20122021 1 cf Gtls lgo Gq 0 f

![cf. Gtl/s lgo. Gq 0 f / n]vfk/LIf 0 f tyf a]? h' s[i](https://slidetodoc.com/presentation_image_h2/1f569fe110ede50c6de824e9a8e63853/image-2.jpg "cf. Gtl/s lgo. Gq 0 f / n]vfk/LIf 0 f tyf a]? h' s[i")

Creates value b) Integral part")

^$")

![cfly{s sfo{ljlw lgodfjn. L, @)^$======= �-@_ pklgod -!_ adf]lhdsf] cf. Gtl/s lgo. Gq 0](https://slidetodoc.com/presentation_image_h2/1f569fe110ede50c6de824e9a8e63853/image-16.jpg "cfly{s sfo{ljlw lgodfjn. L, @)^$======= �-@_ pklgod -!_ adf]lhdsf] cf. Gtl/s lgo. Gq 0")

^$==== �cf. Gtl/s lgo. Gq 0 f k|0 ffn. Lnf.")

![g]kfndf cf. Gtl/s lgo. Gq 0 f ; Dj. Gw. L Joj: yf •](https://slidetodoc.com/presentation_image_h2/1f569fe110ede50c6de824e9a8e63853/image-18.jpg "g]kfndf cf. Gtl/s lgo. Gq 0 f ; Dj. Gw. L Joj: yf •")

![cjsf] af 6 f]===== • cf. Gtl/s lgo. Gq 0 f k|0 ffn. Lsf]](https://slidetodoc.com/presentation_image_h2/1f569fe110ede50c6de824e9a8e63853/image-24.jpg "cjsf] af 6 f]===== • cf. Gtl/s lgo. Gq 0 f k|0 ffn. Lsf]")

![n]vfk/LIf 0 f �cfly+s sf/f]jf/; u ; Dal. Gwt n]vf, sfuhft / clen]vsf] :](https://slidetodoc.com/presentation_image_h2/1f569fe110ede50c6de824e9a8e63853/image-25.jpg "n]vfk/LIf 0 f �cfly+s sf/f]jf/; u ; Dal. Gwt n]vf, sfuhft / clen]vsf] :")

![n]vfk/LIf 0 fsf] p 2]Zo �lal. Qo laj/0 fsf] z'4 tf k/LIf 0 f](https://slidetodoc.com/presentation_image_h2/1f569fe110ede50c6de824e9a8e63853/image-26.jpg "n]vfk/LIf 0 fsf] p 2]Zo �lal. Qo laj/0 fsf] z'4 tf k/LIf 0 f")

![n]vfk/LIf 0 fsf l; 4 f. Gt / b[li 6 sf]0 f Principles/Core values](https://slidetodoc.com/presentation_image_h2/1f569fe110ede50c6de824e9a8e63853/image-27.jpg "n]vfk/LIf 0 fsf l; 4 f. Gt / b[li 6 sf]0 f Principles/Core values")

![cf. Dbfg. L Pj_ vr+ sfg'g; _Ddt 9_ujf 6 ul/Psf] 5 5}g, n]vfk/LIf 0](https://slidetodoc.com/presentation_image_h2/1f569fe110ede50c6de824e9a8e63853/image-28.jpg "cf. Dbfg. L Pj_ vr+ sfg'g; _Ddt 9_ujf 6 ul/Psf] 5 5}g, n]vfk/LIf 0")

![n]vfk/LIf 0 fsf k|sf/ �lal. Qo n]vfk/LIf 0 f. M lal. Qo laj/0 fsf]](https://slidetodoc.com/presentation_image_h2/1f569fe110ede50c6de824e9a8e63853/image-29.jpg "n]vfk/LIf 0 fsf k|sf/ �lal. Qo n]vfk/LIf 0 f. M lal. Qo laj/0 fsf]")

![a]? h" / a]? h" km 5of}{6 � a]? h' sf] kl/efiff �; fdf.](https://slidetodoc.com/presentation_image_h2/1f569fe110ede50c6de824e9a8e63853/image-30.jpg "a]? h\" / a]? h\" km 5of}{6 � a]? h' sf] kl/efiff �; fdf.")

