20211214 Comparative Study on Measures of Window Dressing

• 舞弊是个法律概念,CPA不对某项行为是否属于舞弊 作出法律决定 •")

年度 净资产 1999 20, 709 主营收 入 6, 757 2000 3, 014")

项 目 年初余额 本年增加数 本年转回数 年末余额 坏账准备 其中:应收账款 其他应收款 42, 724 32,")

• 财务状况一览表 年度 股东权益 g/通用格式 净资产比 率(%) 1998 123, 024 39. 1")

g/通用格式 年度 1998 1999 主营 收入 主 营 利 润 7, 754")

- Slides: 77

财务报表粉饰与分析 2021/12/14 Comparative Study on Measures of Window Dressing 1

Overview of Financial Fraud 93 100 90 80 70 60 50 40 30 20 10 0 22 15 6 Enron Xerox Rite Aid World. Com Faked Profit 2021/12/14 Comparative Study on Measures of Window Dressing 3

Biggest U. S Bankruptcies Since 1980 g/通用格式 g/通用格式 g/通用格式 g/通用格式 L NT t Km ar p or Mc PG &E ia el Ad si os Cr ph ng A FC co Te xa n ro En G. Wo rl d. C om g/通用格式 Total Assets 2021/12/14 Comparative Study on Measures of Window Dressing 4

Debts owned to Banks and Institutional Investors by World. Com Total Assets: BV $ 107 billion; MV $15 billion; Total Debts $41 billion) ( $ in million Bank & Trust JP Morgan Trust Co. Amount Institutional Investors amount 17, 200. 00 CALPERS 387. 5 Deutsche Bank 240. 25 Prudential 386. 5 ABN Amco Bank 202. 75 Metropolitan Life Insur. 300. 3 Citibank 154. 88 Vanguard 281. 9 Fleet 150. 00 Travelers Asset mgt. 270. 1 Bank One 100. 00 Northwest Invest. Mgt. 267. 0 Mellon Bank 100. 00 Alliance Capital Mgt. 253. 9 Wells Fargo Bank 100. 00 American Express F. A 212. 4 JP Morgan Chase 6. 00 Wellington Mgt. 212. 1 2021/12/14 Comparative Study on Measures of Window Dressing 5

Merck’ Faked Revenue g/通用格式 g/通用格式 g/通用格式 1999 g/通用格式 2000 Faked Revenue 2021/12/14 g/通用格式 2001 Total Revenue Comparative Study on Measures of Window Dressing 6

Financial Frauds and Independent Directors • Overview of financial frauds or earnings management 舞弊种类 及金额 公司名称 (事务所名称) Enron (AA) 虚增利润 6亿美元, 隐瞒负 债 30多亿美元 是否由AC 是否由 独立懂事/ 发现? CPA发现? 董事会人数 否 否 15/17 Xerox (KPMG) 虚增利润 15亿美元 否 否 7/9 Rite Aid(KPMG) 虚增利润 22亿美元 否 否 7/9 World. Com 虚增利润 93亿美元 否 否 9/11 (AA) • 其他公司 – Microsoft, GE, IBM, Boeing, Lucent, Cisco, Oracle, AOL, Nortel, Qwest, Tyco, Global Crossing, Cendant, WMX, Sunbeam, Adelphia 2021/12/14 Comparative Study on Measures of Window Dressing 7

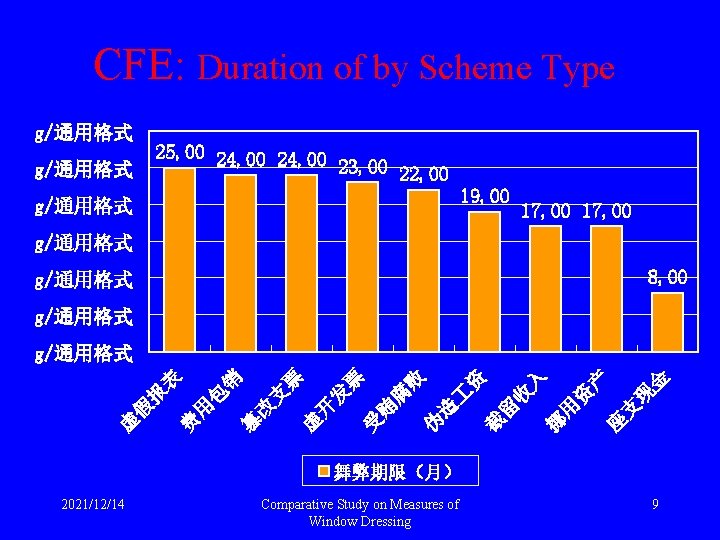

CFE’s Classification Scheme Fraud Corruption Conflicts of Interest Bribery Illegal Gratuities Economic Extortion 2021/12/14 Asset Misappropriation Cash Fraudulent Statements Bogus Revenue Timing Differences Fraudulent Disbursements Inventories and All Other Assets Comparative Study on Measures of Window Dressing Concealed L & E Improper Disclosure Improper Valuation 8

