2007 CAS Ratemaking Seminar Market Cycle Management Blunt

2007 CAS Ratemaking Seminar Market Cycle Management: Blunt & Straightforward Mark Lyons Keynote Address Support Slides Unless otherwise noted, slides have been sourced by the presenter

PICC Your Battles Passion Intuition Courage Credibility

In 2005, Robert Hartwig asked this group: Who’s to Blame for Problem Pricing? 1. Actuaries 2. Senior Management of Company 3. Your Underwriting Department 4. Your Marketing Department 5. Regulators POGO: “We have met the enemy and he is us. ”

Insurance Cycle Terminology Expansion Competitive Phase Contraction Re-underwriting Phase Soft Market Hard Market ft Ha So ‘ 83 ’ 84 ‘ 85 ‘ 86 ‘ 87 *Includes Investment Income Peak rd Peak P O S I T I V E ‘ 88 ‘ 89 ‘ 90 ’ 98 ’ 99 ’ 00 ’ 01 Profit* ’ 02 ’ 03 Crunch Thomas Stamm, NAPSLO Collegiate Symposium, April 1, 2006 N E G A T I V E

Strength of Recent Hard Markets by NWP Growth [2006 to 2010 figures are Insurance Information Institute forecasts] 1975 -78 1984 -87 2001 -04 Current $ Real $ 2005: biggest real drop in premium since early 1980 s Better View than Calendar Year Combined Ratios or Operating Income Note: Shaded areas denote hard market periods A. M. Best, Insurance Information Institute

Many Sub-Cycles Occurring within ONE Underwriting Cycle Different cycle lengths, different rates of improvement and deterioration Some lines are heavily correlated; others only slightly

Impact of the Insurance Cycle on Transaction Variables and Underwriting Soft Market Ø Information ↓ Ø Coverage ↑ Ø Pricing ↓ Ø Attachment Points ↓ Ø Capacity/Limits ↑ Ø Underwriting ↓ Hard Market Ø Information ↑ Ø Coverage ↓ Ø Pricing ↑ Ø Attachment Points ↑ Ø Capacity/Limits ↓ Ø Underwriting ↑

The Complexity of Comparison Insurers Differ Strategically on their Approach towards: Ø Ø Ø Ø Target Markets Distribution Channels Cross-sell leverage Diversification strategy Rating agencies and regulators Market share versus Margins Philosophy Incentive Compensation Cost structures Use of reinsurance/capital markets Capital management strategy Wall Street; quarterly versus longer-term Shareholder expectations Other variables

1 –")

Top Ten Casualty Actuarial Stories of 2006 (per February 2007 Actuarial Review) 1 – Companies continue to sort out what ERM means 1 - Back end 2 – SEC questions reserve ranges/variability 2 - Back end 3 – Continued pressure on audit firms for more critical review of actuarial work 3 - Back end 4 – P/C Cat models continue to evolve 4 - Both 5 – Use of predictive modeling spreads to smaller personal lines carriers & small commercial lines 5 - Both; mostly internal 6 – Casualty softening market continues 6 - Front end 7 – Finite reinsurance probes continue 7 - Back end 8 – Risk transfer initiatives: bifurcation not likely to pass 8 - Back end 9 – Federal judge rules that flood exclusions do not apply to 2005 levee breaks 9 - Front end (full circle); partial impact though 10 – Hard market for property cat risks driven by changes in pricing models and capital requirements creates alternative capacity (cat bonds; side cars) 10 - Both; mostly internal

Executive Assurance “Proxy” Other Liability Claims Made Combined Ratios and ROE Source: Industry Annual Statements, Schedule P and Bernstein Research, August 2006

Tillinghast Annual Price/Limit Indices – D&O

Tillinghast Implied Price Per Million Changes –D&O

Marketplace: EA Competitor Results Source: Competitor Group 2005 Annual Statements – Schedule P

Marketplace: 6 EA Competitor Summary • Underwriting DOES matter • NONE of above Competitors would have made a 15% ROE from 1999 – 2002! • Redefine “SUCCESS”

PICC Your Battles Passion Intuition Courage Credibility

Examples of Business Value Added: PASSION, INTUITION, COURAGE and CREDIBILITY Transaction & LOB Actuaries * Make decisions! Make a difference! Be counted on to be a valuable contributor! * Variability is extremely important but you need to be in the shoes of the underwriter; align with time pressures; wide ranges provide little value * Follow up with UW to see what happened to the quote – show you care, are part of the team & deserve to be notified * Meet w/UW managers & supervisors to get a better “feel” and varying perspectives

