1 OIC PROPOSED METHODOLOGIES Before Fellow Actuaries regulation

รงทแลว 1. OIC PROPOSED METHODOLOGIES • Before Fellow Actuaries regulation in 2016 1 st phase 2 nd phase • Simplified stress test • 1 year prospective projection. • Choices of factors with magnitude will be provided. • Additional sensitivity or scenarios may be prescribed by OIC (such as pandemic events). • Require 1 additional reverse stress test. • 2016 onward • More complex stress test • To be further discussed later.

รงทแลว 2. OIC PROPOSED FACTORS 1. Interest rate, the following variations can be selected • 1. 1 parallel yield curve shift • 1. 2 change of yield curve slope • 1. 3 shift of curve and changing slope 2. Stock price, shock to levels only 3. Credit downgrading 4. Commodity price, shock to levels only 5. Exchange rate, shock to levels only

+ 5.")

รงทแลว 3. PRESCRIBED SCENARIO FOR STANDARD TEST Additional prescribed Scenario a: (a) + 5. 0 deaths per 1000 to mortality rates across all ages; (b) +100 hospitalisation claims incidence per 1000 to rates across all ages; (c) 0% increase in termination rates for health, term life, whole life and other predominantly protection policies, and 50% increase for investment linked, endowment and other pre-dominantly savings or investment policies; (d) 25% decrease in reinsurance recoverables; (e) 20% decrease in new business premiums; (f) 50% decrease for Singapore and overseas equities, 30% decrease for Singapore and overseas properties;

ตอ ( (g) +250 bps for Singapore")

รงทแลว 3. PRESCRIBED SCENARIO FOR STANDARD TEST )ตอ ( (g) +250 bps for Singapore corporate spreads, +200 bps for US corporate spreads, +140 bps for EU corporate spreads and +1680 bps for emerging market corporate spreads (where not stated, please use best estimate based on these parameters and provide justification); (h) -140 bps parallel yield curve shift for SGS yields.

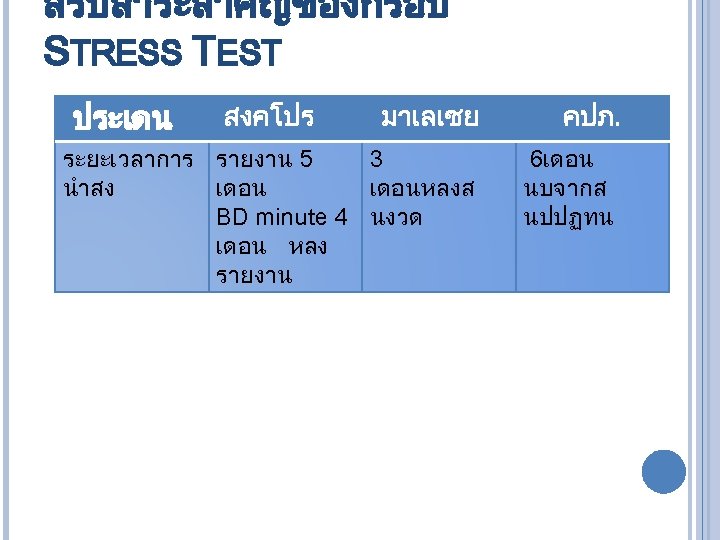

สรปสาระสำคญของกรอบ STRESS TEST ประเดน สงคโปร มาเลเซย Prescribed Self or Self + Self Select + Select+ (prescribed Stress-to- test) Failure Projection Base (3 At least 1 horizon yrs) year Short (1 yr) Medium (3 yrs) Point of Immediate End of คปภ. Prescribed + Self Select+ Stress-to. Failure Base (3 yrs) Short (1 yr) Immediate

