3 2 Black and Cox Model The original

3. 2 Black and Cox Model • The original Merton model does not allow for a premature default, in the sense that the default may only occur at the maturity of the claim. • In most of these models, the time of default is given as the first passage time of the value process V to a deterministic or random barrier. The default may thus occur at any time before or on the bond's maturity date T.

First passage model Merton model FPM P T 3

3. 2 Black and Cox Model • The challenge here is to appropriately specify the lower threshold v, the recovery process Z, and to compute the corresponding functional that appears on the right hand side of (2. 3).

3. 2 Black and Cox Model • The practical problem of the lack of direct observations of the value process V largely limits the applicability of the first passage time models. • In most cases examined below, the default time is denoted by τ; the symbols , and being reserved to some auxiliary random times.

extend Merton's")

3. 2. 1 Corporate Zero Coupon Bond • Black and Cox (1976) extend Merton's (1974) research in several directions. • In particular, they make account for specific features of debt contracts as: safety covenants debt subordination restrictions on the sale of assets. • Assume: the firm's stockholders (or bondholders) receive a continuous dividend payment, proportional to the current value of the firm.

3. 2. 1 Corporate Zero Coupon Bond • κ: constant κ≥ 0 , the payout ratio : >0 , the constant volatility coefficient : , the short term interest rate is assumed to be non random, specifically, where r is a constant. →interest rate risk is disregarded in the original Black and Cox (1976) model

3. 2. 1 Corporate Zero Coupon Bond Safety covenants • Safety covenants provide the firm’s bondholders with the right to force the firm to bankruptcy or reorganization if the firm is doing poorly according to a set standard. • The standard for a poor performance is set in Black and Cox (1976) in terms of a time dependent deterministic barrier for some constants K, > 0.