* Read actual policy files – stay late –")

Transaction & LOB Actuaries (Continued) * Read actual policy files – stay late – learning doesn’t stop when the exams are completed * Insist on a full underwriting submission – NOT JUST LOSS EXPERIENCE * Don’t get “brokered” by an underwriter as to the information supplied * Know what stage of the Underwriting Cycle this Profit Center is in * Be “Universal Translators” (for the Star Trek fans in the audience)

Actuarial Managers/Actuarial Executives * Insist that your actuaries develop critical business skills * Minimize “not my job” syndrome * Consider putting your staff physically with UW units *Get involved in Risk Management endeavors * Where appropriate set up cross views by Business Division and Product within Actuarial *Reserving Actuaries need to meet with UW as well; don’t shut them off and only have Pricing Actuaries communicate

*Adopt effective Meeting Management behaviors that support cycle management *")

Actuarial Managers/Actuarial Executives (Continued) *Adopt effective Meeting Management behaviors that support cycle management * Managers need to provide referral points and escalation points to their actuarial staff no different than underwriting units do * It’s important to begin soft market management at the transaction level; being flexible on marginal deals and being strong and forceful on unprofitable deals. Your line actuaries need to know that they have your support if and when this is escalated over their heads to you. * Don’t become solely the “Premium Prevention Unit”

Actuarial Executives/Chief Actuaries • Stand up and be counted – THIS IS MOSTLY A PROMOTION TRANSITION ISSUE – You are the final stop. The buck stops here! • Need to maintain professional distance • Important to identify with management rather than your employees; you ARE management • Seek out Business Unit executives who themselves are (were) actuaries * One key objective of the Chief Actuary in a soft market should be to become UNPOPULAR

* Need to alert Senior Management, quantitatively, just how profitable")

Actuarial Executives/Chief Actuaries (Continued) * Need to alert Senior Management, quantitatively, just how profitable and unprofitable the subject lines of business have been historically over all points of the Cycle

Other Liability - Combined Ratios Average Combined Ratio 1995 -2005 = 116. 1 A. M. Best; Insurance Information Institute

![Marketplace: Casualty Competitor Results [as of December 31, 2005] Source: Competitor Group 2005 Annual](http://slidetodoc.com/presentation_image_h2/29980862de96cb280e6394d5a21abcef/image-23.jpg "Marketplace: Casualty Competitor Results [as of December 31, 2005] Source: Competitor Group 2005 Annual")

Marketplace: Casualty Competitor Results [as of December 31, 2005] Source: Competitor Group 2005 Annual Statements – Schedule P • The cycle will swing back • Insurers’ results will deteriorate Paradoxes: • All companies have the “best underwriters in the industry” • Underwriting makes a difference • All companies are “better than average”

![Excess Liability Market Capacity [in Billions] Capacity dropped 30% from 2000 to 2003 but](http://slidetodoc.com/presentation_image_h2/29980862de96cb280e6394d5a21abcef/image-24.jpg "Excess Liability Market Capacity [in Billions] Capacity dropped 30% from 2000 to 2003 but")

Excess Liability Market Capacity [in Billions] Capacity dropped 30% from 2000 to 2003 but has since increased by 10. 2% 2005 Limits of Liability Report, Marsh, Inc.

Marketplace: XS Casualty Industry Historical “Known” Loss/ALAE Ratios M A R Hard Market K E T C Y Hard Market C L E Arch, November 2, 2006

* Set up a clear basis with Senior Management (of")