![a]? h"df sf/jfx. L ug]{ ; Dj. Gw. L sfg'g. L Joj: yf �cfly{s](https://slidetodoc.com/presentation_image_h2/1f569fe110ede50c6de824e9a8e63853/image-31.jpg "a]? h\"df sf/jfx. L ug]{ ; Dj. Gw. L sfg'g. L Joj: yf �cfly{s")

![a]? h' km 5of}{6 sf sfg'g. L cfwf/ M ; f/f+zdf ! �k|df 0](https://slidetodoc.com/presentation_image_h2/1f569fe110ede50c6de824e9a8e63853/image-32.jpg "a]? h' km 5of}{6 sf sfg'g. L cfwf/ M ; f/f+zdf ! �k|df 0")

![a]? h' km 5of}{6 sf sfg'g. L cfwf/ M ; f/f+zdf @ v= c;](https://slidetodoc.com/presentation_image_h2/1f569fe110ede50c6de824e9a8e63853/image-33.jpg "a]? h' km 5of}{6 sf sfg'g. L cfwf/ M ; f/f+zdf @ v= c;")

![a]? h' km 5of}{6 sf sfg'g. L cfwf/ M ; f/f+zdf # u= ld.](https://slidetodoc.com/presentation_image_h2/1f569fe110ede50c6de824e9a8e63853/image-34.jpg "a]? h' km 5of}{6 sf sfg'g. L cfwf/ M ; f/f+zdf # u= ld.")

![a]? h" km 5of}{6 ; Dj. Gw. L ; d: ofx? M ; f/f+zdf](https://slidetodoc.com/presentation_image_h2/1f569fe110ede50c6de824e9a8e63853/image-35.jpg "a]? h\" km 5of}{6 ; Dj. Gw. L ; d: ofx? M ; f/f+zdf")

![cfly{s clgoldttf tyf a]? h"; Da. Gw. L ; d: of ; dfwfgsf s]lx](https://slidetodoc.com/presentation_image_h2/1f569fe110ede50c6de824e9a8e63853/image-36.jpg "cfly{s clgoldttf tyf a]? h\"; Da. Gw. L ; d: of ; dfwfgsf s]lx")

![qmdz. M ==== �; fj{hlgs lgodgsf/L lgsfox¿sf] k"j{lqmofz. Lntf a 9 fpg' kg]{ �n]vfk/LIf](https://slidetodoc.com/presentation_image_h2/1f569fe110ede50c6de824e9a8e63853/image-37.jpg "qmdz. M ==== �; fj{hlgs lgodgsf/L lgsfox¿sf] k\"j{lqmofz. Lntf a 9 fpg' kg]{ �n]vfk/LIf")

- Slides: 39

20/12/2021 1

cf. Gtl/s lgo. Gq 0 f / n]vfk/LIf 0 f tyf a]? h' s[i 0 f k|; fb ltl. D; gf k|d'v sf]if lgo. Gqs (*$!#@)$$%

Internal Control Defined The COSO publication Internal Control – Integrated Framework defines internal control as Internal control is process , effected by an entity’s board of directors , management and other personnel , designed to provide reasonable assurance regarding the achievement of objectives in the following categories �Effectiveness and efficiency of operations. �Reliability of financial reporting. �Compliance with applicable laws and regulations

Internal Control Defined �Fundamental concepts are inherent in this definition: v. Internal control is a process effected by people at all organizational levels. v. Management and board receive reasonable, not absolute assurance. v. Internal control is geared toward the achievement of organizational objectives. In brief , internal control enable an entity’s management to achieve the organization’s mission , goals and objectives.

Internal Control Frameworks The COSO Framework What is COSO? COSO = Committee of Sponsoring Organization (the USA) established in 1980. �American Institute of Certified Public Accounts �American Accounting Association �Financial Executive Institute �The Institute of Internal Auditors �The Institute of management Accountants COSO’s mission was to improve the quality of financial reporting through a focus on corporate governance internal control and ethical standards.

Framework for RMS: COSO ERM https: //image. slidesharecdn. com/enterpriseriskmanagement-150220032546 -conversiongate 01/95/enterprise-risk-management-23 -638. jpg? cb=1424402804 20/12/2021 6

COSO Report �In 1992 COSO published Internal Control—Integrated Framework, a report that established a common definition of internal control and provided a standard through which organizations could assess and improve their control systems

The COSO Framework According to COSO model , internal control provides reasonable assurance to an organization regarding the achievement of objectives in the following areas. �Effectiveness and efficiency of operations This category is related to an organization’s basic business objectives including performance , profitability, and safeguarding of resources. �Reliability of financial reporting Financial reporting encompasses the preparation of reliable financial statements. �Compliance with applicable laws and regulation This category includes all laws and regulations that apply to the organization.

The COSO Components The five inter-related components of COSO’s internal control framework CONTROL ENVIRONMENT The attitude and actions of the board and management regarding the importance of control within the organization. The control environment provides the discipline and structure for the achievement of the primary objectives of the system of internal control. The control environment includes the following elements: � Integrity and ethical values. � Management’s philosophy and operating style. � Organizational structure. � Assignment of authority and responsibility. � Human resource policies and practices. � Competence of personnel.