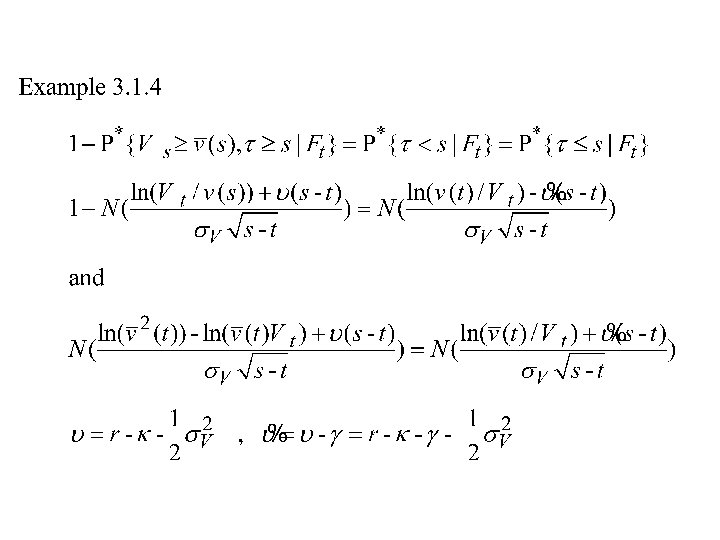

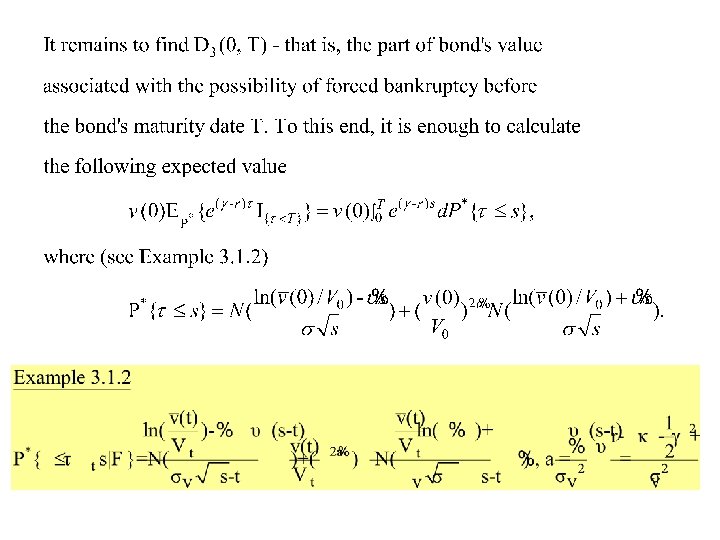

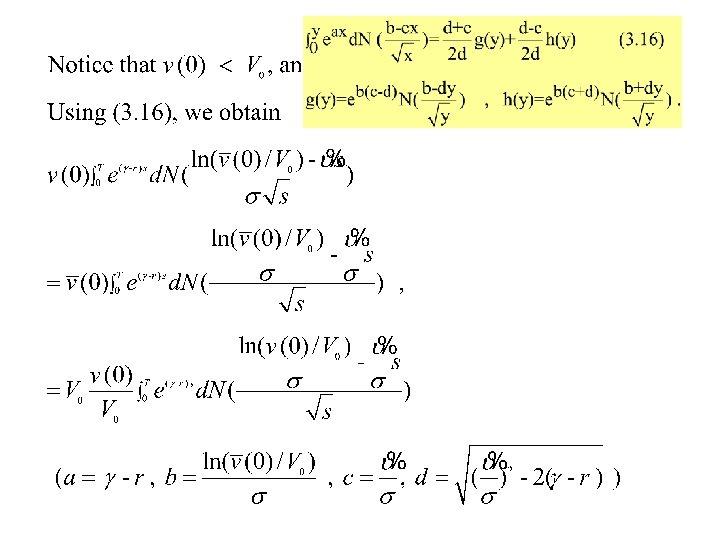

3. 2. 1 Corporate Zero Coupon Bond • They postulate that as soon as the value of firm's assets crosses this lower threshold, the bondholders take over the firm. Otherwise, default takes place at debt's maturity or not depending on whether VT < L or not. • Let us set

3. 2. 1 Corporate Zero Coupon Bond

3. 2. 1 Corporate Zero Coupon Bond

3. 2. 1 Corporate Zero Coupon Bond

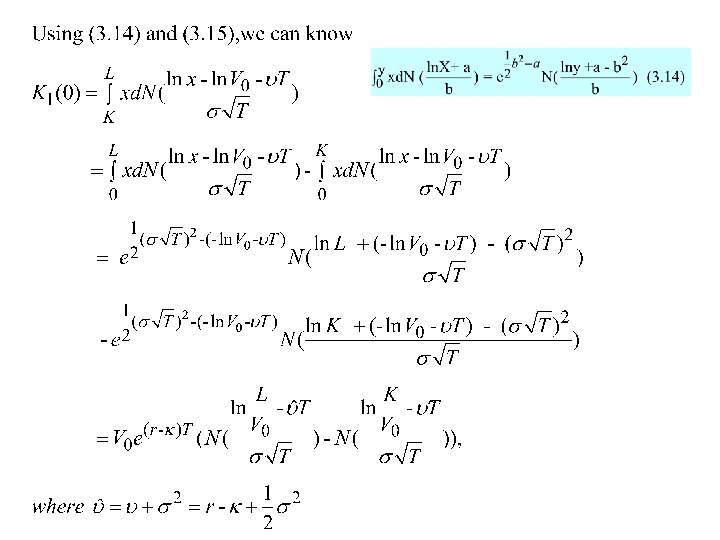

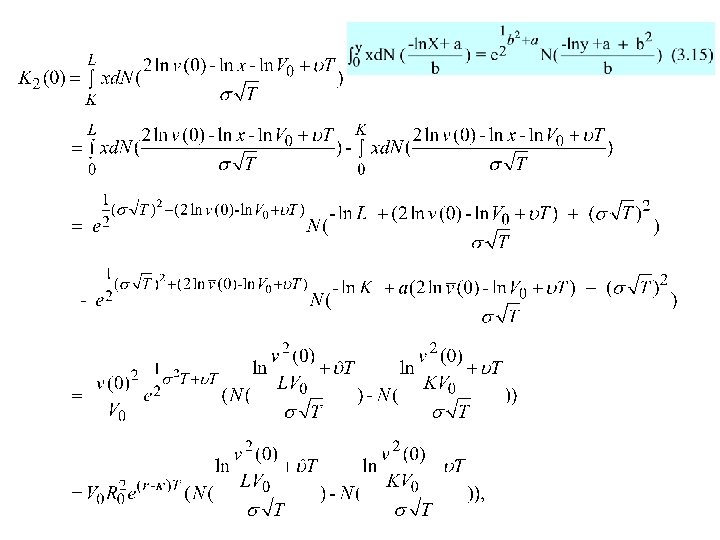

3. 2. 1 Corporate Zero Coupon Bond • Since the interest rate r is assumed to be constant, the pricing function u = u(V, t) of a defaultable bond solves the following PDE:

