1 Uses of Accounting Information and the Financial

but managed")

•")

and")

")

- Slides: 65

1 Uses of Accounting Information and the Financial Statements

Accounting as an Information System OBJECTIVE 1: Define accounting and describe its role in making informed decisions, identify business goals and activities, and explain the importance of ethics in accounting.

Figure 1: Accounting as an Information System

Figure 2: Business Goals and Activities

Accounting as an Information System • Accounting is an information system that measures, processes, and communicates financial information. – Accounting is a link between business activities and decision makers. – Management must have a good understanding of accounting to set financial goals and make financial decisions. – Management must not only understand how accounting information is compiled and processed but also realize that accounting information is imperfect and should be interpreted with caution.

Accounting as an Information System • A business is an economic unit that aims to sell goods and services to customers at prices that will provide an adequate return to its owners. – Goals • Profitability—earning a sufficient return to maintain owner interest • Liquidity—having enough cash to pay debts as they come due

Accounting as an Information System – Activities • Operating—selling goods and services to customers; employing managers and workers; buying and producing goods and services; and paying taxes • Investing—spending the capital a company receives in productive ways that help it achieve its objectives • Financing—obtaining funds to begin operations and to continue operating

Accounting as an Information System – Performance measures • Performance measures relate to achieving goals and assessing the management of business activities. • Financial analysis is the evaluation and interpretation of the financial statements and related performance measures. • Performance measures must be crafted to motivate managers to make decisions that are in the best interest of the business.

Accounting as an Information System • Categories of accounting – Management accounting—accounting information for internal decision makers – Financial accounting—accounting information for external decision makers; reports are called financial statements.

Accounting as an Information System • Ways in which accounting information is processed – Bookkeeping is the mechanical and repetitive recordkeeping aspect of accounting. – Computerized accounting • Computerized accounting is useful for routine bookkeeping chores and complex accounting calculations. • Computerized information is only as useful as the data input into the system. – A management information system (MIS) consists of the interconnected subsystems that provide the information needed to run a business.

Accounting as an Information System • Ethical financial reporting – Ethics is a code of conduct that addresses whether actions are right or wrong. • Ethics in the preparation of financial reports is important because users of these reports must depend on the good faith of the people involved in their preparation. • The intentional preparation of misleading financial statements is called fraudulent financial reporting. • Fraudulent financial reporting can result from the distortion of records, falsified transactions, or the misapplication of various accounting principles. • The motivation for fraudulent financial reporting could be to inflate the perceived value of a business, meet stockholders’ and financial analysts’ expectations, obtain financing, or receive personal gain.

Accounting as an Information System – Congress passed the Sarbanes-Oxley Act in 2002 to regulate financial reporting in public corporations.

Decision Makers: The Users of Accounting Information OBJECTIVE 2: Identify the users of accounting information.

Figure 3: The Users of Accounting Information

Decision Makers: The Users of Accounting Information • Three major groups use accounting information. – Management (internal users) – Outsiders with a direct financial interest • Present or potential investor • Present or potential creditors – People, organizations, and agencies with an indirect financial interest • Tax authorities • Regulatory agencies – a Securities and Exchange Commission (SEC) • Other groups (labor unions, financial advisers, economic planners, etc. )

Decision Makers: The Users of Accounting Information • Government and not-for-profit organizations also use financial information.

Accounting Measurement OBJECTIVE 3: Explain the importance of business transactions, money measure, and separate entity.

Table 1: Examples of Foreign Exchange Rates

Accounting Measurement • Four questions must be answered to make an accounting measurement. – What is measured? – When should the measurement be made? – What value should be placed on what is measured? – How should what is measured be classified?

Accounting Measurement • A business transaction is an economic event that affects a business’s financial position. – It may involve an exchange of value (a purchase, sale, payment, collection, or loan). – Alternatively, it may involve a “nonexchange” of value (physical wear and tear or losses from fire, flood, explosion, and theft).

Accounting Measurement • The money measure concept states that a business transaction should be recorded in terms of money. – Transactions between countries must involve the translation of amounts of money using the appropriate exchange rate.

Accounting Measurement • In accounting, a business is treated as a separate entity from its owners, creditors, and customers.

The Forms of Business Organization OBJECTIVE 4: Describe the characteristics of a corporation.