The COSO Components RISK ASSESMENT The identification and analysis of relevant risks to the achievement of objectives , forming a basis for determining how the risks should be managed. CONTROL ACTIVITIES These are the policies and procedures that help ensure that management’ objectives are carried out. Control activities are designed to prevent and detect errors and omissions and the conduct of routine business functions. Examples include physical and logical security to prevent unauthorized access to resource , segregation of duties.

The COSO Components INFORMATION AND COMMUNICATION Pertinent information must be identified captured and communicated in a form and time frame that enable people to carry out their responsibilities. Effective communication must also occur in a boarder sense flowing down, across and up the organization. MONITORING Internal control system should be monitored - a process that assesses the quality of the system’s performance over time. This is accomplished through ongoing monitoring activities, separate evaluation , or a combination of two.

Framework for RMS: COSO ERM 2017 http: //www. manorgroup. net/images/tmp 5704. png 20/12/2021 12

Framework for RMS: Implimentation http: //4. bp. blogspot. com/j 0 w. Xbigltm. Y/T 7 v. V 3 A 9 l. S 5 I/AAAAAXc/68 hp 9 p. ZF 4 X 4/s 1600/RM+Framework. png 20/12/2021 13

RELATIONSHIPS BETWEEN RISK MANAGEMENT PRINCIPLES, FRAMEWORK AND PROCESS a) Creates value b) Integral part of organizational processes c) Part of decision making d) Explicitly addresses uncertainty e) Systematic, structured and timely f) Based on the best available information g) Tailored h) Takes human and cultural factors into account i) Transparent and inclusive j) Dynamic, iterative and responsive to change k) Facilitates continual improvement and enhancement of the organization Principles (Clause 3) Mandate and Commitment (4. 2) Design of framework (4. 3) Continual improvement of the Framework (4. 6) Implementing risk Management (4. 4) Monitoring and review of the Framework (4. 5) Framework (Clause 4) C o m u n i c a t i o n & c o n s u l t a t i o n 5. 2 Establishing the context (5. 3) M o n i t o r i n g Risk assessment (5. 4) Risk identification (5. 4. 2) Risk analysis (5. 4. 3) & Risk evaluation (5. 4. 4) r e v i e w (5. 6) Risk treatment (5. 5) Process (Clause 5) ISO 31000: 2009 Figure 1 – Relationship between the principles, framework and process 14

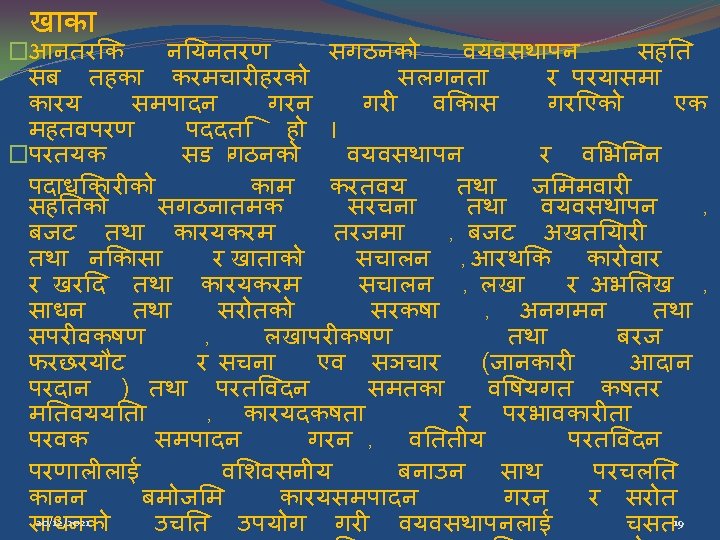

cf. Gtl/s lgo. Gq 0 f k|0 ffn. L cfly{s sfo{ljlw lgodfjn. L, @)^$ �@ -ª_ æcf. Gtl/s lgo. Gq 0 fÆ e. Ggfn] sfg"gn] lg. Wff{/0 f u/]sf k|s[of kl/kfngf eof] e. Pg eg. L tfn's sfof{noaf 6 lg/Gt/ ? kdf ul/g] ; 'kl/j]If 0 f / cg'udg sfo{ ; Demg' k 5{. �(%= cf. Gtl/s lgo. Gq 0 f ; Da. Gw. L Joj: yf M -!_ k|To]s d. Gqfno, ; lrjfno, ; +j}wflgs cË, ljefu. Lo k|d'vn] cfkm" / c. Gtu{t lgsfoaf 6 ; Dkfbg ul/g] sfo{x? ldt. Joo. L, sfo{b. Iftf / k|efjsf/L 9+uaf 6 ; Dkfbg ug{, ljt. Lo k|ltj]bg k|0 ffn. L nf. O{ lj. Zj; g. Lo agfpg tyf k|rlnt sfg"g adf]lhd sfo{ ; Dkfbg ug{ cf–cfkmgf] sfdsf] k|s[lt cg'; f/sf] cf. Gtl/s lgo. Gq 0 f k|0 ffn. L tof/ u/L of] lgod k|f/De e. Psf] Ps jif{leq nfu" u/L ; Sg' kg]{5. 20/12/2021 15