3. 2. 1 Corporate Zero Coupon Bond

3. 2. 1 Corporate Zero Coupon Bond

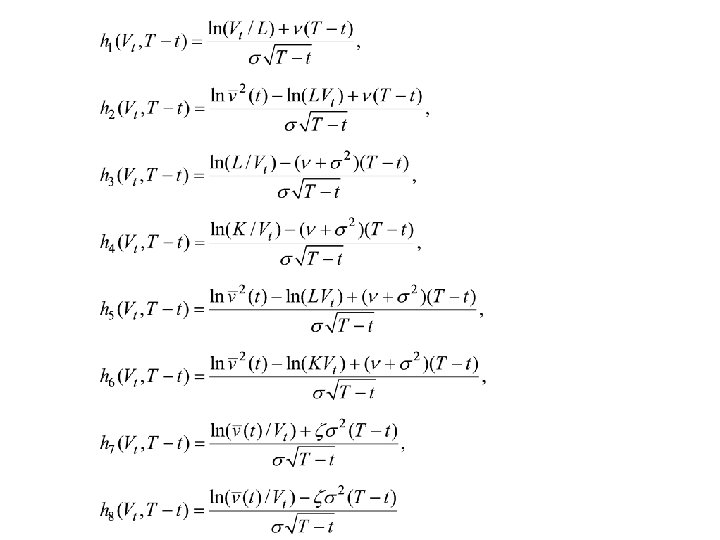

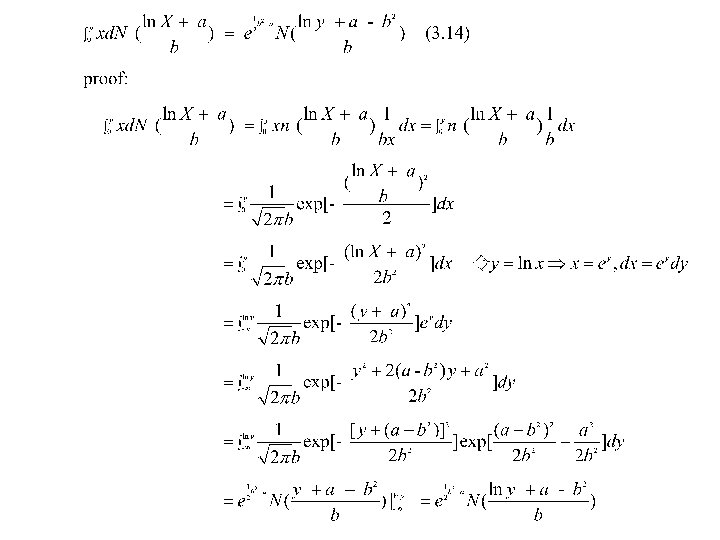

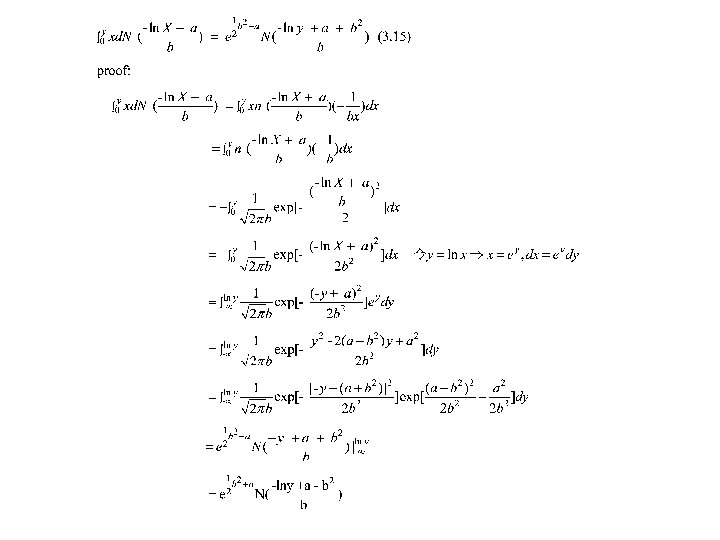

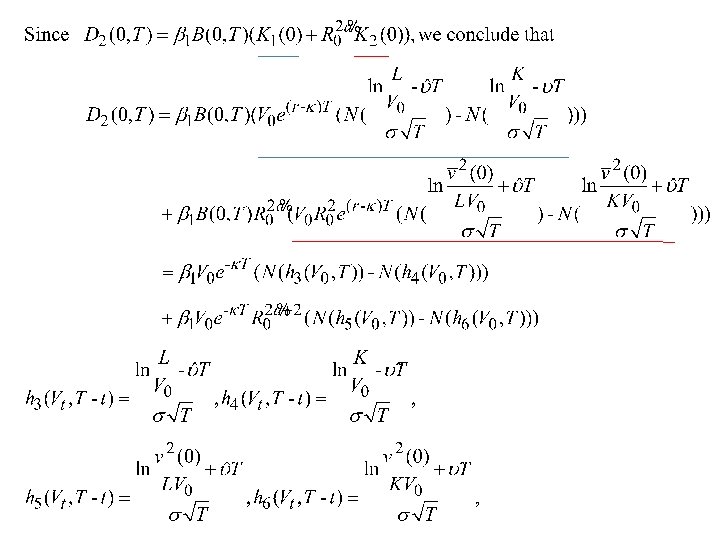