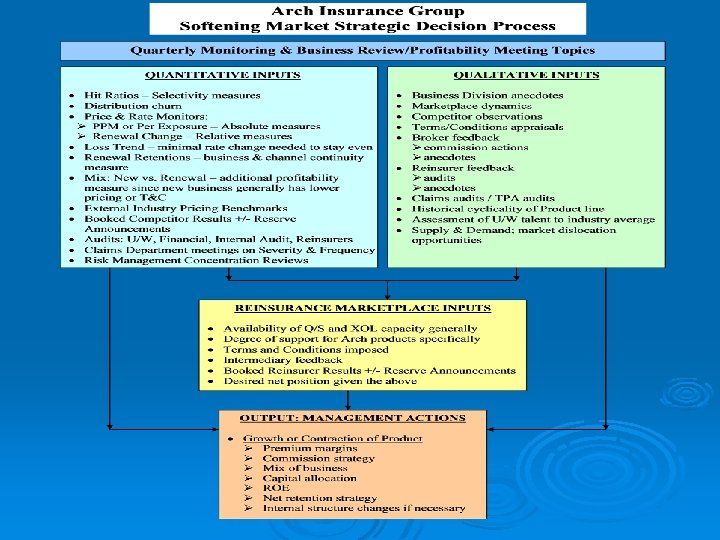

Actuarial Executives/Chief Actuaries (Continued) * Set up a clear basis with Senior Management (of which YOU are a part) as to how the business will be routinely viewed • Set up a clear set of analytics with Senior Management that leverages this data organization basis [LEADING INDICATORS]

LEADING INDICATORS o. Risk Selection - Hit Ratios o. Terms")

Actuarial Executives/Chief Actuaries (Continued) LEADING INDICATORS o. Risk Selection - Hit Ratios o. Terms and Conditions o. Price Monitors o. Changes in Portfolio Mix o. Renewal Retention o. Returns of the Business o. Commission Rates o. Update Returns Quarterly RETROSPECTIVELY AND PROSPECTIVELY FOR THE NEXT ROLLING TWO POLICY YEARS. Communicate graphically! o. New / Renewal Business Mix o. Admitted / Non-Admitted Mix o. Loss Trends

Leading Indicators: Risk Selection * Hit Ratios Need to be viewed as a time series & best if done on a Policy Quarter basis (not Calendar Quarter) Also meshes with other Leading Indicator’s data organization Critical to be done separately for New versus Renewal Business Renewal business should have higher hit ratios >New business, in a softening market, will be where most deterioration lives >New business will be “bought” either by price, T&C, expanded capacity, lower attachment points, expanded services, higher commissions Critical since most carriers measure renewal rate change only – underwriters know this & drive new business knowing that the measurements are delayed until first renewal – masks true state

* Quoted to Submitted – “triage”, risk appetite validation,")

Leading Indicators: Risk Selection (Continued) * Quoted to Submitted – “triage”, risk appetite validation, % deemed attractive enough to quote; can be indicative of changing risk selection standards, changing marketplace messages, better producer management efforts * Bound to Quoted – success rate given that it was quoted; can show changing pressures in the marketplace * Bound to Submitted – the product of the above two; ultimate measure of success-to-activity; can be a masked result similar to a pure premium trend versus that of frequency and severity separately * Sheer volumes of submission, quote, binder Staffing models Verification of Risk Appetite messages to marketplace Been largely ignored by actuaries – too simplistic?

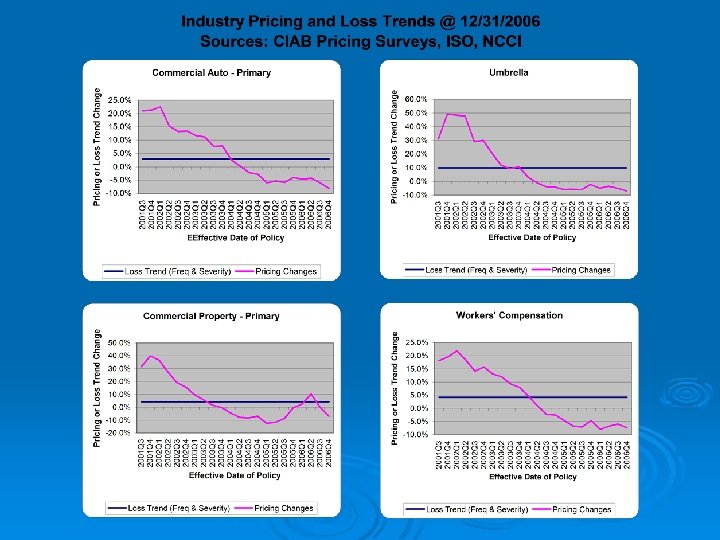

Leading Indicators: Price Monitors ØNeeds to be a continually updated time series ØNeed for Renewal business and New business for all material sectors of the book ØRenewal business (from basic to sophisticated) →Average Policy Premium →Price Per Million (PPM) →Price per unit of exposure →Effective Rate Change ¨Exposure, policy term, limits, attachment/deductibles, layer % ¨Coverage mix changes, endorsement grants, defense costs →Acknowledgement that some products cannot be accurately measured →Compare “apples to apples” with “normalized” and explain any differences →Know how much of the renewal book the monitors represent →Consider giving field underwriters online tools so they can more effectively choose between alternatives AND not get disadvantaged by brokers asking for multiple quote options