cfly{s sfo{ljlw lgodfjn. L, @)^$======= �-@_ pklgod -!_ adf]lhdsf] cf. Gtl/s lgo. Gq 0 f k|0 ffn. L tof/ ubf{ lgsfout sfdsf] k|s[lt cg'? k cfj. Zos s'/fx? sf] Joj: yf ug'{ kg]{5 / To; df lgo. Gq 0 fsf] jftfj/0 f, hf]lvd If]qsf] klxrfg, ; "rgfsf] cfbfg k|bfg, cg'udg tyf d"NofÍg h: tf ljifonf. O{ ; d]t ; d]l 6 g' kg]{5. �-#_ pklgod -!_ / -@_ adf]lhdsf] cf. Gtl/s lgo. Gq 0 f k|0 ffn. Lsf] cg'udg ug{sf nflu ; Dal. Gwt d. Gqfno, ; lrjfno, ; +j}wflgs cË tyf ljefu. Lo k|d'vn] lh. Dd]jf/ clwsf/L tf]s. L cg'udg ug]{ Joj: yf ldnfpg' kg]{5. �-$_ pklgod -#_ adf]lhd ul/Psf] cg'udgaf 6 b]lv. Psf q'l 6 nf. O{ ; 'wf/ u/L 20/12/2021 16

cfly{s sfo{ljlw lgodfjn. L, @)^$==== �cf. Gtl/s lgo. Gq 0 f k|0 ffn. Lnf. O{ ; 'b[9 jgfpg] lh. Dd]jf/L pklgod -!_ df pl. Nnlvt lgsfosf] x'g]5. �-%_ tfn's sfof{non] o; lgodfjn. L adf]lhd dftxtsf sfof{non] tf]ls. Psf] sfo{x? k|efjsf/L ? kdf kl/kfngf u/] gu/]sf], cfly{s cg'zf; g / lgb]{zgsf] kfngf u/] gu/]sf] ; 'kl/j]If 0 f / cg'udg ug'{ kg]{5. �-^_ pklgod -%_ adf]lhdsf] ; 'kl/j]If 0 f / cg'udg jif{sf] s. Dt. Ldf b'O{ k 6 s ug'{ kg]{5. tfn's sfof{non] cg'udg / ; 'kl/j]If 0 fsf] cfwf/df b]lv. Psf s}lkmotsf] ; 'wf/sf] nflu dftxt sfof{nonf. O{ lgb]{zg lbg' kg]{5 / To: tf] lgb]{zgsf] kfngf ug'{ dftxtsf sfof{nosf] st{Jo x'g]5. 20/12/2021 17

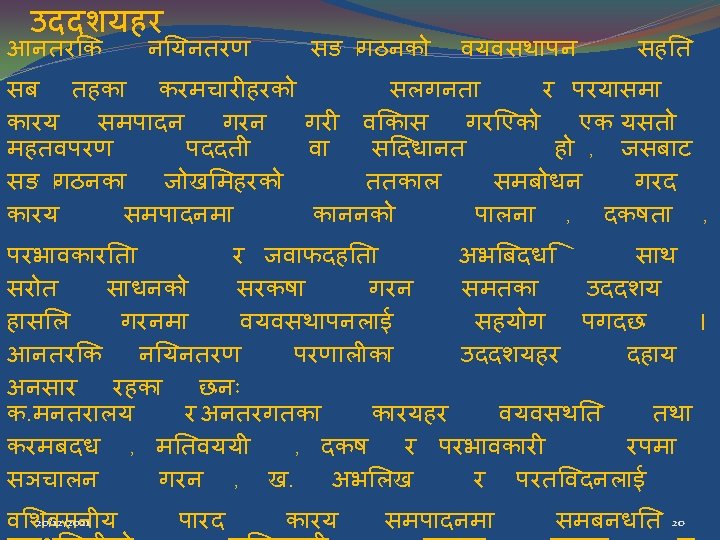

g]kfndf cf. Gtl/s lgo. Gq 0 f ; Dj. Gw. L Joj: yf • k'/: s[t ug]{ k|0 ffn. L - ljle. Gg lghfd. Tf. L k'? : sf/x? _ • Accounting , Budgeting and Reporting sf] Joj: yf • e|i 6 frf/ lgo. Gq 0 f / ; bfrf/ ; Dj. Gw. L sfg'g. L Joj: yf • clwsf/ k|Tofof]hgsf] Joj: yf • sfo{ ljefhg k|0 ffn. L • ; "rgf k|ljlw lgo. Gq 0 f ; Dj. Gw. L k¢lt • ; Dklt ; '/Iff ; Dj. Gw. L ef}lts Pj+ sfg'g. L Joj: yf