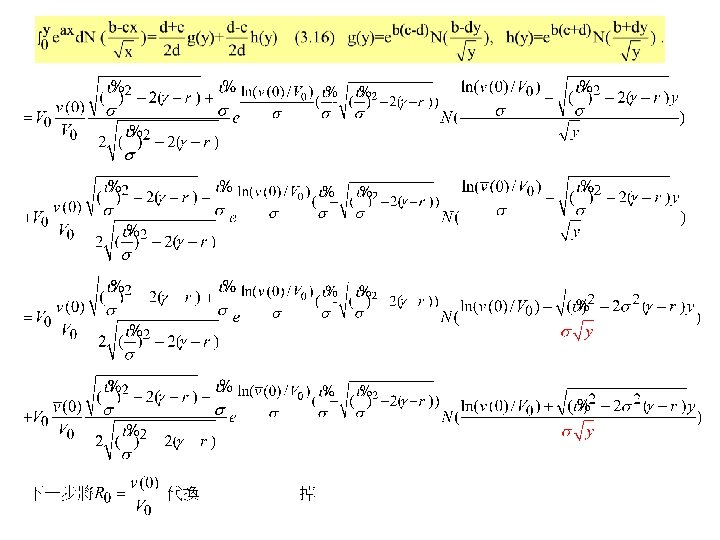

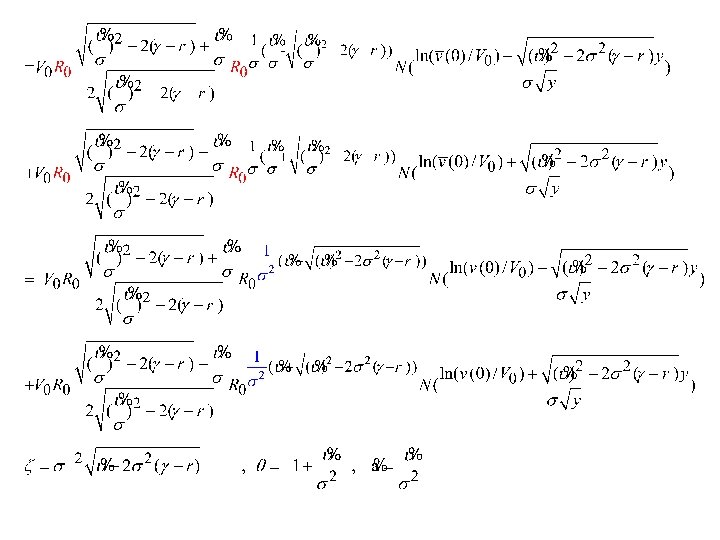

3. 2. 1 Corporate Zero Coupon Bond • Proposition 3. 2. 1

3. 2. 1 Corporate Zero Coupon Bond • Before proceeding to the proof of Proposition 3. 2. 1, we state an elementary lemma. •

