9 10 II u tangible intangible service loan

9

10

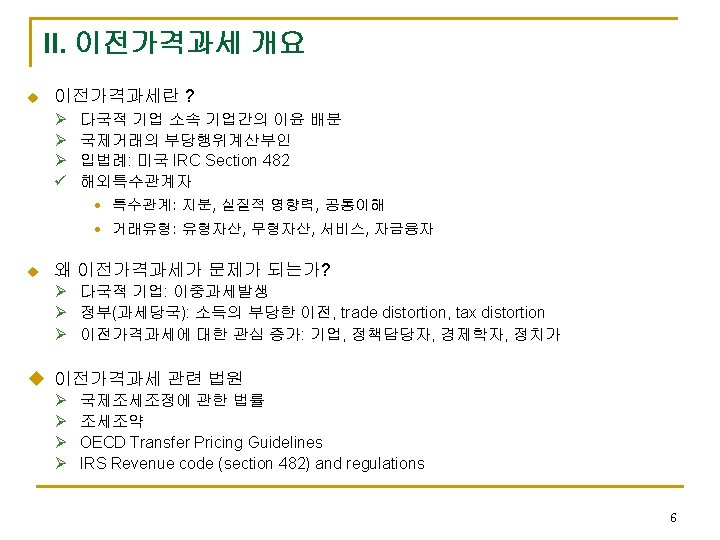

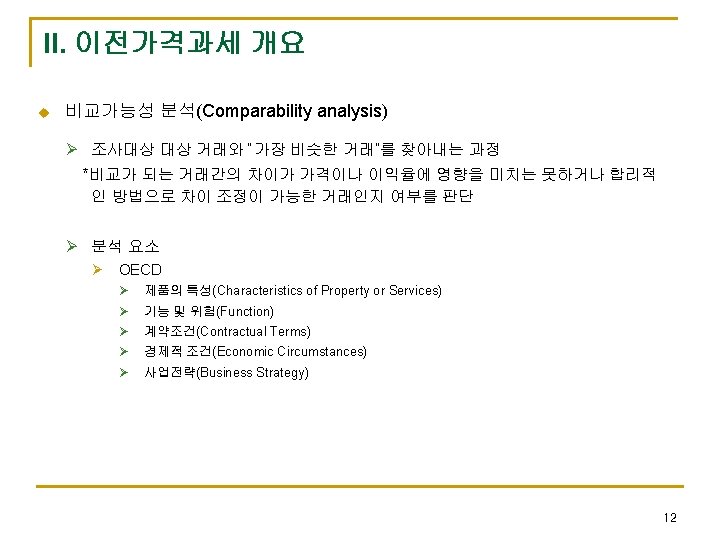

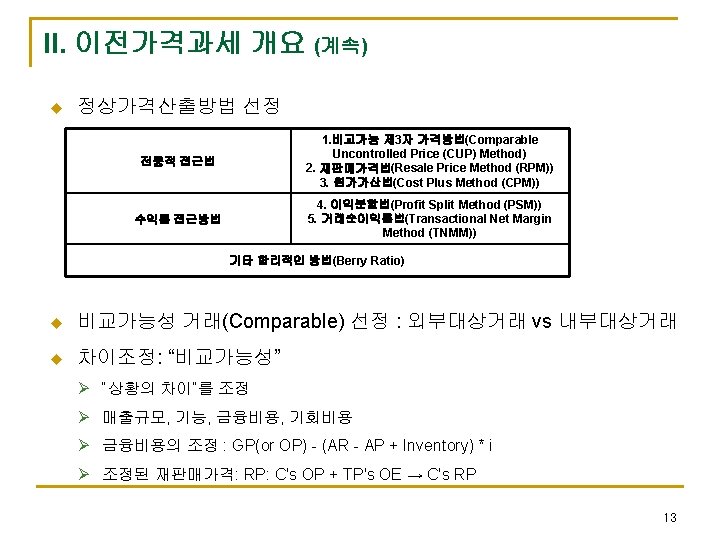

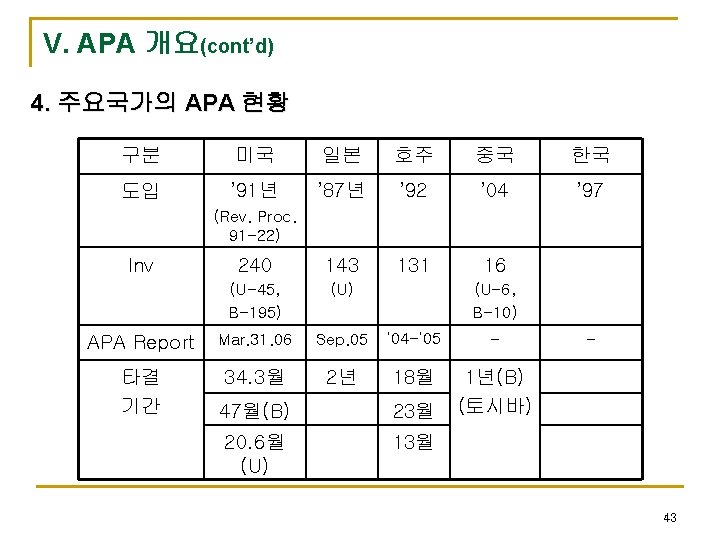

II. 이전가격과세 개요 u 이전가격과세요건 Ø 해외특수관계자간 정상가격을 벗어난 거래 • 특수관계: 출자지분, 실제 경제적 관계, 공통의 이해 • 거래형태: 유형재와, 무형재화, 서비스, 자금융자(tangible, intangible, service, loan) <Article 9 of the OECD Model Convention> When conditions are made or imposed between two associated enterprises in their commercial or financial relations, which differ from those which would be made between independent enterprises, then any profits which would, but for those conditions, have accrued to one of the enterprises, but, by