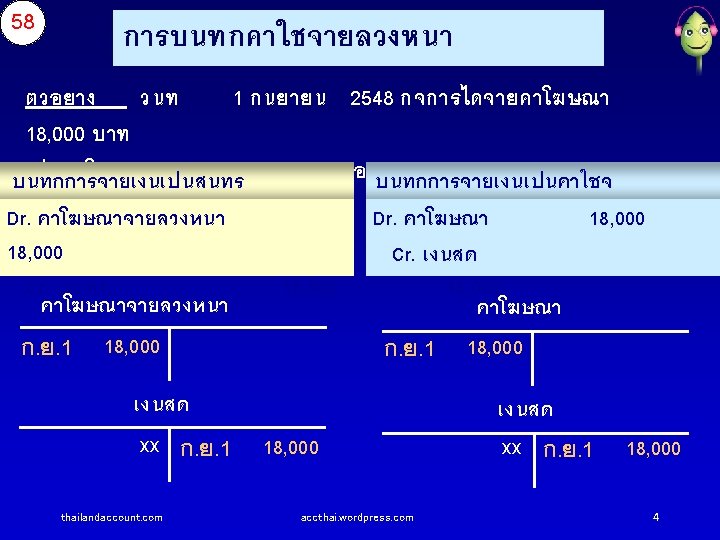

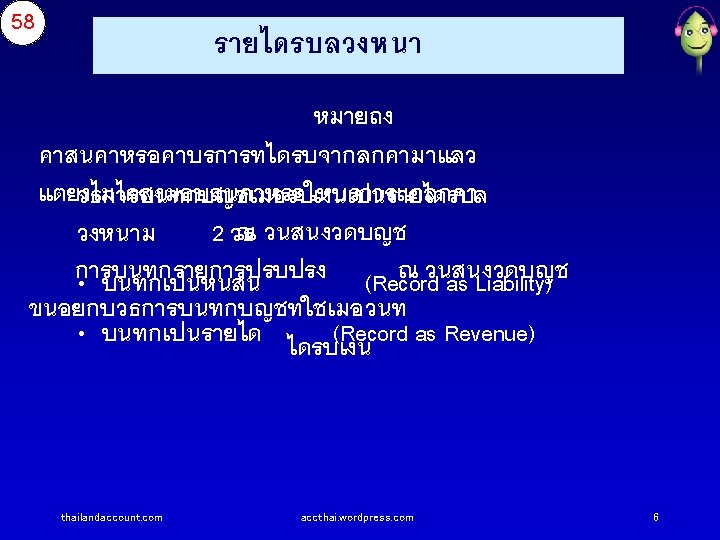

4 Adjusting Entries and Preparing The Financial Statement

วสดสนเปลอง Dec. 31 Bal. 60, 000")

= 12, 000 คดคาเสอมราคาอปกรณ 20%")

คาสาธารณปโภคคางจาย ( Dec. 31 Adj.")

เงนสด")

สนทรพย ( Cash")

หนสนและสวนของเจาของ ( Baht Liabilities )หนสน ): Accounts Payable )เจาหน")

- Slides: 40

บทท 4 รายการปรบปรงและ การจดทำงบการเงน Adjusting Entries and Preparing The Financial Statement Created by Amzy R. Nirvana

คาเสอมราคา Assets 1 ม. ค. 48 31ธ. ค. 49 310, 000 250, 000 190, 000 60, 000 31ธ. ค. 51 31ธ. ค. 52 130, 000 60, 000 70, 000 10, 000 60, 000 Expenses thailandaccount. com accthai. wordpress. com 12

67 รายการปรบปรงรายการท วสดสนเปลองคงเหลอ 1 15, 000 บาท Supplies )วสดสนเปลอง Dec. 31 Bal. 60, 000 Balance 15, 000 Dec. 31 Adj. (1) Supplies Expense )คาวสดสนเปลองใชไป Dec. 31 Adj. (1) 45, 000 ( 45, 000 Bal. (Balance) คงเหลอ thailandaccount. com ( Adj. (Adjustment) ปรบปรง accthai. wordpress. com 17