cf. Gtl/s lgo. Gq 0 f ; Dj. Gw. L ; d: of • cf. Gtl/s lgo. Gq 0 f k|0 ffn. Lnf. O{ ; +u 7 g ljsf; sf] ; fws dflgb}g, • lgo. Gq 0 fsf] jftfj/0 f pko'St 5}g - g}ltstf / ; bfrf/sf] sd. L, sd{rf/Lsf] b. Iftfsf] sd. L, e¢f ; /sf/L ; +u 7 g, b"/b[li 6 sf] cefj, clwsf/ / lh. Dd]jf/Lsf] c: ki 6 tf, cg'ko'St dfgj ; +; fwg g. Llt_ • k|rlnt P]g, sfg'gsf] kl/kfngfsf] sd. L • hf]lvd lj. Zn]if 0 f ug]{ k|j[lt 5}g • cf. Gtl/s lgo. Gq 0 f ; Dj. Gw. L sfg'g. L Joj: yf ck'/f] / c: ki 6 • cf. Gtl/s lgo. Gq 0 f ; Dj. Gw. L Ps. Ls[t 9 f+rf tof/ 5}g • cf. Gtl/s lgo. Gq 0 f ; Dj. Gw. L ; r]tgfsf] cefj • sfg'g jdf]lhd cf. Gtl/s lgo. Gq 0 f ; Dj. Gw. L k|0 ffn. L sfof{nox? n] tof/ gug'{ • cg'udg / d"NofÍg cf}krfl/stfdf ; Lldt • lj. Tt. Lo k|ltj]bg k|0 ffn. Lsf] lj. Zj; lgotfsf] sd. L

cjsf] af 6 f]===== • cf. Gtl/s lgo. Gq 0 f k|0 ffn. Lsf] dx. Tjjf/] ; r]tgf j[l¢. • Ethical tone at the top communicated in words and deeds. • cf. Gtl/s lgo. Gq 0 f ; Dj. Gw. L gd'gf 9 f+rf tof/ u/L nfu" ug]{ -cfly{s sfo{ljlw lgodfjn. Ldf cg'; 'r. Lsf] ? kdf ; +n. Ug ug]{ _. • sfg'g. L kl/efiffnf. O{ Jofks jgfpg]. • ; d. Gjo a 9 fpg] -Joj: yfkg, cf. Gtl/s Pj+ cl. Gtd n]vfk/LIfs, sd{rf/L sfdbf/ _. • hf]lvd lj. Zn]if 0 f ug]{ kl/kf 6 Lsf] ljsf; . • lgo. Gq 0 fsf] jftfj/0 f tof/ ug]{ -x/]s ; +u 7 gn]_. • cf. Gtl/s lgo. Gq 0 f k|0 ffn. Lnf. O{ ; +u 7 gsf] clgjfo{ s[ofsnfksf] ? kdf : j. Lsfg]{.

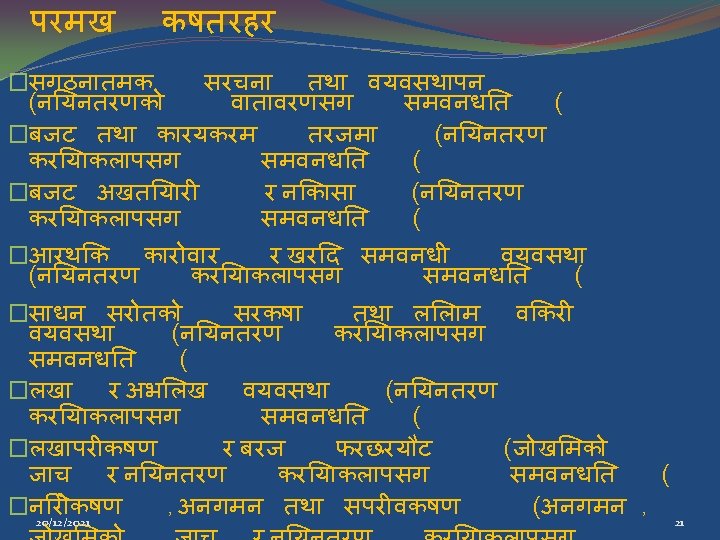

n]vfk/LIf 0 f �cfly+s sf/f]jf/; u ; Dal. Gwt n]vf, sfuhft / clen]vsf] : jt. Gq Pj lgik. If ? kn] ul/]g] k/LIf 0 f g} n]vfk/LIf 0 f xf]. �n]vfk/LIf 0 fn] n]vfsf] hfr / ; f]sf] cfwf/df ul/g] d"Nofsg tyf la. Zn]if 0 f ; d]tnf. O+ hgfp_5. �Auditing starts when the accounting ends �n]vfk/LIf 0 fsf nflu k|rlnt P]g, sfg"g, g. Llt, lgod, sfo+qmd, k|zf; lgs lg 0 f+o, ; Demf}tf tyf n]vfk/LIf 0 f dfgb 08 nf. O+ cfwf/ dflg. G 5. 25