Figure 4: Number and Receipts of U. S. Proprietorships, Partnerships, and Corporations

The Forms of Business Organization • There are three basic forms of business organization. – Sole proprietorship—one owner • The owner takes all of the profits or losses of the business • The owner also has unlimited liability – Partnership—two or more owners • In a partnership two or more owners share profits or losses based on a predetermined arrangement • Unlimited liability can be avoided by forming a limited liability partnership

The Forms of Business Organization – Corporation—owned by many owners (the stockholders) but managed by a board of directors • A corporation is a business unit chartered by the state (when articles of incorporation are filed) and considered a separate legal entity from its owners. • The liability of corporate stockholders is limited to their investment. – A share of stock is a unit of ownership in a corporation. – Common stock is the most universal form of stock.

The Forms of Business Organization • The board of directors sets corporate policy and declares dividends. • The authority to manage a corporation is given by the owners and board of directors to the corporate management. Corporate governance is the oversight of a corporation’s management; ethics is the oversight of the board of directors. • A provision of the Sarbanes-Oxley Act requires boards of directors to establish an audit committee to ensure that the board is objective in evaluating management performance.

Financial Position and the Accounting Equation OBJECTIVE 5: Define financial position, and state the accounting equation.

Figure 5: The Accounting Equation

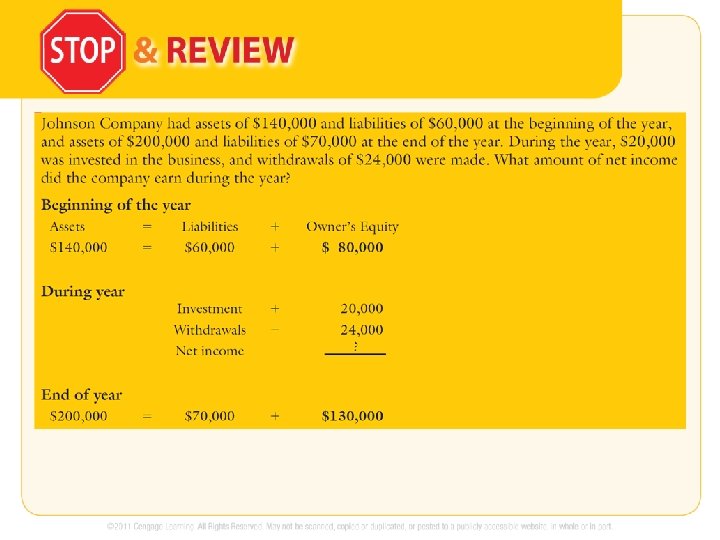

Financial Position and the Accounting Equation • A balance sheet discloses a business’s financial position by showing the relationship among assets, liabilities, and stockholders’ equity. • The accounting equation is Assets = Liabilities + Stockholders’ Equity. • Assets are a company’s economic resources, such as cash, receivables, inventory, and equipment. • Liabilities are the present obligations of a business, such as amounts owed to banks, suppliers, employees, and others.

Financial Position and the Accounting Equation • Stockholders’ equity represents the claims of the owner of a business to the net assets of the business. It is made up of the stockholders’ investment and all earnings not paid back to the stockholders in the form of dividends. • Net income is the excess of revenues over expenses; net loss is the excess of expenses over revenues.

Financial Statements OBJECTIVE 6: Identify the four basic financial statements.

Exhibit 1: Income Statement for Weiss Consultancy, Inc.

Exhibit 2: Statement of Retained Earnings for Weiss Consultancy, Inc.

Exhibit 3: Balance Sheet for Weiss Consultancy, Inc.

Exhibit 4: Statement of Cash Flows for Weiss Consultancy, Inc.

Exhibit 5: Income Statement, Statement of Retained Earnings, Balance Sheet, and Statement of Cash Flows for Weiss Consultancy