CFE: Effective Measures to Prevent Fraud 2021/12/14 Comparative Study on Measures of Window Dressing 11

SAS 99 : Consideration of Fraud in a Financial Statement Audit • AICPA恢复公众信任的一个重大举措 – 2002. 10. 15,AICPA发布采纳SAS 99的决定 – 取代SAS 82 (1996) – 自 2002年 12月15日生效 – SAS将在 2002年 10月末或 11月初正式颁布 2021/12/14 Comparative Study on Measures of Window Dressing 12

Description and Characteristics of Fraud • 1个关键要素 – 舞弊是蓄意行为(Intentional Behavior) • 舞弊是个法律概念,CPA不对某项行为是否属于舞弊 作出法律决定 • 舞弊与差错的差别在于是否故意造成错报或漏报 – 实际 作中难以判断,如不合理会计估计(Unreasonable Accounting Estimates) • 2种舞弊类型 • 虚假财务报告产生的错报 – Misstatements arising from fraudulent financial reporting • 挪用资产产生的错报 – Misstatements arising from misappropriation of Assets 2021/12/14 Comparative Study on Measures of Window Dressing 14

Description and Characteristics of Fraud • 3个必备条件 – 动机或压力 • Management or employees have an incentive or are under pressure – 机会 • Circumstances exist (e. g. absence of control, ineffective control, ability of management to override controls) that provide an opportunity for a fraud to be perpetrated – 理由 • Those involved are able to rationalize a fraudulent act as being consistent with their personal code of ethics 2021/12/14 Comparative Study on Measures of Window Dressing 15

Triangle of Fraud • Albrecht el. al 提出的舞弊铁三角 Pressure Fraud Opportunity 2021/12/14 Comparative Study on Measures of Window Dressing Rationalization 16

Arthur Levitt’s Comments on “ Number Game” • 5 Methods Game Playing identified by Levitt – – – Big-bath charges ( 洗大澡或巨额冲销) Creative acquisition accounting (创造性并购会计) Cook-jar reserves (甜饼盒式准备金) Revenue recognition (收入确认) Materiality (重大性) 2021/12/14 Comparative Study on Measures of Window Dressing 17

A公司的财务图象 (单位:万元) 年度 净资产 1999 20, 709 主营收 入 6, 757 2000 3, 014 6, 797 净利润 g/通用格式 20, 010 g-/通用格式 -16, 585 g-/通用格式 2001 - 198, 868 5, 187 -225, 724 g-/通用格式 1999 净资产 2021/12/14 Comparative Study on Measures of Window Dressing 2000 主营收入 2001 净利润 20

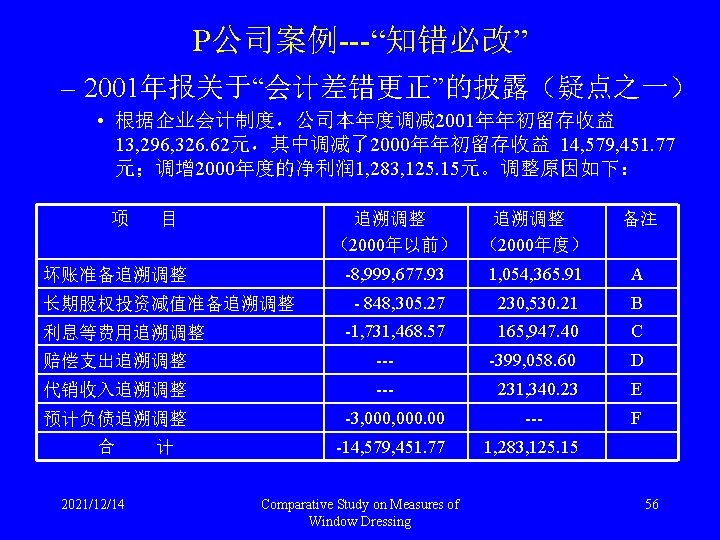

A公司 2001年度减值明细表(单位:万元) 项 目 年初余额 本年增加数 本年转回数 年末余额 坏账准备 其中:应收账款 其他应收款 42, 724 32, 667 10, 057 166, 049 128, 055 37, 994 ------- 208, 773 160, 722 48, 051 存货跌价准备 其中: 原材料 12, 606 10, 855 14, 953 12, 572 83 83 27, 476 23, 344 长期投资减值准备 2, 351 1, 335 --- 3, 686 固定资产减值准备 --- 7, 657 在建 程减值准备 --- 232 190, 226 83 247, 824 合 2021/12/14 计 57, 681 Comparative Study on Measures of Window Dressing 21