n]vfk/LIf 0 fsf] p 2]Zo �lal. Qo laj/0 fsf] z'4 tf k/LIf 0 f ug]{ �k|rlnt sfg"gsf] kfngf l: yltsf] k/LIf 0 f ug]{ �; |f]t ; fwgsf] p 2]Zod"ns pkof]usf] d"Nof+sg ug]{ �cf. Gtl/s lgo. Gq 0 f k|0 ffn. Lsf] d"Nof+sg ug]{ �; ]jf k|jfxsf] k|efjsf/Ltfsf] d"Nof+sg ug]{ �; fj{hlgs ; Dkl. Qsf] ; +/If 0 f / pkof]usf] la. Zn]if 0 f ug]{ �cg'udg d"Nof+sg / k[i 7 kf]if 0 fsf] d"Nof+sg ug]{

n]vfk/LIf 0 fsf l; 4 f. Gt / b[li 6 sf]0 f Principles/Core values �Independence and Objectivity �Integrity and code of conduct �Due care �Confidentiality �Competency �Professional spectism Approach �Process oriented �Result oriented �Problem oriented

cf. Dbfg. L Pj_ vr+ sfg'g; _Ddt 9_ujf 6 ul/Psf] 5 5}g, n]vfk/LIf 0 f (Final Audit) cfly+s ljj/0 f ; lx Pj_ oyf+yk/s 9_un] tof/ e. P ge. Psf] Financial Attestation cfly+s ljj/0 fsf] k|dfl 0 ft. Ls/0 f lgoldttfsf] n]vfk/LIf 0 f Regularity Audit sfo+d'ns n]vfk/LIf 0 f Performance Audit ; |f]t ; fwgsf] k|f. Kt. L Pj_ pkof]u ubf+ ldt. Joo. Ltf, sfo+b. Iftf / k|efjsf/Ltf /x] g/x]sf]

n]vfk/LIf 0 fsf k|sf/ �lal. Qo n]vfk/LIf 0 f. M lal. Qo laj/0 fsf] z'4 tf k/LIf 0 f ul/G 5, (Statutory audit: It is as same as the purpose of any other type of audit to determine whether an organization is providing a fair and accurate representation of its financial position by examining information such as bank balances, bookkeeping records and financial transactions. ) �lgoldttfsf] n]vfk/LIf 0 f. M k|rlnt P]g sfg"gsf] k/Lkfngf e. P ge. Psf] ; Da. Gwdf k/LIf 0 f ul/G 5, �sfo{d"ns tyf laz]if n]vfk/LIf 0 f. M ldt. Joo. Ltf, sfo{b. Iftf, k|efjsf/Ltfsf] d"Nof+sg u/L k/LIf 0 f ul/G 5. o; df d'Votof >f]tsf] k|f. Kt. L, pkof]u / p 2]Zo k|f. Kt. Lsf] la. Zn]if 0 f ul/G 5. ldt. Joo. Ltf eg]sf] Go"gtd nfutdf ; |f]t k|f. Kt ug'{, sfo{b. Iftf eg]sf] lgl. Zrt nfut / u'0 f: t/df a 9 L k/Ldf 0 f k|f. Kt ug'{ jf lgl. Zrt k/Ldf 0 f k|f. Kt ug{ nfutdf sd. L Nofpg', k|efjsf/Ltf eg]sf] lgl. Zrt p 2]Zo jf k|efj xfl; n ug'{ xf]. laz]if n]vfk/LIf 0 f laz]if p 2]Zo k|f. Kt. Lsf] nfu. L ul/G 5.