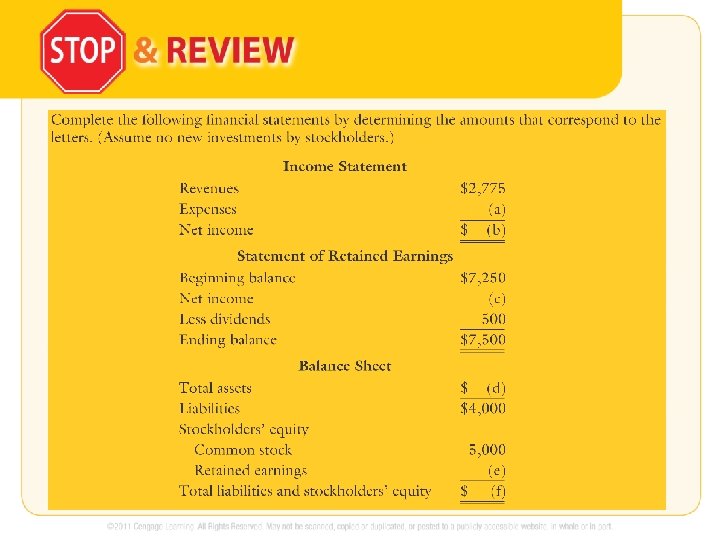

Financial Statements • There are four basic financial statements that are interrelated. – Income statement (also known as the statement of earnings or the profit and loss statement) • Shows revenues earned and expenses incurred for a period of time • Indicates profit or loss for an accounting period – Statement of Retained Earnings • Shows changes in retained earnings over a period of time

Financial Statements – Balance sheet (also known as the statement of financial position) • Usually prepared as of the last day of the accounting period to show the organization’s financial position (or status) as of that specific date • Reflects the accounting equation in its structure – Statement of cash flows • Presents significant financing, investing, and operating activities (cash-generating and cash-using activities) during a given period • Explains the reasons for changes in the organization’s cash during an accounting period

Generally Accepting Accounting Principles OBJECTIVE 7: Explain how generally accepted accounting principles (GAAP) and international financial reporting standards (IFRS) relate to financial statements and the independent CPA’s report, and identify the organizations that influence GAAP.

Table 2: Large International Certified Public Accounting Firms

Generally Accepting Accounting Principles • GAAP are the conventions, rules, and procedures that define acceptable accounting practice at a particular time. – CPAs perform independent audits of businesses’ financial statements. – An audit results in a professional opinion as to whether the financial statements are in accordance with GAAP.

Generally Accepting Accounting Principles • Organizations that issue accounting standards – The FASB is responsible for developing GAAP. – The IASB sets international accounting standards. • More than 40 international financial reporting standards (IFRS) have been approved.

Generally Accepting Accounting Principles • Other Organizations that influence GAAP – The AICPA influences GAAP through advisory committees. – The PCAOB is a governmental body created by the Sarbanes-Oxley Act to regulate the accounting profession. – The SEC sets its own standards for companies whose securities are listed on the stock exchanges. – The GASB was established to issue accounting standards for state and local governments. – IRS guidelines are established to collect taxes but play an influential role in the establishment of accounting practices.

Generally Accepting Accounting Principles • It is important for CPAs to conform to their code of professional ethics because the public relies on them for the following: – Integrity – Objectivity – Independence – Due care – Management accountants have a code of professional ethics that addresses competence, confidentiality, integrity, and objectivity.

Exhibit S-1: CVS’s Income Statements

Exhibit S-2: CVS’s Balance Sheets

Exhibit S-2: CVS’s Balance Sheets (cont’d)

Exhibit S-3: CVS’s Statements of Cash Flows

Exhibit S-3: CVS’s Statements of Cash Flows

Exhibit S-4: CVS’s Statements of Shareholders’ Equity

Exhibit S-4: CVS’s Statements of Shareholders’ Equity

Exhibit S-4: CVS’s Statements of Shareholders’ Equity

Figure S-1: Auditor’s Report for CVS Caremark Corporation

Supplement to Chapter 1: How to Read an Annual Report • Components of an Annual Reports – Letter to the Stockholders – Financial Highlights – Description of the Company – Management’s Discussion and Analysis

Supplement to Chapter 1: How to Read an Annual Report • Financial Statements – Formal financial statements appear in an annual report, usually in comparative form. – Consolidated financial statements are combined statements of affiliated companies. – A statement of stockholders’ equity often replaces the owner’s equity statement.

Supplement to Chapter 1: How to Read an Annual Report • Notes to the Financial Statements – A summary of significant accounting policies should accompany the financial statements. – Notes to the financial statements interpret portions of the financial statements. – Corporations frequently issue interim financial statements that cover less than a year.

Supplement to Chapter 1: How to Read an Annual Report • An annual report usually includes a report of management’s responsibilities as well as management’s discussion and analysis of operations.

Supplement to Chapter 1: How to Read an Annual Report • The independent auditors’ report accompanies the financial statements. – The first paragraph identifies the financial statements and responsibilities. – The scope section describes the extent of the examination. – The opinion section expresses the fairness of presentation of the financial statements. – The fourth paragraph identifies any new accounting standards adopted by the company – The fifth paragraph says the company’s internal controls are effective.