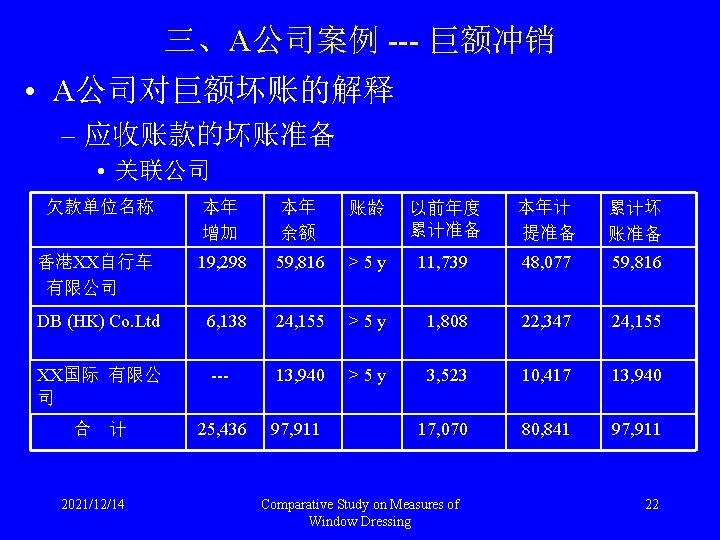

A公司案例 --- 巨额冲销 – 非关联方欠款:S Co. Ltd, Au Co. Ltd,其他出口经 商商、国内客户 欠款单位名称 本年增加 本年欠 款余额 账龄 以前年 度累计 准备 本年计提 准备 累计坏账 准备 S Co. Ltd* 4, 822 9, 793 >5 y --- 9, 793 Au Co. Ltd --- 4, 166 >5 y --- 4, 166 其他出口经销商* 3, 674 12, 711 >5 y 123 12, 588 12, 711 --- 35, 648 >3 y 15, 425 20, 223 35, 648 8, 496 62, 318 15, 548 46, 770 62, 318 国内客户** 合 计 2021/12/14 Comparative Study on Measures of Window Dressing 23