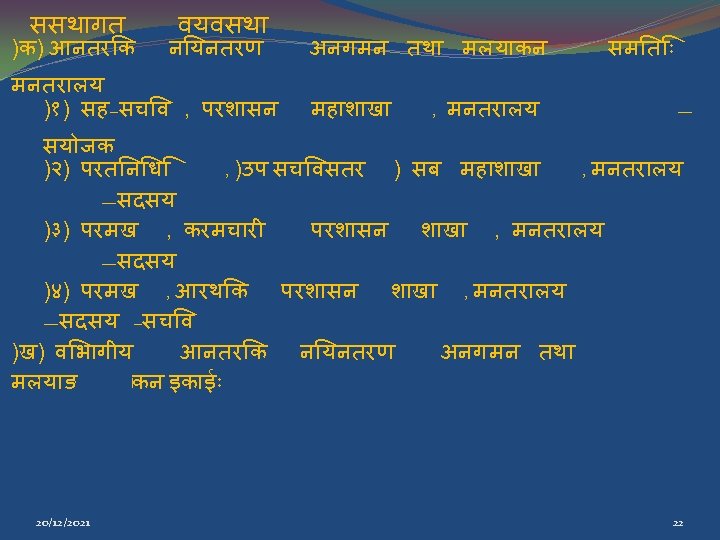

a]? h" / a]? h" km 5of}{6 � a]? h' sf] kl/efiff �; fdf. Go cy{df a]? h" eg]sf] sfg'gsf] /Lt gk'¥of. O{ jf sfg"g ljkl/t ul/Psf lg 0 f{o, sf/f]jf/ Pjd sf/jfx. L xf]. �cfly{s sfo{ljlw P]g, @)%% df æa]? h" e. Ggfn] k|rlnt sfg'g adf]lhd k'¥ofpg' kg]{ /Lt gk'¥of. O{ sf/f]af/ u/]sf] jf /f. Vg' kg]{ n]vf g/fv]sf] tyf clgoldt jf a]dgfl; a tl/sfn] cfly{s sf/f]af/ u/]sf] eg. L n]vfk/LIf 0 f ubf{ cf}+Nof. OPsf] jf 7 x¥of. OPsf] sf/f]af/ ; D´g' k 5{Æ eg]/ kl/efiff ul/Psf] 5. �jf: tjdf cf. Gtl/s / cl. Gtd n]vfk/LIf 0 f ubf{ b]lvg cfpg] s}lkmotx? (Audit Observations) g} a]? h" xf]. 20/12/2021 30

a]? h"df sf/jfx. L ug]{ ; Dj. Gw. L sfg'g. L Joj: yf �cfly{s sfo{ljlw P]g tyf lgodfjn. Ldf a]? h" km 5of{}6 ug]{ u/fpg] tyf km 5of}{6 ; Dj. Gw. L sfd sf/jfx. Lsf] cg'udg ug]{ / lgoldt ug{ ld. Ng] a]? h"x? lgoldt ug]{ clwsf/ / bflo. Tj n]vf p. Q/bfo. L clws[tnf. O{ k|bfg u/]sf] �sfg'gdf a]? h"x? sf] nut /f. Vg] / a]? h"x? sf] k|df 0 f k]z ug]{ jf ; f] c; "n km 5of}{6 sf] nflu sf/jfx. L cufl 8 j 9 fpg] tyf ; Dk/LIf 0 f u/fpg] bflo. Tj lh. Dd]jf/ Jol. Qm ; d]t ; Djl. Gwt sfof{no k|d'vsf] eg. L tf]ls. Psf] �a]? h" km 5of{}6 ; Dj. Gw. L sfo{ gug]{ dfly k|rlnt sfg'g jdf]lhd hl/jfgf jf ljefu. Lo sf/jfx. L Ps jf b'j} ug]{ clwsf/ tfn's lgsfonf. O{ lb. Psf] 20/12/2021 31

a]? h' km 5of}{6 sf sfg'g. L cfwf/ M ; f/f+zdf ! �k|df 0 f e. Psf]df k|df 0 f k]z u/L a]? h' km 5of}{6 ug]{ c. Goyf lg. Dgfg'; f/ ug'{kg]{. s= lgoldt ug]{M (In general, compliance means conforming to a rule, such as a specification, policy, standard or law. Regulatory compliance describes the goal that organizations aspire to achieve in their efforts to ensure that they are aware of and take steps to comply with relevant laws, policies, and regulations. ) cfly{s sfo{ljlw lgodfjn. L, @)^$ sf] lgod !))-!_-@_-#_ cg'; f/ n]vf p. Q/bfo. L clws[tn] k|rlnt sfg'g adf]lhd lgoldt ug{ ld. Ng] a]? h' lgod !))-!_ cg'; f/ cfkm}+n] jf lgod !))-@_ cg'; f/ a'´L jf lgod !))-#_ cg'; f/ sfof{no k|d'v / ljefu. Lo k|d'vsf] l; kmfl/; df lgoldt ug'{kg]{. 20/12/2021 32