ØImportant to have multiple measures both internally and externally")

Leading Indicators: Price Monitors (Continued) ØImportant to have multiple measures both internally and externally produced (these are Renewal oriented) →CIAB – view of the producers via survey →Tillinghast – view of the carriers via defined survey →Advisen / RIMS – view of the customers via survey →Marketscout – view of a producer aggregator via data and survey ¨Know their gathering and sampling approaches ¨Reconcile external indications with internal indications ¨Use as probe with underwriting units

ØNew Business (from basic to sophisticated) →Expiring pricing/terms are")

Leading Indicators: Price Monitors (Continued) ØNew Business (from basic to sophisticated) →Expiring pricing/terms are suspect and not easily verified or subject to audit →Price per unit of exposure →PPM →New business relative to Renewal business in defined clusters ¨Establish benchmarks from bureau information, company manual rates, loss rating indications, credibility weighted – theoretically sound but practically difficult ØNeed to maintain BOTH premium change monitors & effective rate change monitors

Market. Scout Commercial Price Report www. Market. Scout. com

Average Premium Trend by Line of Business

www. Market. Scout. com

Average Commercial Rate Change by Line - CIAB Commercial accounts trended downward from early 2004 to mid-2005 though that trend moderated post-Katrina Council of Insurance Agents & Brokers

")

Marketplace: CIAB D&O Insights (EA)

Leading Indicators: Renewal Retention →Key component of ongoing profitability ¨More familiarity with renewal accounts ¨Cheaper to secure since most effort expended on gaining the account originally as New Business →Should be viewed on both a Renewal Premium basis and a Renewal Count basis →Be mindful of the “Count” mechanism; policy or Account based; policy retention can drop with Account retention staying flat due to changing layers or # policies per Account; consistency is the key →Further retention views by “Renewal Loss Ratio” can help in ascertaining whether the Renewal LR will be lower than the New Business LR →Can aid in commission strategy as softening market puts pressure on commissions

Leading Indicators: New /Renewal Mix →Fundamental that New Business and Renewal business should conceptually have the same Ultimate Loss Ratios (ULR) at ONLY the apex or nadir of that product’s cycle ¨Softening Markets – New Business should have higher LRs than renewals ¨Hardening Markets – New Business should have lower LRs than renewals →Knowing the New/Renewal mix is critical for profitability, reserving, and operating action →Can aid in determining strategy beyond “continuing to hit Plan” or overall grow/shrink decisions →Helps with relative mixture of New / Renewal growth or deceleration year-by-year SEPARATELY for new versus renewal →Demonstrated metrics and management here also permits more flexible and creative reinsurance arrangements

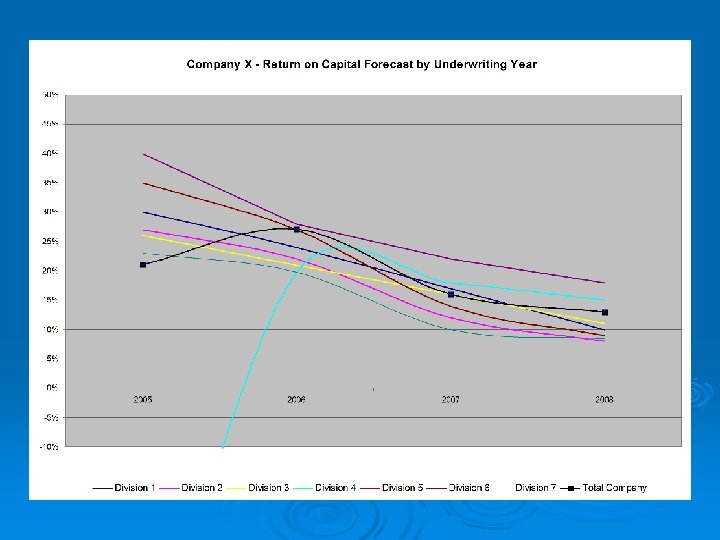

INSURANCE OPERATIONS – Market Cycle Management Graph of Economic Return by Policy Year (and Policy Quarter) N 35% P V or Maximize Writings 25% 15% Slow Writings R O 70% Increase Writings 5% Minimize New Business Writings E (5%) C O M 80% B I N 90% E D R 100% A T IO 110% Focus on Best of Renewals; need at least minimal market presence Policy Years Graph projections driven by estimated rate changes, loss cost trends, other “leading indicators”