68 รายการปรบปรงรายการท 3 240, 000 * 20% * (3/12) = 12, 000 คดคาเสอมราคาอปกรณ 20% ตอป อปกรณซอมาเมอ Equipment 1 ต. ค. 2548 ( )อปกรณ Dec. 31 Bal. 240, 000 Accumulated Depreciation )คาเสอมราคาสะสม Dec. 31 Adj. (3) Depreciation Expense )คาเสอมราคา Dec. 31 Adj. (3) thailandaccount. com ( 12, 000 accthai. wordpress. com 19

68 รายการปรบปรงรายการท คาสาธารณปโภคคางจาย 4 10, 000 บาท Utilities Payable )คาสาธารณปโภคคางจาย ( Dec. 31 Adj. (4) 10, 000 Utilities Expense )คาสาธารณปโภค ( Dec. 31 Bal. 16, 000 Dec. 31 Adj. (4) 10, 000 Balance thailandaccount. com 26, 000 accthai. wordpress. com 20

68 รายการปรบปรงรายการท ตงคาเผอหนสงสยจะสญ 5 200, 000 * 5% = 10, 000 5% ของยอดลกหน Accounts Receivable )ลกหน Dec. 31 Bal. 200, 000 ( Allowance for Doubtful Debt )คาเผอหนสงสยจะสญ Dec. 31 Adj. (5) ) Doubtful Debt Expense )หนสงสยจะสญ Dec. 31 Adj. (5) thailandaccount. com 10, 000 ( 10, 000 accthai. wordpress. com 21

69 Niroth – Accounting Adjusted Trial Balance, December 31, 2005 Account Titles Cash )เงนสด ( Accounts Receivable )ลกหน ) Allowance for Doubtful )คาเผอหนสงสยจะสญ ) Supplies )วสดสนเปลอง ) Prepaid Rent )คาเชาจายลวงหนา ( Equipment )อปกรณ ) Accumulated Depreciation) คาเสอมราคาสะสม Accounts Payable )เจาหน ( Utilities Payable )คาสาธารณปโภคคางจาย ( Capital )ทน ) thailandaccount. com accthai. wordpress. com Debit 412, 000 200, 000 Debt Credit 10, 000 15, 000 90, 000 240, 000 ) 12, 000 8, 000 10, 000 440, 000 22

69 Niroth – Accounting Adjusted Trial Balance, December 31, 2005 Account Titles Debit ……. …. งบกำไรขาดทน Withdrawal )ถอนใชสวนตว ( 300, 000 Revenue )รายได ( Salaries Expense )เงนเดอน ) 200, 000 Utilities Expense )คาสาธารณปโภค ( 26, 000 Supplies Expense 45, 000 )คาวสดสนเปลองใชไป ( Rent Expense )คาเชา ) 30, 000 Depreciation Expense )คาเสอมราคา ( 12, 000 Doubtful Debt Expense )หนสงสยจะสญ ( 10, 000 1, 580, 000 thailandaccount. com accthai. wordpress. com Credit …. 1, 100, 000 1, 580, 000 23

70 Niroth – Accounting Income Statement for 4 th Quarter, 2005 บาท Service Revenue )รายไดคาบรการ ( Expenses: Salaries Expense )เงนเดอน ) Utilities Expense )คาสาธารณปโภค ( Supplies Expense )คาวสดสนเปลองใชไป ( Rent Expense )คาเชา ) Depreciation Expense )คาเสอมราคา ( Doubtful Debt Expense )หนสงสยจะสญ ( thailandaccount. com accthai. wordpress. com 1, 100, 000 26, 000 45, 000 30, 000 12, 000 10, 000 323 , 000 24

69 Niroth – Accounting Adjusted Trial Balance, December 31, 2005 งบแสดงฐานะการเงน Account Titles Cash )เงนสด ( Accounts Receivable )ลกหน ) Allowance for Doubtful Debt )คาเผอหนสงสยจะสญ ) Supplies )วสดสนเปลอง ) Prepaid Rent )คาเชาจายลวงหนา ( Equipment )อปกรณ ) Accumulated Depreciation) คาเสอมราคาสะสม ) Accounts Payable )เจาหน ( Utilities Payable )คาสาธารณปโภคคางจาย ( Capital )ทน ) thailandaccount. com accthai. wordpress. com Debit 412, 000 200, 000 Credit 10, 000 15, 000 90, 000 240, 000 12, 000 8, 000 10, 000 440, 000 25