Proof of proposition 3. 2. 1

Proof of proposition 3. 2. 1

Proof of proposition 3. 2. 1

3. 2. 1 Corporate Zero Coupon Bond

3. 2. 1 Corporate Zero Coupon Bond • Similarly as in the case of the Merton model, the Black and Cox model produces credit spreads close to zero for small maturities, a feature that is inconsistent with empirical studies. The reason again is that the default time is predictable with respect to the natural filtration of the value process V.

Strict priority rule

Strict priority rule

Strict priority rule

Strict priority rule

Special cases

Case γ=r

Case γ=r

Case γ=r

Case γ>r

3. 2. 2 Corporate Coupon Bond • We shall assume now that r > 0 and that a default able bond of fixed maturity T and face value L pays continuously coupons at a constant rate c, so that The coupon payments stop as soon as default occurs. Formally, we consider a defaultable claim specified as follows: with the barrier v given by (3. 12).

3. 2. 2 Corporate Coupon Bond

3. 2. 2 Corporate Coupon Bond

3. 2. 2 Corporate Coupon Bond

Proposition 3. 2. 2 • Consider a defaultable T maturity bond with face value L, which pays continuously coupons at a constant rate c. The arbitrage price of such a bond equals Dc(t, T) = D(t, T) + A(t, T), where D(t, T) is the value a defaultable zero coupon bond given by Proposition 3. 2. 1.

Proposition 3. 2. 2

Proposition 3. 2. 2 • Some authors apply the general result to the special case when the default triggering barrier is postulated to be a constant. In this special case, the coefficient equals zero. insolvency at maturity T is excluded

Corollary 3. 2. 1

Corollary 3. 2. 1 • Let us mention that the valuation formula of Corollary 3. 2. 1 coincides with expression (3) in Leland Toft (1996). Letting the bond's maturity T tend to infinity, we obtain the following result for the arbitrage price of a consol bond (see also Corollary 3. 2. 2 below)

3. 2. 3 Corporate Consol Bond

3. 2. 3 Corporate Consol Bond

Corollary 3. 2. 2

Corollary 3. 2. 2

3. 2 END

3. 3 Optimal Capital Structure

paper is that it")

3. 3 Optimal Capital Structure • Black and Cox (1976) paper is that it originated studies regarding optimal capital structure of a firm in the context of servicing corporate debt • Report other classic approaches to the issue of optimality of bankruptcy. The basic idea is that stockholders can choose the bankruptcy policy in such a way that the value of equities will be maximized.

3. 3. 1 Black and Cox Approach • assume : 1. a consol bond 2. pays continuously coupon rate c. 3. r > 0 4. payout rate κ , is equal to zero in (3. 11). This condition can be given a financial interpretation as the restriction on the sale of assets. In other words, we postulate that the firm's liability can only be financed by issuing new equity.

• Stockholders have the right")

3. 3. 1 Black and Cox Approach (Conti. ) • Stockholders have the right to stop making payments at any time and either turn the firm over to the bondholders or pay them a lump payment of c/r per unit of the bond's notional amount. • Denote by E(Vt) (D(Vt), resp. ) the value at time t of the firm equity (debt, resp. ), hence the total value of the firm's assets satisfies Vt = E(Vt) +D(Vt)

• v*: a critical level")

3. 3. 1 Black and Cox Approach (Conti. ) • v*: a critical level of the value of the firm, below which no more equity can be sold. It may be determined by stockholders in the course of a certain optimization procedure that in fact determines the optimal capital structure of the firm. • To be more specific, the critical value v* will be chosen by stockholders, whose aim is to minimize the value of the bonds, and thus to maximize the value of the equity.