reason of those conditions, have not so accrued, may be included in the profits of that enterprise and taxed accordingly. (Arm’s length principle) u 정상가격원칙(Arm’s length principle) Ø 특수관계가 없는 자간의 거래 Ø 비교가능성이 있는 거래 11

u 비교가능 제 3자 가격법(Comparable uncontrolled price, CUP) Ø Ø")

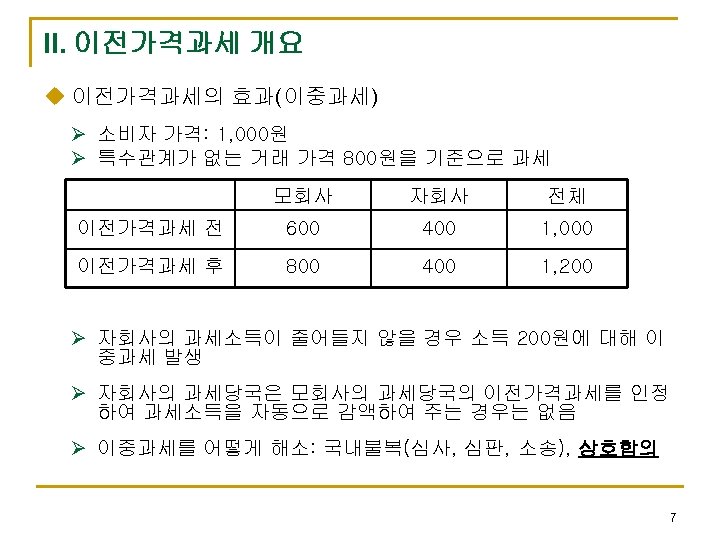

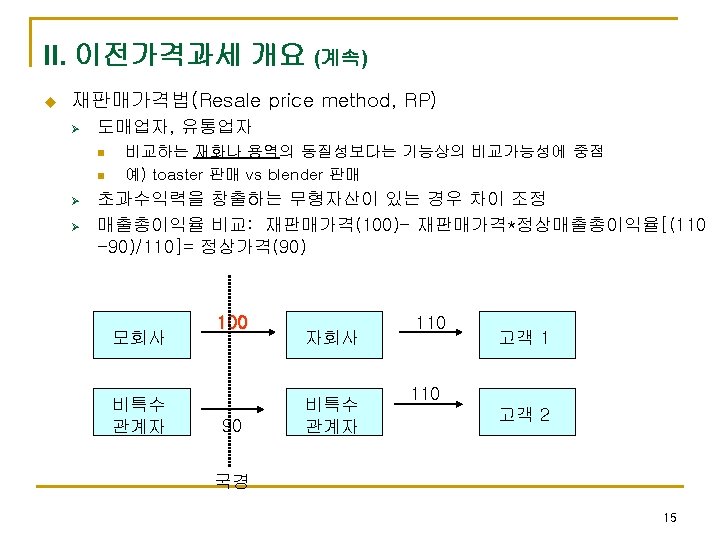

II. 이전가격과세 개요 (계속) u 비교가능 제 3자 가격법(Comparable uncontrolled price, CUP) Ø Ø 가장 신뢰할 수 있는 방법(OECD TP Guideline), 적용가능성이 매우 낮음 n 전제조건 : 비교하는 재화나 용역의 동질성 n 예) unbranded Colombian coffee beans vs unbranded Brazilian coffee bean (2. 11) Internal comparable vs External comparable 모회사 100 자회사 110 고객 1 80 비특수 관계자 90 국경 비특수 관계자 110 고객 2 14