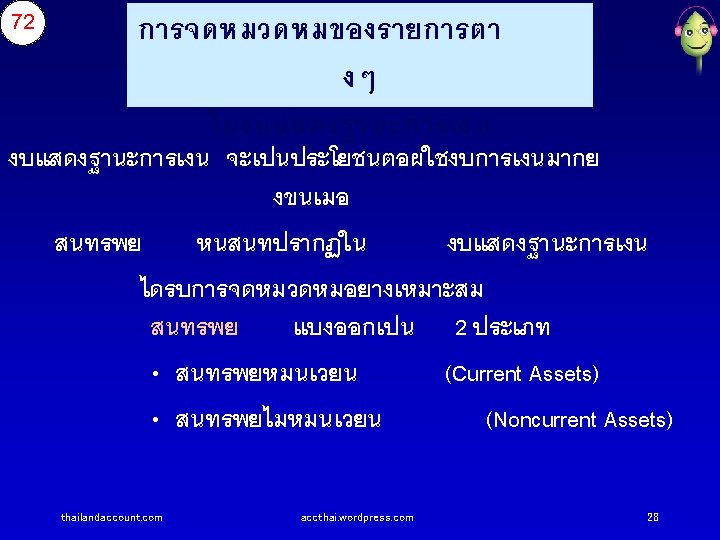

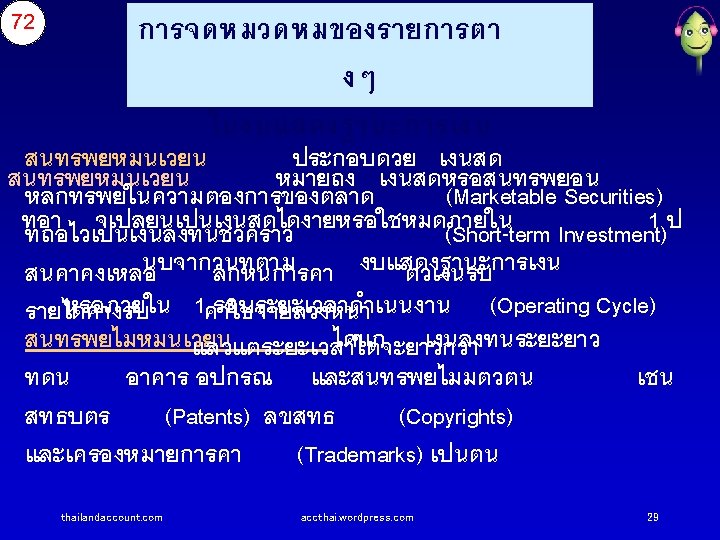

71 Niroth – Accounting Financial Position Statement, December 31, 2005 Assets )สนทรพย ( Cash )เงนสด ( Accounts Receivable )ลกหน ) Less Allowance for Doubtful Debt )คาเผอฯ ) Supplies )วสดสนเปลอง ) Prepaid Rent )คาเชาจายลวงหนา ( Equipment )อปกรณ ) Accumulated Depreciation )คาเสอมราคาสะสม ( Total Assets )รวมสนทรพย ( thailandaccount. com accthai. wordpress. com Baht 412, 000 200, 000 10, 000 240, 000 12, 000 190, 000 15, 000 90, 000 228, 000 935, 000 26

71 Liabilities and Owner’s Equity )หนสนและสวนของเจาของ ( Baht Liabilities )หนสน ): Accounts Payable )เจาหน ( Utilities Payable )คาสาธารณปโภคคางจาย ( Total Liabilities (รวมหนสน ( Owner’s Equity )สวนของเจาของ ): Capital, Beginning )ทนตนงวด ) 440, 000 Add Net Income )กำไรสทธ ) 777, 000 Total )รวม( 1, 217, 000 Less Withdrawal )ถอนใชสวนตว ( 300, 000 Total Owner’s Equity Total Liabilities and Owner’s Equity thailandaccount. com accthai. wordpress. com 8, 000 10, 000 18, 000 917, 000 935, 000 27

thailandaccount. com accthai. wordpress. com 31

thailandaccount. com accthai. wordpress. com 32

thailandaccount. com accthai. wordpress. com 33

thailandaccount. com accthai. wordpress. com 34

thailandaccount. com accthai. wordpress. com 35

thailandaccount. com accthai. wordpress. com 36

thailandaccount. com accthai. wordpress. com 37

thailandaccount. com accthai. wordpress. com 38

thailandaccount. com accthai. wordpress. com 39