สรปสาระสำคญของกรอบ STRESS TEST ประเดน สงคโปร มาเลเซย คปภ. ผรบผ ดชอบจดท ำรายงาน จำนวน test Appointed SM และ BD Actuary 3 Prescribe + at least 1 Self select + 1 Stress to failure 1 scenario รอบ 6 เดอน และอก 3 scenario รอบสนป 3 Prescribe + at least 1 Self select + 1 Stress to failure ลกษณะกา Scenario ทง Scenario

วธการ SHOCK และการรายงานผล End of Year T-1 / Beginning of Year T 1+ End of Year T 1+ Insurance Shocks Business Plan Investment Shocks End of Year T 1+ Report Immediate Impact End of Year T+3

สถานการณทใชในการทดสอบ Scenarios Base Scenario Short Term Scenari os Medium Term Scenari os Projection Period 3 -Years Point of Reporting N/A Immediate, Year 1 1 -Year 1 Prescribed* Self Select Stress to For Stress Failure Test phase 2 Prescribed* Self Select Stress to Failure 3 -Years Year 1 Immediate, Year 3

Short Term (1 -Yr Projection) Scenarios Prescribed: Macroeconomic Scenario")

รายละเอยดสถานการณ Medium Term (3 -Yr) Short Term (1 -Yr Projection) Scenarios Prescribed: Macroeconomic Scenario Prescribed: Financial Crisis Prescribed: Flu Pandemic At least one additional ST scenario Stress-to-Failure 2 e s ha Prescribed: Medium Term (with Low Interest) At least one additional MT scenario p t s Te For s s e Stress-to-Failure

รายละเอยดสถานการณ Prescribed#1: Macroeconomic Scenario § Purpose: To test relevant scenario applicable to financial sector § Remarks: Same scenario used in the industry wide banking stress test. Scenario is revised each year, depending on perceived risks to the financial sector § Shocks: Factors Sources Equity Prices SET Property Prices REIC*, กรมธนารกษ Sovereign Yield Curve BOT, Thai. BMA Credit Spreads BOT, Thai. BMA Exchange Rates BOT Change in NB Premiums Insurance Industry Termination Rate Insurance Industry • Real Estate Information Center ธนาคารอาคารสงเคราะห • จะมการหารอกบ BOT เพมเตมเรอง investment shock

รายละเอยดสถานการณ Prescribed#2: Financial Crisis Scenario § Purpose: To test the effects of a financial crisis § Remarks: Parameters calibrated largely to 2008 -2009 financial crisis. Consists of mainly investment shocks. § Shocks: Factors Sources Equity Prices SET Property Prices REIC, กรมธนารกษ Sovereign Yield Curve BOT, Thai. BMA Credit Spreads BOT, Thai. BMA Exchange Rates BOT Change in NB Premiums Insurance Industry Termination Rate Insurance Industry ยงไมกำหนดวาจะเปน Asian Financial Crisis หรอ Hamburger Crisis

รายละเอยดสถานการณ Prescribed#3: Pandemic Scenario § Purpose: To test the effects of a flu pandemic § Remarks: Combination of Macroeconomic Scenario and insurance pandemic shocks. Insurance shocks involved inputs from Ministry of Health. § Shocks: Factors Sources Equity Prices SET Property Prices REIC, กรมธนารกษ Sovereign Yield Curve BOT, Thai. BMA Credit Spreads BOT, Thai. BMA Exchange Rates BOT Mortality Rate Ministry of Health, Insurance Industry Hospitalisation Rate Ministry of Health, Insurance Industry Change in NB Premiums Insurance Industry Termination Rate Insurance Industry Reinsurance Recoverable Insurance Industry ยงไมไดกำหนดวาจะเปนเหตการณลกษณะใด เชน โรค SARS ระบาด

Scenario § Purpose: To test the combination")

รายละเอยดสถานการณ Stress to Failure (Reverse Stress Test) Scenario § Purpose: To test the combination of factors that can lead to the failure of the insurer, at the end of 1 year and 3 years § Remarks: Actuary to consider combination of factors that would most likely lead to insurer breaching its capital adequacy requirements, or MAS imposed requirement, whichever is higher. § Shocks: To be decided by insurer

