account, not a beneficiary ablenrc. org

is")

Slide 18 ABLE National Resource Center • The ABLE National Resource Center (ANRC) is a collaborative whose supporters share the goal of accelerating the design and availability of ABLE accounts for the benefit of individuals with disabilities and their families. We bring together the investment, support and resources of the country’s largest and most influential national disability organizations. Chris Rodriguez Senior Public Policy Advisor National Disability Institute crodriguez@ndi-inc. org www. ablenrc. org

Aggressive (More Risk) Investment Costs (%) 0. 17 % 0. 19%")

Conservative (Less Risk) Aggressive (More Risk) Investment Costs (%) 0. 17 % 0. 19% 0. 22% 0. 25% 0. 28%

Mi. ABLE Account Features • National Enrollment • Michigan State Income Tax Deduction • Annual Fee: $45. 00 ($11. 25 quarterly) • 5 Investment Options of Various Risk & Costs • FDIC insured account • Debit Card • Optional Public Profile

Mi. ABLE Program Information Statewide Mi. ABLE Outreach is continuing and ongoing Mi. ABLE@michigan. gov Like at Facebook: https: //www. facebook. com/Michigan. ABLE/ Subscribe to our newsletter: www. Michigan. gov/miable Customer Service: 844 -656 -7225

STABLE Kentucky: Kentucky’s ABLE Plan stablekentucky. com

What is ABLE? § Federal legislation passed 2014 § Creates tax-advantaged investment accounts for individuals with disabilities § § Assets in your account do not affect eligibility for federal [or Kentucky] means-tested benefits programs like SSI or Medicaid Hybrid of 529 college savings account + checking account + Special Needs Trust

What is STABLE Kentucky? § STABLE Kentucky is Kentucky’s ABLE Plan § Offered to Kentuckians through a partnership with the Ohio STABLE Account program § Administered by Treasurer of Kentucky, Allison Ball § Launched December 13, 2016

Benefits of Kentucky STABLE Accounts § Provides financial independence for people with disabilities § Account is owned by the individual with the disability § Dramatically increases ability to save § Before ABLE , individuals could only save around $2, 000 of their own money before risking loss of health care and other benefits § Provides new investment opportunity § Tax free earnings – federal

Who Can Have a Kentucky STABLE Account? § Eligibility Quiz at stablekentucky. com § Individuals with disabilities that occurred prior to age 26 § Must be a Kentucky resident § Limit of 1 Account person § Three paths to eligibility: 1. 2. 3. Eligible to receive SSI or SSDI due to disability Have a condition listed on SSA’s “List of Compassionate Allowances Conditions” Self-certification

Select your eligibility criteria 2) If self-certifying… § Need diagnosis of")

Eligibility Certifications 1) Select your eligibility criteria 2) If self-certifying… § Need diagnosis of a physical or mental impairment that causes “marked and severe functional limitations” Ø Such as conditions in the SSA’s Blue Book § Certify that the condition has lasted or is expected to last for at least 1 year § Input physician name, address, date of diagnosis § Do not need to send in written diagnosis, but must have on hand 3) Permanent Disability? Answer “yes” to prevent need for annual re-certification

Enrollment § Online Enrollment § Free - takes approx. 20 minutes § Can be done by individual with disability (“Beneficiary”) or an Authorized Legal Representative (ALR) § ALR = parent, guardian, power of attorney

Funding your Account § § Contributions § Via Electronic Funds Transfer or check § $14, 000 annual limit § $426, 000 lifetime limit § System automatically rejects excess contributions Gifting § Create an e. Gift Event (birthday, holiday, etc. ) ~ system will send out an email to friends and family § System tracks contributors for sending thank-you notes/replies

Investment Options § Four Vanguard mutual funds that range from aggressive to conservative § One FDIC-Insured Option Ø Principal protected

How Can You Spend STABLE funds? § Withdrawals must be used on “Qualified Disability Expenses” Ø Anything that (1) relates to your disability and (2) helps to maintain or improve your health, independence, or quality of life Examples: § Housing and Rent § Basic Living Expenses § Medical Bills § Education § Transportation § Assistive Technology

Non-Qualified Expenditures § Not illegal, but there are consequences Affects Benefits Ø The amount of the expenditure may now be considered a countable resource (but not necessarily) Tax Penalties Ø Pay taxes plus 10% penalty on the earnings portion of the withdrawal Ø Ex: You contribute $90 to your account, and you make $10 in earnings – your balance is now $100. You withdraw that $100 but do not use it for a QDE. You must pay regular income tax on the $10 of earnings, plus an additional 10% penalty on those same earnings.