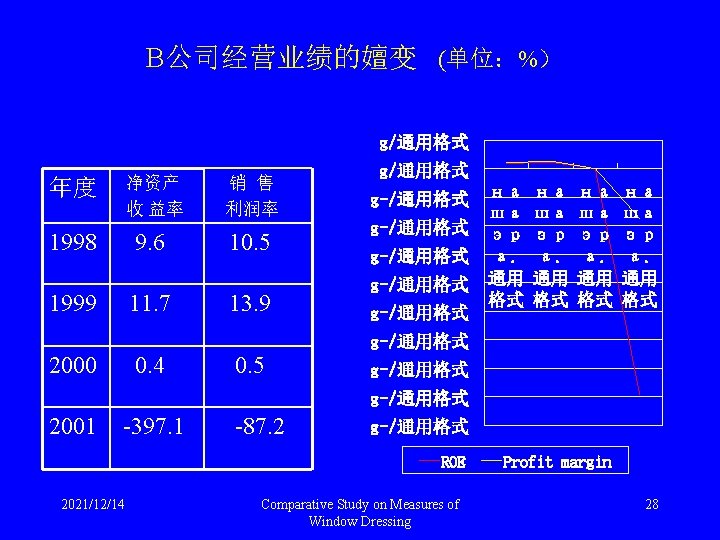

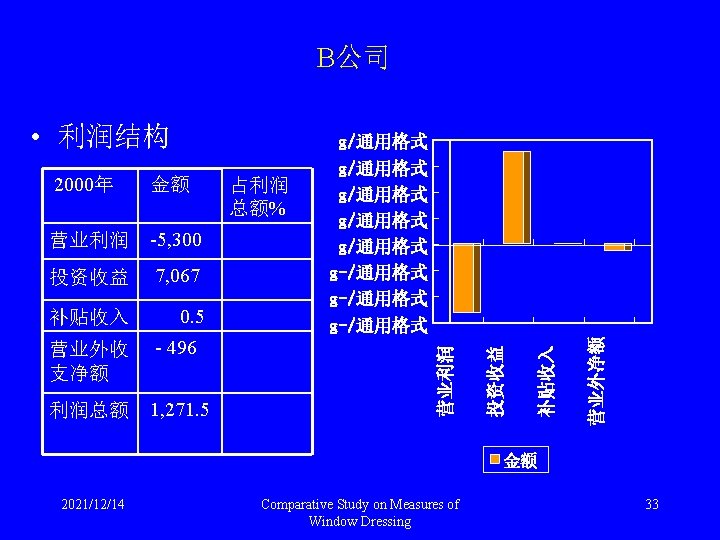

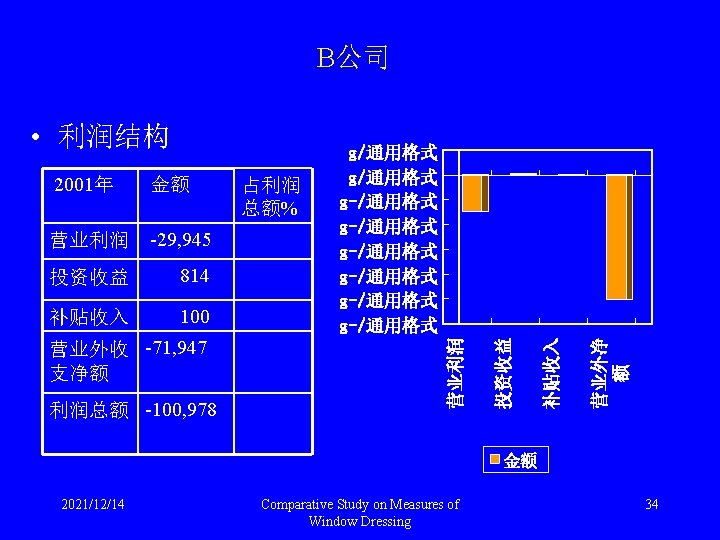

B公司案例:抵债背后的真实故事 • 经营业绩一览表 g/通用格式 主营业务 收 入 净利润 1998 112, 147 11, 800 g/通用格式 1999 111, 296 15, 525 g/通用格式 548 g-/通用格式 年度 2000 105, 753 g/通用格式 g-/通用格式 2001 112, 282 -97, 856 1998 1999 2000 2001 业务收入 2021/12/14 Comparative Study on Measures of Window Dressing 净利润 27

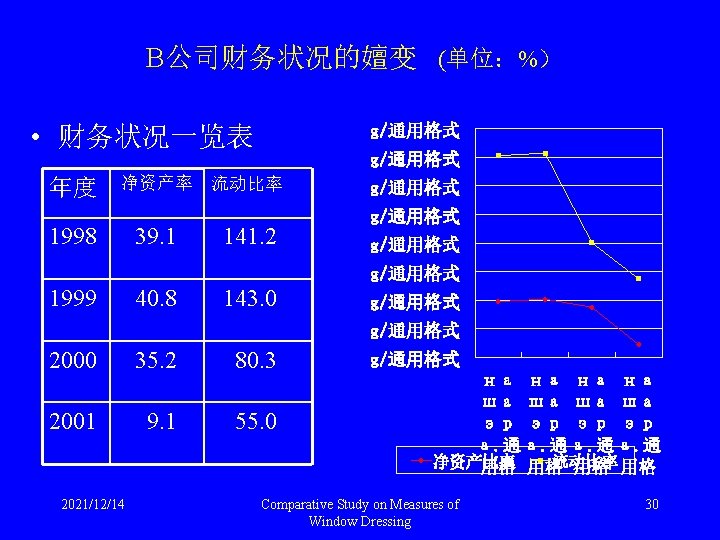

B公司财务状况的嬗变 (单位:万元) • 财务状况一览表 年度 股东权益 g/通用格式 净资产比 率(%) 1998 123, 024 39. 1 1999 132, 792 40. 8 g/通用格式 g/通用格式 2000 122, 671 2001 24, 644 35. 2 9. 1 g/通用格式 1998 1999 2000 2001 股东权益 2021/12/14 Comparative Study on Measures of Window Dressing 29