Leading Indicators: Commissions o. Commission Rates ØCan be used within an overall economic review or can be integrated as part of the price monitor process; either way is fine as long as consistency is maintained and definitions are clear ØReflects the changing impact of the net true “cash received” perspective ØProducers attempt to increase commission rates at the worst possible time for insurers in order to keep THEIR top line growth flat ØInsurers then feel the double whammy of lower prices & increased “net” of producers ØOn the other side, Ceded side, pay attention to whether facultative cessions are being bound and coded net of ceding commission – big effect on ceded LRs

Leading Indicators: Admitted/Non-Admitted o. Admitted/Non-Admitted Mix ØComes down to who is responsible for collecting and submitting associated taxes →Admitted – needs to be charged within the quoted premium and remitted to authorities by insurer →Non-Admitted – is not charged within quoted premium and is collected and remitted to authorities by the Surplus Lines broker ØGenerally speaking, this is about a 3% rate cut, all else being equal, when renewing from a non-admitted basis to an admitted basis

Leading Indicators: Loss Trends ØFrequency ØSeverity ØPure Premium ØReconcile internal versus external data indications ØPrimary versus Leveraged Excess Trend ØImportant to communicate the incremental “ground” that is being lost each quarter ØAgain, can be included as part of the effective rate change or instead be within an overall economic analysis ØI prefer loss trend to be OUTSIDE the effective rate change calculation; this is more straightforward to communicate to Underwriting rather than being clouded/obfuscated by loss trend

Leading Indicators: Change in Portfolio Mix * Can indicate where your Business Units are having increased success and having trouble * It’s our & management’s job to determine whether we should “push down the gas accelerator” on some LOBs and “hit the brakes” on others * Reductions in some LOBs may be more a function of services (Claims, premium audit issues, deductible issues, collateral issues, risk engineering issues) and may not necessarily imply a market below Return thresholds * Forces another review of whether the emerging mix of business meeting economic and strategic objectives * Can alter your view of net retentions, reinsurance programs, upfront capacity usage, attachment points, and the extent of services rendered

Leading Indicators: Returns of the Business ØNPV Margin – % present value ‘profit/loss’ of present value premiums ØROE – same as NPV but related to allocated equity and includes interest income from equity ØROC – same as ROE but related to all capital allocated (eqty, debt, hybid) All three can co-exist but one needs to govern →Best done on an UW Year or Policy Year basis (i. e. “Decision Year”); cleanest implementation and communication approach →Accident Year can’t DIRECTLY relate to UW action ØCall for all insurer’s measures to reflect risk-free interest rates ONLY to stall any desires for cash flow underwriting (even capped rates if Treasuries go uncharacteristically high due to inflation)

Leading Indicators: Returns of the Business ØSenior Executive decision-making and communication can be separate from communication necessary for line-of-sight execution →Demand sophisticated Senior Management views for broad decision-making →Demand simpler Product Line and Region/Office goals, standards, and thresholds ¨Speak in clear traditional “line of sight” language; rate change, premium change, loss ratio, combined ratio

ØExtend the return measures reasonably into the")

Leading Indicators: Returns of the Business (continued) ØExtend the return measures reasonably into the future by Policy QTR →Let’s you see WHEN established return thresholds may be pierced; creates another measure for meetings and action – TIME →Update these reviews quarterly as Leading Indicator information & marketplace dynamics are clearer; make expense, reinsurance and capital management assumptions

Discussion of Priority Order of Individual Risk Softening Market Impacts 1 st - Risk Selection 2 nd - Terms and Conditions 3 rd - Attachment Points and Capacity Usage Can be others 4 th – Price What? ? ? Have you lost your mind? ? ? Measure each: Risk Selection – we’ve discussed – 1 st above Pricing – we’ve discussed – 4 th above Attachment Points & Capacity Usage – next slide Terms and Conditions – next slide

