2 Quality Time Theory of Constraints n Quality

, 시간(Time), 제약자원이론(Theory of Constraints)")

–구매시나 사용 중에 고객을 만 족시키기 위해 작성된 명세서에 따라")

– 제품이나 서비 스의 속성이 소비자의 필요성과 요구에")

과 실패(Failure) To accompany Cost Accounting 12 e, by Horngren/Datar/Foster. Copyright © 2006 by")

품질원가(COQ: cost of quality)란 저품질 제품을 생산함으로써 야기되는 원가 또 는")

4가지 범주별로 품질원가를 집계한 표 품질원가보고서 예: 유인물 참조 To accompany")

n 접수시간(receipt time) n 생산리드타임(manufacturing lead time)")

n 제약이론은 병목공정과 비병목공정들이 동시 에 있는 상황하에서 영업이익을 극대화하는 방법을")

- Slides: 30

전략적 원가관리 2 품질(Quality), 시간(Time), 제약자원이론(Theory of Constraints)

경쟁도구로서의 품질 n 품질(Quality) –구매시나 사용 중에 고객을 만 족시키기 위해 작성된 명세서에 따라 제품 또 는 서비스가 만들어지거나 실행되는 전체적인 특징이나 속성 the total features and characteristics of a product or a service made or performed according to specifications to satisfy customers at the time of purchase and during use n 품질은 원가를 절감시키고 고객을 만족시키는 데 초점을 둔다. To accompany Cost Accounting 12 e, by Horngren/Datar/Foster. Copyright © 2006 by Pearson Education. All rights reserved. 19 -2

품질의 2가지 측면 1. 설계품질(Design Quality) – 제품이나 서비 스의 속성이 소비자의 필요성과 요구에 얼마 나 일치하는지에 대한 것이다. refers to how closely the characteristics of a product or service meet the needs and wants of customers 2. 적합품질(Conformance Quality) – 제품 또 는 서비스의 성과가 그의 설계 및 제품명세서 와 일치하는 가에 대한 것이다. refers to the performance of a product or service relative to its design and product specifications To accompany Cost Accounting 12 e, by Horngren/Datar/Foster. Copyright © 2006 by Pearson Education. All rights reserved. 19 -4

품질(Quality)과 실패(Failure) To accompany Cost Accounting 12 e, by Horngren/Datar/Foster. Copyright © 2006 by Pearson Education. All rights reserved. 19 -5

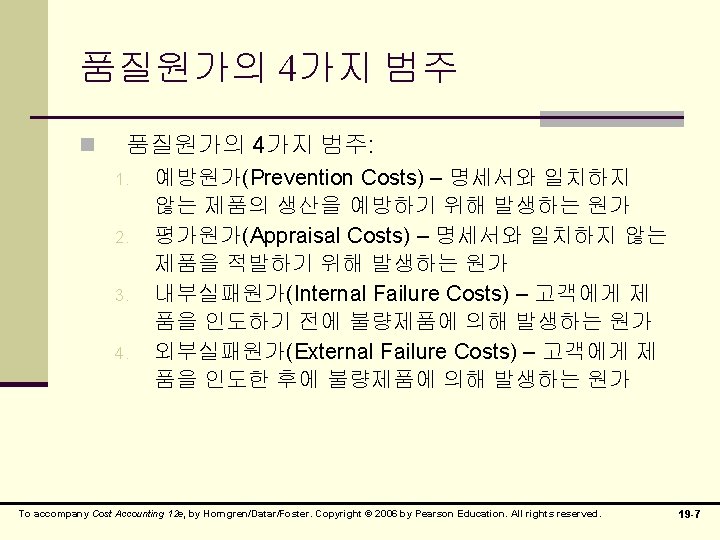

품질원가(Costs of Quality) 품질원가(COQ: cost of quality)란 저품질 제품을 생산함으로써 야기되는 원가 또 는 이를 예방하는 과정에서 발생하는 원가이다. To accompany Cost Accounting 12 e, by Horngren/Datar/Foster. Copyright © 2006 by Pearson Education. All rights reserved. 19 -6

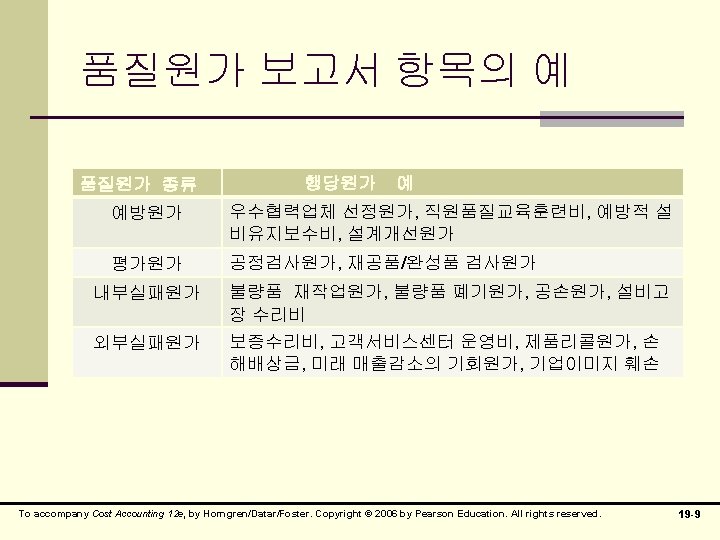

품질원가 보고서(COQ Report) 4가지 범주별로 품질원가를 집계한 표 품질원가보고서 예: 유인물 참조 To accompany Cost Accounting 12 e, by Horngren/Datar/Foster. Copyright © 2006 by Pearson Education. All rights reserved. 19 -8