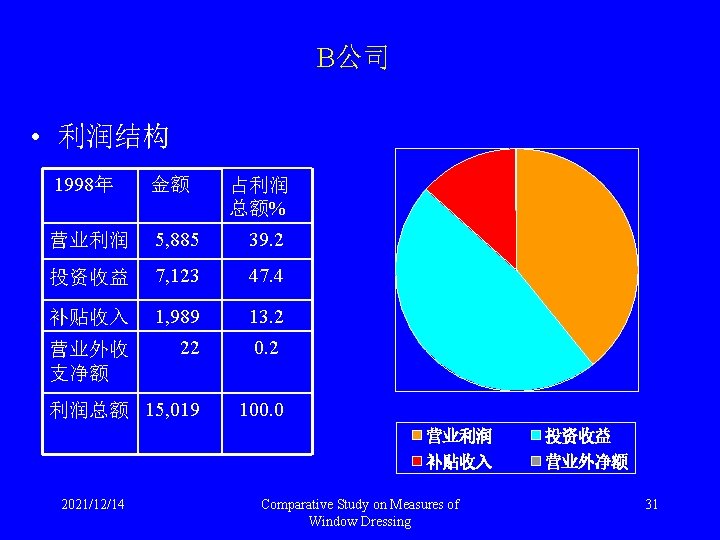

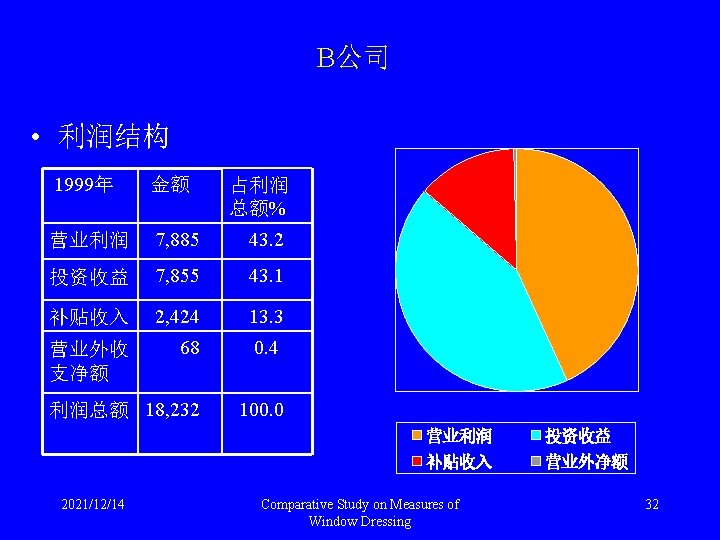

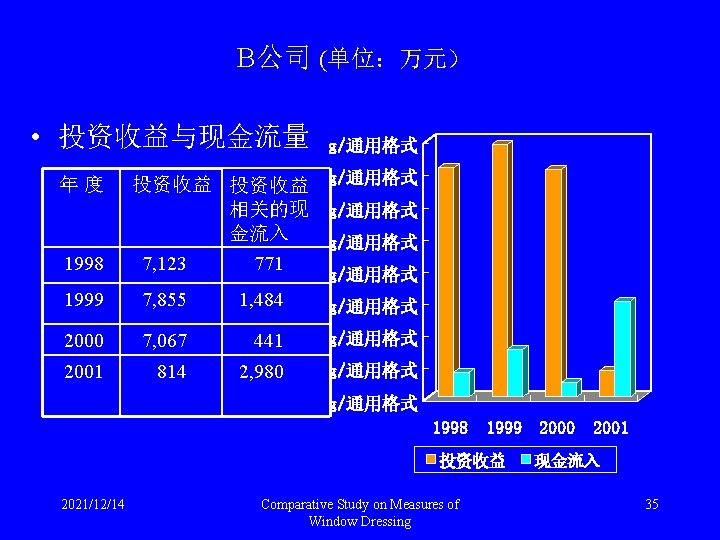

B公司 • 投资收益构成 项目名称 1998 1999 2000 委托贷款收益 43, 627, 932. 64 47, 018, 425. 37 委托贷款准备 (2, 063, 492. 78) (2, 062, 014. 44) 股权投资收益 25, 181, 284. 81 33, 163, 288. 01 34, 421, 843. 26 7, 809, 254. 00 非控股公司分配的利润 5, 376, 000. 00 1, 700, 000. 00 4, 631, 999. 98 5, 300, 400. 00 股权投资差额摊销 (899, 748. 42) 债券投资收益 8, 750. 00 转让收益 --- 长期投资减值准备 --- 合 计 2021/12/14 71, 230, 726. 25 --(368, 869. 26) --78, 551, 081. 28 Comparative Study on Measures of Window Dressing 32, 516, 159. 86 2001 --- (250, 000. 00) --- --- --- --70, 670, 254. 70 (3, 816, 255. 16) 8, 143, 650. 44 36

B公司 – 营业外支出 固定资产清理净损失 固定资产盘亏 固定资产减值准备 2001年 1, 939, 922. 21 --101, 653, 386. 86 2000年 107, 011. 62 6, 750. 91 3, 082, 589. 97 无形资产减值准备 对外担保预计负债 捐赠支出 债务重组损失 其他 合 计 328, 677, 500. 86 286, 357, 085. 06 128, 928. 60 982, 928. 60 100, 240. 03 719, 839, 465. 28 ----2, 187, 890. 00 --15, 732. 00 5, 399, 974. 50 明 细 项 目 2021/12/14 Comparative Study on Measures of Window Dressing 38