Attachment Points/Capacity (Limits)")

Discussion of Priority Order of Individual Risk Softening Market Impacts (Continued) Attachment Points/Capacity (Limits) – we’ve only implicitly discussed these within the effective rate change calculation ØNeeds a quarterly portfolio monitoring →Shifts of capacity upward can get “lost” if only reflected within effective rate change calculations →The appearance of effective rate change trade-offs when higher limits are provided is where the ILF curves are weakest (i. e. bigger blocks at higher attachment points) →Allows explicit questions to be put to underwriting executives →Important to know if XOL treaties are being utilized as intended →Underwriters often drop attachment points to ensure that their premium goals are met (i. e. “close your eyes and pray for miracles”) →If the measurement is for deductibles rather than attachment points, a measure of portfolio credit risk needs to be made as well

Terms and Conditions")

Discussion of Priority Order of Individual Risk Softening Market Impacts (Continued) Terms and Conditions – this represent coverage changes whether granted by form or endorsement; extremely hard to measure ØRecommend isolating KEY coverage areas and monitoring frequency of use ØCan be accomplished via sampling, automated binder issuance or policy issuance systems, reinsurer audit reports ØParticipate on Corporate UW audits and/or read their reports ØNeed to involve the Claims department and develop approximate Loss Ratio impacts of these key coverage grants or retractions ØSome measure should be included even if a SWAG – no mere clarifying footnote will overcome the lack of inclusion of form deterioration in projected LRs

Market Cycle Responsibilities of Senior/Executive Management Clear communication of WHAT CONSTITUTES SUCCESS Repeatedly communicate to the Company at large the importance of Cycle Management and that of Margins over Top Line Revenue Make Market Cycle Management a key component of UW Executive Performance Objectives Align Incentive Compensation directly with Underwriting return measures Corporately highlight and encourage both ends of the spectrum: Home Run Deals AND “Golden Glove” plays; must be true to the culture and behavior desired

Market Cycle Responsibilities of Senior/Executive Management Demonstrate action and not just words; communicate this alignment Make the difficult decisions that we’re paid to make Look for new markets, new methods of distribution, and new innovative products Develop tools for both seasoned and young underwriters to manage the Cycle Influence the structure of Board Committees

Additional Feedback Loops about the Market Cycle Scheduled Business Reviews / Profitability Reviews of all major UW units Business Unit UW Audits Corporate UW Audits Changes in UW Authority Delegation or UW referral thresholds Reinsurer Audit Reports Reinsurance Market approach to treaty renewals and facultative support Requested changes to UW aspects of IT systems Frequency of binder “halts” on approved u/w authority Internal Audit Reports Risk Management Reports Claims Audits / TPA Audits Monthly Executive Reports and Calls o. Profit Center Executives o. Regional Executives Claims Large Loss & Cause of Loss Meetings Trade magazines and studies

Other Career Options for Actuaries *Actuaries are fundamentally qualified for many functions within an insurance enterprise BUT learning never stops Caution: *May only see the 1/9 th of the iceberg above the water *Underwriters are sometimes accused of having just enough understanding of actuarial principles to be dangerous --- we don’t want to be accused of the same thing • Can be difficult to break into these other areas without either a Management Rotational Program or a mentor who helps guide you there

• Recommend collectively sitting down with your boss,")

Other Career Options for Actuaries (Continued) • Recommend collectively sitting down with your boss, H/R, and the “target” functional executive to plot a course towards achieving your goals; may involve additional coursework and/or shifting from your current “comfort zone”; perhaps some units would accept a “transitioning” • You CAN make it work • It may involve a “reality check”. For example, while you were passing exams, underwriting staff with the same years of experience you possess have been accumulating significant experience, trial-byerror knowledge, and possess many business contacts that are critical and difficult to amass quickly. Expect to Pay Your Dues!

* Innovation / Alternative Markets / Capital Markets")

Other Career Options for Actuaries (Continued) * Innovation / Alternative Markets / Capital Markets * Chief Financial Officer * Chief Information Officer * Chief Underwriting Officer * Chief Ceded Reinsurance Officer * Enterprise Risk Management Officer * Chief Risk Officer * Business Unit Executive * Chief Operating Officer * President and/or Chief Executive Officer

PICC Your Battles Passion Intuition Courage Credibility

- Slides: 60