Spending From Your Account Withdrawals § Free + No Limits § STABLE Kentucky will not ask what you spend on, but benefits agencies and IRS can § Transfer to personal checking or savings § Transfer to STABLE Card

STABLE Card § Loadable debit card § Does not pull from account § Online spending records + notate expenses § No commingling of funds with other accounts § Protection – limiting of merchants, no cash access, no overdraft

SSI Considerations § Balances over $100, 000 count as a resource – but SSI merely suspended, not terminated § Beneficiary’s own wages still count as income even if contributed to Kentucky STABLE Account § If you hold on to the money from one calendar month to the next, then housing expenditures and non-qualified expenditures count as resources

Medicaid Considerations § Unlike with SSI, your account balance will not affect Medicaid benefits regardless of the amount § If Beneficiary was on Medicaid and passes away, Medicaid can ask for payback… BUT! First, you can: Ø Ø Ø § Pay any outstanding bills for QDEs Pay for funeral and burial expenses Deduct Medicaid Buy-In premiums you paid Payback is only from date the account was opened

Account Cost § Online Enrollment is free § $50. 00 minimum deposit to open account § $1. 00 minimum for all subsequent deposits Monthly Maintenance Fees Asset-based Fees $5. 00 ($60. 00 Annually) Between 0. 19% and 0. 33% (same as OH residents)

STABLE vs. Special Needs Trust § Complement, not competition, but… § Some benefits specific to STABLE Accounts: Ø Cost-Effective Ø Broader spending power (i. e. housing) Ø Easy account access/closure Ø No federal income tax on earnings Ø No separate returns to file Ø Can be established, administered, and owned by individual with disability

Helpful Resources Customer Service team@stableaccount. com 1 -800 -439 -1653 Mon-Fri 9 a-6 p EST stablekentucky. com

Spread the Message Find us on Facebook: @Treasurer. Ball Find us on Twitter: @KYTreasurer Help us spread the STABLE Kentucky message. Follow us, “like” us, and send us your thoughts.

David Bell, Oregon 529 Savings Network

Cash Option Conservative Moderate Aggressive

� � $22. 50 Annual Fee 0. 30% to 0. 38% Annual Asset Fee � � $55 Annual Fee 0. 30% to 0. 38% Annual Asset Fee

David Bell 503 -431 -7929 david. bell@ost. state. or. us oregon. ABLEsavings. com & ABLEfor. ALL. com @Oregon. ABLE & @ABLEfor. ALL

Presenter: Mary Morris CEO, ABLEnow

What is ABLEnow? • ABLEnow℠ is the Virginia-sponsored ABLE savings program. • Open to eligible individuals nationwide, regardless of state residency. • ABLEnow is administered by Virginia 529℠, the country’s largest college savings plan, which has a newly expanded mission to meet the savings needs of persons with disabilities. 54

ABLEnow Card ABLEnow account holders receive the ABLEnow Card— a debit card providing a simple, fast way to pay qualified disability expenses. 55

Investment Options The first $2, 000 in your ABLEnow account is automatically allocated to the ABLEnow FDIC-insured Deposit Account, which is linked to your ABLEnow Card. Once the balance in the ABLEnow Deposit Account exceeds $2, 000, you may opt to invest additional contributions into one or more of these investment portfolios. 56

Account Costs There are minimal costs associated with maintaining your account, and ABLEnow offers some of the lowest fees in the country among ABLE programs. No enrollment fee No minimum contribution Account service fee is $3. 25 per month If the Account Owner or Authorized Representative chooses to invest some of the funds, there also asset-based fees between 0. 37% and 0. 40%, depending on investment selections • Monthly fee is waived for accounts maintaining a balance over $10, 000 in the deposit account. • • 57

Compare ABLE programs The ABLEnow program: • • • Competitive, low fees Straightforward account opening Ease of use – contributions and payments FDIC-insured interest bearing Deposit Account Four investment options after Deposit Account threshold is met State income tax advantages for Virginians 58

Receive & share information • Visit able-now. com and subscribe to updates • Follow @ABLEnow. VA on Facebook and Twitter • Help spread the word! Please share information about ABLEnow with friends, family and community groups. 59

Questions? able-now. com customerservice@able-now. com Toll Free: 1 -844 -NOW-ABLE The material in this presentation has been prepared by ABLEnow and is general information about ABLEnow current as of the date of this presentation. The information is given in summary form and does not purport to be complete. Call 1 -844 -NOW-ABLE or visit able-now. com to obtain information on the program. Seek the advice of a professional concerning any financial, tax, legal or federal or state benefit implications related to opening and maintaining an ABLEnow account. Participating in ABLEnow involves investment risk including the possible loss of principal. For non-Virginia residents: other states may sponsor an ABLE plan that offers state tax or other benefits not available through ABLEnow. © 2017 Virginia College Savings Plan. All Rights Reserved. 60

is")

Slide 61 ABLE National Resource Center • The ABLE National Resource Center (ANRC) is a collaborative whose supporters share the goal of accelerating the design and availability of ABLE accounts for the benefit of individuals with disabilities and their families. We bring together the investment, support and resources of the country’s largest and most influential national disability organizations. Chris Rodriguez Senior Public Policy Advisor National Disability Institute crodriguez@ndi-inc. org www. ablenrc. org

- Slides: 62