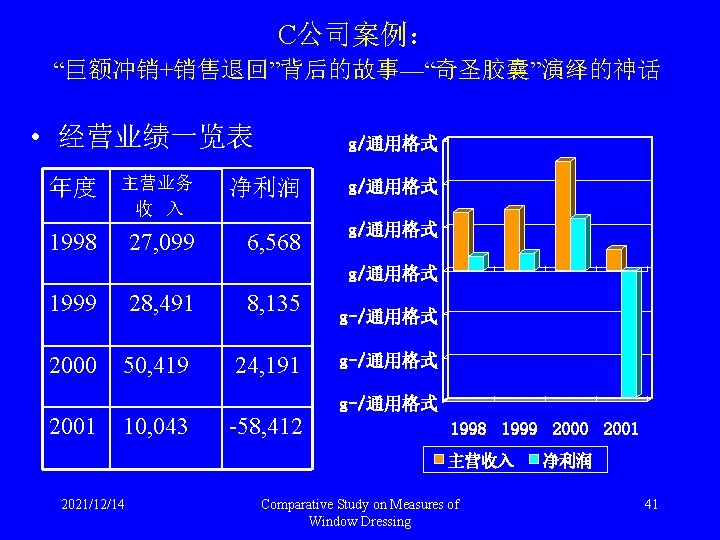

C公司:净利润与经营业绩的反差 • NI v. s CFFOA g/通用格式 年度 净利润 CFFOA g/通用格式 1998 6, 568 - 6, 293 g/通用格式 g-/通用格式 1999 8, 135 - 8, 062 2000 24, 191 19, 615 2001 -58, 412 -74, 034 g-/通用格式 1998 1999 2000 2001 NI 2021/12/14 Comparative Study on Measures of Window Dressing CFFOA 43

C公司---经营活动产生的现金流量 • CFFOA: 2001 v. s 2000 项 目 名 称 销售商品、提供劳务收到的现金 2001 2000 154, 902, 472. 69 514, 146, 801. 97 562, 784. 00 收取的租金 --- 收到的税费返还 收到的其他与经营活动有关的现金 现金流入小计 购买商品、接受劳务支付的现金 126, 146, 385. 14 11, 854, 612. 64 281, 048, 857. 83 537, 718, 699. 41 38, 661, 406. 74 58, 904, 277. 28 --- 经营租赁所支付的现金 11, 154, 500. 80 224, 088. 00 15, 312, 928. 78 15, 312, 719. 45 支付的各项税款 243, 148, 586. 14 110, 460, 669. 35 支付的其他与经营活动有关的现金 724, 266, 389. 07 152, 975, 914. 86 1, 021, 389, 310. 73 341, 564, 738. 92 支付给职 以及为职 支付的现金 现金流出小计 经营活动产生的现金流量净额 2021/12/14 -740, 266, 389. 07 Comparative Study on Measures of Window Dressing 196, 153, 960. 49 44

C公司: 2000 -2002股价最高、最低 g/通用格式 g/通用格式 g/通用格式 00 2 6/ 1 2/ 2 高 2最 20 0 低 2最 20 0 高 1最 20 0 1最 低 高 0最 20 0 0最 低 g/通用格式 Stock Price 2021/12/14 Comparative Study on Measures of Window Dressing 46

C公司---“奇圣胶囊”的功效 • “奇圣胶囊”对主营业务的贡献 项 2001年度 目 2000年度 主营收入 主营成本 毛利率 奇圣胶囊 5, 097 2, 914 43% 52, 091 25, 147 52% 治麋灵栓 3, 013 415 86% 7, 810 929 88% 参莲胶囊 - 1, 328 - 236 82% 2, 981 499 83% 壮骨伸筋胶囊 2, 220 538 76% 2, 207 398 82% 其他 5, 189 1, 675 68% 9, 644 2, 595 73% 内部抵销 4, 147 2, 259 46% 24, 314 22, 520 7% 合 计 10, 043 3, 047 70% 50, 419 7, 048 86% 2021/12/14 Comparative Study on Measures of Window Dressing 47

D公司:经营业绩变动趋势 g/通用格式 主营业 务收入 净利润 1998 90, 382 9, 876 1999 108, 874 12, 631 2000 239, 762 17, 844 2001 205, 145 3, 610 g/通用格式 g-/通用格式 99 20 00 20 1 02 Q 1 - 4, 835 g/通用格式 19 29, 367 g/通用格式 98 2002 Q 1 g/通用格式 19 年度 Sales 2021/12/14 Comparative Study on Measures of Window Dressing NI 51

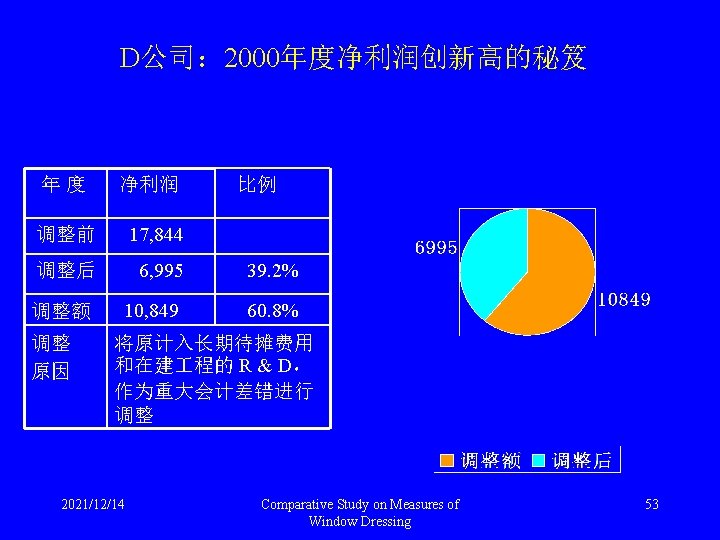

D公司:净利润与现金流量之反差 g/通用格式 年度 净利润 CFFOA g/通用格式 1998 9, 876 - 17, 191 g/通用格式 1999 12, 308 - 21, 248 g-/通用格式 2000 17, 844 - 53, 576 g-/通用格式 2001 3, 610 - 2, 594 g-/通用格式 на ша эр а. 通用 格式 g-/通用格式 NI 2021/12/14 Comparative Study on Measures of Window Dressing CFFOA 52