비재무적인 품질 측정치 n 산출량에서 양품비율 n 산출량에서 불량품비율 n 반품율 n 적시배달율 n 종업원이직율 To accompany Cost Accounting 12 e, by Horngren/Datar/Foster. Copyright © 2006 by Pearson Education. All rights reserved. 19 -10

품질원가 예제 1 To accompany Cost Accounting 12 e, by Horngren/Datar/Foster. Copyright © 2006 by Pearson Education. All rights reserved. 19 -11

품질원가예제 2 To accompany Cost Accounting 12 e, by Horngren/Datar/Foster. Copyright © 2006 by Pearson Education. All rights reserved. 19 -12

품질원가예제 3 To accompany Cost Accounting 12 e, by Horngren/Datar/Foster. Copyright © 2006 by Pearson Education. All rights reserved. 19 -13

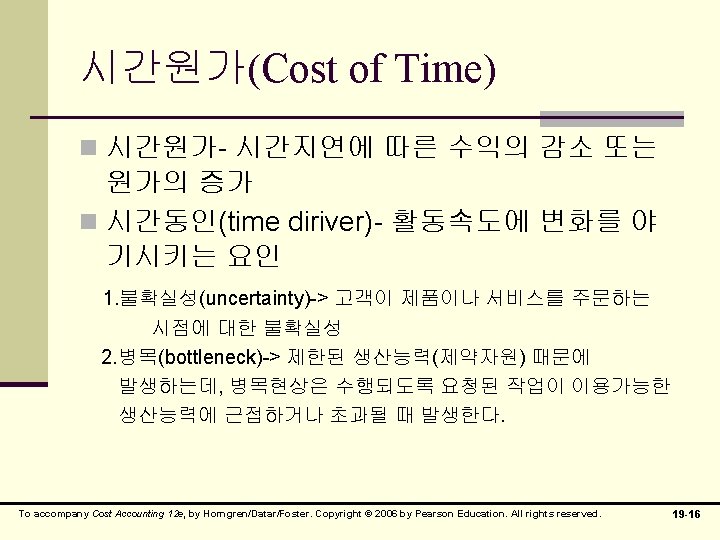

고객대응시간의 구성 n 고객대응시간의 구성(교재 p. 508참조) n 접수시간(receipt time) n 생산리드타임(manufacturing lead time) n 배달시간(delevery time) n 생산리드타임(생산소요시간) n 대기시간(waiting time) n 제조시간(manufacturing time) To accompany Cost Accounting 12 e, by Horngren/Datar/Foster. Copyright © 2006 by Pearson Education. All rights reserved. 19 -15

시간원가 예제 To accompany Cost Accounting 12 e, by Horngren/Datar/Foster. Copyright © 2006 by Pearson Education. All rights reserved. 19 -17

시간원가 예제 계속 To accompany Cost Accounting 12 e, by Horngren/Datar/Foster. Copyright © 2006 by Pearson Education. All rights reserved. 19 -18

시간원가 계속 To accompany Cost Accounting 12 e, by Horngren/Datar/Foster. Copyright © 2006 by Pearson Education. All rights reserved. 19 -19

