A Quantitative Approach Global Asset Allocation Term 3

…A Quantitative Approach Global Asset Allocation Term 3, 2005 Matthew Morse Jason Teeters J. J. Haines

Overview • Hypothesis: – Develop a market-neutral long/short strategy – Motivated by a “pairs trading” strategy which is designed to hedge industry specific risk – Identify a dynamic portfolio strategy which outperforms a general pairs trading strategy through the creation of a “basket” of securities – Industry-specific long and short “baskets” are identified on a monthly basis through a screen of targeted fundamental factors – Identify industry sectors which consistently produce excess returns

Overview • Methodology: – Identify industries and potential fundamental factors – Screen and alpha test individual factors across industry sectors – Score and combine individual factors – Alpha test combined industry long/short “baskets” – Evaluate which industries produce consistent excess returns – Evaluate trading strategies

Industries • • • Communications Manufacturing Transportation Consumer Healthcare

Screens • Factors: Short Interest - total short positions currently open for a given equity as a percentage of total shares Fundamental Debt Factor - incorporates information about cost of debt and leverage ratio Change in Consensus – Percent change in EPS estimate (IBES)

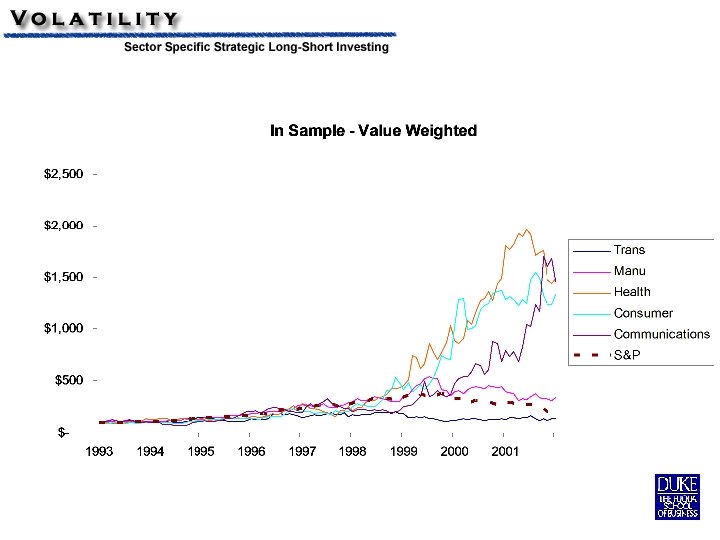

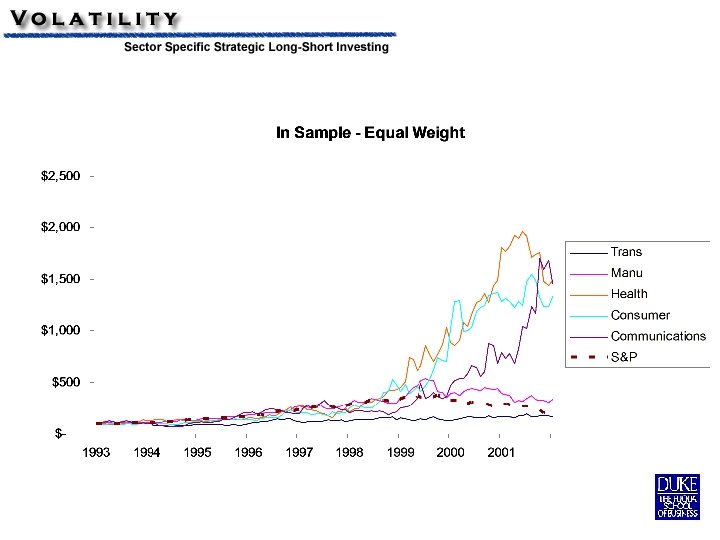

In Sample

Healthcare Communication Consumer Products

Manufacturing Transportation

Healthcare – In Sample

Communications – In Sample

Consumer – In Sample

Manufacturing – In Sample

Transportation – In Sample

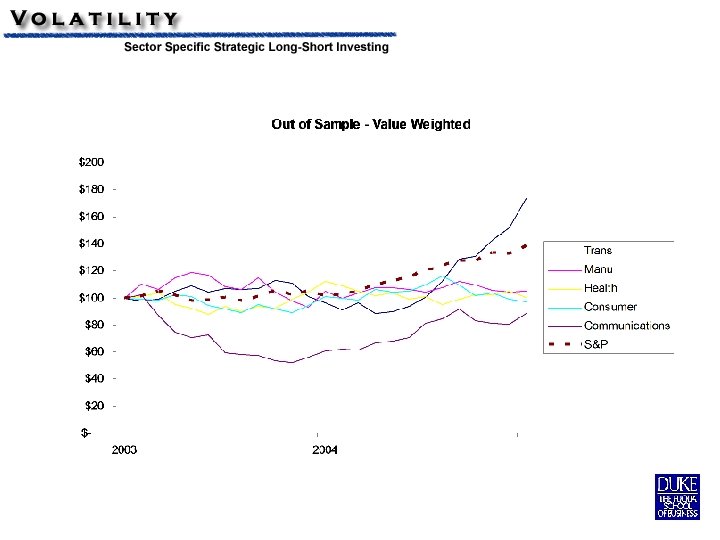

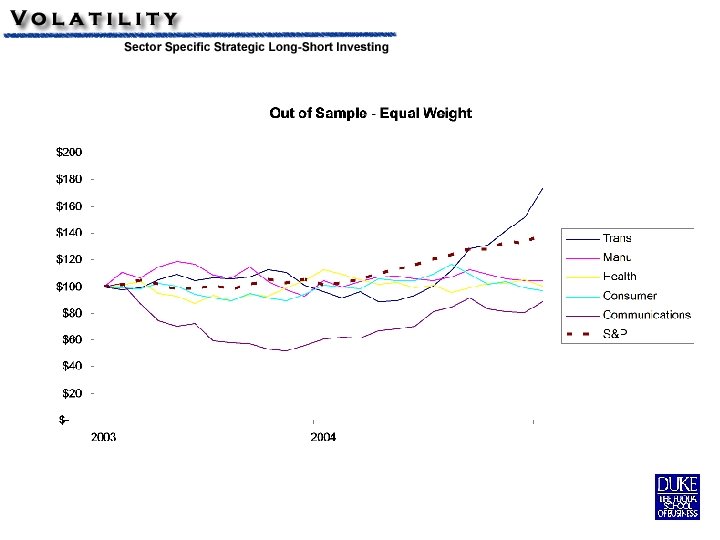

Out of Sample

Healthcare Communication Consumer Products

Manufacturing Transportation

Healthcare – Out Sample

Communications – Out Sample

Consumer – Out Sample

Manufacturing – Out Sample

Transportation – Out Sample

Optimization

Optimization Value Weighted Equal Weighted

Conclusions • Intra-sector excess returns appear to be consistently available • Inconsistent “in-sample” and “out-ofsample” results within certain industry sectors • Additional analysis should lead to effective factors which could consistently produce intra-sector excess returns

Next Steps • Develop and evaluate additional factors which isolate industry specific excess returns • Test additional industry sectors and sub-sectors in-sample • Vary factors weights across industries • Evaluate migration of stocks within fractiles • Develop and evaluate sector-specific, and overall, trading strategies as part of an overall hedge fund charter

- Slides: 29