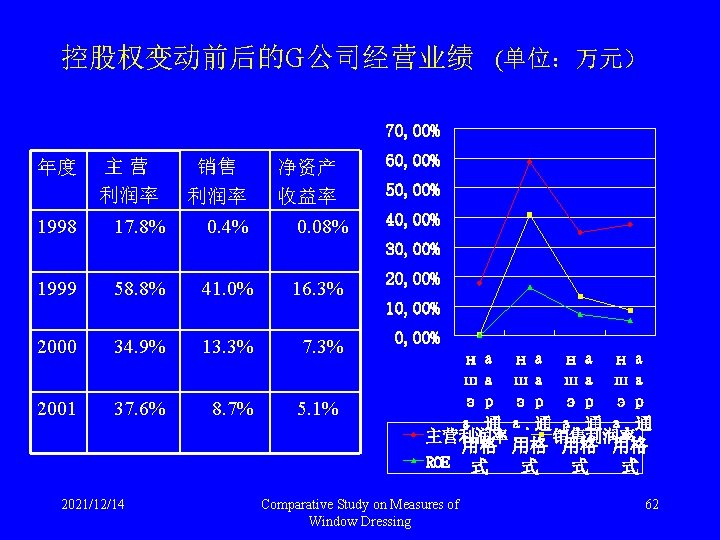

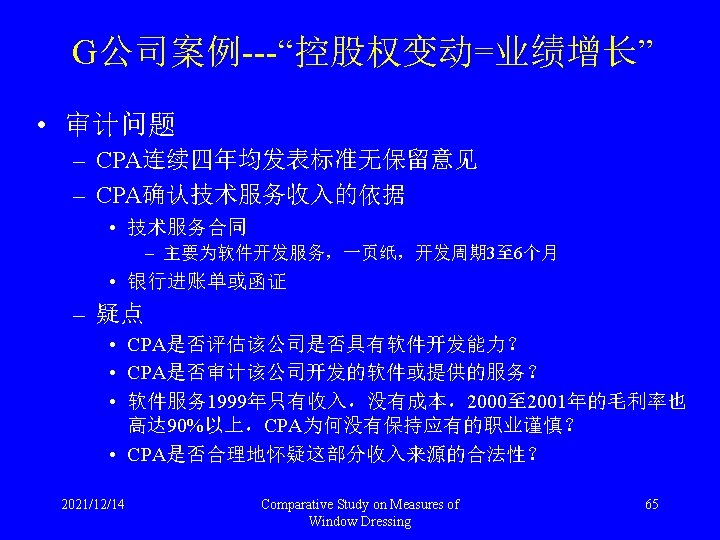

控股权变动前后的G公司经营业绩 (单位:万元) g/通用格式 年度 1998 1999 主营 收入 主 营 利 润 7, 754 1, 383 15, 497 9, 106 净利润 g/通用格式 32 g/通用格式 6, 352 g/通用格式 2000 22, 528 7, 867 2, 994 2001 25, 117 9, 446 2, 185 g/通用格式 1998 主营收入 2021/12/14 Comparative Study on Measures of Window Dressing 1999 2000 主营利润 2001 净利润 61

G公司毛利率 120, 00% 100, 00% 80, 00% 60, 00% 40, 00% 20, 00% наша эра. 通用格 技术服务 其他式 式 发电机组 式通信产品 式 2021/12/14 Comparative Study on Measures of Window Dressing 64

财务分析框架 • 1、From Business Activities to Financial Statements Business Environment Labor Markets Capital Markets Product Markets Supplier Customers Competitors Business Strategy Business Activities Operating Activities Investment Activities Financing Activities Scope of Business: Degree of Diversification Type of Diversification Competitive Positioning: Cost Leadership Differentiation Key Success Factors and Risk Business Regulations Accounting System Accounting Environment Capital Market Structure Contracting & Governance Accounting Conventions And Regulations Tax & Financial Accounting Linkage Third-party Auditing Legal System for Accounting Disputes 2021/12/14 Measure and Report Economic Consequences of Business Activities Accounting Strategy Financial Statements Managers’ Superior inf. On Business Activities Estimation Errors Distortions fm Managers’ Accounting Choices Comparative Study on Measures of Window Dressing Choice of Acctg Policies Choice of Acctg Estimates Choice of Reporting Format Choice of Supplementary Disclosures 66