")

3. 3. 1 Black and Cox Approach (Conti. )

• For the last condition,")

3. 3. 1 Black and Cox Approach (Conti. ) • For the last condition, observe that when the firm's value grows to infinity, the possibility of default becomes meaningless, so that the value of the defaultable consol bond tends to the value c/r of the default free consol bond. It is well known that the general solution to (3. 23) has the following form:

")

3. 3. 1 Black and Cox Approach (Conti. )

• We have thus rediscovered,")

3. 3. 1 Black and Cox Approach (Conti. ) • We have thus rediscovered, using an analytical approach, formula (3. 22) of Corollary 3. 2. 2, with β 2 = 1. •

")

3. 3. 1 Black and Cox Approach (Conti. )

")

3. 3. 1 Black and Cox Approach (Conti. )

• Let us stress that")

3. 3. 1 Black and Cox Approach (Conti. ) • Let us stress that this result was derived under the assumption that stock holders are not allowed to sell assets to cover outstanding interest payments. • It is thus worth noticing that Black and Cox (1976) also examine a situation when the firm's assets can actually be sold to make interest payments.

• A more realistic modeling of the bankruptcy and of the bargaining process, which takes into account other important factors (such as tax benefits and bankruptcy costs) was done by, among others, Leland (1994), Leland Toft (1996), Anderson and Sundaresan (1996), Mella Barral and Perraudin (1997), and Mella Barral (1999).

paper")

3. 3. 2 Leland's Approach • The primary concern of the Leland (1994) paper is the optimal capital structure of a levered firm over an infinite time horizon. • Assume: firm issues a consol paying a coupon at the rate c while the firm is solvent. • The firm becomes insolvent, that is the default occurs, when the process V of the total value of the firm's assets for the first time hits the constant lower reorganization barrier.

• Similarly as in the Black and Cox")

3. 3. 2 Leland's Approach(conti. ) • Similarly as in the Black and Cox approach, the optimal bankruptcy level v* is chosen in such a way that the value of the firm's equity is maximized. • As before, the interest rate is constant, and the dynamics of the firm's value under P* are given by (3. 11) with r> 0 and κ= 0.

Bankruptcy costs

Bankruptcy costs

Tax benefits

")

Tax benefits(conti)

• It is interesting to notice that, under the convention adopted by")

Tax benefits(conti) • It is interesting to notice that, under the convention adopted by Leland (1994), bankruptcy costs do not affect the value of the firm's equity, as opposed to the firm's debt. In other words, in the event of default the bankruptcy costs are paid in full by the bondholders.

Unprotected debt • Let us first assume that no lower bound is imposed on the value of the endogenously chosen level of the triggering barrier. However, we still assume that the bankruptcy necessarily occurs whenever the value of the equity hits zero. Also, the value of the equity at the time of bankruptcy is always 0, no matter what is the chosen level of the default triggering barrier.

• Comparing (3. 31) and (3. 25), we conclude that this corresponds")

Unprotected debt(conti) • Comparing (3. 31) and (3. 25), we conclude that this corresponds to the case examined in Sect. 3. 3. 1 with one minor modification, namely, the coupon rate c needs to be replaced by the net coupon. •

")

Unprotected debt(conti)

")

Unprotected debt(conti)

Protected debt • Consider now the case when bankruptcy is triggered when the value of the firm's assets falls below the principal value of debt. Assume, in addition, that the principal value of the debt was equal to its value at the inception date 0. The level of the default triggering barrier is thus exogenously given to be

")

Protected debt(conti)

3. 3. 3 Leland Toft Approach • finite maturity corporate debt • Assume: the short term interest rate is constant • The process of the total value of the firm's assets satisfies, under the spot martingale measure P*,

")

3. 3. 3 Leland Toft Approach(conti. )

Stationary debt structure • assume : the firm has a stationary debt structure. • at any time t, the debt outstanding is composed of 1. coupon bonds of maturities from the interval [t, t + T] with the constant coupon rate c = C IT 2. the face value uniformly distributed over this interval. the total coupon paid by all outstanding bonds is C per year.

• New bonds issued rate l= L / T per")

Stationary debt structure(conti. ) • New bonds issued rate l= L / T per year (L: the total face value of all outstanding bonds) • The same amount of principal is retired when the previously issued bonds mature. • as long as the firm remains solvent, the total face value remains constant at any date t, and the outstanding bonds have a uniform distribution of face value in the interval [t, t + T].