BNM - FACTORS FOR SENSITIVITY ANALYSIS 1. Interest rate • • • Parallel yield curve shift Change of yield curve slope Shift of curve and changing slope Shocks to swap spreads Shocks to rates and volatilities 2. Equities • Shocks to levels and volatilities • Shocks to levels only • Shocks to volatilities only 3. Exchange rates • Shock to level only • Shocks to levels and volatilities 4. Credit 5. Commodities • Shocks to credit spreads • Shocks to levels and volatilities

6. Emerging markets 7. Others 8.")

BNM - FACTORS FOR SENSITIVITY ANALYSIS (CONT. ) 6. Emerging markets 7. Others 8. Insurance • Parallel yield curve shift • Shocks to interest rates and volatilities • Shocks to various volatilities • Shocks to mortality/ morbidity rates • Shocks to loss ratios • Significant increase in new business causing high new business strain • Significant change in valuation/ reserving basis

BNM - COMMON STRESS TEST SCENARIO Category Historical Equities - Black Monday 1987 - Asian financial crisis 1997 - Bursting of IT bubble 2000 - Terrorist attacks 2001 - Historical equity market decline Hypothetical - Hypothetical stock market crashes - New Economy scenarios - Risk arbitrage market boom - Equity exotics stress - Geopolitical unrest - Terrorist attack - Global economic outlook

Category Historical Interest Rate Products -")

BNM - COMMON STRESS TEST SCENARIO (CONT. ) Category Historical Interest Rate Products - Historical interest rate increases and decreases - Bond market sell-off 1994, 2003 - Asian financial crisis 1997 - LTCM 1998 - Russian devaluation 1998 - Japan 1998 (termination of Japanese MOF Bond Purchase operation) Hypothetical - Global tightening (focusing on increasing of short term and long term interest rate) - US tightening - Differential shocks to short rates - Spike in repo rates - Yield curve twist - US economy outlook - Global economic outlook - Increase in inflation

Category Credit Historical - Russian devaluation")

BNM - COMMON STRESS TEST SCENARIO (CONT. ) Category Credit Historical - Russian devaluation and default 1998 - Asian financial crisis 1997 - Terrorist attack 2001 - - Hypothetical Widening spread Emerging market economic outlook Euro area economic outlook Global economic outlook Natural disaster China change in currency arrangement US government sponsored

Category Others Historical - Gulf war")

BNM - COMMON STRESS TEST SCENARIO (CONT. ) Category Others Historical - Gulf war 1990 - Iraq war 2003 Insurance - 1918 Influenza Pandemic - Equitable Life 2000 - HIH 2001 - Terrorist attack 2001 - Tsunami 2004 - Confederation Life 1993 - Kidder, Peabody & Co 1994 - Barings bank 1995 Operational Hypothetical - Volatility disruption - Bank funding - Global economy - Pandemic (such as Bird Flu, SARS, etc. ) - Major natural disaster - Terrorist attack - Denial of reinsurance cover due to error in reinsurance contract wording - Mis-pricing of risk

INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS: ICAAP

ICAAP ของ MALAYSIA I N T E R N A L G O V E R N A N C E Responsibility of insurers Dialogue Internal Capital Adequacy Assessment Process (ICAAP) Comprehensive risk assessment ICAAP & Regular Updates of insurer’s risk profile and quality of risk management Conduct stress testing base on plausible adverse scenarios and incorporating insurer’s risk profile and business plan Individual target capital level Supervisory Review of ICAAP Supervisory review under the Risk-based Supervisory Framework (RBSF) Review of ICAAP: Offsite reviews, onsite reviews, discussions with board and senior management, discussion with external parties involved in ICAAP Overall assessment and conclusion Capital management plan Board range of supervisory measures Not Satisfactory Supervisory evaluation of on-going compliance with minimum standards and requirements

THANK YOU

- Slides: 38