2007 Thomson SouthWestern The Basic Tools of Finance

© 2007 Thomson South-Western

The Basic Tools of Finance This chapter introduces some tools that help us understand the decisions that people make as they participate in the loanable funds market. Finance is the field that studies how people make decisions regarding the allocation of resources over time and the handling of risk. © 2007 Thomson South-Western

Three topics in Chapter 27 • How to compute the value of money at different points of time • How to manage risk • What determines the value of an asset. © 2007 Thomson South-Western

refers to the")

PRESENT VALUE: MEASURING THE TIME VALUE OF MONEY • Present value(現值,PV) refers to the amount of money today that would be needed to produce, using prevailing interest rates, a given future amount of money at time T ( ): 0 PV T © 2007 Thomson South-Western

Present Value vs. Future Value • The concept of present value is used to answer the following question: Suppose you are going to be paid 1 dollar in T years. How much would you have to put in a bank account today? PV× =$1 → PV= This process is called discounting. (折現) © 2007 Thomson South-Western

is used")

Present Value vs. Future Value • The concept of future value (終值,FV) is used to answer the following question: If you put $1 in a bank account today, how much will it be worth in T year? We can use the compounding (複利計息) process to get the future value of $1 today: FV(T)= $1 in which r is the interest rate and FV(T) in the future value at time T. © 2007 Thomson South-Western

PRESENT VALUE: MEASURING THE TIME VALUE OF MONEY • The concept of present value demonstrates the following: – Receiving a given sum of money in the present is preferred to receiving the same sum in the future. – In order to compare values at different points in time, compute their present values first. – Firms undertake investment projects if the present value of the project exceeds the cost of the project. © 2007 Thomson South-Western

Valuing a stream of cash flows • Most investment opportunities have multiple cash flow that occur at different points in time. • Consider a stream of cash flow in different points of time. 0 1 2 3 . . . T © 2007 Thomson South-Western

Valuing a stream of Cash flows • We first compute the present valus of each individual cash flow in different points of time: PV( )= i= 1, 2, …. , T. Then we can sum them up to get PV= © 2007 Thomson South-Western