")

Stationary debt structure(conti. )

")

Stationary debt structure(conti. )

Proposition 3. 3. 1

Proposition 3. 3. 1 proof

")

Proposition 3. 3. 1 proof(conti. )

3. 3. 3 Leland Toft Approach

3. 3. 4 Further Developments • overview of some further studies of first passage time models with constant interest rate • State variables Strategic debt service Probabilistic approaches Comparative studies

State variables • in first-passage-time model define the default time not in terms of the firm's value, but rather in terms of some other state variables, which reflect the economic fundamentals (such as: the firm's operating earnings, the price of the firm's product, etc. ).

: • a generic first passage time")

State variables Mella Barral and Tychon (1999) : • a generic first passage time model with a state variable that follows a geometric Brownian motion. • default : when the state variable hits a constant threshold level and the value of assets at default is considered an exogenous input, given through some function V( )

State variables • derive the valuation formula for a defaultable coupon bond with finite maturity • examine the term structure of credit spreads under the assumption that the coupon rate is chosen in such a way that the initial bond price is equal to the face value

Strategic debt service • bankruptcy /liquidation costs may induce creditors to accept deviations from contractual payments, rather than to force the firm's bankruptcy • the first to account for debt's renegotiation in case of distress : Anderson and Sundaresan (1996) and Mella Barral and Per raudin (1997) → explicitly deal with strategic debt service (recent papers in this vein include Leland (1998), Mella Barral (1999), and Ericsson (2000)).

• assume : stockholders may persuade")

Strategic debt service Mella Barral and Perraudin (1997) • assume : stockholders may persuade bondholders to renegotiate the debt, and thus to receive less than the originally contracted interest payments. • Using the PDE approach, perform an analysis of the optimality of the debt's renegotiation, in the sense of the maximization of the firm's value

differs from Mella Barral and Perraudin")

Strategic debt service • Anderson and Sundaresan (1996) differs from Mella Barral and Perraudin (1997)(2個) First: • model 'bankruptcy game' between the bondholders and the stockholders. • the bargaining procedure is shown to lead to the discrete time game theoretic model of bankruptcy process.

Strategic debt service Second: • focus on bonds of fixed maturity, (perpetual bonds studied in Mella Barral and Perraudin (1997)). • The continuous time version of the Anderson and Sundaresan model was subsequently examined by means of the PDE approach in Anderson et al. (1996), who studied perpetual corporate bonds. • numerical studies conclusion : bankruptcy /renegotiation costs may have a significant impact on the level of credit spreads.

• most defaultable claims even accounting for bankruptcy")

Probabilistic approaches Ericsson and Reneby (1998) • most defaultable claims even accounting for bankruptcy costs, corporate taxes, or deviations from the strict priority rule can be decomposed into relatively simple three building blocks: a down and out call option a down and out digital option a digital claim which pays one unit of cash in the event of default.

Probabilistic approaches • Assumption : a constant triggering barrier • Obtain the valuation formulae for these 'building blocks'. • Apply to previously studied problems related to strategic debt service. • Rederive, through a probabilistic approach, some formulae previously established through the PDE approach by Mella Barral and Perraudin (1997).

Probabilistic approaches

• consider a corporate perpetuity with a notional")

Comparative studies Anderson and Sundaresan (2000) • consider a corporate perpetuity with a notional amount L and the coupon rate c (as before, we assume that the coupon rate c encompasses the face value L). • They assume a constant level r of the short term interest rate. • Their valuation equation nests the results for corporate perpetuities derived in Black and Cox (1976), Leland (1994), Anderson et al. (1996), and Mella Barral and Perraudin (1997).

Comparative studies • • Particular specifications of these quantities depend on modeling assumptions that are made regarding activities of the firm and its operating covenants.

, Leland (1994) and Anderson")

Comparative studies • For example, in Black and Cox (1976), Leland (1994) and Anderson et al. (1996), the coefficient is known to satisfy , where, > 0 is a constant, which exact value varies across alternative models. • In Mella Barral and Perraudin (1997) the default probability is an explicit function of the price of the firm‘s product.

: • provide a comparative study of structural models")

Comparative studies Anderson and Sundaresan (2000): • provide a comparative study of structural models with and without a strategic debt service, using the time series data for the U. S. corporate bond market. • Conclude the modifications of the classic structural models that allow for the endogenous determination of the default threshold based on economic fundamentals have led to an improvement of structural models.

- Slides: 114