a]? h' km 5of}{6 sf sfg'g. L cfwf/ M ; f/f+zdf @ v= c; 'n ug]{M (Arrears (or arrearage) is a legal term for the part of a money that is overdue after missing one or more required payments. The amount of the arrears is the amount accrued from the date on which the first missed payment was due. ) cfly{s sfo{ljlw P]g, @)%% sf] bkmf @)-#_, bkmf @@, bkmf #) cg'; f/ / cfly{s sfo{ljlw lgodfjn. L, @)^$ sf] lgod !)# cg'; f/, t. Tsfn k|of; -kqfrf/ / tfs]tf, t. Lg k': t] ljj/0 f sd{rf/Lsf] xsdf lghfdt. L lstfj vfgf jf lgj[Qe/0 f Joj: yfkg sfof{no, ; +: yfsf] xsdf ; +: yf btf{ e. Psf] lgsfo / c. Gosf] xsdf kflnsf jf : yfg. Lo k|zf; g, k|x/L dfkm{t k|f. Kt ug{] / ; f] ; lxtsf] ljj/0 f #% lbgsf] Dofb lb. P/ s]Gb|Ls[t ; "rgf klqsfdf k|sfzg_ u/]/ p 7 fpg] jf Ps jif{ leq k|of; ubf{ klg p 7 fpg g; ls. Pdf, ; f] ; do kl 5 cg'; "r. L !% e/L d. Gqfno dfkm{t s]Gb|Lo txl; n sfof{nodf k 7 fpg]. 20/12/2021 33

a]? h' km 5of}{6 sf sfg'g. L cfwf/ M ; f/f+zdf # u= ld. Gxf ug]{M cfly{s sfo{ljlw lgodfjn. L, @)^$ sf] lgod !))-$_ cg'; f/ lgoldt ug{ dgfl; a sf/0 f b]v]df / To; sf nflu ld. Gxf lbg' kg]{ e. Pdf jf a]? h'df c; 'n ug]{ eg. L n]lv. Ptf klg sf/0 f ; lxt n]vf p. Q/bfo. L clws[tn] ls 6 fg. L; fy c; 'n ug{ gkg]{ 7 x¥of. Psf] a]? h' /sd, cfly{s sfo{ljlw P]g, @)%% sf] bkmf @( cg'; f/ c; 'n ug]{ k|of; ubf{ klg p 7g g; s]sf] ; /sf/L af. Fs. L /sd jf k|fs[lts k|sf]k tyf sfa" aflx/sf] kl/l: yltn] jf lnnfd a 9 fa 9 x‘'bf klg gp 7]sf] /sddfq cfly{s sfo{ljlw lgodfjn. L, @)^$ sf] lgod !)^ cg'; f/ ld. Gxf lbg k]z ug]{. 20/12/2021 34

a]? h" km 5of}{6 ; Dj. Gw. L ; d: ofx? M ; f/f+zdf s_ sfg'g sfo{f. Gjogsf] / lh. Dj]jf/L jf]wsf] : t/ sdhf]/ x'g' v_ ; qmd 0 fsfn / cl: y/tf ; d]tsf sf/0 fn] cf. Gtl/s lgo. Gq 0 f / cg'udg Joj: yf k|efjsf/L x'g g; Sg' u_ n]vf p. Q/bfo. L clws[tx? jf 6 p. Q/bflo. Tjsf] efjgf cg'? k sfo{ ; Dkfbg ug{ g. Llt, sfg'g, ; +/rgf / k|0 ffn. L Jojl: yt x'g g; Sg' 3_ a]? h" km 5of}{6 ; Da. Gw. L g. Llt, sfg'g, ; +/rgf / k|0 ffn. L cfj. Zostf cg'; f/ k|efjsf/L agfpg g; lsg' 20/12/2021 35

cfly{s clgoldttf tyf a]? h"; Da. Gw. L ; d: of ; dfwfgsf s]lx pkfox? �a]? h" km 5of}{6 u/L z"Go ug]{; Da. Gw. L g. Llt th'{df u/L cfly{s k|zf; gdf : j. R 5 tf, hjfkmb]lxtf Pj+ kf/blz{tf k|j 4{g ug'{kg]{ �sd{rf/Lnf. O{ lh. Dd]jf/ agf. O{ P]g lgod kl/kfngfsf] : t/ a 9 fpg' kg]{ �cf. Gtl/s lgo. Gq 0 f k|0 ffn. L : yflkt / Jojl: yt ug'{kg]{ �cfly{s sf/f]af/df cg'zf; gsf] : t/ a 9 fpg' kg]{ 20/12/2021 36

qmdz. M ==== �; fj{hlgs lgodgsf/L lgsfox¿sf] k"j{lqmofz. Lntf a 9 fpg' kg]{ �n]vfk/LIf 0 f / ; Dk/LIf 0 fsf] sfo{nf. O{ sfg'gdf tf]ls. Psf] Go"gtd ; do l; df leq ; Dk. Gg ug]{ tkm{ p. Gd'v x'g'kg]{ �; Da 4 kbflwsf/Lx¿df hjfkmb]lxtfsf] : t/ j[l¢ ug'{kg]{ �a]? h" km 5of{}6; Da. Gw. L ljle. Gg lgsfo / ; ldltx¿sf] k|efjsfl/tf j[l¢ ug'{kg]{ 20/12/2021 37

? 20/12/2021 38

w. Gojfb ! 20/12/2021 39