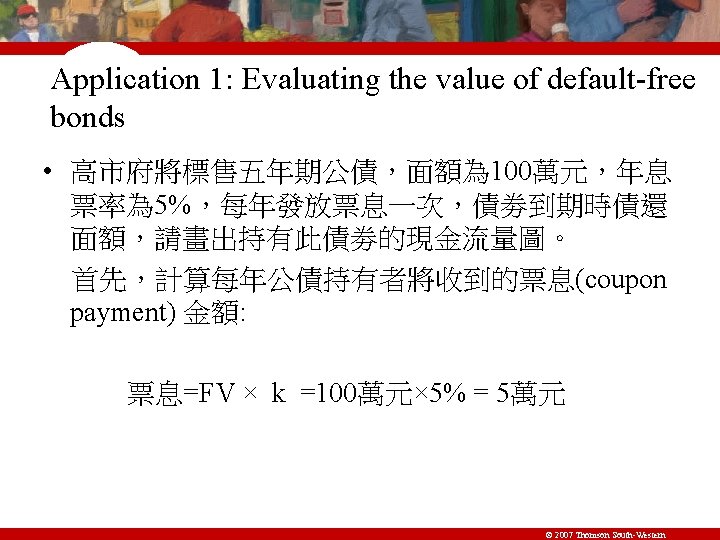

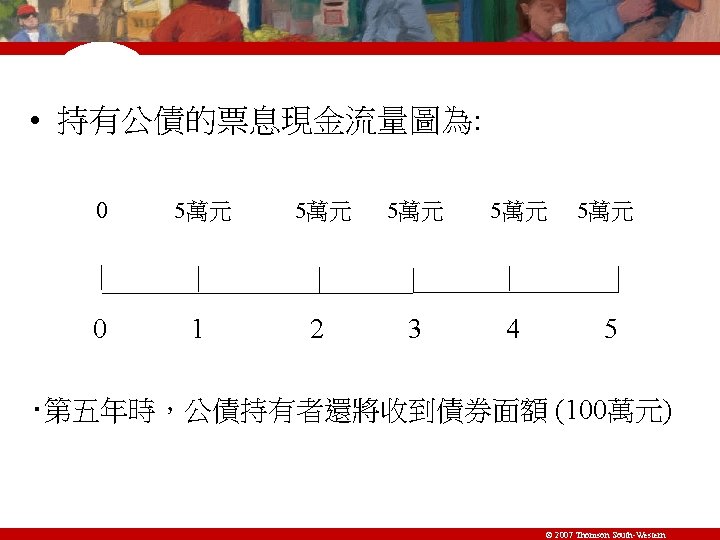

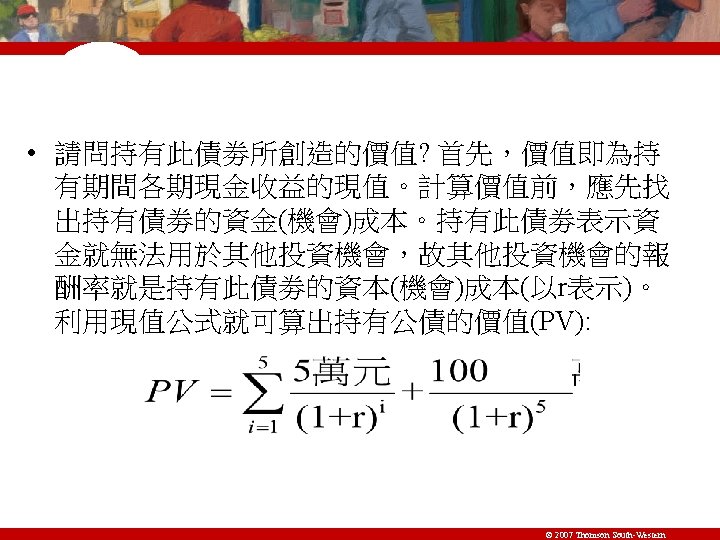

Application 1: Evaluating the value of default-free bonds • Elements of bond --Face value (FV, 面額) --Coupon rate (k , 息票率) --Maturity date (到期日) --The date to return principal (面額償還時間) © 2007 Thomson South-Western

Application 2: Evaluating a real investment project • Suppose firm A is considering a 10 -year real investment project. The capital expenditure of this project is. This project will yield this firm operating cash flow in 10 years: © 2007 Thomson South-Western

Application 2: Evaluating a real investment protect • The cash flow chart for this project: 0 1 2 3 。 。 。 10 Then the net present value (淨現值,NPV) is given by in which r is the opportunity cost of capital. © 2007 Thomson South-Western

Application 2: Evaluating a real investment protect • Given the market interest rate r. We can compute NPV. If NPV> 0, then we undertake this project. Otherwise, we reject it. • The concept of net present value helps explain why real investment -and thus the quantity of loanable funds demanded -declines when the interest rate rises. © 2007 Thomson South-Western

Application 2: Evaluating a real investment protect • When the economy is in recession, central bank can lower the interest rate (r) to stimulate the incentive to undertake the investment project, since the NPV will increase as r decreases. © 2007 Thomson South-Western

Rule of 70 • According to the rule of 70, if some variable grows at a rate of x percent per year, then that variable doubles in approximately 70/x years. © 2007 Thomson South-Western

MANAGING RISK • Risk Aversion – A person is said to be risk averse (風險厭惡)if he or she exhibits a dislike of uncertainty. – Individuals can reduce risk choosing any of the following: • Buy insurance • Diversify (分散投資) • Accept a lower return on their investments © 2007 Thomson South-Western

Risk Aversion Utility gain from winning $1, 000 Utility loss from losing $1, 000 0 $1, 000 loss Current wealth Wealth $1, 000 gain © 2007 Thomson South-Western

The Markets for Insurance • One way to deal with risk is to buy insurance. • The general feature of insurance contracts is that a person facing a risk pays a fee to an insurance company, which in return agrees to accept all or part of the risk. © 2007 Thomson South-Western