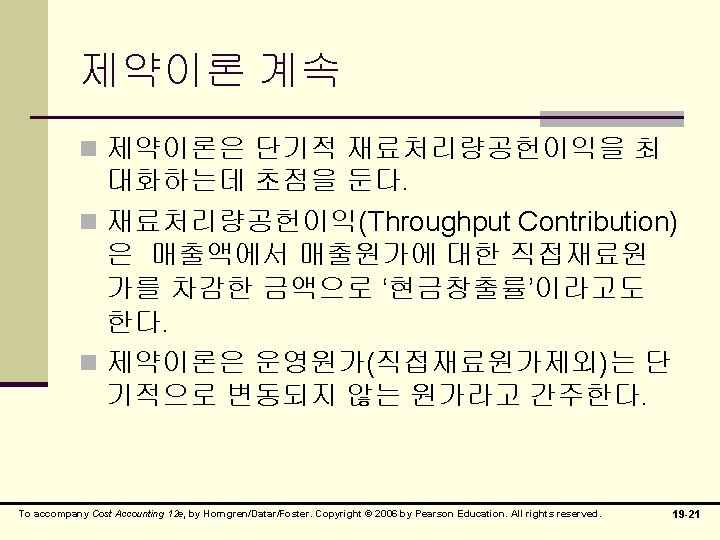

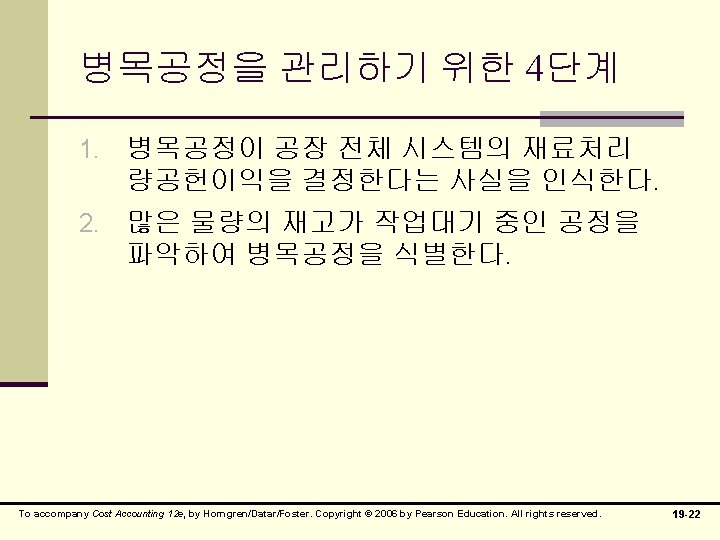

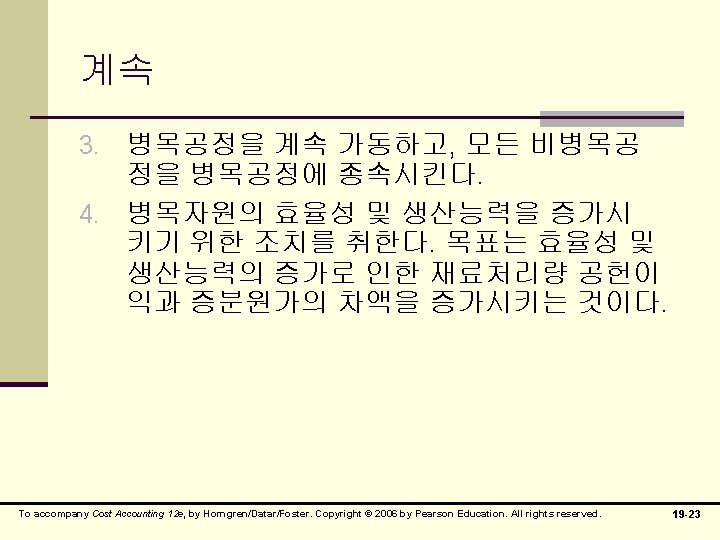

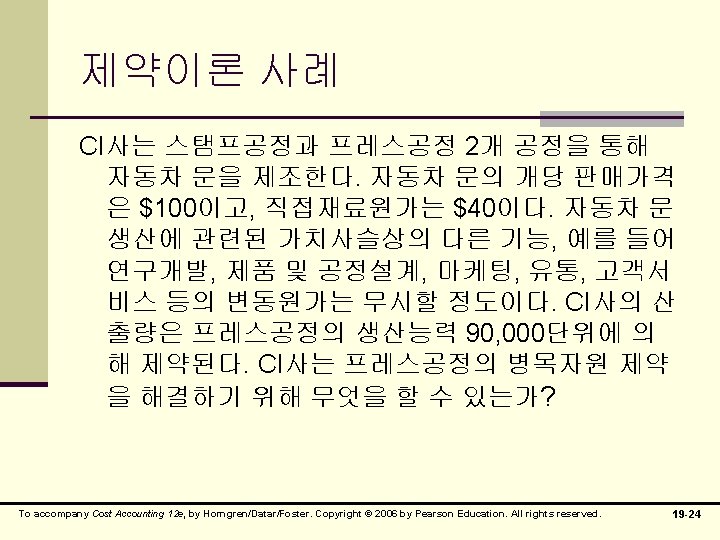

제약이론(Theory of Constraint) n 제약이론은 병목공정과 비병목공정들이 동시 에 있는 상황하에서 영업이익을 극대화하는 방법을 설명한다. Theory of Constraints (TOC) describes methods to maximize operating income when faced with some bottleneck and some nonbottleneck operations n 제약이론의 등장 엘리 골드렛 저 The Goal 이라는 소설 참고: 번역판 동양문고 The Goal(더골) To accompany Cost Accounting 12 e, by Horngren/Datar/Foster. Copyright © 2006 by Pearson Education. All rights reserved. 19 -20

제약자원 사례 계속 스탬프공정 프레스공정 20개 15개 120, 000 90, 000 연간생산판매량 90, 0000개 90, 000개 고정운영원가 $720, 000 $1, 080, 000 개당 $8 개당 $12 시간당 생산능력 연간 생산능력(6, 000시간) 단위당 고정운영원가 To accompany Cost Accounting 12 e, by Horngren/Datar/Foster. Copyright © 2006 by Pearson Education. All rights reserved. 19 -25