IV. OECD와 이전가격과세 1. 개요 n Background on the OECD Transfer Pricing Guidelines n Comparability Issues n Profits Method Issues n Attribution of Profits to Permanent Establishments n Tax Issues Relating to Business Restructurings n Improving Dispute Resolution Mechanisms 25

IV. OECD 와 이전가격과세 2. OECD Transfer Pricing Guidelines q q q 1979: Transfer Pricing and Multinational Enterprises 1984: 3 Taxation issues 1995 to 1999: revision of the 1979 report I. The arm’s length principle II. Traditional transactional methods III. Profit methods IV. Administrative approaches V. Documentation VI. Intangible property VII. Intra-group services VIII. Cost Contribution Arrangements Annexes: Guidelines for Advance Pricing Agreements (…) 26

IV. OECD 와 이전가격과세 3. Comparability issues n WP 6 looking at comparability as part of its monitoring of 1995 Transfer Pricing Guidelines n Comments were solicited during 2003 – significant response received n Series of “Issue Notes” on comparability issues to be publicly released in first half of 2006 n Likely to be followed by business consultation 27

Examples of issues under consideration: n Use")

IV. OECD 와 이전가격과세 3. Comparability issues(계속) Examples of issues under consideration: n Use of data obtained post-transaction n Use of multiple year data n Determining available sources of info and their reliability (e. g. secret comparables, databases) n Aggregation of transactions n Lack of data on uncontrolled transactions n Obtaining info on the 5 comparability factors 28

Examples of issues under consideration: n Selecting")

IV. OECD 와 이전가격과세 3. Comparability issues(계속) Examples of issues under consideration: n Selecting or rejecting third parties or third party transactions n Making comparability adjustments n Defining the arm’s length range n Documenting a search for comparables n Internal versus external comparables n Putting a comparability analysis and search for comparables into perspective 29

IV. OECD 와 이전가격과세 4. Business Restructurings n n January 2005 CTPA Roundtable on topic Joint WP 1 -WP 6 Working Group formed in 2005 Considering tax treaty and transfer pricing aspects of business restructurings Focus is on risk stripping, e. g. : q q Converting full-fledged distributor to commissionaire Converting full-fledged manufacturer to contract or toll manufacturer 30

Transfer pricing issues under consideration, such as:")

IV. OECD 와 이전가격과세 4. Business Restructurings(계속) Transfer pricing issues under consideration, such as: n n n To what extent can tax administrations disregard/recharacterize taxpayers’ contracts? Which member of MNE group bears termination costs? Is risk-stripped entity entitled to any indemnification? Is remuneration required for transfers of “business opportunity”? How to value transfers of assets (e. g. , customer lists, knowhow, goodwill) 31

Transfer pricing issues (cont’d): n n Does")

IV. OECD 와 이전가격과세 4. Business Restructurings(계속) Transfer pricing issues (cont’d): n n Does conversion result in arm’s length allocation of risks? How to determine arm’s length remuneration for risk-stripped entity postconversion? How to allocate efficiency gains derived from restructuring? What documentation requirements should apply? Next steps: n n n Joint WP 1 -WP 6 Working Group to continue in 2006 -2007 Likely to develop draft issues notes for public release in 2007 -2008 Public consultation likely to follow 32

IV. OECD 와 이전가격과세 5. Improving Dispute Resolution Mechanisms n n n Important work underway to improve MAP process Complements OECD’s standard-setting role on Model Treaty, Transfer Pricing Guidelines Country profiles created on OECD website in March 2004 July 2004 Progress Report from CFA on “Improving the Process for Resolving International Tax Disputes” made over 30 proposals February 2006 Public Discussion Draft is the follow-up 33

Key proposals in February 2006")

IV. OECD 와 이전가격과세 5. Improving Dispute Resolution Mechanisms(계속) Key proposals in February 2006 Discussion Draft: n n n New paragraph in Article 25 for mandatory arbitration of unresolved MAP cases Proposed changes to Article 25 Commentary to incorporate proposals for improved MAP operation Online “Manual for Effective Mutual Agreement Procedures” (MEMAP) to explain MAP and describe best practices for tax authorities and taxpayers Supplementary Dispute Resolution Proposal: n n Mandatory, binding arbitration of Article 25(1) cases unresolved after 2 years of MAP Mode of application left to mutual agreement of Contracting States Sample mutual agreement on procedures included in proposal Proposal recognizes not all countries are in a position to include this procedure 34