Diversification of Firm-Specific Risk • Diversification refers to the reduction of risk achieved by replacing a single risk with a large number of risks. • Firm-specific risk (or unique risk)is risk that affects only a single company. • Market risk (or systematic risk)is risk that affects all companies in the stock market. • Diversification cannot remove market risk. © 2007 Thomson South-Western

1. Increasing the")

Diversification can eliminate unique risk Risk (standard deviation of portfolio return) 1. Increasing the number of stocks in a portfolio reduces firm-specific risk through diversification… (More risk) 49 2. …but market risk remains. 20 (Less risk) 0 1 4 6 8 10 20 30 40 Number of Stocks in Portfolio © 2007 Thomson South-Western

Diversification of Firm-Specific Risk • People can reduce risk by accepting a lower rate of return. © 2007 Thomson South-Western

8. 0 The Trade-off between Risk and Return 25% stocks")

Return (percent per year) 8. 0 The Trade-off between Risk and Return 25% stocks 50% stocks 75% stocks 100% stocks No stocks 3. 0 0 5 10 15 Risk 20 (standard deviation) © 2007 Thomson South-Western

VALUATION • Fundamental analysis is the study of a company’s accounting statements and future prospects to determine its value. • People can employ fundamental analysis to try to determine if a stock is undervalued, overvalued, or fairly valued. • The goal is to buy undervalued stock. © 2007 Thomson South-Western

is determined by in which")

Fundamental Analysis • The value of a stock (PV) is determined by in which r in the opportunity cost of capital and is the cash dividend received at time i. © 2007 Thomson South-Western

Fundamental Analysis • Cash dividend depends --demand for the firm’s product. --how much competition this firm faces. --how much capital it has in place. --whether its workers are unionized. --how loyal its customers are --what kinds of government regulations and taxes it faces. © 2007 Thomson South-Western

Fundamental Analysis • If the price of stock is less than the value, the stock is said to be undervalued. You should prefer undervalued stocks. • If the price of stock is said to be overvalued. • If the price and the value are equal, the stock to be fairly valued. © 2007 Thomson South-Western

Fundamental Analysis • In a competitive stock market, the stock is always fairly valued in equilibrium. • If interest rate falls, which signals the lower opportunity cost of capital, then the value of stock rises. Given the supply of stocks, the price of stock increases. © 2007 Thomson South-Western

is theory that asset")

The Efficient Markets Hypothesis • The efficient markets hypothesis(效率市場假 設) is theory that asset prices reflect all publicly available information about the value of an asset. • A market is informationally efficient when it reflects all available information about the value of an asset in a rational way. • If markets are efficient, the only thing an investor can do is buy a diversified portfolio. © 2007 Thomson South-Western

CASE STUDY: Random Walks and Index Funds • Random walk refers to the path of a variable whose changes are impossible to predict. • If markets are efficient, all stocks are fairly valued and no stock is more likely to appreciate than another. Thus stock prices follow a random walk. © 2007 Thomson South-Western

Market Irrationality • Is the stock market really rational? – Keynes suggested asset prices are driven by “animal spirits” of investors – Fed Chairman Alan Greenspan, in the 1990 s, questioned the “irrational exuberance” of the booming stock market • A person might be willing to pay more than a stock is worth today, if it is expected to increase in value tomorrow © 2007 Thomson South-Western

Summary • Because savings can earn interest, a sum of money today is more valuable than the same sum of money in the future. • A person can compare sums from different times using the concept of present value. • The present value of any future sum is the amount that would be needed today, given prevailing interest rates, to produce the future sum. © 2007 Thomson South-Western

Summary • Because of diminishing marginal utility, most people are risk averse. • Risk-averse people can reduce risk using insurance, through diversification, and by choosing a portfolio with lower risk and lower returns. © 2007 Thomson South-Western

Summary • The value of an asset, such as a share of stock, equals the present value of the cash flows the owner of the share will receive, including the stream of dividends and the final sale price. © 2007 Thomson South-Western

Summary • According to the efficient markets hypothesis, financial markets process available information rationally, so a stock price always equals the best estimate of the value of the underlying business. • Some economists question the efficient markets hypothesis, however, and believe that irrational psychological factors also influence asset prices. © 2007 Thomson South-Western

- Slides: 38