财务报表分析框架 • 2、Doing Business Analysis Using Financial Statements Managers’ superior inf on business activities Noise from estimation errors Distortions from managers’ acctg choices Other Public Data Industry and firm data Outside financial statements Business Application Context Credit analysis Securities analysis Mergers and acquisition analysis Debt/dividend analysis Corporate communication strategy analysis General business analysis Analysis Tools Business Strategy Analysis Generate performance expectations through Industry analysis and competitive strategy Analysis Accounting Analysis Financial Analysis Evaluate accounting quality By assessing accounting Policies and estimates Evaluate performance using ratios And cash flow analysis 2021/12/14 Comparative Study on Measures of Window Dressing Prospective Analysis Making forecasts and value Business 67

会计分析 • 1、Doing Accounting Analysis – Step 1: Identify key accounting policies – Step 2: Access accounting flexibility – Step 3: Evaluate accounting strategy • Key questions – How do the firm’s accounting policies compare to the norms in the industry? If they are different, is it because the firm’s competitive strategy is unique? – Does management face strong incentives to use accounting discretion for earnings management? – Has the firm changed any of its policies and estimates? What is the justification? What is impact of changes? – Have the firm’s policies and estimates been realistic in the past? – Does the firm structure any significant business transactions so that it can achieve certain accounting objectives? 2021/12/14 Comparative Study on Measures of Window Dressing 68

会计分析 – Step 4: Evaluate the quality of disclosure • Key questions – Does the firm provide adequate disclosure to assess the firm’s business strategy and its economic consequences? – Do the footnotes adequately explain the key accounting policies and assumptions and their logic? – Does the firm adequately explain its current performance? (MD&A) – If accounting rules and conventions restrict the firm from measuring its key success factors appropriately, does the firm provide adequate additional disclosure to help outsiders understand how these factors are being managed? – If the firm is in multiple business segments, what is the quality of segment disclosure? – How forthcoming is the management with respect to bad news? – How good is the firm’s investor relations program? Does the firm provide fact books with detailed data on the firm’s business and performance? Is the management accessible to analysts? 2021/12/14 Comparative Study on Measures of Window Dressing 69

会计分析 – Step 5: Identify potential red flags • Common red flags – Unexplained changes in accounting policies and estimates, especially when performance is poor – Unexplained transactions that boost profits – Unusual increases in account receivable in relation to sales increases – Unusual increases in inventories in relation to sales increases – An increasing gap between a firm’s reported income and its cash flow from operating activities – An increasing gap between a firm’s reported income and its tax income – A tendency to use financing mechanisms like research and development partnerships and the sale of receivables with recourse – Large fourth-quarter or fist-quarter adjustments – Qualified audit opinions or change in independent auditors that are not well justified – Related-party transactions or transactions between related entities – Step 6: Undo accounting distortions • 4 approaches ( refer to window-dressing of financial statements) 2021/12/14 Comparative Study on Measures of Window Dressing 70

Sarbanes-Oxley Act – SEC对GAAP的确认权力及对准则制定机构的要求 • SEC应当对转而采纳原则基础的会计准则进行专题研究,并在 1年 后向国会报告 – PCAOB的资金来源和运用 • 2002. 10. 25 SEC任命了PCAOB的五名委员 • William H. Webster, Chairman(2007)--Former director of the FBI and CIA • Daniel L. Goelzer(2006) --Former SEC general counsel • Kayla J. Gilan(2005) – Former general counsel of Cal. PERS • Willis D. Gradison Jr. (2004) – Former representative from Ohio • Charles D. Niemaier (2003) – Current chief accountant of the SEC’s Division of Enforcement 2021/12/14 Comparative Study on Measures of Window Dressing 72

Sarbanes – Oxly Act • 2、对审计师的独立性提出了更加严格的要求 – 限制事务所为其审计的客户提供 9项非审计服务 • Bookkeeping or other services related to the accounting records or financial statements of the audit client; • Financial information systems design and implementation • Appraisal or valuation services, fairness opinions, or contribution-in-kind reports; 2021/12/14 Comparative Study on Measures of Window Dressing 73

Sarbanes – Oxley Act • • • Actuarial services; Internal audit outsourcing services Management functions or human resources; Broker or dealer, investment adviser, or investment banking services; Legal services and expert services unrelated to the audit; Any other services that the Board determines, by regulation, is impermissible. – 事务所执行其他非审计业务(如税务咨询),必须事先得 到PCAOP的批准 – 事务所负责某一公司审计的合伙人或复核合伙人至少每 5 年轮换一次 – 规定审计师必须向审计委员汇报的事项 – 限制与被审计客户有利害冲突的人员参与审计 • CEO, CFO, Controller, CAO, etc. 1 year 2021/12/14 Comparative Study on Measures of Window Dressing 74