Proposed changes to Article 25")

IV. OECD 와 이전가격과세 5. Improving Dispute Resolution Mechanisms(계속) Proposed changes to Article 25 Commentary: n Clarify time limitations for invoking MAP n Clarify triggers for MAP access n Clarify (and limit) grounds for denying access n Encourage suspension of collection during MAP n Encourage appropriate treatment of interest and penalties n Encourage use of MAP to make corresponding adjustments n Clarify relationship with domestic law, to encourage full use of MAP 35

Proposed MEMAP website: n n")

IV. OECD 와 이전가격과세 5. Improving Dispute Resolution Mechanisms(계속) Proposed MEMAP website: n n Draft now available online at www. oecd. org/ctp/memap Provides general background on MAP Sets out non-binding guidelines for “best practices” by competent authorities Encourages transparency, timeliness, broad access, principled approaches Next steps: n n Public consultation in Tokyo on 13 March 2006 Comments on public discussion draft due 30 April 2006 Comments on proposed MEMAP due 30 June 2006 Target for completion: January 2007 36

V. APA 개요 <Korea> ② MAP NTS ① APA Application <Country A> ③ APA Approval Korean Taxpayer Country A Authority ① APA Application ④ Apply agreed method Country A Related Party <Explanation> ① APA Application : By the end of the first year of the APA period (no application fees) ② NTS notifies taxpayer within 15 days following completion of the MAP ③ APA Approval : APA approval effective upon the taxpayer’s acceptance of the MAP contents ④ Upon APA approval, the taxpayer files corporate tax returns in accordance with APA 41

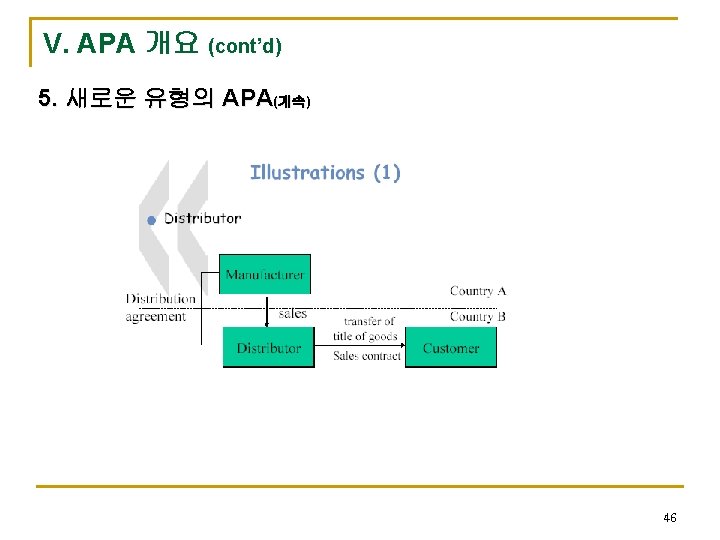

5. 새로운 유형의 APA u Commissionaire and Stripped Distributor u")

V. APA 개요 (cont’d) 5. 새로운 유형의 APA u Commissionaire and Stripped Distributor u Toll Manufacturer u Global Dealing(Financial Transaction) u Profit Split Method u Contribution Factors u Value Factor(Compensation to trader) u Risk Factor(Risk assumed) u Activity Factor(Volume of transaction) 44

5. 새로운 유형의 APA(계속) Commissionaires and Stripped Distributor 45")

V. APA 개요 (cont’d) 5. 새로운 유형의 APA(계속) Commissionaires and Stripped Distributor 45

47")

V. APA 개요 (cont’d) 47

48")

V. APA 개요 (cont’d) 48

5. 새로운 유형의 APA u Commissionaire and Tax Issues Ø")

V. APA 개요 (cont’d) 5. 새로운 유형의 APA u Commissionaire and Tax Issues Ø Ø PE Issue ü Substance-over-form interpretation(acting on behalf of another) ü Strict interpretation of agency law(“Conclude contracts in the name of”…) TP Issues ü Recognition of the Commissionaire arrangement ü Remuneration of the Commissionaire based on analysis of its functions, risks and assets ü Conversion of a distributor into a Commissionaire(transfer of intangibles) 49

- Slides: 49